Base Prospectus Banca Del

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

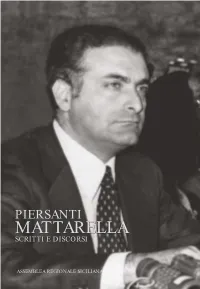

Piersanti Mattarella

Piersanti Mattarella Piersanti Mattarella nacque a Castellammare del Golfo il 24 maggio 1935. Secondogenito di Bernardo Mattarella, uomo politico della Democrazia Cristiana e fratello di Sergio, 12° Presidente della Repubblica Italiana. Piersanti si trasferì a Roma con la famiglia nel 1948. Studiò al San Leone Magno, retto dai Fratelli maristi, e militò nell’Azione cattolica mostrandosi battagliero sostenitore della dottrina sociale della Chiesa che si andava affermando. Si laureò a pieni voti in Giurisprudenza alla Sapienza con una tesi in economia politica, sui problemi dell’integrazione economica europea. Tornò in Sicilia nel 1958 per sposarsi. Divenne assistente ordinario di diritto privato all'Università di Palermo. Ebbe due figli: Bernardo e Maria. Entrò nella Dc tra il 1962 e il 1963 e nel novembre del 1964 si candidò nella relativa lista alle elezioni comunali di Palermo ottenendo più di undicimila preferenze, divenendo consigliere comunale nel pieno dello scandalo del “Sacco di Palermo”. Erano, infatti, gli anni della crisi della Dc in Sicilia, c’era una spaccatura, si stavano affermando Lima e Ciancimino e si preparava il tempo in cui una colata di cemento avrebbe spazzato via le ville liberty di Palermo. Nel 1967 entrò nell’Assemblea Regionale. In politica adottò uno stile tutto suo: parlò di trasparenza, proponendo di ridurre gli incarichi (taglio degli assessorati da dodici ad otto e delle commissioni legislative da sette a cinque e per l'ufficio di presidenza la nomina di soli due vice, un segretario ed un questore) e battendosi per la rotazione delle persone nei centri di potere con dei limiti temporali, in modo da evitare il radicarsi di consorterie pericolose. -

Who Was Partisan Canepa?

GLORY TO OUR COMRADE ANTONIO CANEPA and to the partisans of the Volunteer Army for the Independence of Sicily! NO to the hypocritical tricoloured Liberation Day and to the tainted May Day celebrations! World War II (1939-1945). After the facts were cleaned out by the ideologies, our very own Memory was "purified", what is left of the second WORLD WAR is a lethal confrontation between competing Powers, which turned into the division of the World in two parts, of a divided Europe, a divided Germany, a divided Berlin. And in the long-lasting withdrawal of the old colonialist European Empires, that had "won" the war, triggering India's independence, and most of all the foundation of Mao's People's Republic of China. In July 1943 - with Operation Husky - the "Allies" (supported by an efficient Resistance against Nazi- fascism) occupy Sicily. It was the beginning of the end of a Regime, but, as we will see, it was not what the Sicilian Partisans had fought for. The 24th October 1943, beyond the temporary AMGOT (Allied Military Government for Occupied Territories), was also the birthdate of Washington's "SICILY REGION 1" in the Mediterranean, which remains like an "unsaid" under this sky that is populated by foreign planes, assassin drones, dysfunctional saints and a G7 on a tourist trip. This Sicily is a fought-over island, played like a geopolitical card by Rome, the real mafia capital, and its strategic relation with the AmeriKan friend. A treasure island reduced to Europe's poorhouse, with its habitants being forced to emigrate. -

Banca Del Mezzogiorno – Mediocredito Centrale S.P.A

Banca del Mezzogiorno – MedioCredito Centrale S.p.A. Inaugural Social Bond Executive Summary • Strategic Government-linked entity promoting investments in the South of Italy • Unique business model focused on development support • Strong financials within the Italian banking system • Rated Ba1 by Moody’s / BBB- by S&P • Inaugural Social Bond Transaction 2 Content 1 MedioCredito Centrale ("MCC") Overview 2 Financial Overview 3 Social Framework 4 Transaction Overview MCC Overview Group Profile and Mission MCC at a Glance MedioCredito Centrale S.p.A.: a Bank 100% owned by Italian State through Invitalia MCC Evolution and Overview Board of Directors • Established in 1952 as a public entity, its mission was Chairman Massimiliano CESARE focused on delivering public finance and supporting the expansion of Italian companies overseas. In 2011, following CEO Bernardo MATTARELLA the MEF developing program for the southern Italy, its corporate name was changed to Banca del Mezzogiorno- Directors Pasquale AMBROGIO MedioCredito Centrale Gabriella FORTE • Since August 2017 the Bank has been owned by Invitalia Leonarda SANSONE S.p.A. (formerly Sviluppo Italia S.p.A.) and regulated by the Bank of Italy with a full banking licence • No branch network (Banca di II Livello), MCC operates under Shareholding Structure cooperation agreements with the main Italian banking groups • Total employees as of 31/12/2018, 283: 14 managers, 163 senior officers and 106 employees (and 9 trainees) Board of Statutory Auditors Chairman Paolo PALOMBELLI Standing Auditors Carlo FEROCINO 100% Marcella GALVANI 100% Alternative Auditors Roberto MICOLITTI Sofia PATERNOSTRO 5 Key Stages of MCC’s Development A more than 60 years long history of success, with focus on South of Italy SMEs development since 2011 1952 1994 1999 2007 2011 2017 TODAY Poste Italiane acquires 100% of Law no. -

Piersanti Mattarella Scritti E Discorsi

PIERSANTI MATTARELLA SCRITTI E DISCORSI ASSEMBLEA REGIONALE SICILIANA PIERSANTI MATTARELLA nato a Castellammare del Golfo (Tp) il 24 maggio 1935, assassinato a Palermo il 6 gennaio 1980, gior- no dell’Epifania. Ha ricoperto importanti incarichi diocesani, regiona- li e nazionali nella gioventù di azione cattolica, della cui presidenza ha fatto parte per cinque anni. Consigliere comunale di Palermo dal 1964 al 1967. Componente della direzione regionale, del Consiglio nazionale e della direzione centrale della Democrazia cristiana. Deputato regionale eletto per la D.C. nel collegio di Palermo nella sesta (11 giugno 1967), settima (13 giugno 1971) e ottava legislatura (20 giugno 1976). Nella sesta legislatura è stato componente delle Commissioni legislative permanenti per gli affari interni e per la pubblica istruzione, della giunta di bilancio, della Commissione per il regolamento interno, della Commissione speciale per la riforma burocratica e della Commissione speciale per la rifor- ma urbanistica. Nella settima legislatura ha ricoperto ininterrotta- mente la carica di Assessore alla Presidenza, delegato al bilancio, carica nella quale è stato riconfermato nel primo governo della ottava legislatura. Dal 16 marzo 1978 era Presidente della Regione. ASSEMBLEA REGIONALE SICILIANA XIII LEGISLATURA SCRITTI E DISCORSI di PIERSANTI MATTARELLA VOLUME SECONDO 2 QUADERNI DEL SERVIZIO STUDI LEGISLATIVI DELL’A.R.S. – NUOVA SERIE – SCRITTI E DISCORSI DI PIERSANTI MATTARELLA Introduzione di LEOPOLDO ELIA VOLUME SECONDO ASSEMBLEA REGIONALE SICILIANA Il ruolo delle regioni meridionali per una nuova politica economica dello Stato (*) Palermo, 31 gennaio 1971 Il problema principale da affrontare e risolvere al fine di pervenire ad una nuova politica meridionalistica è eminentemente quello politico della creazione di una forza di pressione nel Sud capace di controbilanciare le spinte e le sollecitazioni che sull’apparato politico-buro- cratico riesce ad esercitare la struttura socio-finanziaria del Nord. -

Il 4 Novembre a Vittorio Veneto (A Cura Di Ido Da Ros)

Il 4 Novembre a Vittorio Veneto (a cura di Ido Da Ros) Presentiamo una sorta di albo d’oro degli oratori ufficiali che si sono succeduti ai microfoni di Piazza del Popolo per la celebrazione del 4 Novembre, anniversario della Vittoria e giornata dell’Unità nazionale e delle Forze armate. In testa alla graduatoria – a partire dal secondo dopoguerra - troviamo l’on. Tina Anselmi e il colonnello Lorenzo Cadeddu, entrambi con quattro presenze, seguiti dagli onorevoli Carlo Bernini e Marino Corder e dal generale comandante il 1° Fod Giovanni Ridinò con tre presenze; lo stesso numero che può vantare Bernardo Mattarella, padre dell’attuale Presidente della Repubblica. Sono sei i Capi di Stato ad aver presieduto la cerimonia nella nostra città: Giovanni Gronchi, Giuseppe Saragat, Sandro Pertini, Francesco Cossiga, Oscar Luigi Scalfaro e Giorgio Napolitano. Tre, invece, i Presidenti del Consiglio: Vittorio Emanuele Orlando (nel 1919), Amintore Fanfani e, per due volte consecutive, Aldo Moro. La prima celebrazione del 4 Novembre risale al 1919 e vide appunto la presenza del Capo del Governo Vittorio Emanuele Orlando e dell’ex Presidente del Consiglio, Luigi Luzzatti. Nel periodo compreso tra le due guerre mondiali la Festa fu in parte “oscurata” anche a Vittorio Veneto dalla vicinanza cronologica dell’anniversario della Marcia su Roma (28 ottobre), che il regime celebrava in grande stile. Meritano comunque di essere ricordate le celebrazioni del Decennale e del Ventennale, svoltesi alla presenza rispettivamente del re Vittorio Emanuele III (1928) e del principe Umberto di Savoia (1938). Dopo la tragica parentesi della Seconda Guerra Mondiale, le celebrazioni ripresero in quest’ordine: 1948: Maurizio Lazzaro di Castiglioni, generale di Corpo d’Armata e Francesco Franceschini, deputato vittoriese. -

I GOVERNI ITALIANI ( 25 Luglio 1943 - 6 Agosto 1970)

Settembre- Ottobre 1970 756. Governi 1943-1970 I GOVERNI ITALIANI ( 25 luglio 1943 - 6 agosto 1970) DALLA CADUTA DEL FASCISMO ALLA ASSEMBLEA COSTITUENTE 0 I• MINISTERO BADOGLIO (25 Luglio 1943 - 17 aprile 1944) ( ) Pr esid. Consiglio: PIETRO BADOGLIO - Affari Ester i: RAFFAELE GUA RIGLIA - PIETRO BADOGLIO - Interno: UMBERTO RICCI - VITO R.EALE - Africa italiana: MELCHIADE GABBA - PIETRO BADOGLIO - Giustizia: GAETANO AZZARITI - ETTORE CASATI - F inanze: DOMENI CO BARTOLINI - GUIDO JUNG - Guerra: ANTONIO SORICE - TADDEO ORLANDO -Marina: RAFFAELE DE COURTEN -Aeronautica: RENATO SANDALLI - Educazione Nazionale: LEONARDO SEVERI - GIOVANNI CUOMO - Lavori Pubblici: ANTONIO ROMANO- RAFFAELE DE CARO - Agricoltura e Foreste: ALESSANDRO BRIZI - FALCONE LUCIFERO - Co mtmicazioni: FEDERICO AMOROSO - TOMMASO SICILIANI - I ndustr ia, Commercio e Lavoro: LEOPOLDO PICCARDI - EPICARMO CORBINO - Cultura popolare: CARLO GALLI - GIOVANNI CUOMO - Scambi e Valute: GIOVANNI ACANFORA- GUIDO JUNG - Produzione bellica: CARLO FA V AGROSSA - Alto commissario per la Sardegna: PINNA - Alto commissa rio per la Sicilia: FRANCESCO MUSOTTO - Alto commissario per l'epum zlone nazionale: TITO ZANffiONI - Commissario generale per l'alimenta zione: CAMll;RA. n• MINISTERO BADOGLIO (22 aprile 1944 - 18 giugno 1944) P·resid. Consiglio: PIETRO BADOGLIO - Ministri senza portafoglio: BE NEDETTO CROCE, CARLO SFORZA, GIULIO RODINO, PIETRO MANCI NI, PALMIRO TOGLIATTI - Esteri: PIETRO BADOGLIO - Interno: SAL VATORE ALDISIO • Africa italiana: PIETRO BADOGLIO - Giustizia : VINCENZO ARAN·GIO-RUIZ - Finanze: QUINTO QUINTIERI - Guer ra : TADDEO ORLANDO - Marina: RAFFAELE DE COURTEN - Aeronautica: RENATO SANDALLI - Pubblica Istruzione: ADOLFO OMODEO - Lavori Pubblici: ALBERTO TARCHIANI - Agricoltura e Foreste: FAUSTO GUL LO - Comunicazioni: FRANCESCO CERABONA - I ndustria e Commercio: ATTILIO DI NAPOLI - ALto commissario per le sanzioni contro iL fasci smo: CARLO SFORZA - Alto commissario per l'assistenza morale e mate riale dei profughi di guerra: TITO ZANIBONI. -

16 Luglio 1953 Il Presidente Della Repubblica Riceve in Udienza Alle

16 luglio 1953 Il Presidente della Repubblica riceve in udienza alle ore : 9,50 - l'On. Sen. Dr. Umberto ZANOTTI BIANCO (alla Palazzina) 10,45 - l'On. Dr. Alcide DE GASPERI, Presidente del Consiglio dei Ministri : per prestare giuramento a norma dell'Art. 93 della Costituzione, (nello studio); 11,00 - l'On. Avv. Attilio PICCIONI, Vice Presidente del Consiglio dei Mini= stri e i sottoindicati nuovi Ministri: per la prestazione del giura= mento a norma dell'Art. 93 della Costituzione (nella Sala della Madonna della Seggiola) : - On. Prof. Amintore FANFANI, Ministro dell'Interno - On. Prof. Guido GONELLA, Ministro di Grazia e Giustizia - On. Prof. Giuseppe PELLA, Ministro del Bilancio e ad interim per il Tesoro - On. Avv. Ezio VANONI, Ministro delle Finanze - On. Prof. Giuseppe CODACCI PISANELLI, Ministro della Difesa - On. Prof. Giuseppe BETTIOL, Ministro della Pubblica Istruzione - On. Avv. Giuseppe SPATARO, Ministro dei Lavori Pubblici - On. Avv. Rocco SALOMONE, Ministro dell'Agricoltura e Foreste - On. Prof. Giuseppe TOGNI, Ministro dei Trasporti - On. Avv. Umberto MERLIN, Ministro delle Poste e Telecomunicazioni - On. Avv. Silvio GAVA, Ministro dell'Industria e Commercio - On. Avv. Leopoldo RUBINACCI, Ministro del Lavoro e Previdenza Sociale - On. Avv. Paolo TAVlANI, Ministro del Commercio con l'Estero - On. Avv. Bernardo MATTARELLA, Ministro della Marina Mercantile - On. Dr. Pietro CAMPILLI, Ministro senza portafoglio, con mansioni di Presidente del Comitato dei Ministri per la Cassa del Mezzo giorno e per le aree dpresse del Centro Nord. 19 luglio 1953 CAPRAROLA Il Presidente della Repubblica riceve in udienza alle ore 13,30, trattenendolo a colazione, Monsignor BARBIERI. 20 luglio 1953 CAPRAROLA Il Presidente della Repubblica riceve in udienza, alle ore 20,30, trattenendoli a pranzo : - l'On. -

Minorities Formation in Italy

Minorities Formation in Italy GIOVANNA CAMPANI Minorities Formation in Italy Introduction For historical reasons Italy has always been characterized as a linguistically and culturally fragmented society. Italy became a unifi ed nation-state in 1860 after having been divided, for centuries, into small regional states and having been dominated, in successive times, by different European countries (France, Spain, and Austria). As a result, two phenomena have marked and still mark the country: - the existence of important regional and local differences (from the cultural, but also economic and political point of view); the main difference is represented by the North-South divide (the question of the Mezzogiorno) that has strongly in- fl uenced Italian history and is still highly present in political debates; and - the presence of numerous “linguistic” minorities (around fi ve percent of the Italian population) that are very different from each other. In Italy, one commonly speaks of linguistic minorities: regional and local differences are expressed by the variety of languages and dialects that are still spoken in Italy. The term “ethnic” is scarcely used in Italy, even if it has been employed to defi ne minorities together with the term “tribes” (see GEO special issue “the tribes of Italy”). When minorities speak of themselves, they speak in terms of populations, peo- ples, languages, and cultures. The greatest concentration of minorities is in border areas in the northeast and northwest that have been at the centre of wars and controversies during the 20th century. Other minorities settled on the two main islands (where they can sometimes constitute a ma- 1 Giovanna Campani jority, such as the Sardinians). -

Libro Aldo Moro X

Consiglio Regionale della Puglia Moro vive Consiglio Regionale della Puglia LEGGI LA PUGLIA Pubblicazione n. 3 della linea editoriale Categoria: Personaggi Proprietà letteraria riservata A cura dell'on. Gero Grassi Per ogni informazione su questa pubblicazione contattare la Sezione Biblioteca e Comunicazione istituzionale via Capruzzi, 212 - 70124 Bari - tel 0805402772 email: [email protected] © Copyright 2018 Consiglio Regionale della Puglia Stampato da Grafiche Arcobaleno snc - Aprile 2018 Avvertenza Questa pubblicazione riflette solo il punto di vista degli autori e il Consiglio Regionale della Puglia non può essere ritenuto responsabile del contenuto, né di qualsivoglia uso venga fatto delle informazioni contenute nel volume. Per le immagini storiche di cui non è stato possibile rintracciare i diritti, il Consiglio Regionale della Puglia si dichiara fin d'ora disponibile a riconoscerli a chi ne facesse legittimamente richiesta, previa verifica della dichiarazione liberatoria rilasciata dall'autore e delle sue responsabilità. Licenze Creative Commons. Libertà di copiare, distribuire o trasmettere l'opera. Si permette che altri copino, distribuiscano, mostrino ed eseguano copie dell'opera e dei lavori derivati da questa a patto che vengano mantenute le indicazioni di chi è l'autore dell'opera. Si permette che altri copino, distribuiscano, mostrino ed eseguano copie dell'opera e dei lavori derivati da questa solo per scopi non commerciali. Tutti i diritti di traduzione, riproduzione e adattamento, totale o parziale, con qualsiasi mezzo (comprese le copie fotostatiche e i microfilm) sono riservati al Consiglio Regionale della Puglia. Moro vive Mario Loizzo Presidente del Consiglio Regionale della Puglia Il 9 maggio 1978 ero a Roma, giovane sindacalista, nella segreteria nazionale della Federbraccianti CGIL di Giuseppe Di Vittorio. -

HISTORIA MAGISTRA Rivista Di Storia Critica – Abstract + Parole Chiave Fascicolo 14-2014

HISTORIA MAGISTRA Rivista di storia critica – www.historiamagistra.it Abstract + parole chiave Fascicolo 14-2014 POLITICA AL FEMMINILE. MARGHERITA BONTADE MILITANTE DEMOCRISTIANA NELLA SICILIA DEI PRIMI ANNI DELLA REPUBBLICA. Alessandra Dino Margherita Bontade was one of the most singular figures of women involved in politics in Sicily after the World War II; she was also one of the few women who found space among the powerful Christian Democrats of that period, who where occupied in a strong opposition to the advancing of the parties if the so called “Blocco del Popolo”, with the blessing of the Catholic Church's hierarchies. Her electoral success depended, on one hand, on her close bonding with the Curia and on her personal relationship with Ernesto Ruffini, Cardinal in Palermo; on the other hand, on her political alliance at first with Bernardo Mattarella, then with Franco Restivo. But her striking political career, that took place in the arch of twenty years – between the end of the 40s and the end of the 60s – wasn't characterized by a particular intense parliamentary activity; instead her ambiguous relationships with powerful men of Cosa Nostra's world, and her public defence of Francesco Paolo Bontade, boss of the township of Villagrazia in Palermo, produced a lot of critique around her. Key words: Christian Democracy; Cosa Nostra; Catholic Church; Women; Politics; Sicily, World War II; Postwar Period. Parole chiave: Democrazia Cristiana; Cosa Nostra; Chiesa cattolica; Donne; Politica; Sicilia; Secondo dopoguerra. RISCRITTURE DELLA STORIA: L'ESEMPIO DELL'UNGHERIA DI ORBÁN Massimo Congiu The government led by Viktor Orbán has been confirmed to lead the country at the elections of April 6, 2014 and has maintained a parliamentary majority of two-third that it obtained four years ago. -

Sergio Mattarella

Sergio Mattarella Italia, Presidente de la República (2015-) Duración del mandato: 03 de Febrero de 2015 - En funciones Nacimiento: Palermo, región de Sicilia, 23 de Julio de 1941 Partido político: sin filiación (anteriormente, del Partido Democrático, PD) Profesión : Abogado, profesor de Derecho y juez Resumen Sergio Mattarella, antiguo responsable político de posiciones centro-reformistas y últimamente magistrado del Tribunal Constitucional, fue elegido presidente de la República Italiana el 31 de enero de 2015 a instancias del Gobierno de Matteo Renzi y en sucesión de Giorgio Napolitano. Mattarella, retratado como un servidor público sobrio, íntegro y sin afanes de protagonismo, militó en cuatro partidos (la Democracia Cristiana, el PPI, La Margarita y el PD de Renzi) antes de convertirse en independiente y fue otras tantas veces ministro entre 1987 y 2001, primero en los años postreros del Pentapartito andreottiano y luego en los gobiernos centro-izquierdistas de El Olivo. En el perfil del estadista siciliano tres rasgos destacan: su intenso compromiso en la lucha contra la Mafia, de cuya capacidad para corromper la política republicana tiene un preciso conocimiento, a raíz del asesinato de su hermano en 1980 por la Cosa Nostra; su condición de jurista puntilloso con el respeto a la legalidad; y su pésima opinión de Silvio Berlusconi. En su discurso inaugural, el nuevo presidente, con un mandato de siete años, ya ha dejado claro que respalda el ambicioso programa de reformas políticas del primer ministro Renzi y ha recordado sus roles institucionales de representante de la unidad nacional y garante de la Carta Magna, texto que afronta este año enmiendas en profundidad. -

Presidential Election: Blank Ballots on Day One Published on Iitaly.Org (

Italy - Presidential Election: Blank Ballots on Day One Published on iItaly.org (http://www.iitaly.org) Italy - Presidential Election: Blank Ballots on Day One (January 29, 2015) On Day One of the election for the twelfth president of Italy, the polling opened in the Chamber of Deputies at 3 pm. Four hours later the vote is still being counted, but results show clearly that no one was elected today. The two parties of a pre-election pact, Premier Matteo Renzi’s Partito Democratico (PD) and former Premier Silvio Berlusconi’s Forza Italia (FI), had agreed to vote blank ballots today, and did. But tomorrow is another day, and the voting continues. ROME – The moment of truth is at hand. On Day One of the election for the twelfth president of Italy, the polls opened in the Chamber of Deputies at 3 pm. At this writing, the vote is almost complete and shows 536 blank ballots by comparison with 360 for specific candidates such as former magistrate Ferdinando Imposimatok with 120 votes. The two parties which had made a pact to cooperate, Premier Matteo Renzi’s Partito Democratico (PD) and former Premier Silvio Berlusconi’s Forza Italia (FI), had agreed to vote blank ballots, and did. But tomorrow is another day, and the voting continues. Page 1 of 3 Italy - Presidential Election: Blank Ballots on Day One Published on iItaly.org (http://www.iitaly.org) Altogether 1,009 are entitled to vote: 630 from the Chamber of Deputies; 315 from the Senate; 58 delegates from the 20 regions; and six lifetime senators.