4-6-11 Sj Ccfd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Downtown Walking

N Montgomery St Clinton Ct Autumn A B C D E F G H I J d v N Blv Stockton Av A Guadalupe Gardens n Mineta San José Market Center VTA Light Rail Japantown African Aut t North S 1 mile to Mountain View 1.1 miles ame 0.8 miles International Airport ne American u i m a D + Alum Rock 1 n 3.2 miles e Community t r Terr Avaya Stadium St S N Almade N St James Services th Not 2.2 miles Peralta Adobe Arts + Entertainment Whole Park 0.2 miles 5 N Foods Fallon House St James Bike Share Anno Domini Gallery H6 Hackworth IMAX F5 San José Improv I3 Market W St John St Little Italy W St John St 366 S 1st St Dome 201 S Market St 62 S 2nd St Alum Rock Alum Food + Drink | Cafés St James California Theatre H6 Institute of H8 San José G4 Mountain View 345 S 1st St Contemporary Art Museum of Art Winchester Bike Share US Post Santa Teresa 560 S 1st St 110 S Market St Oce Camera 3 Cinema I5 One grid square E St John St 288 S 2nd St KALEID Gallery J3 San José Stage Co. H7 Center for the E5 88 S 4th St 490 S 1st St represents approx. Trinity Performing Arts Episcopal MACLA/Movimiento H8 SAP Center B2 255 Almaden Blvd 3 minutes walk SAP Center n St Cathedral de Arte y Cultura Latino 525 W Santa Clara St San José Sharks | Music m Americana 510 S 1st St tu Children’s D7 Tabard Theatre Co. -

S Artan Dail Mrs

Wm` Mabel 14 01111a, Librarian Calilornia Stnta Library Saosaninto 9, Calitottia .1.) DEBATERS SX/1 490if State &liege , _ "r4.14`4,yri1/41 MK , siE WILL DEFEND REP4ACES THIRD PARTY MISS ROOSE Henry Wallace and the Third S artan Dail Mrs. Bill Elam replaced Miss Party will occupy the attention FULL LEASED WIRE SERVICE OF UNITED PRESS Josephine Roose at veterans' co- of college orators during debate ordinator without a hitch in op- tryouts this afternoon at 3:30, Entered as second class maittir in the San Jose Post Office. The Press of the Globe Printing Co., San Jose, Calif. erations yesterday. Wilbur Luick, debating coach, re- Volume XXXVI SAN JOSE, CALIFORNIA, TUESDAY, APRIL 13, 1948 Number 114 Miss Roose left Friday to be- ported yesterday. come the bride of Carl G. Arf- The Forensic Squad, the debat- wedson of Redondo Beach April ing team, will uphold the affirma- 15. tive side of the question, "Re- The new veterans' representa- solved, that a third party is de- NOMINATIONS ASB SCHEDULED tive has been working in the of- sirable in American politics" fice she now heads for the last against the University of Califor- year and one-half. She is the wife nia debaters next Monday. The of Bill Elam, varsity right half- debate will be held before the FOR 2 : 3 0 TOMORROW; MELITA back last season. She is a native International Relations club here. of Oregon and attended Oregon Speakers to _represent this State college. school will be chosen after the HALL SUCCEEDS BEVERLY CLAY Veterans' affairs and the Job tryouts. -

Spare the Air Employer Program Members

Spare the Air Employer Program Members 511 Affymetrix Inc. 1000 Journals Project Agilent Technologies ‐ Sonoma County 3Com Corporation Public Affairs 511 Contra Costa Agnews Developmental Center 511 Regional Rideshare Program AHDD Architecture 7‐Flags Car Wash Air Products and Chemicals, Inc. A&D Christopher Ranch Air Systems Inc. A9.com Akeena Solar AB & I Akira ABA Staffing, Inc. Akraya Inc. ABB Systems Control Alameda Co. Health Care for the Homeless Abgenix, Inc. Program ABM Industries, Inc Alameda County Waste Management Auth. Above Telecommunications, Inc. Alameda Free Library Absolute Center Alameda Hospital AC Transit Alameda Unified School District Academy of Art University Alder & Colvin Academy of Chinese Culture & Health Alexa Internet Acclaim Print & Copy Centers Allergy Medical Group Of S F A Accolo Alliance Credit Union Accretive Solutions Alliance Occupational Medicine ACF Components Allied Waste Services/Republic Services Acologix Inc. Allison & Partners ACRT, Inc Alta Bates/Summit Medical Center ACS State & Local Solutions Alter Eco Act Now Alter Eco Americas Acterra ALTRANS TMA, Inc Actify, Inc. Alum Rock Library Adaptive Planning Alza Corporation Addis Creson American Century Investment Adina for Life, Inc. American International (Group) Companies Adler & Colvin American Lithographers ADP ‐ Automatic Data Processing American Lung Association Advance Design Consultants, Inc. American Musical Theatre of San Jose Advance Health Center American President Lines Ltd Advance Orthopaedics Amgen, Inc Advanced Fibre Communications Amtrak Advanced Hyperbaric Recovery of Marin Amy’s Kitchen Advanced Micro Devices, Inc. Ananda Skin Spa Advantage Sales & Marketing Anderson Zeigler Disharoon Gallagher & Advent Software, Inc Gray Aerofund Financial Svcs.,Inc. Anixter Inc. Affordable Housing Associates Anomaly Design Affymax Research Institute Anritsu Corporation Anshen + Allen, Architects BabyCenter.com Antenna Group Inc BACE Geotechnical Anza Library BackFlip APEX Wellness Bacon's Applied Biosystems BAE Systems Applied Materials, Inc. -

Spare the Air Employer Program Members List Last Updated: April

Spare the Air Employer Program Members 1000 Journals Project Affymax Research Institute 511 Contra Costa - Pleasant Hill Affymetrix Inc. 511 Contra Costa - San Pablo Agilent 511 Regional Rideshare Program Agilent Technologies - Sonoma County 7 Flags Car Wash Public Affairs A Nobel Smile Air Products and Chemicals, Inc. A&D Christopher Ranch Air Systems Inc. A. Maciel Printing Airtreks A9.com Akira AB & I Akraya Inc. ABA Staffing, Inc. Alameda Co. Health Care for the Homeless ABB Systems Control Program Abbott Alameda County Waste Management Auth. Abgenix, Inc. Alameda Free Library Able Services Alameda Hospital ABM Industries, Inc Alameda Publishing Group Above Telecommunications, Inc. Alexa Internet Absolute Center All Covered AC Transit Allergy Medical Group Of S F A Academy of Chinese Culture & Health Alliance Credit Union Acclaim Print & Copy Centers Alliance Occupational Medicine Accolo Allied Waste Services Accretive Solutions Allied Waste Services -- SCCO Division ACF Components 4915 ACRT, Inc Allied Waste Services/Republic Services ACS State & Local Solutions Allison & Partners Act Now Alta Bates/Summit Medical Center Acterra Alter Eco Actify, Inc. Alter Eco Americas Actiontec Electronics ALTRANS TMA, Inc Adaptive Planning Alum Rock Library Addis Creson AMC Entertainment, Inc Adina for Life, Inc. Amelias Antics Adler & Colvin American Century Investment Adobe Lumber American International (Group) Companies ADP - Automatic Data Processing American Lung Association in California Adura Technologies American President Lines Ltd Advance Design Consultants, Inc. Amgen, Inc Advance Health Center Amtrak Advance Orthopaedics Amy’s Kitchen Advanced Hyperbaric Recovery of Marin Anderson Zeigler Disharoon Gallagher & Advantage Sales & Marketing Gray Advent Software, Inc Andrades Automotive Aerofund Financial Svcs.,Inc. Angela Klein, Architect Affinture Anixter Inc. -

Download the September 2017 Valley Access Magazine

aprila\G SEPTEMBER 2017 "A Hospitality Networking Organization" WWW.SILICONVALLEYCONCIERGE.COM Gilroy Welcome Center Graphic Always Guglielmo Winery Hammer Theater Happy Hollow Zoo Hermitage Brewery Holiday Inn Silicon Valley Homewood Suites by Hilton San Jose North Hornblower Cruises & Events Hotel De Anza & La Pastaia Restaurant Il Fornaio San Jose Last Call Band LB Steak Magnolia Jazz Band Mineta San Jose International Airport Monopoly in the Park Mosaic Global Transportation Moving Green Today Rexford Winery Roaring Camp Railways Roudin-Smith Winery San Jose AV San Jose Downtown Association & Foundation San Jose Marriott Hotel & Arcadia Restaurant San Jose Museum of Art San Jose Theaters Santa Clara Convention & Visitors Bureau Santa Clara Convention Center Santa Clara Valley Brewing Santa Cruz Mountain Wine Growers Association Sedona Pies Alameda Family Funeral &Cremations Christmas in the Park See's Candies AreaOwl Cinnabar Hills Golf Club Silicon Valley Business Journal Balloonatics Citti's Florist Starbright Theater Bijan Bakery ComedySportz Strike Brewery Boudin Bakery Corinthian Transporation tacolicious Buca di Beppo Discover Silicon Valley TAPSNAP 1050 Business Women of Silicon Valley Double Tree By Hilton Campbell Testarossa Winery with/Maggianno's Eastridge Center The Cocoa Exchange Cake Expressions Equinox Winery The Mountain Winery Cal Coast Kettle Corn Every Circle The Tech Museum of Innovation Campbell Chamber of Commerce Fairfield Enterprise The Ultimate Benefit Canine Companions Fitz Place The Walt Disney Family Museum -

A Hospitality Networking Organization"

SEPTEMBER 2018 “A Hospitality Networking Organization" WWW.SILICONVALLEYCONCIERGE.COM H We believe that “A Hospitality Networking Organization” is beneficial to all of us. The art of creating and maintaining positive relationships is a significant factor in the success of the SVCA and our hospitality partners. We thank you in advance for your consideration in supporting the Silicon Valley Concierge Association and look forward to seeing you at the awards event! THINGS TO DO BAYAREA.COM THURSDAY, SEPT. 6TH “Behind-the-Scenes- Adventure”@the Hammer Theatre September sips: 6 wine/beer tasting events to check out By Lisa Herendeen Live Music on the Terrace Summer is coming to a close, but harvest lies Raffles for Hammer Theatre just ahead. Clearly it’s time for some serious Gift Certificates fun, from a barbera festival to a Gatsby party $100 Visa Gift Card @ 8pm and a Bloody Mary fest. Here are 6 awesome San Jose Photo Booth wine, beer and cocktail events to check out. (Elite Entertainment) Standard Party Rentals Harvest Wine Celebration: 12-5 p.m. Sept. 2. SJSU Spartan Eats More than 35 wineries will host festivities, including barrel samples and vineyard tours plus food, wine, art, crafts and live music at this 36th annual event in the Livermore Valley. $40 in advance; $45 day of at participating wineries. www.lvwine.org Farm to Table Wine Dinner: 6-9 p.m. Sept. 7 and 28. Chaminade Resort & Spa, 1 SILICON VALLEY CONCIERGE ASSOCIATION Chaminade Lane, Santa Cruz. This five-course dinner showcases the region’s Summit to Sea wineries as well as its seasonal bounty. -

Download the January 2018 Valley

aprila\G JANUARY 2018 "A Hospitality Networking Organization" WWW.SILICONVALLEYCONCIERGE.COM Congratulations Recognition from the Santa Clara City Council in December of 2017 #SanJoseEATS takes place Jan. 15-28 as part of California Restaurant Month. Now in its eighth year, California Citti’s Florist was recognized for their years of Restaurant Month is a state-wide program sponsored by service to the City of Santa Clara serving the encouraging visitors to partake in California cuisine. Mission City for decades. Chris Citti accepting In 2016, travelers in California spent $33.9 billion on food and beverage (Source: Dean Runyan Associates), and 38 million the award. domestic visitors participated in fine dining throughout the state. The SVO is a proud partner with SVO member Team San Jose on this event aimed at celebrating our diverse culinary offerings in San Jose. Below are the SVO members participating. Be sure to stop by and show them support. EMC Seafood & Raw Bar Santana Row LB Steak Santana Row Fountain Restaurant Olla Cocina Fogo de Chão Santana Row The Farmers Union Loft Bar & Bistro Dining with Bella! I spent the week between Christmas and New Years in Palm Springs. The average daily temperature was 80 degrees with full sun. Swimming in January, lying by the pool with an adult beverage, all things I highly recommend in the dead of winter. Tried a couple of different restaurants while I was there. TRIO Best deal in town if you eat before 6:00 p.m. They have a three-course The CAMPBELL Chamber is looking for a welcoming person meal at 19.99 that is absolutely delicious. -

When Richard Thompson Returns to the Bay Area in December

***For Immediate Release*** Winter Fest 2015 Friday, February 27 - Sunday, March 8, 2015 Cafe Stritch, The Continental, Hedley Club, MACLA, San Pedro Square Market, San Jose Stage Company and other venues in Downtown San Jose, CA Event Info: www.sanjosejazz.org/winterfest Tickets: $15 - $30, $175/VIP All Concert Pass; Select Youth Band Shows Are Free National Headliners: Taylor McFerrin Kris Bowers Kendrick Scott Oracle Marc Cary Focus Trio Diane Schuur Mads Tolling Quartet with Tierney Sutton Denise Perrier Trio with Houston Person Les Yeux Noirs Bay Area Youth Ensemble Performances: San Jose Jazz High School All Stars Homestead Jazz Ensemble Valley Christian Jazz Ensemble Los Gatos High School Jazz Band Kuumbwa Jazz Honor Band "McFerrin has a knack for knowing just how many elements he can balance." -Pitchfork "Kris Bowers is definitely an artist to watch." -Huffington Post "Kendrick Scott is already one of the very finest drummers on the jazz scene." -All About Jazz "(Marc Cary is) a jazz pianist of broad expertise." -New York Times "Now, as a bandleader (Mads Tolling will) showcase not just his flying bow and creatively nimble improvisation, but also his eclectic arrangements." -SF Bay Guardian "To hear this band (Les Yeux Noirs) reworking traditional dance music and Yiddish lullabies is to behold a remarkably deft aesthetic transformation." -Chicago Tribune San Jose, CA -- Friday, February 20, 2015 -- Renowned for its annual Summer Fest, the iconic Bay Area institution San Jose Jazz kicks off 2015 with dynamic arts programming honoring the jazz tradition and ever-expanding definitions of the genre with singular concerts curated for audiences within the heart of Silicon Valley. -

W. Santa Clara Street

DOWNTOWN SAN JOSE SUBLEASE 333 W. Santa Clara Street SPACE DETAILS • 4,740 RSF • Term through May 31, 2021 • $3.00 Full Service • Ground Floor Suite • Exclusive Exterior Entrance • Mix of Open Office, Meeting Rooms, Break Room • Dedicated Restrooms • Kitchen Facilities • Dedicated IT Room FEATURES • Walking Distance to • Proximity to San Pedro Square Market • Parking 3/1000 • On Site 24/7 Security • Credit Sublessor Colliers International Jake Smart John Colyar 225 W. Santa Clara Street, Suite 1000 Senior Associate Vice President San Jose, CA 95113 LIC. 02031308 LIC. 01987484 www.colliers.com/sanjose 650 492 5216 650 492 5209 [email protected] [email protected] FOR SUBLEASE 333 W. Santa Clara Street // San Jose SUITE 1 4,740 SQUARE FEET Jake Smart John Colyar Colliers International Senior Associate Vice President 225 W. Santa Clara Street, Suite 1000 LIC. 02031308 LIC. 01987484 San Jose, CA 95113 www.colliers.com/sanjose 650 492 5216 650 492 5209 [email protected] [email protected] N M o n t g o m e r y S 333 W. Santa Clara Street San Jose FOR SUBLEASEt // t Clin tumn C ton Au A B C D E F G H I J d v l v B N S A n Market Center VTA Light Rail t Guadalupe Gardens Mineta San José Japantown African A e t o e u S North c d m e k t a 1 mile to Mountain View 1.1 miles a 0.8 miles International Airport n American u t i o m a D m r l AMENITIES r + Alum Rock n 1 e n e A 3.2 miles Community t r A T Avaya Stadium t S S v N o St James t Services h t N 2.2 miles 5 Peralta Adobe Arts + Entertainment Whole Park 0.2 miles N Foods Fallon House St James Bike Share Anno Domini Gallery H6 Hackworth IMAX F5 San José Improv I3 Market W St John St Little Italy W St John St 366 S 1st St Dome 201 S Market St 62 S 2nd St 333 W. -

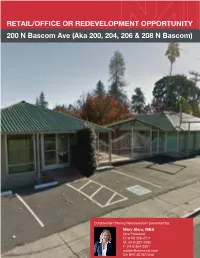

200 N Bascom

Retail/ Office Or Redevelopment Opportunity 200 N Bascom Ave, San Jose, CA 95128 telRETAIL/OFFICE+1 415 358 2111 OR REDEVELOPMENT OPPORTUNITY cell +1 415 297 5586 fax +1 415 354 3501 200 N Bascom Ave (Aka 200, 204, 206 & 208 N Bascom) Confidential Offering Memorandum presented by: Mary Alam, MBA Vice President O: (415) 358-2111 M: (415) 297-5586 F: (415) 354-3501 [email protected] CA BRE #01927340 Table of Contents 5 Section 1 Property Information 12 Section 2 Location Information 24 Section 3 Demographics Confidentiality & Disclosure Agreement The information contained in the following Investment Summary is proprietary and strictly confidential. It is intended to be reviewed only by the party receiving it from NAI Northern California Investment Real Estate Brokerage and should not be made available to any other person or entity without the written consent of Broker. This Investment Summary has been prepared to provide summary, unverified information to prospective purchasers, and to establish only a preliminary level of interest in the subject property. The information contained herein is not a substitute for a thorough due diligence investigation. Broker has not made any investigation, and makes no warranty or representation, with respect to the income or expenses for the subject property, the future projected financial performance of the property, the size and square footage of the property and improvements, the presence or absence of contaminating substances, PCB’s or asbestos, the compliance with State and Federal regulations, the physical condition of improvements thereon, or the financial condition or business prospects of any tenant, or any tenant’s plans or intentions to continue occupancy of the subject property. -

Board of Directors Regular Meeting Notice Thursday, August 8Th

0 ZONE A Gary Hageman – Hilton San Jose & Towers* John Southwell - San Jose Marriott * Dan McGowan– The Fairmont San Jose * Yves Hansel- Hotel De Anza Sherrie Carreno– Hyatt Place Stephen Sanatana – The Westin San Jose Wes Santos- AC by Marriott San Jose Randy Zimmerman – Four Points Sheraton Downtown Mike Chu- Arena Hotel Board of Directors Regular Meeting Notice ZONE B th Tanya Fleming– Holiday Inn San Jose Airport* Thursday, August 8 , 2019 8:30 a.m. Open– Extended Stay America SJ Airport VIP Room - Team San Jose Misoon Kong – DoubleTree by Hilton San Jose* 408 Almaden Blvd. San Jose, CA 95110 John McEntee– Hyatt House SJ/ Silicon Valley* Minutes Allen Anderson - Wyndham Garden SJ Airport Open– Extended Stay America SJ Downtown I. CALL TO ORDER/INTRODUCTION – 8:38am Gary Hageman Sanjiv Gupta- Courtyard Marriott San Jose Airport Billy Mendez– Four Points by Sheraton SJ Airport II. Attendees: Jordan Muchk – E Z 8 #1, San Jose Board Members: John Southwell, San Jose Marriott; Brent Gaines, Hotel Valencia; Rhoda Balbas – Fairfield Inn & Suites SJ Airport Ryan Davis– Staybridge Suites San Jose Misoon Kong, DoubleTree San Jose; Dan McGowan, Fairmont; Jeff Carpenter, Hayes Luis Robles – Homewood Suites by Hilton Airport Alex Martinez– La Quinta Inn San Jose Airport Mansion; Gary Hageman, Hilton San Jose; Stephen Santana; The Westin, Wes Santos, David Oskiouan – E Z 8 Motel #2, San Jose AC Marriott; Michelle Govan, AC Marriott. Brian Morgan- Residence Inn Marriott/ Springhill St Pete Horoszko- Country Inn & Suites SJ Airport Team San Jose Staff: Matthew Martinucci, VP of Sales & Destination Services; Ben ZONE C Roschke, Director of Research and Strategic Development; Becky Gile, Tradeshow & Brent Gaines – Hotel Valencia Santana Row* Jeff Carpenter – Hayes Mansion Registration Sr. -

23Rd Annual San Jose Jazz Summer Fest Friday, August 10

***For Immediate Release*** 23rd Annual San Jose Jazz Summer Fest Friday, August 10 - Sunday, August 12, 2012 Plaza de Cesar Chavez Park, Downtown San Jose, CA Event Info: jazzfest.sanjosejazz.org Tickets: $15 - $20 (Children 5 - 12, $5) "If you live within 50 miles of San Jose, you probably know about the South Bay's biggest annual cultural event: San Jose Jazz Summer Fest. About 100,000 people attended [in 2011], the weather was tank-top perfect, and the musical arc of the weekend was increasingly impressive." -San Jose Mercury News "San Jose Jazz deserves a good deal of credit for spotting some of the region's most exciting artists long before they're headliners." -Andy Gilbert, San Jose Mercury News "Over 1,000 artists and 100,000 music lovers converge on San Jose for a weekend of jazz, funk, fusion, blues, salsa, Latin, R&B, electronica and many other forms of contemporary music." -KQED "…the festival continues to up the ante with the roster of about 80 performers that encompasses everything from marquee names to unique up and comers, and both national and local acts...." -Silicon Valley Community Newspapers San Jose, CA - June 7, 2012 - San Jose Jazz sets the stage for the 23rd Annual San Jose Jazz Summer Fest with exceptional musical and cultural programming featuring some of today's most distinguished national acts, hottest jazz and Latin artists, and the Bay Area's top local talent. Known as one of the biggest Latin festivals in the nation, Summer Fest will take place from Friday, August 10 - Sunday, August 12, 2012 in and around Plaza de Cesar Chavez Park in downtown San Jose, CA.