TANZANIA Transport Sector Review Acknowledgement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

THE UNITED REPUBLIC of TANZANIA Tanzania Airports Authority

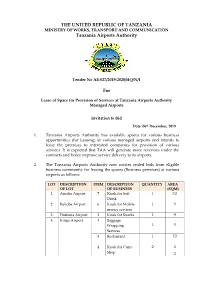

THE UNITED REPUBLIC OF TANZANIA MINISTRY OF WORKS, TRANSPORT AND COMMUNICATION Tanzania Airports Authority Tender No AE-027/2019-2020/HQ/N/1 For Lease of Space for Provision of Services at Tanzania Airports Authority Managed Airports Invitation to Bid Date: 06th December, 2019 1. Tanzania Airports Authority has available spaces for various business opportunities (for Leasing) at various managed airports and intends to lease the premises to interested companies for provision of various services. It is expected that TAA will generate more revenues under the contracts and hence improve service delivery to its airports. 2. The Tanzania Airports Authority now invites sealed bids from eligible business community for leasing the spaces (Business premises) at various airports as follows: LOT DESCRIPTION ITEM DESCRIPTION QUANTITY AREA OF LOT OF BUSINESS (SQM) 1. Arusha Airport 7 Kiosk for Soft 1 33 Drink 2. Bukoba Airport 6 Kiosk for Mobile 1 4 money services 3. Dodoma Airport 3 Kiosk for Snacks 1 4 4. Iringa Airport 1 Baggage Wrapping 1 4 Services 3 Restaurant 1 72 4 Kiosk for Curio 2 3 Shop 3 LOT DESCRIPTION ITEM DESCRIPTION QUANTITY AREA OF LOT OF BUSINESS (SQM) 5 Kiosk for Retail 1 3.5 shop 5. Kigoma Airport 1 Baggage Wrapping 1 4 Services 2 Restaurant 1 19.49 3 Kiosk for Retail 2 19.21 shop 4 Kiosk for Snacks 1 9 5 Kiosk for Curio 1 6.8 Shop 6. Kilwa Masoko 1 Restaurant 1 40 Airport 2 Kiosk for soft 1 9 drinks 7. Lake Manyara 2 Kiosk for Curio 10 84.179 Airport Shop 3 Kiosk for Soft 1 9 Drink 4 Kiosk for Ice 1 9 Cream and Beverage Outlet 5 Car Wash 1 49 6 Kiosk for Mobile 1 2 money services 8. -

ITINERARY for ROMANTIC EAST AFRICA SAFARI Tanzania & Zanzibar

ITINERARY FOR ROMANTIC EAST AFRICA SAFARI Tanzania & Zanzibar Let your imagination soar Journey overview Indulge in the drama of East Africa’s most beautiful landscapes, from the romance of classical safari to the wonder of breath-taking landscapes and the barefoot luxury of a private island. At Lake Manyara you will share a cosy tree house in the heart of a scenic landscape, where lions lounge in the forks of trees and pink flamingo wade near the lakeshore. Enjoy a taste of adventure combined with the ultimate luxury on the open plains of the Serengeti, where Persian carpets and fully sized beds are separated from the African night by only a thin sheet of canvas and the light of lanterns sparkles on silver and crystal as your private feast is served in the open air. Wrap yourself in the glamour and decadence of another era as you gaze out at endless misty views of the Ngorongoro Crater from beside a blazing fireplace. End your adventure with a moonlight walk on the white beaches of andBeyond Mnemba Island, serenaded by the whisper of the waves. HIGHLIGHTS OF THE ITINERARY: � Exceptional game viewing in the renowned Serengeti National Park � Viewing the abundance of birds in Lake Manyara National Park and the curious antics of tree-climbing lions � Explore Lake Manyara by bicycle � Peering over the edge of the world’s largest intact caldera in the Ngorongoro Conservation Area � Tucking into truly mouth-watering seafood feasts � Friendly encounters with soul-tickling personalities MAKE THE MOST OF YOUR ADVENTURE: � Glide high above the Serengeti on a Hot-air balloon safari � Walk in the first footsteps of our ancestors in the Cradle of Mankind at Olduvai Gorge � Dance in a Masaai Village and make new friends � No stay on Zanzibar is complete without spending a day or night in Stone Town. -

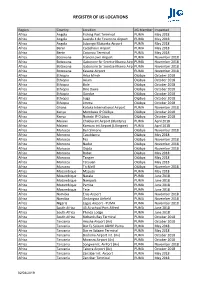

Register of IJS Locations V1.Xlsx

REGISTER OF IJS LOCATIONS Region Country Location JIG Member Inspected Africa Angola Fishing Port Terminal PUMA May 2018 Africa Angola Luanda 4 de Fevereiro Airport PUMA May 2018 Africa Angola Lubango Mukanka Airport PUMA May 2018 Africa Benin Cadjehoun Airport PUMA May 2018 Africa Benin Cotonou Terminal PUMA May 2018 Africa Botswana Francistown Airport PUMA November 2018 Africa Botswana Gaborone Sir Seretse Khama AirpoPUMA November 2018 Africa Botswana Gaborone Sir Seretse Khama AirpoPUMA November 2018 Africa Botswana Kasane Airport PUMA November 2018 Africa Ethiopia Arba Minch OiLibya October 2018 Africa Ethiopia Axum OiLibya October 2018 Africa Ethiopia Bole OiLibya October 2018 Africa Ethiopia Dire Dawa OiLibya October 2018 Africa Ethiopia Gondar OiLibya October 2018 Africa Ethiopia Jijiga OiLibya October 2018 Africa Ethiopia Jimma OiLibya October 2018 Africa Ghana Kotoka International Airport PUMA November 2018 Africa Kenya Mombasa IP OiLibya OiLibya October 2018 Africa Kenya Nairobi IP OiLibya OiLibya October 2018 Africa Malawi Chileka Int Airport (Blantyre) PUMA April 2018 Africa Malawi Kamuzu int.Airport (Lilongwe) PUMA April 2018 Africa Morocco Ben Slimane OiLibya November 2018 Africa Morocco Casablanca OiLibya May 2018 Africa Morocco Fez OiLibya November 2018 Africa Morocco Nador OiLibya November 2018 Africa Morocco Oujda OiLibya November 2018 Africa Morocco Rabat OiLibya May 2018 Africa Morocco Tangier OiLibya May 2018 Africa Morocco Tetouan OiLibya May 2018 Africa Morocco Tit Melil OiLibya November 2018 Africa Mozambique Maputo -

Socio-Economic Baseline Survey of Villages Adjacent to the Vidunda Catchment Area, Bordering Udzungwa Mountains National Park

Socio-Economic Baseline Survey of Villages Adjacent to the Vidunda Catchment Area, Bordering Udzungwa Mountains National Park Incorporating a Socio-Economic Monitoring Plan for 29 Villages North and East of the Udzungwa Mountains National Park Paul Harrison November 2006 WORLD WIDE FUND FOR NATURE TANZANIA PROGRAMME OFFICE (WWF-TPO) WITH SUPPORT FROM WWF NORWAY AND NORAD Socio-Economic Baseline Survey of Villages Adjacent to the Vidunda Catchment Area, Bordering Udzungwa Mountains National Park Report compiled by Paul Harrison, Kilimanyika Produced on behalf of WWF Tanzania Programme Office, P. O. Box 63117, Dar es Salaam, Tanzania Co-Financed by NORAD and WWF Norway All photographs © Kilimanyika, unless otherwise stated. A series of photographs accompanying this report may be obtained by contacting Kilimanyika The views expressed in this report do not necessarily reflect those of WWF Tanzania, WWF Norway or NORAD. Bankipore House High Street Brill, Bucks HP18 9ST, UK Tel. +44 7739 803 704 Email: [email protected] Web: www.kilimanyika.com 2 Paul Harrison/Kilimanyika for WWF Tanzania Table of Contents Tables and Figures..............................................................................................................................................4 Abbreviations and Acronyms .............................................................................................................................5 Acknowledgements ............................................................................................................................................6 -

Mara Swamp and Musoma Bay Fisheries Assessment Report Mara River Basin, Tanzania

Mara Swamp and Musoma Bay Fisheries Assessment Report Mara River Basin, Tanzania Mkindo River Catchment, Wami RivrBasin, Tanzania |i Integrated Management of Coastal and Freshwater Systems Program Fisheries in Mara Swamp and Musoma Bay Baseline Survey of Fisheries Resources in the Mara Swamp and Musoma Bay Mara River Basin, Tanzania Mara Basin, Tanzania Fisheries in Mara Swamp and Musoma Bay Funding for this publication was provided by the people of the United States of America through the U.S. Agency for International Development (USAID), as a component of the Integrated Management of Coastal and Freshwater Systems Leader with Associates (LWA) Agreement No. EPP-A-00-04-00015-00. The views and opinions of authors expressed herein do not necessarily state or reflect those of the United States Agency for International Development of the United States Government or Florida International University. Copyright © Global Water for Sustainability Program – Florida International University This publication may be reproduced in whole or in part and in any form for educational or non-profit purposes without special permission from the copyright holder, provided acknowledgement of the source is made. No use of the publication may be made for resale or for any commercial purposes whatsoever without the prior permission in writing from the Florida International University - Global Water for Sustainability Program. Any inquiries can be addressed to the same at the following address: Global Water for Sustainability Program Florida International University Biscayne Bay Campus 3000 NE 151 St. ACI-267 North Miami, FL 33181 USA Email: [email protected] Website: www.globalwaters.net For bibliographic purposes, this document should be cited as: Baseline Survey of Fisheries Resources in the Mara Swamp and Musoma Bay, Mara6 Basin, Tanzania. -

Wildlife Judicial and Prosecutorial Assistance Trainings Series (Tanzania) Proceedings

WILDLIFE JUDICIAL AND PROSECUTORIAL ASSISTANCE TRAININGS SERIES (TANZANIA) THEME: “STRENGTHENING LEGAL MECHANISMS TO COMBAT WILDLIFE CRIME” HELD AT OCEANIC BAY HOTEL, BAGAMOYO 24TH TO 26TH MAY 2016 WILDLIFE JUDICIAL AND PROSECUTORIAL ASSISTANCE TRAININGS SERIES (TANZANIA) PROCEEDINGS _____________________ PRODUCED BY THE SECRETARIAT: Daniel Gumbo – Widlife Division Tanzania Didi Wamukoya – African Wildlife Foundation Jia Qiao – African Wildlife Foundation Julie Thompson – TRAFFIC Lorelie Escot – IUCN Environmental Law Centre Lydia Slobodian – IUCN Environmental Law Centre Mariam George Kisusi – Judiciary Tanzania Nathan Gichohi – African Wildlife Foundation Philip Muruthi – African Wildlife Foundation Shanny Pelle – TRAFFIC WILDLIFE JUDICIAL AND PROSECUTORIAL ASSISTANCE TRAININGS SERIES (TANZANIA) TABLE OF CONTENTS ____________________ PAGE LIST OF ACRONYMS................................................................................................................................................................(i) INTRODUCTION TO PROCEEDINGS......................................................................................................................................(ii) OPENING REMARKS By Daniel Gumbo..........................................................................................…..…….....................……...........…...………..1 REMARKS By Hon Euphemia H. Mingi...................................................................................................................................................2 REMARKS By -

Tanzania 2018 International Religious Freedom Report

TANZANIA 2018 INTERNATIONAL RELIGIOUS FREEDOM REPORT Executive Summary The constitutions of the union government and of the semiautonomous government in Zanzibar both prohibit religious discrimination and provide for freedom of religious choice. Since independence, the country has been governed by alternating Christian and Muslim presidents. Sixty-one members of Uamsho, an Islamist group advocating for Zanzibar’s full autonomy, remained in custody without a trial since their arrest in 2013 under terrorism charges. In May the Office of the Registrar of Societies, an entity within the Ministry of Home Affairs charged with overseeing religious organizations, released a letter ordering the leadership of the Catholic and Lutheran Churches to retract statements that condemned the government for increasing restrictions on freedoms of speech and assembly, and alleged human rights abuses. After a public outcry, the minister of home affairs denounced the letter and suspended the registrar. The Zanzibar Ministry of Agriculture and Natural Resources destroyed a church being built on property owned by the Pentecostal Assemblies of God after the High Court of Zanzibar ruled the church was built on government property. This followed a protracted court battle in which Zanzibar courts ruled the church was allowed on the property. Vigilante killings of persons accused of practicing witchcraft continued to occur. As of July, the government reported 117 witchcraft-related incidents. There were some attacks on churches and mosques throughout the country, especially in rural regions. Civil society groups continued to promote peaceful interactions and religious tolerance. The embassy launched a three-month public diplomacy campaign in support of interfaith dialogue and sponsored the visit of an imam from the United States to discuss interfaith and religious freedom topics with government officials and civil society. -

Lake Tanganyika, Regional Fisheries Programme (TREFIP)

FAO/NORWAY GOVERNMENT GCP/INT/648/NOR COOPERATIVE PROGRAMME Field Report F-14 (En) eries FISHCODE MANAGEMENT LAKE TANGANYIKA REGIONAL FISHERIES PROGRAMME (TREFIP) PREPARED BY THE JOINT AfDB/FAO/FISHCODE MISSION C. MAGNET, J.E. REYNOLDS AND H. BRU FOOD AND AGRICULTURE ORGANIZATION OF THE UNITED NATIONS ROME, JULY 2000 FAO/Norway Programme of Assistance to Developing Countries for the Implementation of the Code of Conduct for Responsible of the Code Conduct FAO/NorwayFish Programme of Assistance to Developing Countries for the Implementation Fisheries Management for the Provision Advice of Scientific for Improving Countries to Developing Assistance F: Sub-programme LAKE TANGANYIKA REGIONAL FISHERIES PROGRAMME (TREFIP) A proposal for implementation of the Lake Tanganyika Framework Fisheries Management Plan Prepared by: The Joint AfDB/FAO/FISHCODE Lake Tanganyika Mission Christophe Magnet (Team Leader/Economist, AfDB), J.Eric Reynolds (Development Planner/Socio-Economist, FAO), & Hervé Bru (Infrastructure/Marketing Specialist, AfDB) African Development Bank, Food and Agriculture Organization Abidjan of the United Nations, Rome July 2000 The designations employed and the presentation of material in this publication do not imply the expression of any opinion whatsoever on the part of the Food and Agriculture Organization of the United Nations concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. LAKE TANGANYIKA REGIONAL FISHERIES PROGRAMME (TREFIP) 18.07.00 ACKNOWLEDGEMENTS This document was drafted on behalf of the AfDB and the four Lake Tanganyika littoral States of Burundi, the Democratic Republic of Congo (DRC), Tanzania, and Zambia. Responsibility for its preparation was assigned to the Fisheries Policy and Planning Service (FIPP) of FAO, with funding provided by the AfDB and the FAO FISHCODE Programme (GCP/INT/648/NOR -- Interregional Programme of Assistance to Developing Countries for the Implementation of the Code of Conduct for Responsible Fisheries). -

United Republic of Tanzania

INTER-AGENCY OPERATIONAL UPDATE #10 > TANZANIA/NOVEMBER 2019 United Republic of Tanzania KEY FIGURES FUNDING LEVEL AS OF 30 NOVEMBER 2019 279,484 Funded Unfunded Total number of refugees and asylum-seekers living in Tanzania USD 61 M 25% received 236,863 Total camp based population 205,830 Burundian population of concern 75% USD 181 M gap 73,169 Congolese population of concern 78,797 USD 15.9 M Requested for Tanzania in 2019 Burundian refugees returned voluntarily since September 2017 Operational Highlights L I Traditional Burundian drummers kick off 16 Days of Activism commemorations in Nyarugusu camp ©UNHCR / Mtengela 1 2 billion kilometres. 1 global movement. Join us and #StepWithRefugees INTER-AGENCY OPERATIONAL UPDATE #10 > TANZANIA/NOVEMBER 2019 ■ On 25 November, UNHCR and partners came together to launch 16 Days of Activism in Tanzania. The theme of this year’s global campaign is ‘End Gender-Based Violence in the World of Work’. A series of events were held in Nduta, Mtendeli and Nyarugusu camps and in Dar es Salaam. These include, workshops, drama performances and traditional songs and dances highlighting the importance of eliminating violence against women and girls. UNHCR Kibondo Field Office also participated in an interactive workshop where staff discussed how to promote a diverse and inclusive work environment, free of sexual exploitation, abuse and harassment. In Dar es Salaam, UNHCR partnered with UNCDF and Noa Ubongo, to train refugees on entrepreneurship skills focussing on how to generate business ideas. ■ The 21st Meeting of the Tripartite Commission for the Voluntary Repatriation of Burundian Refugees in Tanzania was held in Dar es Salaam on 29 November 2019. -

The Migration of Indians to Eastern Africa: a Case Study of the Ismaili Community, 1866-1966

University of Central Florida STARS Electronic Theses and Dissertations, 2004-2019 2019 The Migration of Indians to Eastern Africa: A Case Study of the Ismaili Community, 1866-1966 Azizeddin Tejpar University of Central Florida Part of the African History Commons Find similar works at: https://stars.library.ucf.edu/etd University of Central Florida Libraries http://library.ucf.edu This Masters Thesis (Open Access) is brought to you for free and open access by STARS. It has been accepted for inclusion in Electronic Theses and Dissertations, 2004-2019 by an authorized administrator of STARS. For more information, please contact [email protected]. STARS Citation Tejpar, Azizeddin, "The Migration of Indians to Eastern Africa: A Case Study of the Ismaili Community, 1866-1966" (2019). Electronic Theses and Dissertations, 2004-2019. 6324. https://stars.library.ucf.edu/etd/6324 THE MIGRATION OF INDIANS TO EASTERN AFRICA: A CASE STUDY OF THE ISMAILI COMMUNITY, 1866-1966 by AZIZEDDIN TEJPAR B.A. Binghamton University 1971 A thesis submitted in partial fulfillment of the requirements for the degree of Master of Arts in the Department of History in the College of Arts and Humanities at the University of Central Florida Orlando, Florida Spring Term 2019 Major Professor: Yovanna Pineda © 2019 Azizeddin Tejpar ii ABSTRACT Much of the Ismaili settlement in Eastern Africa, together with several other immigrant communities of Indian origin, took place in the late nineteenth century and early twentieth centuries. This thesis argues that the primary mover of the migration were the edicts, or Farmans, of the Ismaili spiritual leader. They were instrumental in motivating Ismailis to go to East Africa. -

LAKE VICTORIA Commercial Agriculture –Especiallycoffee Andcotton–Are Increasingly Important

© Lonely Planet Publications 240 Lake Victoria LAKE VICTORIA Lake Victoria is Africa’s largest lake, and the second-largest freshwater lake in the world. While the Tanzanian portion sees only a trickle of tourists, the region holds many attractions for those who have a bent for the offbeat and who want to immerse themselves in the rhythms of local life. At the Bujora Cultural Centre near Mwanza, you can learn Sukuma dancing and get acquainted with the culture of Tanzania’s largest tribal group. Further north at Butiama is the Nyerere museum, an essential stop for anyone interested in the great statesman. Musoma and Bukoba – both with a sleepy, waterside charm – are ideal places for getting a taste of lakeshore life. Bukoba is also notable as the heartland of the Haya people, who had one of the most highly developed early societies on the continent. Mwanza, to the southeast, is Tanzania’s second largest city after Dar es Salaam, and an increasingly popular jumping off point for safaris into the Serengeti’s Western Corridor. To the southwest is Rubondo Island National Park for bird-watching and relaxing. The best way to explore the lake region is as part of a larger loop combining Uganda and/or Kenya with Tanzania’s northern circuit via the western Serengeti, although you’ll need time, and a tolerance for rough roads. While most accommodation is no-frills, there are a few idyllic getaways – notably on Rubondo and Lukuba Islands, and near Mwanza. Most locals you’ll meet rely on fishing and small-scale farming for their living, although industry and commercial agriculture – especially coffee and cotton – are increasingly important. -

Bagamoyo Town the Conference Will Be Held at the Stella Maris Hotel in Bagamoyo

Bagamoyo Town The conference will be held at the Stella Maris Hotel in Bagamoyo. Located north of Dar es Salaam (65 km) along the coast, Bagamoyo historically started as a coastal Swahili fishing village that grew to become pivotal during the Arab settlements on the coast of Tanzania in the 13th century and later the first German colonial capital during the European colonial settlement in East Africa in 1888 to 1891. Bagamoyo was a gateway during the Ivory and Slave trade where many unfortunate Africans from as far as Congo and Malawi were kept imprisoned before they were shipped to Zanzibar to be sold. As a trading town during the East African Slave Trade, Bagamoyo also known as “Bwaga-Moyo” literally translated as “Lay down your heart” or “Give up your Hope”, Bagamoyo attracted traders, missionaries, and colonial powers from the Persian Gulf (Shiraz), Mongoles, Asia, and Europe. “…Be happy, my soul, release all cares, for we soon reach the place you yearn for The town of palms, Bagamoyo! When you were far away, how my heart ached when I thought of you, you pearl You place of happiness, Bagamoyo! The women wear their hair parted; you can drink palm wine all year through In the gardens of love of Bagamoyo! The dhows arrive with streaming sails to take aboard the treasures of Europe In the harbor of Bagamoyo! Oh, such delight to hear the drums and the lovely girls swaying in dance All night through in Bagamoyo! Be quiet, my heart, all cares are gone. Let the drumbeats rejoice: We are reaching Bagamoyo!” Traditional Swahili porters’ song Today, this Swahili town with a population of about 35,000 inhabitants is a multicultural town and a capital for Bagamoyo District in Pwani Region.