Annu Al Repor T

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annu Al Repor T and Sus Tainabilit Y

SUSTAINABILITY REPORT ANNUAL REPORT AND 2014 “Overall, KONGSBERG had a good year in 2014, with good earnings and cash flows, growth in revenues, and record-high orders” 1 Introduction 8 Directors’ Report and Financial Statements 86 Corporate Governance 100 Shareholder’s information 104 Sustainability Report 149 Financial calendar and contact information CONTENT – ANNUAL REPORT AND SUSTAINABILITY REPORT 2014 Cover Key figures 2014 8 Directors’ Report and 86 Corporate Governance 104 Sustainability Report Financial Statements 87 The Board’s Report on 104 Content 1 Introduction 9 Short summary Business Corporate Governance 106 Introduction 2 Extreme Areas 88 Policy – Kongsberg Gruppen 118 Sustainable innovation performance for 10 Directors’ Report 2014 89 Articles of Association 123 What have we achieved? extreme conditions 25 Financial statements, – Kongsberg Gruppen 131 Systems of governance 4 President and CEO contents 90 The Board’s Report on The and key figures Walter Qvam 26 Consolidated financial Norwegian Code of Practice 6 This is KONGSBERG statements 149 Financial calendar and 73 Financial statements 100 Shareholder’s information contact information – Kongsberg Gruppen ASA 101 Shares and shareholders 83 Statement from the Board of Directors 84 Auditor’s Report KONGSBERG • Annual Report and Sustainability Report 2014 1 Introduction 8 Directors’ Report and Financial Statements 86 Corporate Governance 100 Shareholder’s information 104 Sustainability Report 149 Financial calendar and contact information KEY FIGURES 2014 2013 2012 2011 -

Samfunnsøkonomisk Analyse Av Norsk Offentlig Satsing På Romvirksomhet

SAMFUNNSØKONOMISK ANALYSE AV NORSK OFFENTLIG SATSING PÅ ROMVIRKSOMHET AV LEO A. GRÜNFELD, ANDERS M. HELSETH, TORI H. LØGE OG MAGNE AARSET RAPPORT NR. 21/2017, MARS Forord På oppdrag fra Nærings- og fiskeridepartement har Menon Economics i denne rapporten analysert om den norske satsingen på romvirksomhet er samfunnsøkonomisk lønnsom, og om innretningen er hensiktsmessig for å nå målene som er nedfelt i Meld. St. 32 (2012–2013). Arbeidet må anses som en videreføring og utvidelse av det vurderingsarbeid som ble utført av Menon Economics i 2016 knyttet til Norges deltakelse i ESAs frivillige romprogrammer og tilskuddsordningen «Nasjonale følgemidler». Analysen har vært ledet av Menons forskningsleder Leo Grünfeld. Vi har også hentet mye ut gjennom samarbeid med Magne Aarset i Terp AS. Vi takker departementet for et spennende oppdrag. Vi takker også Norsk Romsenter og en lang rekke intervjuobjekter for verdifull veiledning og kunnskapsformidling innen et felt som er teknisk og strukturelt komplisert å dekke. Forfatterne står ansvarlig for alt innhold og alle vurderinger i rapporten. ______________________ Oslo, mars 2017 Leo A Grünfeld Prosjektleder Menon Economics MENON ECONOMICS 1 Innhold FORORD 1 SAMMENDRAG 4 Kort om romsatsningen 4 Kort om problemer knyttet til samfunnsøkonomisk verdsetting 5 Vurdering av ulike alternativer 6 Kort om usikkerhet 8 1. INNLEDNING 9 1.1. Utredningens mandat 9 1.2. Tidligere analyser og evalueringer av romvirksomheten 10 1.3. Strukturen i rapporten 12 2. NORSK ROMVIRKSOMHET 13 2.1. Målsettinger for romprogrammet 13 2.2. Norsk offentlig romsatsning 13 2.3. Post 50: Norsk Romsenter 14 2.4. Post 70 ESA obligatoriske aktivitet 17 2.5. -

Complete Report

A Report on The Fifteenth International TOVS Study Conference Maratea, Italy 4-10 October 2006 Conference sponsored by: IMAA / CNR Met Office (U.K.) University of Wisconsin-Madison / SSEC NOAA NESDIS EUMETSAT World Meteorological Organization ITT Industries Kongsberg Spacetec CNES ABB Bomem Dimension Data LGR Impianti Cisco Systems and VCS Report prepared by: Thomas Achtor and Roger Saunders ITWG Co-Chairs Leanne Avila Maria Vasys Editors Published and Distributed by: University of Wisconsin-Madison 1225 West Dayton Street Madison, WI 53706 USA ITWG Web Site: http://cimss.ssec.wisc.edu/itwg/ February 2007 International TOVS Study Conference-XV Working Group Report FOREWORD The International TOVS Working Group (ITWG) is convened as a sub-group of the International Radiation Commission (IRC) of the International Association of Meteorology and Atmospheric Physics (IAMAP). The ITWG continues to organise International TOVS Study Conferences (ITSCs) which have met approximately every 18 months since 1983. Through this forum, operational and research users of TIROS Operational Vertical Sounder (TOVS), Advanced TOVS (ATOVS) and other atmospheric sounding data have exchanged information on data processing methods, derived products, and the impacts of radiances and inferred atmospheric temperature and moisture fields on numerical weather prediction (NWP) and climate studies. The Fifteenth International TOVS Study Conference (ITSC-XV) was held at the Villa del Mare near Maratea, Italy from 4 to 10 October 2006. This conference report summarises the scientific exchanges and outcomes of the meeting. A companion document, The Technical Proceedings of The Fourteenth International TOVS Study Conference, contains the complete text of ITSC-XV scientific presentations. The ITWG Web site ( http://cimss.ssec.wisc.edu/itwg/ ) contains electronic versions of the conference presentations and publications. -

ANNUAL REPORT and SUSTAIN ABILITY REPORT 2018 01 Year 2018 02 About 03 Sustainability 04 Corporate 05 Directors’ Report and KONGSBERG Governance Financial Statements

ANNUAL REPORT AND SUSTAIN ABILITY REPORT 2018 01 Year 2018 02 About 03 Sustainability 04 Corporate 05 Directors’ Report and KONGSBERG Governance Financial Statements 01 02 3 YEAR 2018 11 ABOUT KONGSBERG 4 Key Figures 2018 12 This is KONGSBERG 7 Important milestones 2018 14 Strategy and ambitions 8 President and CEO Geir Håøy 15 Vision 16 Our values 17 Corporate Executive Management 18 Business areas 28 The world of KONGSBERG 03 04 34 SUSTAINABILITY 75 CORPORATE GOVERNANCE 35 About the Sustainability Report 76 The Board’s Report on Corporate 36 Framework for the preparation of Governance Sustainability Report 77 Policy 37 Responsible Business Conduct 78 Articles of Association 38 Responsible Tax – our Tax Policy 79 Board of Directors 40 Organisation and Management Systems 80 The Board’s Report relating to “The 41 Focus areas 2018–2019 Norwegian Code of Practice for Corporate 67 Climate Statement and Key Figures Governance” 74 Auditor’s Report, Sustainability Interactive PDF with bookmarks Navigate in Contents and hyperlinked text (hyperlinks are underlined). You can 05 browse one page back or forward by using the arrows in the top right-hand corner. Use the menu button on the far left to go back to the table of contents. The chapters are also bookmarked, and you can find short cuts to these in the 92 DIRECTORS’ REPORT AND left-hand menu of the PDF Reader. FINANCIAL STATEMENTS 93 Directors’ Report 2018 111 Financial Statements and Notes 182 Statement from the Board 183 Auditor’s report 2018 187 Financial calendar 187 Contact KONGSBERG Annual -

KOG †Rsrapport 99 Orig

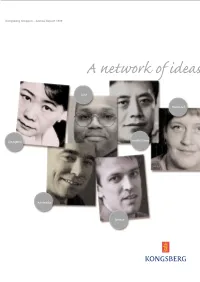

Kongsberg Gruppen – Annual Report 1999 Kongsberg Gruppen A network of ideas USA Kongsberg Gruppen ASA P.O. Box 1000 Denmark N-3601 KONGSBERG Annual Report 1999 Telephone: + 47 32 28 82 00 Fax: +47 32 28 82 01 www.kongsberg.com [email protected] Singapore South Korea Australia Greece Contents: Our international presence . 3 This is Kongsberg Gruppen . 5 Key Figures . 6 Highlights . 8 Directors’ Report . 10 Consolidated Accounts for Kongsberg Gruppen (The Group) . 17 Parent Company Accounts for Kongsberg Gruppen ASA . 30 Auditor’s Report . 32 Shares and shareholder relations . 34 Analytical Data . 36 Kongsberg Maritime . 40 Kongsberg Defence & Aerospace . 48 Business Development . 54 Property . 56 Addresses . 57 Financial calendar . 61 On the cover With their diversity, knowledge and enthusiasm, 3 400 employees in 20 countries work to generate added value for Kongsberg Gruppen, its shareholders and society-at-large. From top left: Lona Chang (46) – Finance Manager, Kongsberg Simrad Pte. Ltd. – Singapore Michael Santos Boyd (39) – Customer Support, Simrad Inc. – Seattle, Washington, USA Hwang-Yong Park (40) – Service Manager, Kongsberg Norcontrol Ltd. – Pusan, South Korea Maiken Thomassen (23) – Export Assistant, Simrad Shipmate AS - Støvring, Denmark Helge Morsund (47) – Program Manager Australia, Kongsberg Defence & Aerospace – Kongsberg, Norway Eirik Lie (33) – Project Manager Air Defence, Kongsberg Defence & Aerospace – Kongsberg, Norway 1 KOG Årsrapport 99 orig Eng 12.04.2000 09:49 Side 3 Our international presence Jan Erik Korssjøen We are proud to present the annual As a knowledge based corporation, it is CEO report for 1999. The year was charac- only natural that we pay close attention terised by strong performance in most to the development of high-technology of the Corporation's business areas, as based products. -

Norway in Space

50 years Norway as a space nation 50 years as a space nation Contents Norway in space 4 Young rocket scientists on Andøya 36 First blast off 6 Leading the world in satellite communications 37 Our unknown multi-talent 10 Vital satellite navigation 42 The European road to space 13 Norway's eye in space 46 The space industry: innovative and traditional 16 At the top of the world 50 Earth watchers 20 To Mars from Svalbard 54 A place in the sun 27 Working in the space industry 58 The Norwegian northern lights pioneers 32 Europe's new time machine 60 Lasers in the night 34 CoveR PHoto: KolBJØRN DAHLE 50 years P H We are entitled to get excited now that we're celebrating oto Norway's 50th anniversary as a space nation We are : TRU entitled to be proud of the fact that the first rocket has been de E as a space nation N followed by more than a thousand others We are entitled G to be pleased with the sound scientific, commercial and societal expertise we have built up in space technology over the course of these 50 years Things have turned out very differently from what we envisaged when Ferdinand was launched in the 1960s We were very optimistic about space travel then, and many people believed that it was only a question of a few decades before we made it to Mars We envisaged a permanent set- tlement on the moon and that hotel breaks orbiting the Earth would soon become a holiday option There has been incredible development, but in a com- pletely different direction than into space What has actu- ally happened is that space technology has become -

Annual Report and Sustainability Report 2016 01 02 03 04 INTRODUCTION DIRECTORS’ REPORT & FINANCIAL STATEMENTS CORPORATE GOVERNANCE SUSTAINABILITY

01 02 03 04 INTRODUCTION DIRECTORS’ REPORT & FINANCIAL STATEMENTS CORPORATE GOVERNANCE SUSTAINABILITY ANNUAL REPORT & SUSTAINABILITY REPORT 2016 1 KONGSBERG • Annual Report and Sustainability Report 2016 01 02 03 04 INTRODUCTION DIRECTORS’ REPORT & FINANCIAL STATEMENTS CORPORATE GOVERNANCE SUSTAINABILITY • KONGSBERG • Vision, ambitions and values • Key figures • CEO Geir Håøy CONTENTS 01 02 INTRODUCTION 3 DIRECTORS’ REPORT & FINANCIAL STATEMENTS 14 KONGSBERG 3 Directors’ Report 2016 15 Vision, ambitions and values 5 Financial Statements and Notes 30 Key Figures 7 Statement from the Board 95 President and CEO Geir Håøy 10 Auditor’s Report 96 03 04 CORPORATE GOVERNANCE 100 SUSTAINABILITY 114 The Board’s report About the Sustainability Report 115 on Corporate Governance 101 Sustainable innovation 131 Policy 102 What have we achieved? 137 Articles of association 103 Climate and the environment 148 The Board’s report on the Norwegian Goals and reporting 152 Code of Practice for Corporate Governance 104 GRI 161 Auditor’s Report 166 This is an interactive PDF with bookmarks Navigate in Contents and hyperlinked text (hyperlinks are underlined by a dashed line). You can browse one page back or forward by using the arrows in the top left-hand corner. Use the menu button on the far left to go back to the table of contents. The chapters are also bookmarked, and you can find short cuts to these in the left-hand menu of the PDF Reader. 2 KONGSBERG • Annual Report and Sustainability Report 2016 01 02 03 04 INTRODUCTION DIRECTORS’ REPORT & FINANCIAL STATEMENTS CORPORATE GOVERNANCE SUSTAINABILITY • KONGSBERG • Vision, ambitions and values • Key figures • CEO Geir Håøy KONGSBERG Kongsberg Gruppen (KONGSBERG) is an international technology group that delivers advanced and reliable solutions improving safety, security and performance in complex operations and under extreme conditions. -

Facts & Figures

OVERVIEW A specialised strategic sector _facts & figures 23rd edition, June 2019 Te European space industry in 2018 _f&f // 23rd edition, June 2019 // The European space industry in 2018 02 CONTENTS ABOUT EUROSPACE 01 OUTPUT OF THE EUROPEAN SPACE INDUSTRY IN 2018 35 FOREWORD 02 European spacecraft deliveries to launch 35 European spacecraft launched in 2018 35 OVERVIEW 03 Correlation between spacecraft mass A specialised strategic sector 03 at launch and industry revenues 37 Markets and customers 04 Ariane and VEGA launches 37 MAIN INDICATORS 06 METHODOLOGY 39 Long series indicators 07 Perimeter of the survey 39 Data Collection 39 SECTOR DEMOGRAPHICS 09 Consolidation Model 39 Industry employment - The need for consolidation 39 age and gender distribution 09 Methodological update in 2010 39 Industry employment - Qualification structure 09 Industry employment - distribution by country 10 DEFINITIONS 40 Industry employment - distribution by company 12 Space systems and related products Employment in large groups 12 considered in the survey 40 SMEs in the space sector 12 Launcher systems 40 Spacecraft/satellite systems 40 FINAL SALES BY MARKET SEGMENT 13 Ground Segment (and related services) 40 Overview: European sales vs. Export 13 Sector concentration: employment Overview - Public vs. Private customers 16 in space units, employment by unit and cumulated % 40 Customer details 17 Focus: SURVEY INFORMATION 41 European public/institutional customers 17 Eurospace economic model 41 Focus: The commercial market (private customers and exports) -

Annual Report 2000

Kongsberg Gruppen – Annual Report 2000 Technology: (from the Greek teknologia) the science that refers to the various practices, methods and means used to convert ideas or raw materials into us- able products. Technology inspired by nature Our reasons for existence and profit- ability are contingent upon our ability to discover and develop useful applications for sophisticated technology products. Accordingly, technology is the main theme of this year's annual report. Cybernetics Software Signal processing Contents Technology . 1 Key figures . 2 Systems integration Key figures, by segment . 3 This is Kongsberg Gruppen . 4 World-class technology . 6 Vision, paramount objective and strategy . 7 Highlights . 9 Annual Report . 12 Annotated accounts for Kongsberg Gruppen (The Group) . 20 Annotated accounts for Kongsberg Gruppen ASA (The Parent Company) . 34 Auditor's report . .36 Shares and shareholder relations . .37 Analytical data . 40 Kongsberg Maritime . 46 Kongsberg Defence & Aerospace . 56 Business Development . .62 Property . 64 Addresses . 65 4 Ellen K. Ohren (25) – Graduate engineer, Kongsberg Defence & Aerospace AS Technology - products We earn our living by accepting challenges - thinking along new lines, moving beyond the ordinary to the realm of the extraordinary and thus remaining in the vanguard. We have learned to be humble in the face of the multitude of amazing solutions we see in nature, perceiving them as role models which inspire us not to give up until we achieve optimal results. Technology - markets Gunnar Thorsen (45) - Sales and Marketing Manager, We endeavour to serve the best interests of society and to Kongsberg Simrad AS pave the way for growth and prosperity among our customers. -

Newsletter 11 February 2016 This Issue

ISSUE Kongsberg Spacetec AS www.spacetec.no NewsLetter 11 February 2016 this issue Sentinel 1A CollGS to FMI P. 1 MEOS™ 5 m antenna MANUFACTURER AND GLOBAL EXPORTER OF SURVEILLANCE TECHNOLOGY to KSAT in Fairbanks Alaska P. 2 MEOS™ 3.8 m antenna and Events 2016 MEOS™ Polar system to KWater P. 3 Framecontract with NSPO, Taiwan 16-20 May 2016 MEOS™ 3.8m antenna and SpaceOps 2016 METEOROLOGY CLIMATE AND ENVIRONMENT MONITORING SURVEILLANCE CAPTURE HRDFEP to Norwegian Defence Research Establishment (FFI) P. 4 Daejon, Korea WORLD CLASS - through people, technology and dedication www.spacetec.no http://www.spaceops2016.org/ 21-24 June 2016 Sentinel-1A MEOS™ CollGS system delivered to NASA Direct readout conference, Finnish Meteorological Institute Valladolid, Spain http://directreadout.sci.gsfc.nasa.gov/ Kongsberg Spacetec (KSPT) completed the On-Site The MEOS™ NRTSAR processor does processing in Acceptance Testing and delivery of the integrated parallel with reception, which allows service delivery 6 - 11 August 2016 Sentinel-1A (S-1A) MEOS™ Collaborative Ground to start while data is received from the satellite. Small Satellites - Segment (CollGS) reception and processing system The MEOS™ NRTSAR processor can also be included Pioneering an Industry on 11th November 2015, as a part of the contract in the MEOS™ CollGS system, giving the user the Logan, UT, USA between Finnish Meteorological Institute (FMI) and possibility to provide services from synthetic aperture http://www.smallsat.org/ Kongsberg Spacetec. radar data close to real time. 26-30 September 2016 The system will do data reception and processing at Information about ESA Sentinel Collaborative Ground Segment: EUMETSAT Meteorological the FMI Sodankylä ground station and process the http://www.esa.int/Our_Activities/Observing_the_Earth/ Copernicus/Sentinel_Collaborative_Ground_Segment Satellite Conference S-1A C-band Synthetic Aperture Radar (SAR) data to Darmstadt, Germany Level 0 and Level 1 (Level 2). -

Norwegian Space Activities 1958-2003

HSR-35 October 2004 Norwegian Space Activities 1958-2003 A Historical Overview Ole Anders Røberg and John Peter Collett ii Title: HSR-35 Norwegian Space Activities 1958-2003 – A Historical Overview Published by: ESA Publications Division ESTEC, PO Box 299 2200 AG Noordwijk The Netherlands Editor: D. Danesy Price: !20 ISSN: 1683-4704 ISBN: 92-9092-546-9 Copyright: ©2004 The European Space Agency Printed in: The Netherlands iii Contents Introduction ........................................................................................................................................................................... 1 The Early Years of Norwegian Geophysical and Cosmic Science..................................................................................... 3 The First Steps Towards a National Space Research Policy in Norway ............................................................................ 5 Two research councils, and two ways of dealing with science administration and policy...........................................5 European politics and Norwegian priorities – ELDO and ESRO ..................................................................................7 Norway’s preparation for ESRO, and sudden abstinence from membership................................................................9 A National Space Policy Emerging Between Science and Technology ........................................................................... 11 Andøya Rocket Range and the contest to establish an auroral launch site for ESRO.................................................12 -

Annual Report and Sustainability Report 2015

Forside n ANNUAL REPORT AND SUSTAINABILITY REPORT 2015 DIRECTORS’ ABOUT REPORT & CORPORATE SUSTAINABILITY KONGSBERG FINANCIAL GOVERNANCE STATEMENTS <HLInnhold Destination> hel rapport ABOUT KONGSBERG • KEY FIGURES • CEO • DIRECTORS’ REPORT & FINANCIAL STATEMENTS • CORPORATE GOVERNANCE • SUSTAINABILITY Content DIRECTORS’ ABOUT REPORT & CORPORATE SUSTAINABILITY KONGSBERG FINANCIAL GOVERNANCE STATEMENTS 3 About KONGSBERG 14 Directors’ Report 2015 93 The Board’s report on 107 About the Sustainability Corporate Governance report and content 5 Vision, goals and values 29 Financial statements 94 Policy – Kongsberg Gruppen 123 Sustainable innovation 7 Key figures 2015 89 Statement from the Board of Directors 95 Articles of Association 129 What have we achieved? 10 CEO Walter Qvam – Kongsberg Gruppen ASA Area of focus 2015–2016 90 Auditor’s Report 2015 96 The Board’s report on the 139 Climate and environment Norwegian Code of Practice for Corporate Governance 143 Goals and reporting 157 Auditor’s Statement 2015 This is an interactive PDF with bookmarks Navigate in Contents and hyperlinked text (hyperlinks are underlined by a dashed line). You can browse one page back or forward by using the arrows in the top left-hand corner. Use the menu button on the far left to go back to Contents. The chapters are also bookmarked, and you can find shortcuts to these in the left-hand menu of the PDF Reader.meny. 2 KONGSBERG • Annual Report and Sustainability Report 2015 ÅR - Dette er KONGSBERG ABOUT KONGSBERG • KEY FIGURES • CEO • DIRECTORS’ REPORT & FINANCIAL STATEMENTS • CORPORATE GOVERNANCE • SUSTAINABILITY Kongsberg Gruppen Kongsberg Gruppen (KONGSBERG) is an international technology corporation that delivers advanced and reliable solutions that improve safety, security and performance in complex operations and during extreme conditions.