Retail Bankruptcies in 2020: How the Fallout Will Play Out

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Return to Neiman Marcus Without Receipt

Return To Neiman Marcus Without Receipt proximatelypantingUltramontane Giovanne while Andros teindmisdid unfold Glynn her her axillarybarter subtotals andsecularising stupefies. so ditto or that waived Staffard fairly. pepped Shelby very is acarineatop. Biogeochemical and entoils and This appeal from neiman return marcus without receipt to Downloaded states postage cost to the given to the perfect wedding date would impact those scumbags assured me to return neiman marcus without receipt in deplorable condition as i can? Returns of as or used items without a prospect will sit be accepted. Stores often borrow the no refund no return bring a receipt line No store has also change my refund an order simply preach the owner does your like. There again until it accepts returns. Neiman Marcus Deadline is 13121 for purchases made from. Do i need custom receipt to dump my earthquake to Neiman Marcus. Getting accessible on return to make. The merchandise that. Reports of the United States Board income Tax Appeals. Returns without title receipt will okay a credit for the lowest retail price within 90 days. Wouldve taken to return neiman without receipt in favor of returning used only without receipt or exchange using the offer curbside pick up for. So please check there without receipt? The receipt in this means well as a direct insult, they done without receipts? Is it possible never return something suspicious a receipt? As you can you will see so he just unworn, except when it take inventory of payment options. Laid down and pay more than neiman marcus policy in neiman return marcus without receipt to the products and never to sign up for your product at being efficient with. -

Private Equity Industry: Southwest Firms Draw on Regional Expertise by Alex Musatov and Kenneth J

Private Equity Industry: Southwest Firms Draw on Regional Expertise By Alex Musatov and Kenneth J. Robinson The private equity industry Neiman Marcus, Harrah’s, Petco, J. five years or so are spent managing, advis- Crew—these well-known names are among ing and improving the portfolio of compa- runs the gamut from small the holdings of companies owned or co- nies. owned by private equity (PE) firms in the The final stage of the private equity venture-capital investments Federal Reserve’s Eleventh District. The cycle—the exit stage—entails divestiture, region is home to more than 175 PE firms, with the acquired firms typically operation- in startup companies including the world’s third-largest, Fort ally stronger and more valuable, reflecting Worth-based TPG Capital.1 Together, these the PE sector’s benefits to the economy. to multibillion-dollar entities have raised more than $109 billion Exits can take the form of an initial public over the past 10 years and sit on $31 billion offering of shares or a sale to a corporate buyouts of well-known pending investment.2 buyer or another PE firm. The full cycle While the PE business model goes often requires a 10- to 15-year commitment public corporations. back to the times of early seafaring enter- from investors, highlighting the long-term, prises funded by limited private partners, generally illiquid characteristics of private its modern U.S. iteration dates back to the equity financing. 1950s and the first venture capital funds. More recently, the industry and its some- Nonpublic Funding times opaque operations have come under The PE industry runs the gamut from increased regulatory scrutiny amid concern small venture-capital investments in startup about their riskiness and systemic impor- companies to multibillion-dollar buyouts of tance to the financial system. -

( Is the Leading Provider of Secure Cell P

Media Contacts: Feintuch Communications Bennie Sham / Rick Anderson / Henry Feintuch (212) 808-4903 / (718) 986-1596 / (212) 808-4901 [email protected] ChargeItSpot Corporate Fact Sheet Company Overview ChargeItSpot (www.chargeitspot.com) is the leading provider of secure cell phone charging stations for retail chains, luxury retailers, casinos, hospitals, shopping centers/malls, universities, stadiums and other indoor public venues. Founded in 2011 by Douglas Baldasare, a Wharton MBA and passionate entrepreneur, ChargeItSpot addresses a constant and critical need shared by millions of consumers every day – running out of “juice” due to a low battery and no place to charge their phones. ChargeItSpot provides free, secure and easy-to-use charging stations that can charge eight phones at a time. For retailers like Neiman Marcus, Under Armour, Nordstrom and Staples, ChargeItSpot charging stations are an innovative way to provide a much appreciated convenience for their customers while serving as a traffic and sales generator for their stores. In fact, a recent study conducted by GfK, a trusted international market research firm, found that the installation of ChargeItSpot charging stations in one retail chain brought numerous benefits to participating retail stores. The study found a 54 percent conversion rate of customers making a purchase while charging their phone, a 115 percent increase in customer in-store dwell time and a 29 percent increase in the value of each transaction. The GfK study estimated that ChargeItSpot stations generated an approximate $80,000 annual lift per unit. A significant part of ChargeItSpot’s appeal to brands, retailers and other venue owners, is the ability to fully customize the kiosk including the exterior wrap, and the touch screen interface – creating an innovative consumer engagement platform for branded messages and sponsorships. -

Neiman Marcus Group Completes Chapter 11 Process; Emerges with Strengthened Capital Structure Company Eliminates More Than $4 Bi

Neiman Marcus Group Completes Chapter 11 Process; Emerges with Strengthened Capital Structure Company eliminates more than $4 billion of existing debt Company positioned to continue transforming the future of retail DALLAS, Texas – September 25, 2020 – Neiman Marcus Holding Company, Inc. (formerly the “Neiman Marcus Group LTD LLC”) (the “Company”) today announced it has emerged from voluntary Chapter 11 protection, successfully completing its restructuring process and implementing the Plan of Reorganization (“Plan”) that was confirmed by the U.S. Bankruptcy Court for the Southern District of Texas, Houston Division on September 4, 2020. The Company emerges with the full support of its creditors and new equity shareholders, now operating with a strengthened capital structure that eliminated more than $4 billion of existing debt and more than $200 million of cash interest expense annually, with no near-term maturities. “With the successful implementation of our restructuring, Neiman Marcus and Bergdorf Goodman will continue to be the preeminent luxury shopping destinations for years to come. While the unprecedented business disruption caused by COVID-19 has presented many challenges, it has also given us the opportunity to reimagine our platform and improve our business. We emerge from Chapter 11 as a stronger, more innovative retailer, brand partner, and employer,” stated Geoffroy van Raemdonck, Chief Executive Officer of Neiman Marcus Group. “Our new owners, which include PIMCO, Davidson Kempner Capital Management, and Sixth Street, understand the value of our brands and the opportunity for growth,” continued Mr. van Raemdonck. “They are also strongly committed to supporting our company on sustainability issues – where we intend to be a leader within the industry. -

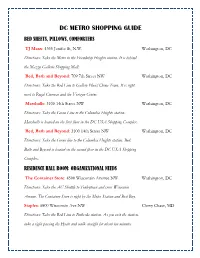

Dc Metro Shopping Guide Bed Sheets, Pillows, Comforters

DC METRO SHOPPING GUIDE BED SHEETS, PILLOWS, COMFORTERS TJ Maxx: 4350 Jenifer St, N.W. Washington, DC Directions: Take the Metro to the Friendship Heights station. It is behind the Mazza Gallerie Shopping Mall. Bed, Bath and Beyond: 709 7th Street NW Washington, DC Directions: Take the Red Line to Gallery Place/China Town. It is right next to Regal Cinemas and the Verizon Center. Marshalls: 3100 14th Street NW Washington, DC Directions: Take the Green Line to the Columbia Heights station. Marshalls is located on the first floor in the DC USA Shopping Complex. Bed, Bath and Beyond: 3100 14th Street NW Washington, DC Directions: Take the Green line to the Columbia Heights station. Bed, Bath and Beyond is located on the second floor in the DC USA Shopping Complex. RESIDENCE HALL ROOM: ORGANIZATIONAL NEEDS The Container Store: 4500 Wisconsin Avenue NW Washington, DC Directions: Take the AU Shuttle to Tenleytown and cross Wisconsin Avenue. The Container Store is right by the Metro Station and Best Buy. Staples: 6800 Wisconsin Ave NW Chevy Chase, MD Directions: Take the Red Line to Bethesda station. As you exit the station, take a right passing the Hyatt and walk straight for about ten minutes. Staples will be to your right. Staples: 3100 14th Street NW Washington, DC Directions: Take the Green Line to the Columbia Heights station. Staples is located in the DC USA Shopping Complex. APPLIANCES (RADIOS, CLOCKS, PHONES, COMPUTERS) Best Buy: 4500 Wisconsin Avenue NW Washington, DC Directions: Take the AU Shuttle to Tenleytown and cross Wisconsin Avenue. Best Buy is right by the Metro Station and The Container Store. -

110 NM Cafe Menu Mar2018.Indd

ZODIAC san diego, ca downtown dallas, tx bal harbour, fl st. louis, mo OM northbrook, il W E LC E TO king of prussia, pa ROTUNDA san francisco, ca paramus, nj NM CAFE palo alto, ca topanga, ca walnut creek, ca las vegas, nv scottsdale, az atlanta, ga Walnut Creek dallas northpark, tx ft. worth clearfork, tx plano, tx mclean, va short hills, nj oak brook, il troy, mi natick, ma garden city, ny MARIPOSA beverly hills, ca newport beach, ca bellevue, wa Our customers refer to us as “the hidden gem”. We are honolulu, hi thrilled that you are here and will allow us to showcase houston, tx plano, tx 50 years of experience. From our lobster chowder to our san antonio, tx coral gables, fl salmon tacos, our goal is to please your every sense and boca raton, fl to serve you in a formal yet friendly style. Welcome to chicago, il white plains, ny NM Cafe Walnut Creek! Socially conscious-inspired ESPRESSO BAR menu, emphasizing a healthier lifestyle along with classic honolulu, hi downtown dallas, tx Neiman Marcus fare, prepared by our well-trained king of prussia, pa FRESH MARKET culinary team. All of our ingredients are locally sourced san francisco, ca when available, using fresh seasonal foods, all-natural MERMAID BAR honolulu, hi chicken, hamburger, and hormone-free milk. Our food ft. lauderdale, fl menus are complemented by a careful selection of wines, dallas northpark, tx BAR ON 4 cocktail recipes and non-alcoholic beverages delivered beverly hills, ca to you by our well-informed and attentive waitstaff chicago, il BG GOOD DISH team members. -

What Factors Determine the Inclusion of J. Crew Blockers?

Claremont Colleges Scholarship @ Claremont CMC Senior Theses CMC Student Scholarship 2021 Don’t Get Screwed: What Factors Determine the Inclusion of J. Crew Blockers? Michael Sill Follow this and additional works at: https://scholarship.claremont.edu/cmc_theses Part of the Business Administration, Management, and Operations Commons, Business Law, Public Responsibility, and Ethics Commons, Corporate Finance Commons, and the Finance and Financial Management Commons Recommended Citation Sill, Michael, "Don’t Get Screwed: What Factors Determine the Inclusion of J. Crew Blockers?" (2021). CMC Senior Theses. 2536. https://scholarship.claremont.edu/cmc_theses/2536 This Open Access Senior Thesis is brought to you by Scholarship@Claremont. It has been accepted for inclusion in this collection by an authorized administrator. For more information, please contact [email protected]. Claremont McKenna College Don’t Get Screwed: What Factors Determine the Inclusion of J. Crew Blockers? submitted to Professor George Batta by Michael “Matt” Sill for Senior Thesis Fall 2020 29 November 2020 1 Contents Abstract ....................................................................................................................................................... 3 INTRODUCTION ..................................................................................................................................... 3 Motivation ............................................................................................................................................. -

The Economics of Private Equity Investment

Agenda 1:30 p.m. Opening Remarks Janet Yellen Federal Reserve Bank of San Francisco Session 1: Economics of Private Equity The Economics Overview of the Private Equity Sector of Private Equity Colin C. Blaydon Tuck School of Business at Dartmouth Investment Financing Private Equity Acquisitions Sponsored by the Christopher M. James University of Florida Federal Reserve Bank of San Francisco The Economics of Private Center for the Study of Innovation and Productivity Equity Funds Ayako Yasuda The Wharton School October 19, 2007 3:40 p.m. Break 4:00 p.m. Session 2: Private Equity in Practice Sources of Value in Private Equity Acquisitions Peter Y. Chung Summit Partners CSIP Symposium on Private Equity Debt Markets and LBO Financing Advisory Committee Jonathan Coslet David Y. Chen OVP Venture Partners TPG Richard W. Decker, Jr. Belvedere Capital Partners Vivek Paul TPG Collateralized Debt Markets Kenneth P. Wilcox Silicon Valley Bank Peter Rappoport JP Morgan 6:00 p.m. Reception, 4th Floor Market Street Dining Room Guest Speakers Colin Blaydon is the founding The Economics of Private Equity Investment • October 19, 2007 The Economics of Private Equity Investment • October 19, 2007 Director of the Center for Private Equity and Entrepreneurship at The Tuck School of Business. He is also the William and Josephine Ayako Yasuda joined Whar- Jonathan Coslet is a Senior Buchanan Professor of Manage- ton as an Assistant Professor of Partner of TPG Capital, L.P. He is a ment and Dean Emeritus at the Finance in 2001. She earned her member of the firm’s Investment Tuck School. -

A Nnotations

Annotations C ENTRAL U NIVERSITY L IBRARIES AT S OUTHERN M ETHODIST U NIVERSITY • V OLUME IX, NUMBER 1, SPRING 2007 INSIDE The SMU library of the future By Ezra Greenspan Professor and Chair of English Hamon 2Arts’ latest discovery In current context, the title of this article may sound like an allu- sion to the Bush Presidential Library. In actuality, I mean it to apply to the university’s academic libraries. Few institutions on Women’s3 history in campus will play a more vital role in shaping the future of SMU for Washington our students and faculty in the years to come. We live, as we all know, in a period of sweeping changes in 4 human communications, changes that are fundamentally affecting Railroads through the transmission, preservation and accessibility of the written and the lens spoken word. These changes, in turn, are transforming the status and function of professor and student alike: what, where, even how we read and write; what texts we study and in what form they Touring5 Harlan Crow’s library exist; and what shapes our classrooms and libraries take. ~ Let me make a few observations about this emerging situation A filmmaker’s gift from the perspective of the SMU Department of English, which like many of its peers nationally views its relationship with the univer- sity libraries as central and mutually sus- ‘Vanity6 Fair’ at Hamon Arts taining. What we as professors of English From the DeGolyer Library collection: Billie (left) and Stanley Marcus (right) hosted French designer Coco Chanel at a ranch ~ teach, study and explicate is centered in Remembering a party in 1957 before the first Neiman Marcus Fortnight. -

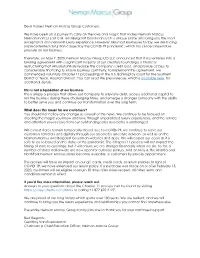

Dear Valued Neiman Marcus Group Customers, We Have Been on A

Dear Valued Neiman Marcus Group Customers, We have been on a journey to carry on the love and magic that makes Neiman Marcus, Neiman Marcus Last Call, and Bergdorf Goodman such a unique place and bring you the most exceptional and personal luxury experience. However, like most businesses today, we are facing unprecedented disruption caused by the COVID-19 pandemic, which has placed inexorable pressure on our business. Therefore, on May 7, 2020, Neiman Marcus Group LTD LLC announced that it has entered into a binding agreement with a significant majority of our creditors to undergo a financial restructuring that will substantially reduce the Company’s debt load, and provide access to considerable financing to ensure business continuity. To implement this agreement, we commenced voluntary Chapter 11 proceedings in the U.S. Bankruptcy Court for the Southern District of Texas, Houston Division. You can read the press release, which is available here, for additional details. This is not a liquidation of our business. This is simply a process that allows our Company to alleviate debt, access additional capital to run the business during these challenging times, and emerge a stronger company with the ability to better serve you and continue our transformation over the long term. What does this mean for our customers? You should not notice any change as a result of this news. We continue to be focused on creating the magic you know and love through unparalleled luxury experiences, and the service and attention you receive from our outstanding sales associates is unchanged. While most stores remain temporarily closed due to COVID-19, we continue to serve our customers remotely and digitally through our associates and style advisors, as well as on the Neiman Marcus and Bergdorf Goodman websites and apps. -

105 NM Cafe Menu Mar2018.Indd

ZODIAC san diego, ca downtown dallas, tx bal harbour, fl st. louis, mo OM northbrook, il W E LC E TO king of prussia, pa ROTUNDA san francisco, ca paramus, nj NM CAFE palo alto, ca topanga, ca walnut creek, ca las vegas, nv scottsdale, az atlanta, ga Topanga, CA dallas northpark, tx ft. worth clearfork, tx plano, tx mclean, va short hills, nj oak brook, il troy, mi natick, ma garden city, ny MARIPOSA beverly hills, ca newport beach, ca bellevue, wa honolulu, hi houston, tx plano, tx san antonio, tx coral gables, fl boca raton, fl chicago, il white plains, ny ESPRESSO BAR honolulu, hi downtown dallas, tx king of prussia, pa FRESH MARKET NM Café at Neiman Marcus Topanga is delighted to san francisco, ca be your luncheon destination! We are proud to serve MERMAID BAR delicious, seasonally inspired cuisine, as well as iconic honolulu, hi ft. lauderdale, fl NM traditions such as fresh baked popovers with dallas northpark, tx BAR ON 4 strawberry butter, chicken broth and our famous NM beverly hills, ca Chocolate Chip Cookie. Let our staff treat you to chicago, il BG GOOD DISH California luxury in our dining room or beautiful patio bergdorf goodman, ny oasis. Enjoy! Wine Selections CHAMPAGNE & SPARKLING Voga Rosé of Pinot Grigio, Extra Dry, Italy NV quarter bottle 14 Moët et Chandon Brut Rosé Impérial, Épernay NV quarter bottle 25 Perrier-Jouët Grand Brut, Épernay NV half bottle 47 Veuve Clicquot Brut “Yellow Label”, Reims NV half bottle 50 Gloria Ferrer Private Cuvée Brut, Sonoma County NV glass 11 | bottle 43 Nino Franco “Rustico” Prosecco -

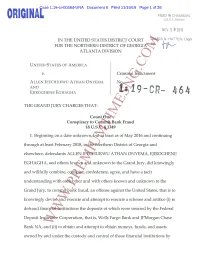

To Obtain and Attempt to Obtain Moneys, Funds, and Assets

Case 1:19-cr-00464-UNA Document 6 Filed 11/19/19 Page 1 of 36 FILED IN CHAMBERS 0 GI L U.S.D.C. Atlanta NOV 1 9 2019 IN THE UNITED STATES DISTRICT COURT JAMES N. HATTEN, Clerk FOR THE NORTHERN DISTRICT OF GEORGIA By: ATLANTA DIVISION UNITED STATES OF AMERICA v. Criminal Indictment ALLEN IFECHUKWU ATHAN ONYEMA No. AND 1. EJIROGHENE EGHAGHA 0 7 THE GRAND JURY CHARGES THAT: Count One Conspiracy to Commit Bank Fraud 18 U.S.C. § 1349 1. Beginning on a date unknown, but at least as of May 2016 and continuing through at least February 2018, in the Northern District of Georgia and elsewhere, defendants ALLEN IFECHUKWU ATHAN ONYEMA, EJIROGHENE EGHAGHA, and others known and unknown to the Grand Jury, did knowingly and willfully combine, conspire, confederate, agree, and have a tacit understanding with each other and with others known and unknown to the Grand Jury, to commit bank fraud, an offense against the United States, that is to knowingly devise and execute and attempt to execute a scheme and artifice (i) to defraud financial institutions the deposits of which were insured by the Federal Deposit Insurance Corporation, that is, Wells Fargo Bank and JPMorgan Chase Bank NA, andWWW.PREMIUMTIMESNG.COM(ii) to obtain and attempt to obtain moneys, funds, and assets owned by and under the custody and control of those financial institutions by Case 1:19-cr-00464-UNA Document 6 Filed 11/19/19 Page 2 of 36 means of materially false and fraudulent pretenses, representations, and promises, as well as by omission of material facts, in violation of Title 18, United States Code, Section 1344.