1. Overview of Government Companies and Statutory Corporations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Experiential Learning- Projectwork- Fieldwork

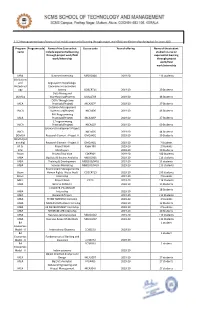

1.3.2 Average percentage of courses that include experiential learning through project work/field work/internship during last five years (10) Program Program code Name of the Course that Course code Year of offering Name of the student name include experiential learning studied course on through project work/field experiential learning work/internship through project work/field work/internship MBA Summer Internship MB010304 2019-20 113 students BSc Botany and Angiosperm morphology, Biotechnol taxonomy and economic ogy botany BO6CRT11 2019-20 20 Students Data Mining and DDMCA Warehousing(Project) DMCA703 2019-20 48 Students OOPs Through Java MCA Practicals(Project) MCA307P 2019-20 27 Students Database Management IMCA Systems Lab(Project) IMCA406 2019-20 46 Students PHP Programmimg MCA Practicals(Project) MCA306P 2019-20 27 Students C Programmomg IMCA Practicals(Project) IMCA107 2019-20 59 Students SoGware Development-Project IMCA I IMCA605 2019-20 44 Students DDMCA Research Element - Project II DMCAX01 2019-20 39 Students DDMCA(Int ernship) Research Element - Project II DMCAX01 2019-20 7 Students M.Sc Project Work Paper XIII 2019-20 2 Students B.Sc MiniProject 2019-20 20 Students Bcom Project/Viva Voce C06PR01 2019-20 100 Students MBA Big Data & Busines Analytics MB010301 2019-20 113 students MBA Training & Development MB82 03/0401 2019-20 13 students MBA Services Marketing MB81 03/0403 2019-20 113 students Environment Management & Bcom Human Rights- Water Audit CO5CRT15 2019-20 100 Students Bcom Internship 2019-20 7 Students MBA Project Work -

Mumtaz Hotels Limited

MUMTAZ HOTELS LIMITED BOARD OF DIRECTORS Mr. Prithviraj Singh Oberoi, Chairperson Mr. Shivy Bhasin, Vice Chairman Mr. Bharath Bhushan Goyal, Managing Director (upto 6th April 2019) Mr. T. K. Sibal Mr. Manish Goyal, Managing Director (w.e.f. 17th May 2019) Mr. Vikramjit Singh Oberoi Mr. Arjun Singh Oberoi Mr. Manav Goyal (w.e.f. 17th May 2019) Mr. Raj Kumar Kataria, Independent Director (upto 25th February 2020) Additional Director (w.e.f. 31st March 2020) Mr. Sandeep Kumar Barasia, Independent Director Dr. Chhavi Rajawat, Additional Director (w.e.f. 25th October 2019) CHIEF FINANCIAL OFFICER Mr. Kallol Kundu SECRETARY Mr. S.N. Sridhar AUDITORS Deloitte Haskins & Sells LLP, Chartered Accountants 7th Floor, Building 10, Tower B DLF Cyber City Complex DLF City Phase – II Gurugram – 122002 Haryana REGISTERED OFFICE 4, Mangoe Lane Kolkata 700 001 CORPORATE OFFICE 7, Sham Nath Marg Delhi 110 054 DIRECTORS’ REPORT The Members Mumtaz Hotels Limited The Board presents its Thirtieth Annual Report together with the Audited Financial Statement and the Auditor’s Report in respect of the Financial Year ended on 31st March 2020. Financial Highlights The Financial Highlights of the year under review as compared to the previous year are given below: PARTICULARS ` (in million) 2019-20 2018-19 Total Revenue 1005.42 1,071.29 Earnings before Interest, Depreciation and Amortization, Taxes 436.39 496.38 and Exceptional Items (EBIDTA) Finance Costs 0.18 0.32 Depreciation 28.12 22.34 Profit before Tax 408.09 473.72 Current Tax 105.12 135.47 Deferred Tax (18.46) 0.53 Profit after Tax 321.43 337.72 Other Comprehensive Income/(Loss), net of tax (0.47) (0.06) Total Comprehensive Income 320.96 337.66 Profit/ (Loss) Brought forward from earlier years 777.14 626.20 Dividend (154.88) (154.88) Dividend Distribution Tax (31.84) (31.84) General Reserve - - Profit/ Loss Carried Over 911.38 777.14 Performance During the Financial Year under review, the Company’s Total Revenue was ` 1005.42 million as compared to ` 1,071.29 million in the previous year. -

Brief Industrial Profile of Thiruvananthapuram District

Government of India Ministry of MSME Brief Industrial Profile of Thiruvananthapuram District Carried out by MSME-Development Institute Kanjani Road, Ayyanthole P.O Thrissur - 680 003 - Kerala www.msmedithrissur.gov.in MSME HELPLINE: 1800-180-MSME or 1800-180-6763 1 Contents S. No. Topic Page No. 1. General Characteristics of the District 3-5 1.1 Location & Geographical Area 3 1.2 Topography 3 1.3 Availability of Minerals. 4 1.4 Forest 5 1.5 Administrative set up 5 2. District at a glance 6-8 2.1 Existing Status of Industrial Area in the District Thiruvananthapuram 9 3. Industrial Scenario Of Thiruvananthapuram 9-21 3.1 Industry at a Glance 9 3.2 Year Wise Trend Of Units Registered 10 3.3 Details Of Existing Micro & Small Enterprises & Artisan Units In The 11 District 3.4 Large Scale Industries / Public Sector undertakings 11-15 3.5 Major Exportable Item 15 3.6 Growth Trend 15-16 3.7 Vendorisation / Ancillarisation of the Industry 16 3.8 Medium Scale Enterprises 16-1 3.8.1 List of the units in Thiruvananthapuram & near by Area 16-20 3.8.2 Major Exportable Item 20 3.9 Service Enterprises 20 3.9.1 Coaching Industry 20 3.9.2 Potentials areas for service industry 20 3.10 Potential for new MSMEs 21 4. Existing Clusters of Micro & Small Enterprise 21 4.1 Detail Of Major Clusters 21-22 4.1.1 Manufacturing Sector 21 4.1.2 Service Sector 21 4.2 Details of Identified cluster 22 4.2.1 Welding Electrodes - 4.2.2 Stone cluster - 4.2.3 Chemical cluster - 4.2.4 Fabrication and General Engg Cluster - 4.2. -

125 Annexure 1 Statement Showing Particulars of Up-To-Date Capital

Annexure Annexure 1 Statement showing particulars of up-to-date capital, loans outstanding and manpower as on 31 March 2009 in respect of Government companies and Statutory Corporations (Referred to in paragraph 1.7) (Figures in columns 5 (a) to 6 (d) are Rupees in crore) Debt Loans** outstanding at the close of Manpower Paid-up capital* equity Sector & Name of Month and 2008-09 (No. of Name of the ratio for Sl.No. the company/ Year of employees) Department 2008-09 corporation incorporation (as on State Central State Central (Previous 31.3.2009) Govern- Govern- Others Total Govern- Govern- Others Total year) ment ment ment ment (1) (2) (3) (4) 5(a) 5(b) 5(c) 5(d) 6 (a) 6(b) 6 (c) 6 (d) (7) (8) A. Working Government Companies AGRICULTURE & ALLIED Kerala Agro- Machinery 1 Agriculture March 1973 1.61 … … 1.61 … … ... … … 567 Corporation Limited (KAMCO) Kerala Forest Development 0.32:1 2 Forest January 1975 7.02 0.93 … 7.95 1.19 … 1.38 2.57 804 Corporation Limited (0.49:1) (KFDC) Kerala Livestock November 3 Development Board Agriculture 7.33 ... ... 7.33 … … … … … 347 1975 Limited (KLDB) Kerala State Horticultural Products 0.59:1 4 Agriculture March 1989 5.93 … … 5.93 … … 3.50 3.50 139 Development (0.60:1) Corporation Limited (Horticorp) 125 Audit Report (Commercial) for the year ended 31 March 2009 Debt Loans** outstanding at the close of Manpower Paid-up capital* equity Sector & Name of Month and 2008-09 (No. of Name of the ratio for Sl.No. -

Malabar Cements Limited

MALABAR CEMENTS LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1. Preamble Corporate Social Responsibility is a voluntary concept that consists of environmental and social issues with the aim to improve community well-being, respect human rights and to preserve the environment. CSR is also closely linked to the concept of Sustainable Development. The objectives of business should be of three fold, namely profit, people and planet. Business must sub serve the economic, social and the environmental concerns in its growth strategy. This CSR policy will form as a master guide to the implementation of social responsibility measures of Malabar Cements Limited. The Companies Act, 2013 has introduced the idea of CSR to the forefront and through its disclose-or-explain mandate, promoting greater transparency and disclosure to the CSR activities of the Company. Further the Companies (CSR Policy) Rules, 2014 lays down the framework and modalities of carrying out CSR activities, which are specified in, schedule VII of the act. 2. CSR Outlook Malabar Cements Limited is one of the prestigious organizations of the Government of Kerala in Palakkad District. This Company incorporated in the year 1978 is the only integrated grey cement manufacturing plant in Kerala with its captive Limestone mine at Walayar. MCL is a healthy Company, with sound financial base. Company started earning Net profit continuously from the year 1991-92 onwards. Even before the introduction of Company Act 2013, MCL utilized a share of its profit for CSR activities. Many social welfare projects in this regard were implemented from 2012 onwards. In association with Kerala State Security Mission many CSR continuing schemes are implemented. -

Public Sector Under Takings

GOVERNMENT OF KERALA KERALA STATE PLANNING BOARD THIRTEENTH FIVE-YEAR PLAN (2017-2022) WORKING GROUP ON PUBLIC SECTOR UNDER TAKINGS REPORT INDUSTRY AND INFRASTRUCTURE DIVISION KERALA STATE PLANNING BOARD THIRUVANANTHAPURAM MARCH 2017 PREFACE In Kerala, the process of a Five-Year Plan is an exercise in people’s participation. At the end of September 2016, the Kerala State Planning Board began an effort to conduct the widest possible consultations before formulating the Plan. The Planning Board formed 43 Working Groups, with a total of more than 700 members – scholars, administrators, social and political activists and other experts. Although the Reports do not represent the official position of the Government of Kerala, their content will help in the formulation of the Thirteenth Five-Year Plan document. This document is the report of the Working Group on Public Sector Enterprises. The Chairpersons of the Working Group were Sri. Paul Antony IAS, Additional Chief Secretary, Industries Department and Dr. M.P. Sukumaran Nair, Chairman, RIAB. The Member of the Planning Board who coordinated the activities of the Working Group was Dr. Jayan Jose Thomas. The concerned Chief of Division was Sri. Joy N.R. Member Secretary FOREWORD Industrial development is crucial for the growth of any nation. It is also linked to the modernization of agriculture, development of science and technology, entrepreneurship, self- reliance in defense production, success in international trade, efficient utilization of natural resources, alleviation of poverty and unemployment and increase in per capita income and standard of living of the people. Expansion of industry and Services is essential for economic development and growth, as these are major enablers of productivity increases. -

MALABAR CEMENTS LIMITED (A Govt

MALABAR CEMENTS LIMITED (A Govt. of Kerala Undertaking) WALAYAR, PALAKKAD DISTRICT, KERALA-678 624 Ph: 2862266/73/74 Fax: 0491-2862230 Website: www.malabarcements.com E.mail:[email protected] NOTICE INVITING TENDER Tender No. MCL/02/PRT/830/2020 Date.05.05.2020 Separate tenders are being invited by the Managing Director, on behalf of the Malabar Cements Ltd,Walayar(P.O) Palakkad 678624,Kerala India, through electronic tender (e-tender) for the Works/Service mentioned in the list given in next page from eligible and resourceful bidders having sufficient credential and financial capability for execution of Works /Service as per the tender. Intending bidders desirous of participating in the e-tender are to login to the website www.etenders.kerala.gov.in (the official website of kerala Government e portal) Contractors/bidders willing to take part in the process of e-tender are required to obtain Digital Signature Certificate (DSC) from any of the authorized ‘Certifying Authorities’ (CA) The prospective bidders may contact the e-tendering State Level Help desk located Thiruvananthapuram Ph: 0471 2577088, Kannur Ph: 0497 2764188 , 0497 2764788 and Malappuram Ph: 0483 7732941 on any working day within working hours for any query on e-tendering. Intending bidders are required to download the e-tender documents directly from the website www.etenders.kerala.gov.in . Tender documents consisting of Technical specification, schedule of quantities, PAGE NO. 1 commercial terms and conditions etc. MCL reserves the right to reject any or all tenders without assigning any reason thereof. If any clarification required, tenderers may also send their queries to the e-mail [email protected] . -

Recruitment and Training of Managers in the Public Sector Concerns in Kerala

RECRUITMENT AND TRAINING OF MANAGERS IN THE PUBLIC SECTOR CONCERNS IN KERALA Thesis Submitted to the Univetsity of Cochin for the award of the Degree of Doctor of Philosophy in Management under the faculty of Social Sciences by N. CHANDRASEKHARAN PILLAI under the Supervision of Dr. N. PARAMESWARAN NAIR SCHOOL OF MANAGEMENT STUDIES UNIVERSITY OF COCHIN COCHIN - 682 022 MARCH 1983 PREFACE Public undertakings have been assigned a significant role to play in the systematic socio-eco nomic development of India. My interest in the subject was kindled while I was doing my Masters Diploma in Public Administration at the Indian Institute of Public Administration, New Delhi during 1960-61. It was further strengthened by my teaching of the subject in different courses offered by me at the School of Manage» ment Studies and in several programmes organised by various voluntary and training organisations like the Institute of Management in Government, Trivandrum, Centre for Management Development, Trivandrum, etc. The several years in which I served as a member of the faculty in the School of Management Studies, University of Cochin,gave me the opportunity to come into close contact with different public sector concerns and their managers at various levels. This rich opportunity gave me a better insight into the problems faced by these concerns. The present study is a result of the interest so developed. In completing the study I am thankful to Dr. N. Parameswaran Nair, Professor and Director, School of Management Studies, University of Cochin for his invaluable guidance and constant encouragement. ii My thanks are also due to all my colleagues in the School of Management. -

Government of Kerala Circular

GOVERNMENT OF KERALA General Administration (Political C) Department CIRCULAR No. 31519/Pol.C3/76/GAD. Dated, Trivandrum, 14th April 1977 Sub:- Resettlement of army reservists in civil life – Instructions issued. Ref:- Letter No. 1761/DGR/EMP/RES-3 dated 23-2-1976 from the Director General of Resettlement, Government of India, Ministry, of Defense, Ministry Azad, DHQ.P.O., New Delhi. The Director General of Resettlement has requested all State Governments to consider the desirability of impressing upon all Departments including Public and Private Sector Undertakings and autonomous bodies to recruit army reservists to the maximum extent possible under the Rules. As per Government of India letter No. 1902/D (AG-11/67) dated 13-4-1967, once a person acquires the status of a reservist, he is automatically treated as an ex-serviceman. Accordingly the concession of preference in appointment available to ex-servicemen in general is available to reservists also. However it is noticed that the recruiting authorities are reluctant to appoint reservists because of the fact that they are frequently called for attending refresher courses there by sousing hardship to the institutions/ establishments where they were taken. The Director General Resettlement as stated that the period of reserve liability of Reserve Forces who were liable to be recalled for duty in case of emergency has now been substantially reduced and that the requirement of refresher training has also been substantially reduced and that the requirement of refresher training has also been dispensed and their employers will be able to have their services continuously without much disruption. The existing system of reserves has now been modified as the enrolment in the army will be made only on the following two periods of engagement with effect from 1-2-1976: 1. -

O4jcr3f,O Cs4 4

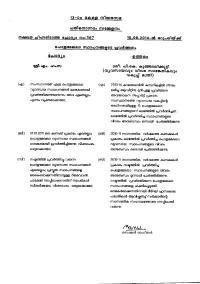

13-Oo O60F (T,lQrocue olo)lo(l)cmco (ruo4og(I)o magto !.n6rpo1so6np oaloBro mo:567 10.08.2014-d oo)olslctdd, OoJC@COOlelC (tu65^lmaEn6tf,rc r,r^r'llm6- o4Jcr3f,o gGnDoo l&1."Oo. .oomJ [@1. o-n.o6. 6]durooen6o]g,l ((UjoJfiuocor(U)o ojloJo fluoob(D'l6oJlo clet*J ornol) (.O) (ru.mmc.n(o|o" oO@ 6)drcpoo6lelc (€) 2013-14 aoeJ@eloird d,mrrlaEld (rtcna" o{o(rDc(o) o\rl}cdl(r)arBoa el.eo@oc(ot er44 o|onrl{lco qc6"g@ @oiaoro)cD @or6(dE@(mo6rB(rro.(sooo{]o(oqco rdlootoelc6(T)[email protected]. .OCrOo O$dlOOC6)CC@c; (TUomtOCCnOlOllt o5otm)cOr Oa.dlOr$ croutcDo(otqee 15 o.rcpco6lelc cDocdloarBec6m- e]cBolold @odorDl4(U): eicc(dotd @ol(a(drdl4 m)ocoJo@Eq6s olcx.do Grd(o6Dtou)o 6t(mc(on q-td@|otadlefilo. (srjl) 0101.2011 oer 6mD6" @acoo o4o.o)sco (5nl) 2O1Oll ducn!@djle o6.sooro 6,5rD66,oa o.rcp(Da|elcoJ.llmjca,(lloonrrr@Bo8 etocooaccoroil(i@od@ot4o.,rcpcooreo ercG6@occor@,od(orol-drooo:ojlcoocorno o{crcuc(o .y\)ocorfi)eBgosoLx@. elGlocdccoc; GrocF6tufitDo 66rBCCDl Odd(t'roJld6(ro, (ad) (n.E(oroid @o6oril4 orcrm (.n ) 2010-11 (rucfillrorole otd.so(oto 65rD€6sA 6k1lcprlo6leDo{ormiceo)mlocdJ(n6t3ua @ac(do(r)qoiotd@ol6(od4 .6l6xo9loo; @rru(o cruocoJoeBo€ ooJcpco6)tac ffuocorn@Bgos olo(do elcl36@oc6fi)ot(r)cc{@ doooloxd Grdco6nicr\l). qcmcst cdrEoroJlolacrn. orco6s-(r)sqjleJc6cm(otfil(r)soJdld,d m.ry@loJlad@o6(o|6t6(rDodrcgcootelc arulla(o16ooc;ol(6rjc.(6" eJBlocaccoc; (ruocdlodrBogoaoiloggoojl elcc6(.OC6fin(6t(r)c(D, .id"e/ hgfu4cel dcD.diloua Gqot.gdaf nud@c(dl6r0 mrccnroojla fu.ocaoconrcos (r)sqjleloddl o(acrE, Cs4 4- oald,graa 6]cdnlaud GFm6 mDo - | Sl No Name of Company KERALA STATE INDUSTRIAL DEVELOPMENT ]. -

Government Of'kerala

GOVERNMENT OF'KERALA F'INANCE (BUDGET WING. A) DEPARTMENT CIRCULAR No.09/2021lX'in. Dated, Thiruvananthapuram, 27th J anrtary 2021. Sub:- Budget 2021-22 - Budget documents - Distribution to the Heads of Departments - Instructions - Issued. Arrangements have been made for the printing and supply of the Budget documents for 2021-2022 to all concerned. The Superintendent of Government Presses, Thiruvananthapuram will distribute the documents to the Heads of Departments and others in accordance *ith the fixed scale of supply. He will also distribute one set each containing all documents to the Public Sector Undertakings. All Heads of Departments/Public Sector Undertakings are therefore directed to collect the copies of budget documents 2O2l-22 from the Government Press, Thiruvananthapuram. The Heads of Departments will note that though there are three volumes of Demands for Grants, they will be supplied with the volumes concemed with their Deparffnents outlay only. One set of documents for the purpose of distribution will consist of the following items. l. Demands for Grants (Relevant Volumes only) 2. Revenue Budget 3. Explanatory Memorandum 4. Works Appendix-Vol.I ,. 5. Debt Head Budget 6. Budget Speech (English & Malayalam) 7. Appendix IV (Provisions earmarked to Local Self Government Institutions) 8. Thirteenth Five Year Plart 2017- 2022 - 5ft Year's Programm e - 2021-22 9. - Annual Plan202l-22 10. Vote on Account In addition to the items mentioned above, all Heads of Departments and others would be supplied with one copy each of the following documents th-at are meant for restricted Q supply. 1. Appendix I (Details of staff) 2. Annual Financial Statement 3. -

Social Welfare/Health and Family Welfare/Labour And

Appendices Appendix V (Reference: Paragraph 1.4.1 ; Page 5) Part A – Government Accounts I. Form of Annual Accounts The accounts of the State Government are prepared in two volumes viz., the Finance Accounts and the Appropriation Accounts. The Finance Accounts present the details of all transactions pertaining to both receipts and expenditure under appropriate classification in the Government accounts. The Appropriation Accounts, present the details of expenditure by the State Government vis-à-vis the amounts authorised by the State Legislature in the budget grants. Any expenditure in excess of the grants requires regularisation by the Legislature. Part B - List of terms used in the Chapter-I and basis for their calculation Terms Basis for calculation Buoyancy of a parameter Rate of Growth of the parameter GSDP Growth Buoyancy of a parameter (X) Rate of Growth of the parameter (X) with respect to another Rate of Growth of the parameter (Y) parameter (Y) Rate of Growth (ROG) [(Current year Amount/previous year Amount) –1] * 100 Development Expenditure Social Services + Economic Services Weighted Interest Rate Interest Payment / [(Amount of previous year’s Fiscal Liabilities + Current year’s Fiscal Liabilities)/2]*100 Interest spread GSDP growth – Weighted Interest Rate Interest received as per cent (Interest Received / Closing balance of Loans and to outstanding loans and Advances)*100 advances Revenue Deficit Revenue Receipt – Revenue Expenditure Fiscal Deficit Revenue Expenditure + Capital Expenditure + Net Loans and Advances – Revenue Receipts – Miscellaneous Capital Receipts Primary Deficit Fiscal Deficit – Interest Payments Balance from Current Revenue Receipt minus Plan grants and Non-Plan Revenue Revenue (BCR) Expenditure excluding debits under 2048-Appropriation for Reduction or Avoidance of Debt 139 Audit Report (Civil) for the year ended 31 March 2005 Appendix VI List of Autonomous Institutions which had not rendered accounts for the year 2004-05 (Reference: Paragraph 1.7.8; Page 16) Sl.