Oil and Gas Fields in Norway

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Preparing for Carbon Pricing: Case Studies from Company Experience

TECHNICAL NOTE 9 | JANUARY 2015 Preparing for Carbon Pricing Case Studies from Company Experience: Royal Dutch Shell, Rio Tinto, and Pacific Gas and Electric Company Acknowledgments and Methodology This Technical Note was prepared for the PMR Secretariat by Janet Peace, Tim Juliani, Anthony Mansell, and Jason Ye (Center for Climate and Energy Solutions—C2ES), with input and supervision from Pierre Guigon and Sarah Moyer (PMR Secretariat). The note comprises case studies with three companies: Royal Dutch Shell, Rio Tinto, and Pacific Gas and Electric Company (PG&E). All three have operated in jurisdictions where carbon emissions are regulated. This note captures their experiences and lessons learned preparing for and operating under policies that price carbon emissions. The following information sources were used during the research for these case studies: 1. Interviews conducted between February and October 2014 with current and former employees who had first-hand knowledge of these companies’ activities related to preparing for and operating under carbon pricing regulation. 2. Publicly available resources, including corporate sustainability reports, annual reports, and Carbon Disclosure Project responses. 3. Internal company review of the draft case studies. 4. C2ES’s history of engagement with corporations on carbon pricing policies. Early insights from this research were presented at a business-government dialogue co-hosted by the PMR, the International Finance Corporation, and the Business-PMR of the International Emissions Trading Association (IETA) in Cologne, Germany, in May 2014. Feedback from that event has also been incorporated into the final version. We would like to acknowledge experts at Royal Dutch Shell, Rio Tinto, and Pacific Gas and Electric Company (PG&E)—among whom Laurel Green, David Hone, Sue Lacey and Neil Marshman—for their collaboration and for sharing insights during the preparation of the report. -

Mongstad Mongstad

North Sea Sweden Project Profile Norway Mongstad Mongstad The Mongstad facilities in western Norway have been in operation since the mid-1970’s and today encompass a refinery, a crude oil terminal, a technical development center and a wet gas processing factory. Throughout decades of expansion and modernization, ABB has kept pace with Mongstad’s dynamic process control and electrification requirements by providing advanced, flexible solutions designed to meet both current and future needs. A key link in the Norwegian oil supply chain OilUpstream & andGas Midstream Comprising Norway’s largest oil refinery, a high-traffic shipping port and storage facilities for around one-third of the crude oil produced by the Norwegian state, Mongstad is vital to the Norwegian oil industry. Keeping the oil flowing in and out of Mongstad in a safe, efficient and environmental manner takes state-of-the-art technology, including electric power and process Facts about Mongstad: automation systems from ABB. ABB is the leading supplier of integrated The oil refinery is the largest of its kind electrotechnical solutions to the oil and gas industry, and has provided in Norway with an annual capacity of innovative solutions to the Mongstad facilities for over 30 years. 10 million tons of crude. It is owned by By consistently providing reliable, high performance process control capabilities Mongstad Refining (79% StatoilHydro to Mongstad, the scope of ABB automation technology has steadily increased. and 21% Shell). Today, ABB automation technology at Mongstad encompasses: The crude oil terminal provides inter- 2,700 I/O boards with over 25,000 I/O´s 4 INFINET rings mediate storage of more than 1/3 of 150 redundant controllers distributed 13 HMI servers, 33 dual-VDU consoles over 17 equipment outstations all crude oil produced on the Norwegian 500 process graphics continental shelf. -

CCS from the Gas-Fired Power Station at Kårstø? a Commercial Analysis1

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Research Papers in Economics CCS from the gas-fired power station at Kårstø? A commercial analysis1 by Petter Osmundsen* and Magne Emhjellen** * University of Stavanger ** Petoro AS Summary The article presents a commercial investment analysis of the carbon capture project at the Kårstø gas processing plant in south-western Norway. We update an earlier analysis and critically review the methods used including those applied for cost estimating. Our conclusion is that carbon capture and storage (CCS) at Kårstø would be a very unprofitable climate measure with poor cost efficiency. It would require more than USD 1.7 billion2 in subsidies, or in excess of USD 133 million per year. That corresponds to a subsidy of roughly USD 0.1 per kilowatt-hour on the power station s electricity output. The cost per tonne of carbon emissions abated is about USD 333, which is about 20 times the international carbon emission allowance price and many times higher than alternative domestic climate measures. * Petter Osmundsen, department of industrial economics and risk management, University of Stavanger, NO-4036 Stavanger, Norway E-mail: [email protected], home page: http://www5.uis.no/kompetansekatalog/visCV.aspx?ID=08643&sprak=BOKMAL ** Magne Emhjellen, Petoro AS, P O Box 300 Sentrum, NO- 4002 Stavanger, Norway. E-mail: [email protected] 1 Thanks are due to Johan Gjærum, Per Ivar Gjærum, Kåre Petter Hagen and Knut Einar Rosendahl for constructive comments. We would also like to thank a number of specialists in business and the civil service for useful comments and proposals. -

Uncertainty Analysis of Emissions from the Statoil Mongstad Oil Refinery

25th International North Sea Flow Measurement Workshop, Oslo, Norway, 16-19 October 2007 Uncertainty analysis of emissions from the Statoil Mongstad oil refinery Kjell-Eivind Frøysa1, Anne Lise Hopland Vågenes2, Bernhard Sørli2 and Helge Jørgenvik2 1Christian Michelsen Research AS, Box 6031 Postterminalen, N-5892 Bergen, Norway. 2Statoil Mongstad, 5954 Mongstad, Norway ABSTRACT In new European and national legislations, there is increased focus on the reporting of the emmissions related to greenhouse gases from process plants. This includes reporting and documentation of uncertainty in the reported emmissions, in addition to specific uncertainty limits depending on the type of emission and type of measurement regime. In a process plant like the Statoil Mongstad oil raffinery, there may be a huge number of measurement points for mass flow. These measured mass flow rates have to be added in order to obtain the total emission for a given source. Typically, orifice plates are used at many of the measurement points. These orifice plate meters are ususally not equipped with individual densitometers. In stead, they are pressure and temperature corrected from a common upstream densitometer. This will give correllations between the individual flow meters. In the present paper, the flow meter set-up for Statoil Mongstad will be briefly addressed. thereafter, an uncertainty model suitable for the CO2 emission from the Statoil Mongstad oil raffinery will be presented, included a practically method for handling the partial correllation between the uncertainty of the various flow meters. This model will comply with the ISO 5168 for measurement uncertainty. Various uncertainty contributions will be reviewed, in order to work out an uncertainty budget for the specific emission sources. -

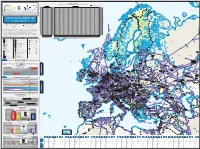

System Development Map 2019 / 2020 Presents Existing Infrastructure & Capacity from the Perspective of the Year 2020

7125/1-1 7124/3-1 SNØHVIT ASKELADD ALBATROSS 7122/6-1 7125/4-1 ALBATROSS S ASKELADD W GOLIAT 7128/4-1 Novaya Import & Transmission Capacity Zemlya 17 December 2020 (GWh/d) ALKE JAN MAYEN (Values submitted by TSO from Transparency Platform-the lowest value between the values submitted by cross border TSOs) Key DEg market area GASPOOL Den market area Net Connect Germany Barents Sea Import Capacities Cross-Border Capacities Hammerfest AZ DZ LNG LY NO RU TR AT BE BG CH CZ DEg DEn DK EE ES FI FR GR HR HU IE IT LT LU LV MD MK NL PL PT RO RS RU SE SI SK SM TR UA UK AT 0 AT 350 194 1.570 2.114 AT KILDIN N BE 477 488 965 BE 131 189 270 1.437 652 2.679 BE BG 577 577 BG 65 806 21 892 BG CH 0 CH 349 258 444 1.051 CH Pechora Sea CZ 0 CZ 2.306 400 2.706 CZ MURMAN DEg 511 2.973 3.484 DEg 129 335 34 330 932 1.760 DEg DEn 729 729 DEn 390 268 164 896 593 4 1.116 3.431 DEn MURMANSK DK 0 DK 101 23 124 DK GULYAYEV N PESCHANO-OZER EE 27 27 EE 10 168 10 EE PIRAZLOM Kolguyev POMOR ES 732 1.911 2.642 ES 165 80 245 ES Island Murmansk FI 220 220 FI 40 - FI FR 809 590 1.399 FR 850 100 609 224 1.783 FR GR 350 205 49 604 GR 118 118 GR BELUZEY HR 77 77 HR 77 54 131 HR Pomoriy SYSTEM DEVELOPMENT MAP HU 517 517 HU 153 49 50 129 517 381 HU Strait IE 0 IE 385 385 IE Kanin Peninsula IT 1.138 601 420 2.159 IT 1.150 640 291 22 2.103 IT TO TO LT 122 325 447 LT 65 65 LT 2019 / 2020 LU 0 LU 49 24 73 LU Kola Peninsula LV 63 63 LV 68 68 LV MD 0 MD 16 16 MD AASTA HANSTEEN Kandalaksha Avenue de Cortenbergh 100 Avenue de Cortenbergh 100 MK 0 MK 20 20 MK 1000 Brussels - BELGIUM 1000 Brussels - BELGIUM NL 418 963 1.381 NL 393 348 245 168 1.154 NL T +32 2 894 51 00 T +32 2 209 05 00 PL 158 1.336 1.494 PL 28 234 262 PL Twitter @ENTSOG Twitter @GIEBrussels PT 200 200 PT 144 144 PT [email protected] [email protected] RO 1.114 RO 148 77 RO www.entsog.eu www.gie.eu 1.114 225 RS 0 RS 174 142 316 RS The System Development Map 2019 / 2020 presents existing infrastructure & capacity from the perspective of the year 2020. -

Supreme Court of Norway

SUPREME COURT OF NORWAY On 28 June 2018, the Supreme Court gave judgment in HR-2018-1258-A (case no. 2017/1891), civil case, appeal against judgment, CapeOmega AS (Counsel Thomas G. Michelet) (Assisting counsel: Kyrre Eggen) Solveig Gas Norway AS Silex Gas Norway AS Infragas Norge AS (Counsel Jan B. Jansen Counsel Thomas K. Svensen) (Assisting counsel: Kyrre Eggen) v. The state represented by the Ministry of Petroleum and Energy (The Attorney-General represented Tolle Stabell and Christian Fredrik Michelet) (Assisting counsel: Håvard H. Holdø) VOTING : (1) Justice Bårdsen: The case concerns the validity of the Ministry of Petroleum and Energy's Regulations 26 June 2013 no. 792 relating to amendment of the Regulations relating to the stipulation of tariffs etc. for certain facilities (the Tariff Regulations), adopted under section 4-8 of the Petroleum Act, among others. 2 (2) The Tariff Regulations 20 December 2002 no. 1724 regulate the tariffs that third parties must pay for shipment of gas in the pipelines owned by the joint venture Gassled. The joint venture was established in 2003, and tariffs were stipulated in the Tariff Regulations for the various areas of the pipeline network. This network is the world’s biggest offshore system for transport and processing of gas, consisting of a number of gas pipelines on the seabed of the North Sea and the Norwegian Sea, some onshore processing plants in Norway and six receiving facilities in the UK, France, Belgium and Germany. The system is subject to licences from the Ministry of Petroleum and Energy pursuant to section 4-3 of the Petroleum Act. -

Management Meeting with Equinor Low Carbon Solutions 07.05.2020

European Gas Virtual 2021 Natural gas to blue hydrogen – Pipeline Transportation to Market and Decarbonisation in Multiple Sectors [email protected] .... Developing Clean Energy Solutions Large scale, emission-free production of hydrogen – HyPro-ZeroTM Existing technology in a new combination! Clean and affordable! Air separation unit (ASU) Purified hydrogen Oxygen (99.9-100%) Water / Gas Natural gas Reforming Hydrogen Hydrogen separation Shift by ATR (+GHR) (WGS) + CO2 Palladium-membrane* Cryogenic CO Capture Rate: 98-99% CO2 2 separation ready for transport of CO 2 and storage * Patented by HYDROGEN Mem-Tech AS (subsidiary) Competitive emission-free, blue hydrogen production Hydrogen production cost (incl. CO2 capture)*: 1.2 €/kgH2 + CO2 transport and storage cost: 0.3 - 0.5 €/kgH2 Total production cost**: 1.5 - 1.7 €/kgH2 * Natural gas price assumption: 0.12 €/SM3 ** Net cost, excl. financing, distribution of hydrogen etc. Significant global demand for new blue hydrogen production plants - and associated CCUS capacity 50 8 45 7.5 7 40 Carbon Capture 6.65 6 35 5.8 5 30 Biofuel 4.95 /YEAR 25 4 2 4.1 20 GTCO 3 3.25 15 2.4 2 NO OF NEW WORLD PLANTS/YR SCALE OF NO 10 Direct use and “E-fuel 1.7 1 5 1 0 0.5 0 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 Data from: “World scale plant”: 400.000 tH2/year IAE report; Energy Technology Perspective (Sept. 2020) Concawe report; biofuel and “E-fuel” Sept. 2020 Gas pipelines for efficient hydrogen transportation - Examples Existing gas pipeline New hydrogen pipeline New pipeline -

Information to Neighbours from Equinor Mongstad PDF 566 KB

Information to neighbours from Equinor Mongstad in compliance with the Major Accident Regulations The purpose of this brochure is to inform people regulation because flammable substances are outside the Mongstad process plant regarding handled at the facility. substances and situations that could represent a Based on this regulations a safety report, which deals hazard in the event of an undesirable incident. with the latest changes in the plant, will be prepared We will explain the plant’s emergency response for the public. The plant was updated in 2017. measures, and the precautions that should be taken if an undesirable incident, for example a gas leak or Other regulations that govern the activity as well as fire, should occur at the plant. In this manner, audit reports can be obtained upon inquiry to the Equinor wants to contribute to increased Petroleum Safety Authority (www.ptil.no) knowledge in connection with operation of the plant at Mongstad. Activities at Equinor Mongstad Equinor’s activity at Mongstad comprises Equinor Mongstad is one of several major operation of an oil refinery, a process plant for enterprises in Norway that handle chemicals and refining wet gas and condensate to propane, flammable substances, and is therefore subject to butane and naphtha, a crude oil terminal and a the “Regulations relating to measures to prevent cogeneration plant that is closely integrated with and limit the consequences of major accidents in the refinery. Equinor is also co-owner of the CO2 enterprises where hazardous chemicals occur Technology Centre Mongstad (TCM), which is (Major Accident Regulations)”. The facility is the world’s largest facility for testing and operated in accordance with this regulation. -

Europe, Middle East and North Africa Total 99 12 646 219

Europe, Middle East Europe,and North Africa Middle East andFact Sheet—March North 2021 Africa Fact Sheet—March 2021 ConocoPhillips has operated in Europe for more than 50 years, with significant developments in the 2020 Production Norwegian sector of the North Sea and in the Norwegian Sea. In Qatar, the company has interests in a producing field as well as liquefied natural gas production and export. The company also has Thousand interests in a concession in Libya. barrels of oil Operated assets in Europe include the Greater Ekofisk Area in Norway. The company also conducts 219 equivalent per day exploration activity in Norway. The company has leveraged its existing operations, infrastructure and basin expertise to create incremental growth projects in recent years, and development 2020 Proved Reserves* opportunities still exist in ConocoPhillips’ legacy areas. In Qatar, the Qatargas 3 joint venture continues providing stable production. Billion barrels of oil In Libya, the company has an interest in the Waha Concession in the Sirte Basin. Production equivalent operations in Libya and related oil exports have been periodically interrupted over the last several 0.6 years due to forced shutdowns of the Es Sider terminal. ConocoPhillips—Average Daily Net Production, 2020 Crude Oil NGL Natural Gas Total Area Interest Operator (MBD) (MBD) (MMCFD) (MBOED) Greater Ekofisk Area 30.7%-35.1% ConocoPhillips 46 2 39 55 Heidrun 24.0% Equinor 12 1 32 18 Aasta Hansteen 10.0% Equinor - - 82 14 Troll 1.6% Equinor 2 - 54 11 Visund 9.1% Equinor 2 1 40 10 Alvheim 20.0% Aker BP 8 - 13 10 Other Various Equinor 8 - 10 9 Norway Total 78 4 270 127 Qatargas 3 30.0% Qatargas Operating Co. -

Bringing Norwegian Gas to Europe

Melkøya Asterix Luva design by by design NORNE GAS colours TRANSPORT .no SYSTEM Zidane Skarv Bringing Norwegian gas Linnorm to Europe Njord www.gassco.no TAMPEN LINK TH LANGELED NOR Gjøa Valemon Gassco-operated systems at 2014 PIPELINE FROM TO LENGTH DIAMETER CAPACITY (Mscm/d) Haltenpipe Heidrun Tjeldbergodden 250 km 16” 7.0 mill Norne Gas Transport (NGTS) Norne Heidrun 128 km 16” 7.0 mill Åsgard Transport Åsgard Kårstø 707 km 42” 70.4 mill Kvitebjørn Pipeline Kvitebjørn Kollsnes 147 km 30” 26.5 mill Statpipe rich gas Statfjord Kårstø 308 km 30” 25.6 mill Statpipe Kårstø Draupner S 228 km 28” 21.1 mill Statpipe Draupner S Ekofisk Y 203 km 36” 44.4 mill Statpipe Heimdal Draupner S 155 km 36” 30.7 mill Zeepipe Sleipner Zeebrugge 813 km 40” 42,2 mill Zeepipe Sleipner Draupner S 38 km 30” 55.0 mill Zeepipe IIA Kollsnes Sleipner 299 km 40” 77.0 mill Zeepipe IIB Kollsnes Draupner E 301 km 40” 75.0 mill Europipe Draupner E Dornum/Emden 620 km 40” 45.7 mill Europipe II Kårstø Dornum 658 km 42” 71.9 mill Franpipe Draupner E Dunkerque 840 km 42” 54.8 mill H Norpipe Ekofisk Emden 440 km 36” 32.4 mill UT Vesterled Heimdal St Fergus 360 km 32” 38.9 mill Oseberg Gas Transport (OGT) Oseberg Heimdal 109 km 36” 35.0 mill Langeled North (LLN) Nyhamna Sleipner 627 km 42” 74.7 mill Langeled South (LLS) Sleipner Easington 543 km 44” 72.1 mill LANGELED SO Tampen Link Statfjord FLAGS 23 km 32” 25.0 mill Gjøa Gas Pipe Gjøa FLAGS 131 km 28” 17.8 mill Total 7928 km Onshore facilities: Zones and tarrifs Kårstø gas processing plant, Norway Gassled is divided into areas, with fixed tariffs for Kollsnes gas processing plant, Norway transport and/or processing within each of these. -

Bringing Gas to the Market

Bringing Gas to the Market Bringing Gas to the Market Gas Transit and Transmission Tariffs in Energy Charter Treaty Countries: Bringing Gas Regulatory Aspects and Tariff Methodologies Tariffs for the utilisation of gas transmission pipelines are an essential factor Gas Transit and Transmission Tariffs in Energy CharterTreaty Countries: Regulatory AspectsTariff and Methodologies to the Market determining the openness of international gas markets. The availability of interconnections and economically acceptable transportation costs are a condition for natural gas reaching consumer markets. With the dependence of major consuming countries on imported natural gas increasing – with the exception of countries that can rely on significant own reserves of unconventional gas – international trade in natural gas is expected to grow over the next decades. Common principles are necessary to enable such trade and to facilitate transit. Basic principles for transmission tariffs and some other aspects related to the utilisation of energy transport facilities have been elaborated in the Energy Charter. This study analyses methodologies and tariff principles for natural gas transmission Gas Transit and Transmission Tariffs in used in member countries of the Energy Charter Treaty, paying particular attention to developments in Europe, the Black Sea region and Central Asia. Common basic principles exist across this area, but concrete methodologies vary, as well as the Energy Charter Treaty Countries: choice of the market structure and the treatment of transit, in particular between the European Union on the one hand and some Eastern European and Central Asian countries on the other. The study compares the following aspects of regulatory regimes: Regulatory Aspects and - the role of the regulator, third-party access and unbundling; - the treatment of gas transit; Tariff Methodologies - methodologies to calculate capital and operational costs; - unit tariff methodologies. -

Environmental Statement for the Gjøa to FLAGS Pipeline

Environmental Statement for the Gjøa to FLAGS pipeline PL 153 Gjøa Vega Gas export Power from shore Oil export November 2006 PL 153 Gjøa Environmental Statement for the Gjøa to FLAGS pipeline November 2006 Standard Information Sheet Project name: Gjøa to FLAGS Gas Export Pipeline DTI Project reference: D/3325/2006 Type of project: Field Development Undertaker Name: Statoil ASA Address: Statoil ASA N-4035 Stavanger Norway Licensees/Owners: RWE Dea Norge AS 8% A/S Norske Shell 12% Statoil ASA 20% Petoro AS 30% Gaz de France Norge AS 30% Short description: Statoil are proposing to install a new 28” (ID) gas export pipeline between the Gjøa SEMI and FLAGS, as part of the Gjøa project. The new export pipeline will be connected to a new Gjøa semi-submersible platform via two 12” risers. The pipeline will be connected to FLAGS at the Tampen Link connection, via a new Hot Tap Tee-piece. All connections at Gjøa and at FLAGS will be stabilised using gravel and rock and will be fitted with protective structures. Dates Anticipated commencement May 2007 of works: Date and reference number Not applicable of any earlier Statement related to this project: Significant environmental Physical Presence of Vessels impacts identified: Anchoring of vessels during pipeline Installation Pipeline installation Physical presence of the pipeline and subsea structures Emissions from anodes Accidental spills of diesel Statement Prepared By: Statoil ASA BMT Cordah Limited, Aberdeen i PL 153 Gjøa Environmental Statement for the Gjøa to FLAGS pipeline November 2006 This