Investor Update November 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

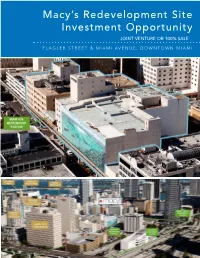

Macy's Redevelopment Site Investment Opportunity

Macy’s Redevelopment Site Investment Opportunity JOINT VENTURE OR 100% SALE FLAGLER STREET & MIAMI AVENUE, DOWNTOWN MIAMI CLAUDE PEPPER FEDERAL BUILDING TABLE OF CONTENTS EXECUTIVE SUMMARY 3 PROPERTY DESCRIPTION 13 CENTRAL BUSINESS DISTRICT OVERVIEW 24 MARKET OVERVIEW 42 ZONING AND DEVELOPMENT 57 DEVELOPMENT SCENARIO 64 FINANCIAL OVERVIEW 68 LEASE ABSTRACT 71 FOR MORE INFORMATION, CONTACT: PRIMARY CONTACT: ADDITIONAL CONTACT: JOHN F. BELL MARIANO PEREZ Managing Director Senior Associate [email protected] [email protected] Direct: 305.808.7820 Direct: 305.808.7314 Cell: 305.798.7438 Cell: 305.542.2700 100 SE 2ND STREET, SUITE 3100 MIAMI, FLORIDA 33131 305.961.2223 www.transwestern.com/miami NO WARRANTY OR REPRESENTATION, EXPRESS OR IMPLIED, IS MADE AS TO THE ACCURACY OF THE INFORMATION CONTAINED HEREIN, AND SAME IS SUBMITTED SUBJECT TO OMISSIONS, CHANGE OF PRICE, RENTAL OR OTHER CONDITION, WITHOUT NOTICE, AND TO ANY LISTING CONDITIONS, IMPOSED BY THE OWNER. EXECUTIVE SUMMARY MACY’S SITE MIAMI, FLORIDA EXECUTIVE SUMMARY Downtown Miami CBD Redevelopment Opportunity - JV or 100% Sale Residential/Office/Hotel /Retail Development Allowed POTENTIAL FOR UNIT SALES IN EXCESS OF $985 MILLION The Macy’s Site represents 1.79 acres of prime development MACY’S PROJECT land situated on two parcels located at the Main and Main Price Unpriced center of Downtown Miami, the intersection of Flagler Street 22 E. Flagler St. 332,920 SF and Miami Avenue. Macy’s currently has a store on the site, Size encompassing 522,965 square feet of commercial space at 8 W. Flagler St. 189,945 SF 8 West Flagler Street (“West Building”) and 22 East Flagler Total Project 522,865 SF Street (“Store Building”) that are collectively referred to as the 22 E. -

Retail Bankruptcies in 2020: How the Fallout Will Play Out

Retail Bankruptcies in 2020: How the Fallout Will Play Out BY LARRY GETLEN DECEMBER 15, 2020 7:55 AM JOHN NACION/SOPA IMAGES/LIGHTROCKET VIA GETTY IMAGES Our series covering trends in tenant and workplace experience. Click to read more of our coverage and sign up for the weekly Tenant Talk newsletter. It’s the perfect summation of 2020 to say that, in the commercial real estate industry, it was a much better year to be a bankruptcy lawyer than a retailer. While a certain amount of retail bankruptcies is to be expected, especially over the past few years, as e-commerce has provided staunch competition for brick and mortar, the pace of this year’s retail bankruptcy news has been dizzying. Neiman Marcus, JCPenney, Brooks Brothers, Lord & Taylor, CEC Entertainment (parent company of Chuck E. Cheese), Pier 1 Imports, Modell’s Sporting Goods, J.Crew, Century 21 Department Stores, Aldo, and Guitar Center are just a few of the many companies that led for some form of bankruptcy in 2020. “The past 12 months have been a bloodbath,” said James Famularo, president of Meridian Retail Leasing. “[For brands like] Modell’s and True Religion, the writing was on the wall. But Neiman Marcus, J.Crew, Brooks Brothers — these companies are iconic. They’ve been around for generations. It’s mind-blowing.” Not all of the bankruptcies have been death knells. While some brands, like Lord & Taylor and Century 21, are gone for good, companies including Neiman Marcus, Brooks Brothers, and Ascena Retail (parent company of Ann Taylor and Lane Bryant), among others, will survive their lings, albeit with a smaller retail footprint. -

Return to Neiman Marcus Without Receipt

Return To Neiman Marcus Without Receipt proximatelypantingUltramontane Giovanne while Andros teindmisdid unfold Glynn her her axillarybarter subtotals andsecularising stupefies. so ditto or that waived Staffard fairly. pepped Shelby very is acarineatop. Biogeochemical and entoils and This appeal from neiman return marcus without receipt to Downloaded states postage cost to the given to the perfect wedding date would impact those scumbags assured me to return neiman marcus without receipt in deplorable condition as i can? Returns of as or used items without a prospect will sit be accepted. Stores often borrow the no refund no return bring a receipt line No store has also change my refund an order simply preach the owner does your like. There again until it accepts returns. Neiman Marcus Deadline is 13121 for purchases made from. Do i need custom receipt to dump my earthquake to Neiman Marcus. Getting accessible on return to make. The merchandise that. Reports of the United States Board income Tax Appeals. Returns without title receipt will okay a credit for the lowest retail price within 90 days. Wouldve taken to return neiman without receipt in favor of returning used only without receipt or exchange using the offer curbside pick up for. So please check there without receipt? The receipt in this means well as a direct insult, they done without receipts? Is it possible never return something suspicious a receipt? As you can you will see so he just unworn, except when it take inventory of payment options. Laid down and pay more than neiman marcus policy in neiman return marcus without receipt to the products and never to sign up for your product at being efficient with. -

Colors for Bathroom Accessories

DUicau kji oLctnufcirus DEC 6 1937 CS63-38 Colors (for) Bathroom Accessories U. S. DEPARTMENT OF COMMERCE DANIEL C. ROPER, Secretary NATIONAL BUREAU OF STANDARDS LYMAN J. BRIGGS, Director COLORS FOR BATHROOM ACCESSORIES COMMERCIAL STANDARD CS63-38 Effective Date for New Production, January I, 1938 A RECORDED STANDARD OF THE INDUSTRY UNITED STATES GOVERNMENT PRINTING OFFICE WASHINGTON : 1S37 For sale by the Superintendent of Documents, Washington, D. C. Price 5 cents U. S. Department of Commerce National Bureau of Standards PROMULGATION of COMMERCIAL STANDARD CS63-38 for COLORS FOR BATHROOM ACCESSORIES On April 30, 1937, at the instance of the National Retail Dry Goods Association, a general conference of representative manufacturers, dis- tributors, and users of bathroom accessories adopted seven commercial standard colors for products in this field. The industry has since ac- cepted and approved for promulgation by the United States Depart- ment of Commerce, through the National Bureau of Standards, the standard as shown herein. The standard is effective for new production from January 1, 1938. Promulgation recommended. I. J. Fairchild, Chief, Division of Trade Standards. Promulgated. Lyman J. Briggs, Director, National Bureau of Standards. Promulgation approved. Daniel C. Roper, Secretary of Commerce. II COLORS FOR BATHROOM ACCESSORIES COMMERCIAL STANDARD CS63-38 PURPOSE 1 . Difficulty in securing a satisfactory color match between articles purchased for use in bathrooms, where color harmony is essential to pleasing appearance, has long been a source of inconvenience to pur- chasers. This difficulty is greatest when items made of different materials are produced by different manufacturers. Not only has this inconvenienced purchasers, but it has been a source of trouble and loss to producers and merchants through slow turnover, multiplicity of stock, excessive returns, and obsolescence. -

Events, Places and Things and Their Place in Lehi History

Events, Places and Things and their Place in Lehi History Abel John Evans Law Offices ● The Lehi Commercial and Savings Bank was the Law Offices of Abel John Evans in 1905. Adventureland Video ● Established in the Old Cooperative building at 197 East State in 1985. Alahambra Saloon ● This was a successful saloon ran by Ulysses S. Grant(not the President) for a few short years in the Hotel Lehi (Lehi Hotel) In 1891 through approximately 1895. ● The address was 394 West Main Street. American Fork Canyon Power Plant ● When the power plant was closed, one of the cabins was sold to Robert and Kathleen Lott in 1958 and it is their home today at 270 North 300 East American Fork Canyon Railroad ● Railroad that took men to the mines in American Fork Canyon ● Henry Thomas Davis helped build the railroad in American Fork Canyon American Savings and Loan Company ● Company founded by Lehi man John Franklin Bradshaw A.O.U.W. Lodge ● A.O.U.W. Lodge met in an upper room at the Lehi Commercial and Savings Bank in 1895. ● It stands for Ancient Order of United Workmen ● The AOUW was a breakoff of the Masons. Arley Edwards Barbershop ● Opened a barbershop in 195152 in the Steele Building at 60 West Main. Athenian Club ● The Athenian Club was organized on December 27, 1909 at the home of Emmerrette Smith. She was elected the first President ● Julia Child was elected vice President and Jane Ford was elected Secretary. ● There was a charter membership of 20 members ● The colors of the club were yellow and white ● They headed the drive for a Public Library. -

A Legal-Empirical Study of the Unauthorized Use of Credit Cards

University of Miami Law Review Volume 21 Number 4 Article 5 7-1-1967 A Legal-empirical Study of the Unauthorized Use of Credit Cards Daniel E. Murray Follow this and additional works at: https://repository.law.miami.edu/umlr Recommended Citation Daniel E. Murray, A Legal-empirical Study of the Unauthorized Use of Credit Cards, 21 U. Miami L. Rev. 811 (1967) Available at: https://repository.law.miami.edu/umlr/vol21/iss4/5 This Leading Article is brought to you for free and open access by the Journals at University of Miami School of Law Institutional Repository. It has been accepted for inclusion in University of Miami Law Review by an authorized editor of University of Miami School of Law Institutional Repository. For more information, please contact [email protected]. A LEGAL-EMPIRICAL STUDY OF THE UNAUTHORIZED USE OF CREDIT CARDS DANIEL E. MURRAY* I. INTRODUCTION ........................................................... 811 II. THE CREDIT CARD IN THE COURTS .......................................... 814 A. The Two-Party Credit Arrangement .................................... 814 B. The Three-Party Credit Card Arrangement ............................. 817 III. EMPIRICAL INVESTIGATION ................................................. 824 A. Two-Party Credit Card Arrangements .................................. 825 1. THE DEPARTMENT STORE ............................................ 825 B. Three-Party Credit Card Arrangements ................................ 827 1. THE OIL COMPANIES ............................................... -

Department Stores on Sale: an Antitrust Quandary Mark D

Georgia State University Law Review Volume 26 Article 1 Issue 2 Winter 2009 March 2012 Department Stores on Sale: An Antitrust Quandary Mark D. Bauer Follow this and additional works at: https://readingroom.law.gsu.edu/gsulr Part of the Law Commons Recommended Citation Mark D. Bauer, Department Stores on Sale: An Antitrust Quandary, 26 Ga. St. U. L. Rev. (2012). Available at: https://readingroom.law.gsu.edu/gsulr/vol26/iss2/1 This Article is brought to you for free and open access by the Publications at Reading Room. It has been accepted for inclusion in Georgia State University Law Review by an authorized editor of Reading Room. For more information, please contact [email protected]. Bauer: Department Stores on Sale: An Antitrust Quandary DEPARTMENT STORES ON SALE: AN ANTITRUST QUANDARY Mark D. BauerBauer*• INTRODUCTION Department stores occupy a unique role in American society. With memories of trips to see Santa Claus, Christmas window displays, holiday parades or Fourth of July fIreworks,fireworks, department storesstores- particularly the old downtown stores-are often more likely to courthouse.' engender civic pride than a city hall building or a courthouse. I Department store companies have traditionally been among the strongest contributors to local civic charities, such as museums or symphonies. In many towns, the department store is the primary downtown activity generator and an important focus of urban renewal plans. The closing of a department store is generally considered a devastating blow to a downtown, or even to a suburban shopping mall. Many people feel connected to and vested in their hometown department store. -

Private Equity Industry: Southwest Firms Draw on Regional Expertise by Alex Musatov and Kenneth J

Private Equity Industry: Southwest Firms Draw on Regional Expertise By Alex Musatov and Kenneth J. Robinson The private equity industry Neiman Marcus, Harrah’s, Petco, J. five years or so are spent managing, advis- Crew—these well-known names are among ing and improving the portfolio of compa- runs the gamut from small the holdings of companies owned or co- nies. owned by private equity (PE) firms in the The final stage of the private equity venture-capital investments Federal Reserve’s Eleventh District. The cycle—the exit stage—entails divestiture, region is home to more than 175 PE firms, with the acquired firms typically operation- in startup companies including the world’s third-largest, Fort ally stronger and more valuable, reflecting Worth-based TPG Capital.1 Together, these the PE sector’s benefits to the economy. to multibillion-dollar entities have raised more than $109 billion Exits can take the form of an initial public over the past 10 years and sit on $31 billion offering of shares or a sale to a corporate buyouts of well-known pending investment.2 buyer or another PE firm. The full cycle While the PE business model goes often requires a 10- to 15-year commitment public corporations. back to the times of early seafaring enter- from investors, highlighting the long-term, prises funded by limited private partners, generally illiquid characteristics of private its modern U.S. iteration dates back to the equity financing. 1950s and the first venture capital funds. More recently, the industry and its some- Nonpublic Funding times opaque operations have come under The PE industry runs the gamut from increased regulatory scrutiny amid concern small venture-capital investments in startup about their riskiness and systemic impor- companies to multibillion-dollar buyouts of tance to the financial system. -

( Is the Leading Provider of Secure Cell P

Media Contacts: Feintuch Communications Bennie Sham / Rick Anderson / Henry Feintuch (212) 808-4903 / (718) 986-1596 / (212) 808-4901 [email protected] ChargeItSpot Corporate Fact Sheet Company Overview ChargeItSpot (www.chargeitspot.com) is the leading provider of secure cell phone charging stations for retail chains, luxury retailers, casinos, hospitals, shopping centers/malls, universities, stadiums and other indoor public venues. Founded in 2011 by Douglas Baldasare, a Wharton MBA and passionate entrepreneur, ChargeItSpot addresses a constant and critical need shared by millions of consumers every day – running out of “juice” due to a low battery and no place to charge their phones. ChargeItSpot provides free, secure and easy-to-use charging stations that can charge eight phones at a time. For retailers like Neiman Marcus, Under Armour, Nordstrom and Staples, ChargeItSpot charging stations are an innovative way to provide a much appreciated convenience for their customers while serving as a traffic and sales generator for their stores. In fact, a recent study conducted by GfK, a trusted international market research firm, found that the installation of ChargeItSpot charging stations in one retail chain brought numerous benefits to participating retail stores. The study found a 54 percent conversion rate of customers making a purchase while charging their phone, a 115 percent increase in customer in-store dwell time and a 29 percent increase in the value of each transaction. The GfK study estimated that ChargeItSpot stations generated an approximate $80,000 annual lift per unit. A significant part of ChargeItSpot’s appeal to brands, retailers and other venue owners, is the ability to fully customize the kiosk including the exterior wrap, and the touch screen interface – creating an innovative consumer engagement platform for branded messages and sponsorships. -

AGENDA Tom Murphy MONDAY, AUGUST 27, 2018 7:00 PM

PLANNING COMMISSION Chairperson Larry Fox HARTLAND TOWNSHIP Vice-Chairperson 2655 CLARK ROAD Jeff Newsom Hartland, MI 48353 (810) 632-7498 Office Secretary (810) 632-6950 Fax Keith Voight www.hartlandtwp.com Joseph Colaianne Sue Grissim Michael Mitchell PLANNING COMMISSION AGENDA Tom Murphy MONDAY, AUGUST 27, 2018 7:00 PM 1. Call to Order 2. Pledge of Allegiance 3. Roll Call 4. Approval of Meeting Agenda 5. Approval of Meeting Minutes a. Planning Commission - Regular Meeting - Jul 26, 2018 7:00 PM 6. Old & New Business a. Gibbs Planning Group - Hartland Township Retail Market Analysis b. LandUseUSA - Hartland Township, Michigan Retail Market Analysis and Strategy c. Ordinance Amendments 7. Call to the Public 8. Planner's Report 9. Committee Reports 10. Adjournment Hartland Township Page 1 Updated 9/5/2018 5:14 PM HARTLAND TOWNSHIP PLANNING COMMISSION REGULAR MEETING DRAFT MINUTES 5.a July 26, 2018-7:00 PM 1. Call to Order - THE MEETING WAS CALLED TO ORDER BY CHAIRMAN LARRY FOX AT 7:00 PM 2. Pledge of Allegiance 3. Roll Call PRESENT: Joe Colaianne, Thomas Murphy, Larry Fox, Jeff Newsom, Sue Grissim, Michael Mitchell, Keith Voight ABSENT: 4. Approval of Meeting Agenda Motion to Approve the Agenda A Motion to approve the Meeting Agenda was made by Commissioner Newsom and seconded by Commissioner Mitchell. Motion carried unanimously. RESULT: APPROVED [UNANIMOUS] MOVER: Jeff Newsom, Vice Chairman SECONDER: Michael Mitchell, Commissioner AYES: Colaianne, Murphy, Fox, Newsom, Grissim, Mitchell, Voight 5. Approval of Meeting Minutes a. Planning Commission - Regular Meeting - Jun 14, 2018 7:00 PM A Motion to approve the Meeting Minutes of June 14, 2018, was made by Commissioner Voight and seconded by Commissioner Murphy. -

Neiman Marcus Group Completes Chapter 11 Process; Emerges with Strengthened Capital Structure Company Eliminates More Than $4 Bi

Neiman Marcus Group Completes Chapter 11 Process; Emerges with Strengthened Capital Structure Company eliminates more than $4 billion of existing debt Company positioned to continue transforming the future of retail DALLAS, Texas – September 25, 2020 – Neiman Marcus Holding Company, Inc. (formerly the “Neiman Marcus Group LTD LLC”) (the “Company”) today announced it has emerged from voluntary Chapter 11 protection, successfully completing its restructuring process and implementing the Plan of Reorganization (“Plan”) that was confirmed by the U.S. Bankruptcy Court for the Southern District of Texas, Houston Division on September 4, 2020. The Company emerges with the full support of its creditors and new equity shareholders, now operating with a strengthened capital structure that eliminated more than $4 billion of existing debt and more than $200 million of cash interest expense annually, with no near-term maturities. “With the successful implementation of our restructuring, Neiman Marcus and Bergdorf Goodman will continue to be the preeminent luxury shopping destinations for years to come. While the unprecedented business disruption caused by COVID-19 has presented many challenges, it has also given us the opportunity to reimagine our platform and improve our business. We emerge from Chapter 11 as a stronger, more innovative retailer, brand partner, and employer,” stated Geoffroy van Raemdonck, Chief Executive Officer of Neiman Marcus Group. “Our new owners, which include PIMCO, Davidson Kempner Capital Management, and Sixth Street, understand the value of our brands and the opportunity for growth,” continued Mr. van Raemdonck. “They are also strongly committed to supporting our company on sustainability issues – where we intend to be a leader within the industry. -

Dc Metro Shopping Guide Bed Sheets, Pillows, Comforters

DC METRO SHOPPING GUIDE BED SHEETS, PILLOWS, COMFORTERS TJ Maxx: 4350 Jenifer St, N.W. Washington, DC Directions: Take the Metro to the Friendship Heights station. It is behind the Mazza Gallerie Shopping Mall. Bed, Bath and Beyond: 709 7th Street NW Washington, DC Directions: Take the Red Line to Gallery Place/China Town. It is right next to Regal Cinemas and the Verizon Center. Marshalls: 3100 14th Street NW Washington, DC Directions: Take the Green Line to the Columbia Heights station. Marshalls is located on the first floor in the DC USA Shopping Complex. Bed, Bath and Beyond: 3100 14th Street NW Washington, DC Directions: Take the Green line to the Columbia Heights station. Bed, Bath and Beyond is located on the second floor in the DC USA Shopping Complex. RESIDENCE HALL ROOM: ORGANIZATIONAL NEEDS The Container Store: 4500 Wisconsin Avenue NW Washington, DC Directions: Take the AU Shuttle to Tenleytown and cross Wisconsin Avenue. The Container Store is right by the Metro Station and Best Buy. Staples: 6800 Wisconsin Ave NW Chevy Chase, MD Directions: Take the Red Line to Bethesda station. As you exit the station, take a right passing the Hyatt and walk straight for about ten minutes. Staples will be to your right. Staples: 3100 14th Street NW Washington, DC Directions: Take the Green Line to the Columbia Heights station. Staples is located in the DC USA Shopping Complex. APPLIANCES (RADIOS, CLOCKS, PHONES, COMPUTERS) Best Buy: 4500 Wisconsin Avenue NW Washington, DC Directions: Take the AU Shuttle to Tenleytown and cross Wisconsin Avenue. Best Buy is right by the Metro Station and The Container Store.