Residential City Profile Berlin En Germany

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

STADTTEILPROFIL 2015 Malchow, Wartenberg Und Falkenberg (01)

STADTTEILPROFIL 2015 Malchow, Wartenberg und Falkenberg (01) Teil 2 – Ziele und Handlungsfelder Naturschutzstation Malchow Tierheim Berlin, Falkenberg Hochlandrinder Barnimer Feldweg Impressum Herausgeber: Bezirksamt Lichtenberg von Berlin Arbeitsgruppe Sozialraumorientierung Koordination: OE Sozialraumorientierte Planungskoordination Bearbeitung: Frau Pöhl Bildnachweis Titelseite: Fotoverein, Olm, Bezirksamt Lichtenberg, Bezirksamt Lichtenberg Bearbeitungsstand: Berlin, 31.August 2016 2 STADTTEILPROFIL 2015 – Malchow, Wartenberg, Falkenberg Inhaltsverzeichnis 0. Einleitung .................................................................................................................................................... 5 1. Zusammenfassung: Potenziale und Herausforderungen ........................................................................... 6 2. Handlungsfelder und Strategien für den Stadtteil ...................................................................................... 8 2.1 Wohnen und Wohnumfeld ................................................................................................................. 8 2.2 Lebensqualität ................................................................................................................................... 9 2.3 Verkehr und Mobilität ....................................................................................................................... 11 3. Übersicht: Geplante Maßnahmen und Maßnahmenvorschläge für den Stadtteil ................................... -

Köpenick <> Ostkreuz Ersatzverkehr Mit Bussen

x3 Köpenick <> Ostkreuz 25. 6. 2020 (Do) – 13. 7. 2020 (Mo) 4 Uhr 1.30 Uhr Ersatzverkehr mit Bussen Replacement service by bus S 3 fährt bis Wuhlheide und bis Rummelsburg. Sehr geehrte Fahrgäste, vom 25.06.2020 (Do) 4 Uhr bis 13.07.2020 (Mo) 1:30 Uhr wird in Karlshorst das historische Bahnsteigdach wieder aufgebaut. Zeitgleich dazu wird in Karlshorst eine Lärmschutzwand errichtet und das Gleislayout in Rummelsburg verändert. Die S3 kann im Abschnitt Wuhlheide <> Karlshorst <> Rummelsburg nicht fahren. Ersatzverkehr mit Bussen wird zwischen: 0b S3 Köpenick <> Tram-/Nachtbushaltestelle „Freizeit- und Erholungszentrum (FEZ)“ <> Karlshorst <> U-Bf. Tierpark (Zusatzhalt) <> Bushaltestelle „Michiganseestraße“ (Halt für Betriebsbahnhof Rummelsburg <> Rummelsburg <> Ostkreuz eingerichtet. Bitte steigen Sie zwischen der S3 (Erkner <> Köpenick <> Wuhlheide) und dem Ersatzverkehr mit Bussen in beiden Fahrtrichtungen in Köpenick um. Zwischen dem Ersatzverkehr und der S3 (Rummelsburg <> Ostbahnhof/ Spandau) können Sie sowohl in Rummelsburg, als auch in Ostkreuz umsteigen. Im Abschnitt Rummelsburg <> Ostkreuz fahren die S3 und der Ersatzverkehr mit Bussen parallel. Fahrgäste von Wuhlheide in Richtung Karlshorst/Ostkreuz nutzen bitte zuerst die S3 in Richtung Erkner bis Köpenick (1 Station) und steigen dort in den Ersatzverkehr mit Bussen um. In der Gegenrichtung nutzen Fahrgäste nach Wuhlheide zunächst den Ersatzverkehr mit Bussen bis Köpenick und steigen dort in die S3 nach Wuhlheide um. Bitte beachten Sie in Karlshorst die wechselnden Abfahrtshaltestellen des Ersatzverkehrs. In Betriebsbahnhof Rummelsburg halten die Busse des Ersatzverkehr nicht direkt am S-Bahnhof, sondern an der Bushaltestelle „Michiganseestraße“ in der Sewanstraße. In Ostkreuz fährt die S3 nach Rummelsburg von Gleis 5 (Bahnsteig stadteinwärts). Die S75 wird während dieser Bauarbeiten mit allen Fahrten bis/ab Ostbahnhof verlängert. -

Vorhaben 2019 Im Bezirk Marzahn-Hellersdorf Zur Verbesserung Der Barrierefreiheit

Vorhaben 2019 im Bezirk Marzahn-Hellersdorf zur Verbesserung der Barrierefreiheit Bauvorhaben, Straße Art der Arbeiten Stadtteil (Bezirksregion) Sozialraum Greifswalder Str. von Hönower Str. bis Taxusweg Neubau Gehweg Süd Mahlsdorf Mahlsdorf-Nord Bansiner Straße vor Seniorenheim Neubau Gehweg Hellersdorf-Süd Kaulsdorf Nord I Florastraße am Seniorenheim Neubau Gehweg Mahlsdorf Mahlsdorf-Nord Lübzer Str. 9 Gehweg und GWÜ Mahlsdorf Mahlsdorf-Nord Melanchthonstr. 96 Lückenschluss Mahlsdorf Mahlsdorf-Nord Terwestenstraße 11 bis Dahlwitzer Str. Gehweg Mahlsdorf Mahlsdorf-Nord Köpenicker Straße - Südbereich Gehweg Biesdorf Biesdorf-Süd Dohlengrund von Grabensprung bis Anschluss U-Bahn Neubau Gehweg Biesdorf Biesdorf-Süd Maratstraße Gehweg Biesdorf Oberfeldstraße Ringenwalder Straße 23 Gehweg Sanierung Marzahn-Mitte Marzahn-Ost Marzahner Franz-Stenzer-Straße 53-55 Gehweg Sanierung Marzahn-Mitte Promenade Kemberger Straße - Haltestelle Gehweg Sanierung Marzahn-Mitte Marzahn-Ost Alt-Mahrzahn Gehweg Sanierung Marzahn-Süd Alt-Marzahn Rudolf-Leonhardt-Str. (MUF) Gehweg Marzahn-Mitte Ringkolonnaden Straße An der Schule zwischen Zufahrt und Wendehammer Pestalozzistraße Schulweg (provisorisch in Asphalt) Mahlsdorf Alt-Mahlsdorf Hultschiner Damm Lückenschlüsse 5 Teilstücke Gehweg Mahlsdorf Mahlsdorf-Süd Wielandstr. 9-10 Gehweg Mahlsdorf Mahlsdorf-Süd Kiekemaler Str. 11-12 Gehweg Mahlsdorf Mahlsdorf-Süd Feldberger Ring 6 Gehweg barrierefreie Anbindung Hellersdorf-Süd Kaulsdorf Nord II Hellersdorfer Str. 205-207 Gehweg Hellersdorf-Süd Kaulsdorf Nord II Florastr. -

Steglitz-Zehlendorf

Bezirksamt Steglitz-Zehlendorf Steglitz-Zehlendorf Ein Wegweiser durch den Bezirk Sie fi nden uns 4x in Berlin Steglitz- Zehlendorf HIER SIND WIR ZUHAUSE · Versorgung aller Pfl egegrade · Abwechslungsreiches Beschäftigungs- · Spezielle Wohnbereiche für und Veranstaltungsangebot Menschen mit Demenz · Persönliche Möblierung ist gerne möglich Rufen Sie uns an oder kommen Sie vorbei, wir beraten Sie gerne persönlich und individuell. Infos zu unseren Veranstaltungen erhalten Sie im jeweiligen Haus. Vitanas Senioren Centrum Am Bäkepark Vitanas Senioren Centrum Schäferberg Bahnhofstraße 29 | 12207 Berlin Königstraße 25 – 27 | 14109 Berlin (030) 754 44 - 0 (030) 80 10 58 - 0 Vitanas Senioren Centrum Am Stadtpark Vitanas Senioren Centrum Rosengarten Stindestraße 31 | 12167 Berlin Preysingstraße 40 – 46 | 12249 Berlin (030) 92 90 16 - 0 (030) 766 85 - 5 www.vitanas.de Interview mit der Bezirksbürgermeisterin Cerstin Richter-Kotowski „Ich möchte den Menschen auf Augenhöhe begegnen!“ Athene-Grundschule angesprochen wurde, im Bürgertreffpunkt eine Ausstellung zu IM GESPRÄCH machen, habe ich mir Gedanken darüber gemacht, was ich als Lebenskundelehrerin mit meiner Klasse dazu beitragen kann. Ich habe mich gefragt, was ein Bürgertreff ist und nach einem Synonym dafür gesucht und bin auf den Begriff „Nachbarschaft“ ge- stoßen. Die Kinder sammelten zum Thema Nachbarschaft Wörter wie Toleranz, Hilfe, Unterstützung, Rücksichtnahme, Kommuni- kation, Alt und Jung zusammen, Sicherheit. Dabei war es wichtig, mit den Kindern die Unterschiede heraus zu arbeiten zwischen der Nachbarschaft, dort wo sie leben, und die der Schule. Damit die Kinder eine Vor- Eröffnung der Dahlem Route am 29.06.2018: stellung davon entwickeln konnten, was ein Henner Bunde, Staatssekretär der Senatsver- Bürgertreff ist, haben wir diesen im Bahn- waltung für Wirtschaft, Energie und Betriebe, Bezirksbürgermeisterin Cerstin Richter-Ko- hof Lichterfelde West besucht und dort Fo- towski und Marit Schützendübel, Direktorin tos gemacht. -

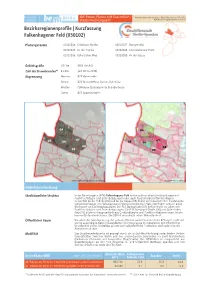

Kurzfassung Falkenhagener Feld

Abt. Bauen, Planen und Gesundheit | Kontakt: Karsten Kruse (Bau 2 Stapl A8) | (030) 90279-2191 | Stadtentwicklungsamt [email protected] Bezirksregionenprofile | Kurzfassung Falkenhagener Feld (050102) Planungsräume 05010204 Griesinger Straße 05010207 Darbystraße 05010205 An der Tränke 05010208 Germersheimer Platz 05010206 Gütersloher Weg 05010209 An der Kappe Gebietsgröße 697 ha (RBS-Fläche) Zahl der Einwohnenden* 41.435 (am 30.06.2018) Abgrenzung Norden: BZR Hakenfelde Süden: BZR Brunsbütteler Damm, Bahnlinie Westen: Falkensee (Landesgrenze Brandenburg) Osten: BZR Spandau Mitte 04 04 05 07 07 06 05 06 08 08 09 09 Digitale farbige Orthophotos 2017 (FIS-Broker) Ausschnitt ÜK50 (FIS-Broker) Gebietsbeschreibung Stadträumliche Struktur In der Bezirksregion (BZR) Falkenhagener Feld finden sich vor allem Großsiedlungen mit Punkthochhäuser und Zeilenbebauungen aber auch freistehende Einfamilienhäuser. In den PLR An der Tränke (05) und An der Kappe (09) finden sich hauptsächlich freistehende Einfamilienhäuser. Im Planungsraum (PLR) Germersheimer Platz (08) finden sich vor allem Blockrand- und Zeilenbebauungen. Der PLR Darbystraße (07) definiert sich vor allem mit Punkthochhäuser und Zeilenbebauungen. Die PLR Griesinger Straße (04) und Gütersloher Weg (06) bestehen hauptsächlich aus Großsiedlungen und Punkthochhäusern sowie freiste- henden Einfamilienhäusern. Die BZR ist ein nahezu reiner Wohnstandort. Öffentlicher Raum Vor allem der Spektegrünzug, der sich von Westen nach Osten durch die BZR zieht, stellt mit seinen ausgiebigen -

Renaming Streets, Inverting Perspectives: Acts of Postcolonial Memory Citizenship in Berlin

Focus on German Studies 20 41 Renaming Streets, Inverting Perspectives: Acts Of Postcolonial Memory Citizenship In Berlin Jenny Engler Humbolt University of Berlin n October 2004, the local assemblyman Christoph Ziermann proposed a motion to rename “Mohrenstraße” (Blackamoor Street) in the city center of Berlin (BVV- Mitte, “Drucksache 1507/II”) and thereby set in train a debate about how to deal Iwith the colonial past of Germany and the material and semantic marks of this past, present in public space. The proposal was discussed heatedly in the media, within the local assembly, in public meetings, in university departments, by historians and linguists, by postcolonial and anti-racist activists, by developmental non-profit organizations, by local politicians, and also by a newly founded citizens’ initiative, garnering much atten- tion. After much attention was given to “Mohrenstraße,” the issue of renaming, finally came to include the so-called African quarter in the north of Berlin, where several streets named after former colonial regions and, most notably, after colonial actors are located. The proposal to rename “Mohrenstraße” was refused by the local assembly. Nev- ertheless, the assembly passed a resolution that encourages the “critical examination of German colonialism in public streets” (BVV-Mitte, “Drucksache 1711/II”) and, ultimately, decided to set up an information board in the so-called African quarter in order to contextualize the street names (BVV-Mitte, “Drucksache 2112/III”). How- ever, the discussion of what the “critical -

Integriertes Entwicklungskonzept Für Das Gebiet Falkenhagener Feld West (Quartiersbeauftragte: Gesop Mbh)

Entwicklungskonzept Falkenhagener Feld – West Oktober 2005 Anlage 1 j Integriertes Entwicklungskonzept für das Gebiet Falkenhagener Feld West (Quartiersbeauftragte: GeSop mbH) 1. Kurzcharakteristik des Gebiets Die Großsiedlung Falkenhagener Feld wurde aufgrund ihrer Größenordnung durch das Stadtteilmanagementverfahren in zwei Teilgebiete unterteilt. Aus diesem Grund gibt es vielfach Statistiken/Daten, die über die Abgrenzung der Teilgebiete hinausgehen. Die Großsiedlung Falkenhagener Feld – West befindet sich beidseitig der Falkenseer Chaussee, westlich der Zeppelinstraße, östlich des „Kiesteiches“, südlich der Pionierstraße und nördlich der Spektewiesen. Bebauungsstruktur Seit dem Jahre 1963 (Baubeginn) wurde auf dem Gebiet des ehemaligen Kleingartenlandes eine Großsiedlung gebaut mit Großsiedlungseinheiten der frühen 60er und 70er Jahre, aus Zeilenbauten, Einzelhäusern und bis zu siebzehngeschossigen Punkthochhäusern. Ab 1990 wurde das Falkenhagener Feld durch Geschosswohnungsbau nachverdichtet; die großzügigen grünen Zwischenräume reduzierten sich. Neben dem Geschosswohnungsbau erstrecken sich auch Siedlungseinheiten aus Einfamilienhäusern durch das gesamte Gebiet. Heute ist die Siedlung (Bereich Ost und West)) mit 56 EW/ha (Vergleich: Spandau 23,5 EW/ha) ein dicht besiedeltes Gebiet, verfügt aber auf Grund der Gesamtgröße, dem relativ hohen Grünanteil und trotz der Nachverdichtung über aufgelockerte Baustrukturen. Mit rund 10 000 Wohneinheiten und knapp 20 000 Einwohnern ist die gesamte Großsiedlung Falkenhagener Feld nach dem Märkischen Viertel und der Gropiusstadt die drittgrößte Großsiedlung in Berlin (West). Die Siedlung wird durch die Osthavelländische Eisenbahn in die beiden Bereiche Falkenhagener Feld Ost und West geteilt, die jeweils als eigenständige Gebiete für das Stadtteilmanagementverfahren ausgewiesen wurden. Wohnungsbestand Das Falkenhagener Feld West verfügt im Geschosswohnungsbau über knapp 4000 Wohneinheiten. Dieser Bestand hat sich in den letzten Jahren massiv verringert. Durch den Verkauf von Wohnungen sind Eigentumswohnungen entstanden. -

Mitte Friedrichshain-Kreuzberg Pankow

► Vorwort 5 Mitte 1 Das »himmelbeet« in Wedding 6 2 Einkäufen im Mini-Kaufhaus in Wedding 8 3 Smart Eating in der Data Kitchen 10 4 Bibliothek am Luisenbad 12 5 Gleim-Oase: die grüne Insel im Wedding 14 6 Leckere Burger in ausgefallener Location 16 7 Franzose mit witzigem Menü-Konzept 18 8 Cocktail trinken in einer versteckten Bar 20 9 Katz Orange: Restaurant in alter Brauerei 22 10 Staunen in der Wunderkammer Olbricht 24 11 Die Dachterrasse des Hotel AMANO 26 12 Brötchen holen in Sarah Wieners Bio-Bäckerei 26 13 Cowshed Spa im Soho House 28 14 Tadshikische Teestube: märchenhaft Tee genießen 30 15 Kennedy Museum: in der Jüdischen Mädchenschule 32 16 Beeindruckende Boros Collection 34 17 Entspannen über den Dächern der Stadt 36 18 Alter Grenzturm am Potsdamer Platz 36 19 Ein Tag Luxus, bitte! 38 Friedrichshain-Kreuzberg 20 Sonnenuntergang auf der Modersohnbrücke 40 21 Das beliebteste Outlet der Stadt 42 22 Minigolf bei Schwarzlicht 44 23 Street Food Thursday 46 24 Panoramablick über Kreuzberg 46 25 Akupunktur, die sich jeder leisten kann 47 26 Ein Besuch im Pfefferhaus 48 27 Die kleinste Disko der Welt 50 28 Crazy Hot Dogs 50 29 Kalifornien zum Schlecken 52 Pankow 30 Erinnerungen in der Alten Bäckerei Pankow 54 31 Die Ruine des Kinderkrankenhauses in Weißensee 56 32 Lustige Tischtennis-Bar im Prenzlauer Berg 56 33 Türkische Küche - modern interpretiert 58 34 Stulle essen bei Suicide Sue 60 35 Onkel Philipp's Spielzeugwerkstatt 62 36 Verwunschene Oase auf dem Friedhof 64 37 Zur Ruhe kommen im Stadtkloster Segen 66 38 Entspannen im Ruhepool -

Die Berliner Erreichen

Preisliste Nr. 34, Print und Online, gültig ab 1.1.2021 Anzeigen Beilagen Berliner Woche Online Buch L01 Blankenfelde Gezielt werben! Frohnau Französisch Karow Buchholz Hermsdorf Lübars Heiligensee Stadtrandsiedl. Die Berliner erreichen. Rosenthal Malchow Waidmannslust Märkisches L29 Wilhelmsruh Blankenburg Borsigwalde Viertel Niederschönhausen Wartenberg L30 Heinersdorf Konradshöhe Malchow Falkenberg Wittenau Mit 30 Lokalausgaben Hakenfelde L04 Neu-Hohenschönhausen Tegel Reinickendorf Pankow L02 L28 Weißensee L05 alle einzeln buchbar und Marzahn Wedding Gesundbrunnen Falkenhagener L03 Alt-Hohenschönhausen frei kombinierbar Feld Haselhorst Charlottenburg L25 Prenzlauer Berg Spandau -Nord L06 Hellersdorf Siemensstadt Moabit Fennpfuhl Staaken L08 Lichtenberg L07 L26 Zur Wochenmitte Hansaviertel Mitte Friedrichshain Westend L10 Biesdorf Tiergarten Friedrichsfelde Mahlsdorf Wilhelmstadt L09 Charlottenburg Rummelsburg vor den einkaufsstarken Tagen Kreuzberg L11 Kaulsdorf Halensee L22 Wilmersdorf Schöneberg Alt-Treptow Karlshorst L23 L24 Neukölln Gatow Schmargendorf Grunewald Tempelhof L16 Plänterwald Friedenau Oberschöneweide L27 Friedrichshagen L20 Niederschöneweide Steglitz L17 Britz Kladow Rahnsdorf Dahlem Baumschulenweg Köpenick Nikolassee Johannisthal Mariendorf L15 L12 Adlershof Zehlendorf Lankwitz L19 L13 Grünau L21 Buckow Gropiusstadt Müggelheim Altglienicke Lichterfelde L14 Marienfelde Wannsee Rudow Bohnsdorf L18 Schmöckwitz Lichtenrade Nr. Lokalausgaben Auflage 4c-mm-Preis/€ L01 Pankow-Nord 36.920 1,74 Die Berliner Woche erscheint -

Und Informations-Dialog 2018 Baumaßnahmen Im Netz Der Berliner S-Bahn 2018 - 2020

2. Bau- und Informations-Dialog 2018 Baumaßnahmen im Netz der Berliner S-Bahn 2018 - 2020 DB Netz AG | I.NP-O-D-BLN(BS) + I.NM-O-F(S) | Berlin | 17.07.2018 Übersicht Regionalbereich Ost – Netz Berliner S-Bahn Bauschwerpunkte 2018 Ersatzneubau SÜ Rhinstraße + ESTW+ZBS S7 Ost SEV Lichtenberg–Springpfuhl/ Wuhletal Wochenenden April bis Juni + Dezember 2018 Brückenarbeiten S2 Nord + Neubau SÜ BAB114 SEV Lichtenberg–Ahrensfelde/ Wartenberg SEV Blankenburg–Karow + Blankenburg- 19.10.–25.10.2018 Schönfließ SEV Sprinpfuhl–Wartenberg/ Ahrensfelde 26.06.–16.07.2018 20.07.–23.07.2018 SEV Blankenburg–Buch + Blankenburg- Schönfließ 16.07.–23.07.2018 SEV Blankenburg–Buch Ersatzneubau 23.07.–17.08.2018 EÜ Thälmannstr. + Entflechtung S-/F- ZBS S5 West Schienenauswechslung Bahn Bf Strausberg SEV Westkreuz–Spandau SEV Tiergarten–Charlottenburg SEV Mahlsdorf– 13.08.–16.08.2018 (in Prüfung 23.07.-03.08.2017 Strausberg Nord Verschiebung IBN nach 01/2019) 23.11.–29.11.2018 Umbau Ostkreuz – Neubau Bahnsteig Karlshorst Ibn Endzustand 4-gleisigkeit SEV Rummelsburg–Wuhlheide ZBS S7 West + Begegnungsabschn. Potsdam SEV Ostkreuz–Karlshorst 06.07.–16.07.2018 SEV Wannsee–Potsdam 02.11.–12.11.2018 kein Verkehrshalt Karlshorst 03.08.–06.08. + 10.08.–13.08. + 14.12.–17.12.2018 SEV Alexanderplatz–Lichtenberg 06.07. – 06.08.2018 SEV Westkreuz–Wannsee + Babelsberg–Potsdam 02.11.–05.11. + 09.11.–12.11.2018 eingleisig Wuhlheide – Karlshorst 31.08.–03.09.2018 06.08. – 15.08.2018 SEV Westkreuz–Grunewald 16.11.–19.11.2018 Ende Neubau EÜ Sterndamm + Neubau PT Schöneweide bis 2021 bis 20.08.2018 halbseitg. -

Museum Pankow – Gedenktafeln 1 Gedenk

Museum Pankow – Gedenktafeln Gedenk- und Informationstafel zur Geschichte des Straßenbahnbetriebshofs Niederschönhausen Dietzgenstraße 100, 13158 Berlin Einweihung: 03.11.2020 Abb.: Straßenbahnbetriebshof - Verwaltungsgebäude des Bahnhofs III der Großen Berliner Straßenbahn in Niederschönhausen, um 1910 © Museum Pankow / Foto: Max Skladanowski: Gedenk- und Informationstafel zur Geschichte des Bürgerparks Pankow und seines Obergärtners Wilhelm Perring (1838 Ampfurth – 1906 Berlin) Bürgerpark Pankow, Wilhelm-Kuhr-Straße 9, 13187 Berlin Einweihung: 28.08.2020 Abb.: Porträt von Obergärtner Wilhelm Perring um 1865 © Museum Pankow Gedenk- und Informationstafel in Erinnerung an Schuldirektor und Schulreformer Carl Louis Albert Pretzel (1864 – 1935) Journalist und Publizist Sebastian Haffner (1907 – 1999) Kultur- und Bildungszentrum Sebastian Haffner Prenzlauer Allee 227/228, 10405 Berlin Einweihung: 17.01.2019 Abb.: Sebastian Haffner auf der 30. Frankfurter Buchmesse, 1978 © BArch, N2523/230 Bild 34 / dpa-Wieseler, Heinz 1 Museum Pankow – Gedenktafeln Gedenkstele für Marianne Schadow und Johann Gottfried Schadow geschaffen von Liz Mields-Kratochwil, Bildhauerin Vor dem Grundstück Hauptstraße 43/44, 13127 Berlin Einweihung: 16.10.2018 Abb.: Johann Gottfried Schadow (1764 – 850), Bildhauer, Begründer der Berliner Bildhauerschule und Direktor der Königlich Preußischen Akademie der Künste und seine Frau Marianne Schadow, geb. Devidels (1758 – 1815) © Museum Pankow Gedenktafel und Benennung einer Grünfläche in Erinnerung an Werner Klemke (12.03.1917 -

Bezirksamt Treptow Abteilung Bau-, Wohnungswesen Und Umwelt Stadtplanungsamt

Bezirksamt Treptow Abteilung Bau-, Wohnungswesen und Umwelt Stadtplanungsamt Begründung zum Bebauungsplan XV – 39 a für die künftige Rixdorfer Straße in Verlängerung der Karlshorster Straße und parallel zum Industriegleis im Bezirk Treptow, Ortsteil Niederschöneweide. Begründung zum Bebauungsplan XV-39a _________________________________________________________________________________ Inhaltsverzeichnis I. Planungsgegenstand...........................................................................................................4 I.1. Veranlassung und Erforderlichkeit.....................................................................................4 I.2. Plangebiet .........................................................................................................................4 I.2.1. Bestand .............................................................................................................4 I.2.2. Planerische Ausgangssituation ...........................................................................6 II. Planinhalt..........................................................................................................................8 II.1. Entwicklung der Planungsüberlegungen............................................................................8 II.2. Intention des Planes/Planungsziele....................................................................................8 II.3. Wesentlicher Planinhalt....................................................................................................8 II.4.