Europe and North Africa

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bakken Production Optimization Program Prospectus

Bakken Production Optimization Program BAKKEN PRODUCTION OPTIMIZATION PROGRAM 2.0 PROSPECTUS PROGRAM INTRODUCTION Led by the Energy & Environmental Research Center (EERC), the highly successful Bakken Production Optimization Program (BPOP), funded by its members and the North Dakota Industrial Commission, is continuing for the time frame of 2017–2020. The goal of this research program, BPOP 2.0, is to improve Bakken system oil recovery and reduce its environmental footprint. The results of the 3-year program will increase well productivity and the economic output of North Dakota’s oil and gas resources, decrease environmental impacts of wellsite operations, and reduce demand for infrastructure construction and maintenance. BPOP 1.0 PARTNERS A premier partnership program was recently completed which has been cited as an exemplary model by others nationwide. It has demonstrated that state lawmakers, state regulators, and industry can work together for positive results for shareholders and taxpayers alike. Phase I partners focused research on industry-driven challenges and opportunities. Continental Resources, Inc. ® Marathon Oil Corporation America’s Oil Champion Whiting Petroleum Corporation North Dakota Oil and Gas Research Program ConocoPhillips Company Nuverra Environmental Solutions Hitachi Hess Corporation Oasis Petroleum, Inc. SM Energy XTO Energy, Inc. BPOP 1.0 ACHIEVEMENTS (2013–2016) Continental’s Hawkinson Project Water Use and Handling Forecast Aimed at significantly increasing total production and A summary of trends in the Bakken, an estimation of production rates from North Dakota oil wells where oil future demand/disposal needs, an overview of treatment reserves of the second and third benches of the Three technologies, recycling/reuse considerations, and a Forks Formation, located just below the Bakken oil summary of implications for BPOP partners were created. -

Climate and Energy Benchmark in Oil and Gas Insights Report

Climate and Energy Benchmark in Oil and Gas Insights Report Partners XxxxContents Introduction 3 Five key findings 5 Key finding 1: Staying within 1.5°C means companies must 6 keep oil and gas in the ground Key finding 2: Smoke and mirrors: companies are deflecting 8 attention from their inaction and ineffective climate strategies Key finding 3: Greatest contributors to climate change show 11 limited recognition of emissions responsibility through targets and planning Key finding 4: Empty promises: companies’ capital 12 expenditure in low-carbon technologies not nearly enough Key finding 5:National oil companies: big emissions, 16 little transparency, virtually no accountability Ranking 19 Module Summaries 25 Module 1: Targets 25 Module 2: Material Investment 28 Module 3: Intangible Investment 31 Module 4: Sold Products 32 Module 5: Management 34 Module 6: Supplier Engagement 37 Module 7: Client Engagement 39 Module 8: Policy Engagement 41 Module 9: Business Model 43 CLIMATE AND ENERGY BENCHMARK IN OIL AND GAS - INSIGHTS REPORT 2 Introduction Our world needs a major decarbonisation and energy transformation to WBA’s Climate and Energy Benchmark measures and ranks the world’s prevent the climate crisis we’re facing and meet the Paris Agreement goal 100 most influential oil and gas companies on their low-carbon transition. of limiting global warming to 1.5°C. Without urgent climate action, we will The Oil and Gas Benchmark is the first comprehensive assessment experience more extreme weather events, rising sea levels and immense of companies in the oil and gas sector using the International Energy negative impacts on ecosystems. -

Statoil ASA Statoil Petroleum AS

Offering Circular A9.4.1.1 Statoil ASA (incorporated with limited liability in the Kingdom of Norway) Notes issued under the programme may be unconditionally and irrevocably guaranteed by Statoil Petroleum AS (incorporated with limited liability in the Kingdom of Norway) €20,000,000,000 Euro Medium Term Note Programme On 21 March 1997, Statoil ASA (the Issuer) entered into a Euro Medium Term Note Programme (the Programme) and issued an Offering Circular on that date describing the Programme. The Programme has been subsequently amended and updated. This Offering Circular supersedes any previous dated offering circulars. Any Notes (as defined below) issued under the Programme on or after the date of this Offering Circular are issued subject to the provisions described herein. This does not affect any Notes issued prior to the date hereof. Under this Programme, Statoil ASA may from time to time issue notes (the Notes) denominated in any currency agreed between the Issuer and the relevant Dealer (as defined below). The Notes may be issued in bearer form or in uncertificated book entry form (VPS Notes) settled through the Norwegian Central Securities Depositary, Verdipapirsentralen ASA (the VPS). The maximum aggregate nominal amount of all Notes from time to time outstanding will not exceed €20,000,000,000 (or its equivalent in other currencies calculated as described herein). The payments of all amounts due in respect of the Notes issued by the Issuer may be unconditionally and irrevocably guaranteed by Statoil A6.1 Petroleum AS (the Guarantor). The Notes may be issued on a continuing basis to one or more of the Dealers specified on page 6 and any additional Dealer appointed under the Programme from time to time, which appointment may be for a specific issue or on an ongoing basis (each a Dealer and together the Dealers). -

Oil and Gas Fields in Norway

This book is a work of reference which provides an easily understandable Oil and gas fields in n survey of all the areas, fields and installations on the Norwegian continental shelf. It also describes developments in these waters since the 1960s, Oil and gas fields including why Norway was able to become an oil nation, the role of government and the rapid technological progress made. In addition, the book serves as an industrial heritage plan for the oil in nOrway and gas industry. This provides the basis for prioritising offshore installations worth designating as national monuments and which should be documented. industrial heritage plan The book will help to raise awareness of the oil industry as industrial heritage and the management of these assets. Harald Tønnesen (b 1947) is curator of the O Norwegian Petroleum Museum. rway rway With an engineering degree from the University of Newcastle-upon- Tyne, he has broad experience in the petroleum industry. He began his career at Robertson Radio i Elektro before moving to ndustrial Rogaland Research, and was head of research at Esso Norge AS before joining the museum. h eritage plan Gunleiv Hadland (b 1971) is a researcher at the Norwegian Petroleum Museum. He has an MA, majoring in history, from the University of Bergen and wrote his thesis on hydropower ????????? development and nature conser- Photo: Øyvind Hagen/Statoil vation. He has earlier worked on projects for the Norwegian Museum of Science and Technology, the ????????? Norwegian Water Resources and Photo: Øyvind Hagen/Statoil Energy Directorate (NVE) and others. 55 tHe ekoFIsk AReA The Ekofisk area lies in 70-75 metres of water at the southern end of Norway’s North Sea sector, about 280 kilometres south-west of Stavanger. -

Whiting Petroleum Corporation and Our Ability to Grow MMBOE: One Million BOE

Whiting Petroleum Corporation ANNUAL REPORT 8 0 0 2 NATU RAL HUM+AN Resources ABOUT THE COVER Having assembled a solid foundation of quality assets through acquisition, we are now more focused on organic drilling activity and on the development of previously acquired properties. We believe that our experienced team of management, engineering and geoscience professionals is generating superior results as evidenced by our reserves and production growth in the Bakken formation in North CONTENTS Dakota and our two CO 2 enhanced oil recovery projects. Corporate Profile 1 From our Bakken play in North Dakota, our average net daily production jumped 516% to 14,165 BOE in December 2008 Financial and Operations Summary 2 from 2,300 BOE in December 2007. We also completed Letter to the Shareholders 4 our first two infill wells in the Sanish field, which we believe Drilling and Operations Overview 7 adds a total of 78 potential infill well locations. Also of note was our first Three Forks horizontal well completion in the Northern Rockies 8 Sanish field. Production and pressure data from this well are Central Rockies 10 being analyzed to determine the viability of developing the Three Forks in the Sanish field. EOR Projects 12 Board of Directors 14 At our two EOR projects, our average net daily production Annual Report on Form 10-K 15 from the Postle and North Ward Estes fields increased 26% to 13,700 BOE in December 2008 from 10,900 BOE in Corporate Investor Information Inside back cover December 2007. We expect production from both EOR projects to continue to increase as 2009 progresses. -

Ranking Operator by Gas 1999

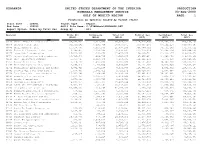

PDRANKOP UNITED STATES DEPARTMENT OF THE INTERIOR PRODUCTION MINERALS MANAGEMENT SERVICE 03-AUG-2000 GULF OF MEXICO REGION PAGE: 1 Production by Operator Ranked by Volume (4120) Start Date : 199901 Report Type : Report End Date : 199912 ASCII File Name: C:\TIMSWork\PDRANKOP.DAT Report Option: Order by Total Gas Group By : All Operator Crude Oil Condensate Total Oil Natural Gas Casinghead Total Gas (BBLS) (BBLS) (BBLS) (MCF) (MCF) (MCF) 02140 Shell Deepwater Production Inc. 85,672,533 9,411,739 95,084,272 245,810,790 213,353,317 459,164,107 00078 Chevron U.S.A. Inc. 50,545,262 6,292,709 56,837,971 353,305,284 87,102,210 440,407,494 00689 Shell Offshore Inc. 15,438,780 6,417,500 21,856,280 300,789,310 30,544,202 331,333,512 00003 Union Oil Company of California 6,344,477 2,334,388 8,678,865 253,150,024 15,694,524 268,844,548 00276 Exxon Mobil Corporation 16,626,406 1,243,669 17,870,075 168,330,701 51,313,377 219,644,078 00771 Texaco Exploration and Production Inc 10,785,640 1,908,736 12,694,376 187,865,901 31,396,468 219,262,369 00114 Amoco Production Company 1,853,723 2,410,438 4,264,161 182,121,250 1,573,019 183,694,269 01855 Vastar Resources, Inc. 7,750,730 1,435,200 9,185,930 114,537,982 34,747,390 149,285,372 01364 Newfield Exploration Company 4,368,048 2,162,039 6,530,087 132,431,383 10,633,590 143,064,973 02332 PennzEnergy Exploration and Production 5,772,629 3,160,145 8,932,774 118,870,351 9,572,802 128,443,153 00491 Coastal Oil & Gas Corporation 1,038,860 1,682,412 2,721,272 119,028,667 2,687,097 121,715,764 02219 Kerr-McGee Oil & Gas Corporation 13,307,198 1,569,590 14,876,788 102,681,653 14,762,861 117,444,514 00185 Samedan Oil Corporation 2,673,355 2,285,513 4,958,868 104,938,141 7,424,318 112,362,459 00105 Apache Corporation 6,574,028 1,660,755 8,234,783 92,723,545 12,356,983 105,080,528 00059 Amerada Hess Corporation 9,001,254 7,825,335 16,826,589 76,749,036 23,640,310 100,389,346 00540 MOBIL OIL EXPLORATION & PRODUCING SOUT 8,967,820 1,142,597 10,110,417 88,168,916 11,699,694 99,868,610 01680 BP Exploration & Oil Inc. -

New Document

ANNUAL STATEMENT OF RESERVES 2016 AKER BP ASA Annual Statement of Reserves 2016 Annual Statement of Reserves 2016 Table of Contents 1 Classification of Reserves and Contingent Resources 1 2 Reserves, Developed and Non-Developed 2 3 Description of Reserves 5 3.1 Producing Assets 5 3.1.1 Alvheim and Viper/Kobra (PL036, Pl088BS, PL203) 5 3.1.2 Vilje (PL036D) 7 3.1.3 Volund (PL150) 8 3.1.4 Bøyla (PL340) 9 3.1.5 Atla (PL102C) 11 3.1.6 Jette (PL027D), PL169C, PL504) 11 3.1.7 Jotun (PL027B, PL203B) 12 3.1.8 Varg (PL038) 12 3.1.9 Ivar Aasen Unit and Hanz (Pl001B, PL028B, PL242, PL338BS, PL457) 13 3.1.10 Valhall (PL006B, PL033B) 15 3.1.11 Hod (PL033) 16 3.1.12 Ula (PL019) 17 3.1.13 Tambar (PL065) 19 3.1.14 Tambar East (PL065, PL300, PL019B) 20 3.1.15 Skarv/Snadd (PL262, PL159, PL212B, PL212) 21 3.2 Development Projects 22 3.2.1 Johan Sverdrup (PL265, PL501, PL502; Pl501B) 22 3.2.2 Gina Krog (PL029B) 25 3.2.3 Oda (PL405) 26 4 Contingent Resources 28 5 Management’s Discussion and Analysis 34 Annual Statement of Reserves 2016 List of Figures 1.1 SPE reserves and recourses classification systen .................................................................... 1 3.1 Alvheim and Viper/Kobra Location Map.................................................................................... 5 3.2 Vilje location map ...................................................................................................................... 7 3.3 Volund location map.................................................................................................................. 8 3.4 Bøyla location map.................................................................................................................. 10 3.5 Ivar Aasen Unit and Hanz location map.................................................................................. 13 3.6 Valhall and Hod location map................................................................................................. -

Two Studies on Roman London. Part B: Population Decline and Ritual Landscapes in Antonine London

Two Studies on Roman London. Part B: population decline and ritual landscapes in Antonine London In this paper I turn my attention to the changes that took place in London in the mid to late second century. Until recently the prevailing orthodoxy amongst students of Roman London was that the settlement suffered a major population decline in this period. Recent excavations have shown that not all properties were blighted by abandonment or neglect, and this has encouraged some to suggest that the evidence for decline may have been exaggerated.1 Here I wish to restate the case for a significant decline in housing density in the period circa AD 160, but also draw attention to evidence for this being a period of increased investment in the architecture of religion and ceremony. New discoveries of temple complexes have considerably improved our ability to describe London’s evolving ritual landscape. This evidence allows for the speculative reconstruction of the main processional routes through the city. It also shows that the main investment in ceremonial architecture took place at the very time that London’s population was entering a period of rapid decline. We are therefore faced with two puzzling developments: why were parts of London emptied of houses in the middle second century, and why was this contraction accompanied by increased spending on religious architecture? This apparent contradiction merits detailed consideration. The causes of the changes of this period have been much debated, with most emphasis given to the economic and political factors that reduced London’s importance in late antiquity. These arguments remain valid, but here I wish to return to the suggestion that the Antonine plague, also known as the plague of Galen, may have been instrumental in setting London on its new trajectory.2 The possible demographic and economic consequences of this plague have been much debated in the pages of this journal, with a conservative view of its impact generally prevailing. -

Lyle Tompsen, Student Number 28001102, Masters Dissertation

Lyle Tompsen, Student Number 28001102, Masters Dissertation The Mari Lwyd and the Horse Queen: Palimpsests of Ancient ideas A dissertation submitted to the University of Wales Trinity Saint David in fulfilment of the requirements for the Degree of Master of Arts Celtic Studies 2012 Lyle Tompsen 1 Lyle Tompsen, Student Number 28001102, Masters Dissertation Abstract The idea of a horse as a deity of the land, sovereignty and fertility can be seen in many cultures with Indo-European roots. The earliest and most complete reference to this deity can be seen in Vedic texts from 1500 BCE. Documentary evidence in rock art, and sixth century BCE Tartessian inscriptions demonstrate that the ancient Celtic world saw this deity of the land as a Horse Queen that ruled the land and granted fertility. Evidence suggests that she could grant sovereignty rights to humans by uniting with them (literally or symbolically), through ingestion, or intercourse. The Horse Queen is represented, or alluded to in such divergent areas as Bronze Age English hill figures, Celtic coinage, Roman horse deities, mediaeval and modern Celtic masked traditions. Even modern Welsh traditions, such as the Mari Lwyd, infer her existence and confirm the value of her symbolism in the modern world. 2 Lyle Tompsen, Student Number 28001102, Masters Dissertation Table of Contents List of definitions: ............................................................................................................ 8 Introduction .................................................................................................................. -

Drilling the Monterey Shale

A New California Oil Boom? Drilling the Monterey Shale By Robert Collier December 2013 Table of Contents Table of Contents 2 Part 1: Distracted by Fracking? 3 Part 2: The Most dangerous chemical you’ve never heard of 6 Part 3: The Climate conundrum 9 Part 4: Monterey Shale: Twice as polluting as Keystone XL? 13 Part 5: Is California really like North Dakota? 18 Part 6: Keeping the story straight: industry reports at odds on California oil 24 Notes 27 Page 2 | Drilling the Monterey Shale Part 1: Distracted by Fracking? Over the past few years, the United States has found the more likely candidate for tapping the Monterey itself in the midst of a major boom in oil and gas Shale: A technique, already widely in use in the oil production. Rapid expansion in the use of a drilling industry, known as “acidizing.” technique called hydraulic fracturing, or “fracking,” has opened up previously unreachable pockets of oil It’s not widely discussed in publicly, but for some and gas, and returned the U.S. to its historic position time oil companies have found acidizing more as a major global producer of these fossil fuels. effective in the Monterey Shale than fracking. And it seems the boom may be coming to Acidizing typically involves the injection of high California. Once a leading producer of oil in the U.S., volumes of hydrofluoric acid, a powerful solvent, California’s production has fallen off dramatically (abbreviated as “HF”) into the oil well to dissolve over the years as oil fields age and are depleted. -

EXXONMOBIL DEVELOPMENT § COMPANY; and EXXONMOBIL § OIL CORPORATION, § § Plaintiffs, § § V

Case 3:17-cv-01930-B Document 110 Filed 12/31/19 Page 1 of 35 PageID <pageID> UNITED STATES DISTRICT COURT NORTHERN DISTRICT OF TEXAS DALLAS DIVISION EXXON MOBIL CORPORATION; § EXXONMOBIL DEVELOPMENT § COMPANY; and EXXONMOBIL § OIL CORPORATION, § § Plaintiffs, § § v. § CIVIL ACTION NO. 3:17-CV-1930-B § STEVEN MNUCHIN, in his official § capacity as Secretary of the U.S. § Department of the Treasury; § ANDREA M. GACKI, in her official § capacity as the Director of the U.S. § Department of the Treasury’s Office § of Foreign Assets Control; and the U.S. § DEPARTMENT OF THE TREASURY’S § OFFICE OF FOREIGN ASSETS § CONTROL, § § Defendants. § MEMORANDUM OPINION AND ORDER Before the Court is Plaintiffs Exxon Mobil Corporation, ExxonMobil Development Company, and ExxonMobil Oil Corporation’s Motion for Summary Judgment (Doc. 92), as well as Defendants Steven Mnuchin, Andrea Gacki, and the Office of Foreign Assets Control’s Cross-Motion for Summary Judgment (Doc. 95). The parties dispute whether the Office of Foreign Assets Control’s imposition of a two-million-dollar fine upon Plaintiffs for alleged violations of Ukraine-related sanctions regulations was lawful. Because the Court concludes that Plaintiffs lacked fair notice that their conduct was prohibited, the Court GRANTS Plaintiffs’ motion (Doc. 92) and DENIES Defendants’ cross-motion (Doc. 95). Further, the Court VACATES the Office of Foreign Asset - 1 - Case 3:17-cv-01930-B Document 110 Filed 12/31/19 Page 2 of 35 PageID <pageID> Control’s Penalty Notice. I. BACKGROUND1 This is an administrative case prompting the Court to determine which party receives the benefit of having its cake and eating it, too—the regulating agency that failed to clarify, or the regulated party that failed to ask. -

Annual Report on Form 20-F ANNUAL REPORT /2012 Annual Report on Form 20-F

ANNUAL REPORT /2012 Annual Report on Form 20-F ANNUAL REPORT /2012 Annual Report on Form 20-F The Annual Report on Form 20-F is our SEC filing for the fiscal year ended December 31, 2012, as submitted to the US Securities and Exchange Commission. The complete edition of our Annual Report is available online at www.statoil.com/2012 © Statoil 2013 STATOIL ASA BOX 8500 NO-4035 STAVANGER NORWAY TELEPHONE: +47 51 99 00 00 www.statoil.com Cover photo: Ole Jørgen Bratland Annual report on Form 20-F Cover Page 1 1 Introduction 3 1.1 About the report 3 1.2 Key figures and highlights 4 2 Strategy and market overview 5 2.1 Our business environment 5 2.1.1 Market overview 5 2.1.2 Oil prices and refining margins 6 2.1.3 Natural gas prices 6 2.2 Our corporate strategy 7 2.3 Our technology 9 2.4 Group outlook 10 3 Business overview 11 3.1 Our history 11 3.2 Our business 12 3.3 Our competitive position 12 3.4 Corporate structure 13 3.5 Development and Production Norway (DPN) 14 3.5.1 DPN overview 14 3.5.2 Fields in production on the NCS 15 3.5.2.1 Operations North 17 3.5.2.2 Operations North Sea West 18 3.5.2.3 Operations North Sea East 19 3.5.2.4 Operations South 19 3.5.2.5 Partner-operated fields 20 3.5.3 Exploration on the NCS 20 3.5.4 Fields under development on the NCS 22 3.5.5 Decommissioning on the NCS 23 3.6 Development and Production International (DPI) 24 3.6.1 DPI overview 24 3.6.2 International production 25 3.6.2.1 North America 27 3.6.2.2 South America and sub-Saharan Africa 28 3.6.2.3 Middle East and North Africa 29 3.6.2.4 Europe and Asia