European and Best Practice Bank Resolution Mechanisms

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Intermediate Elder Law Update

INTERMEDIATE ELDER LAW UPDATE Tuesday, November 1, 2016 New York City Wednesday, November 2, 2016 Westchester Wednesday, November 9, 2016 Buffalo/Amherst Thursday, November 10, 2016 Albany Wednesday, November 16, 2016 Long Island NYSBA Co-Sponsors: Elder Law and Special Needs Section Committee on Continuing Legal Education This program is offered for education purposes. The views and opinions of the faculty expressed during this program are those of the presenters and authors of the materials. Further, the statements made by the faculty during this program do not constitute legal advice. Copyright ©2016 All Rights Reserved New York State Bar Association Lawyer Assistance Program 1.800.255.0569 Q. What is LAP? A. The Lawyer Assistance Program is a program of the New York State Bar Association established to help attorneys, judges, and law students in New York State (NYSBA members and non-members) who are affected by alcoholism, drug abuse, gambling, depression, other mental health issues, or debilitating stress. Q. What services does LAP provide? A. Services are free and include: • Early identification of impairment • Intervention and motivation to seek help • Assessment, evaluation and development of an appropriate treatment plan • Referral to community resources, self-help groups, inpatient treatment, outpatient counseling, and rehabilitation services • Referral to a trained peer assistant – attorneys who have faced their own difficulties and volunteer to assist a struggling colleague by providing support, understanding, guidance, and good listening • Information and consultation for those (family, firm, and judges) concerned about an attorney • Training programs on recognizing, preventing, and dealing with addiction, stress, depression, and other mental health issues Q. -

Virgin Atlantic

Virgin Atlantic Cryptocurrencies: Provisional Lottie Pyper considers the 2020 and beyond Liquidation and guidance given on the first Robert Amey, with Restructuring: Jonathon Milne of The Cayman Islands restructuring plan under Conyers, Cayman, and Hong Kong Part 26A of the Companies on recent case law Michael Popkin of and developments Campbells, takes a Act 2006 in relation to cross-border view cryptocurrencies A regular review of news, cases and www.southsquare.com articles from South Square barristers ‘The set is highly regarded internationally, with barristers regularly appearing in courts Company/ Insolvency Set around the world.’ of the Year 2017, 2018, 2019 & 2020 CHAMBERS UK CHAMBERS BAR AWARDS +44 (0)20 7696 9900 | [email protected] | www.southsquare.com Contents 3 06 14 20 Virgin Atlantic Cryptocurrencies: 2020 and beyond Provisional Liquidation and Lottie Pyper considers the guidance Robert Amey, with Jonathon Milne of Restructuring: The Cayman Islands given on the first restructuring plan Conyers, Cayman, on recent case law and Hong Kong under Part 26A of the Companies and developments arising from this Michael Popkin of Campbells, Act 2006 asset class Hong Kong, takes a cross-border view in these two off-shore jurisdictions ARTICLES REGULARS The Case for Further Reform 28 Euroland 78 From the Editors 04 to Strengthen Business Rescue A regular view from the News in Brief 96 in the UK and Australia: continent provided by Associate South Square Challenge 102 A comparative approach Member Professor Christoph Felicity -

Beyond Guardianship: Toward Alternatives That Promote Greater Self-Determination

Beyond Guardianship: Toward Alternatives That Promote Greater Self-Determination National Council on Disability March 22, 2018 National Council on Disability (NCD) 1331 F Street NW, Suite 850 Washington, DC 20004 Beyond Guardianship: Toward Alternatives That Promote Greater Self-Determination National Council on Disability, March 22, 2018 Celebrating 30 years as an independent federal agency This report is also available in alternative formats. Please visit the National Council on Disability (NCD) website (www.ncd.gov) or contact NCD to request an alternative format using the following information: [email protected] Email 202-272-2004 Voice 202-272-2022 Fax The views contained in this report do not necessarily represent those of the Administration, as this and all NCD documents are not subject to the A-19 Executive Branch review process. National Council on Disability An independent federal agency making recommendations to the President and Congress to enhance the quality of life for all Americans with disabilities and their families. Letter of Transmittal March 22, 2018 President Donald J. Trump The White House 1600 Pennsylvania Avenue NW Washington, DC 20500 Dear Mr. President: The National Council on Disability (NCD) is pleased to submit its report, Beyond Guardianship: Toward Alternatives That Promote Greater Self-Determination for People with Disabilities, which provides a comprehensive review of guardianship against the backdrop of the civil rights advancements of individuals with disabilities in the past several decades. While people with a variety of disabilities may face guardianship, the burgeoning aging population in America has forced issues surrounding guardianship to the fore in national media coverage and policy debates in recent years, making NCD’s report a timely contribution to policy discussions. -

Credit Risk Retention Rules

DEPARTMENT OF THE TREASURY Office of the Comptroller of the Currency 12 CFR Part 43 Docket No. OCC-2013-0010 RIN 1557-AD40 FEDERAL RESERVE SYSTEM 12 CFR Part 244 Docket No. R-1411 RIN 7100-AD70 FEDERAL DEPOSIT INSURANCE CORPORATION 12 CFR Part 373 RIN 3064-AD74 FEDERAL HOUSING FINANCE AGENCY 12 CFR Part 1234 RIN 2590-AA43 SECURITIES AND EXCHANGE COMMISSION 17 CFR Part 246 Release No. 34-73407; File No. S7-14-11 RIN 3235-AK96 DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT 24 CFR Part 267 RIN 2501-AD53 Credit Risk Retention AGENCIES: Office of the Comptroller of the Currency, Treasury (OCC); Board of Governors of the Federal Reserve System (Board); Federal Deposit Insurance Corporation (FDIC); U.S. Securities and Exchange Commission (Commission); Federal Housing Finance Agency (FHFA); and Department of Housing and Urban Development (HUD). ACTION: Final rule. SUMMARY: The OCC, Board, FDIC, Commission, FHFA, and HUD (the agencies) are adopting a joint final rule (the rule, or the final rule) to implement the credit risk retention requirements of section 15G of the Securities Exchange Act of 1934 (15. U.S.C. 78o-11), as added by section 941 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the Act or Dodd-Frank Act). Section 15G generally requires the securitizer of asset- backed securities to retain not less than 5 percent of the credit risk of the assets collateralizing the asset-backed securities. Section 15G includes a variety of exemptions from these requirements, including an exemption for asset-backed securities that are collateralized exclusively by residential mortgages that qualify as “qualified residential mortgages,” as such term is defined by the agencies by rule. -

Fannie Mae and Freddie Mac in Conservatorship: Frequently Asked Questions

Fannie Mae and Freddie Mac in Conservatorship: Frequently Asked Questions Updated May 31, 2019 Congressional Research Service https://crsreports.congress.gov R44525 Fannie Mae and Freddie Mac in Conservatorship: Frequently Asked Questions Summary Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and promote homeownership for underserved groups and locations. The GSEs purchase mortgages, retain the credit risk (for a fee), and package them into mortgage-backed securities (MBSs) that they either keep as investments or sell to institutional investors. In the years following the housing and mortgage market turmoil that began around 2007, the GSEs experienced financial difficulty. By 2008, the GSEs’ financial condition had weakened, generating concerns over their ability to meet their combined obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed at the time. In response, the Federal Housing Finance Agency (FHFA), the GSEs’ primary regulator, took control of them in a process known as conservatorship. Subject to the terms of the Senior Preferred Stock Purchase Agreements (PSPAs) between the U.S. Treasury and the GSEs, Treasury provided funds to keep the GSEs solvent. The GSEs initially agreed to pay Treasury a 10% cash dividend on funds received, and dividends were suspended for all other GSE stockholders. If the GSEs had enough profit at the end of the quarter, the dividend came out of the profit. When the GSEs did not have enough cash to pay their dividend to Treasury, they asked for additional cash to make the payment instead of issuing additional stock. -

The Recognition and Enforcement of Foreign Insolvency Derived Judgments - Rubin

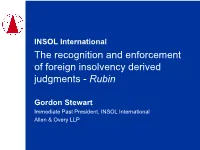

INSOL International The recognition and enforcement of foreign insolvency derived judgments - Rubin Gordon Stewart Immediate Past President, INSOL International Allen & Overy LLP Setting the scene - strands of English cross-border insolvency law COMMON LAW PRINCIPLES OF INSOLVENCY ASSISTANCE CROSS-BORDER INSOLVENCY REGULATIONS 2006 (UNCITRAL MODEL LAW) SECTION 426 COUNTRIES FOREIGN JUDGMENTS ADMINISTRATION OF (RECIPROCAL JUSTICE ACT 1920 ENFORCEMENT) ACT 1933 EU LEGISLATION DIRECTIVE DIRECTIVE EC 2001/24/EC – 2001/17/EC – INSOLVENCY WINDING UP WINDING UP REGULATION - DIRECTIVE FOR DIRECTIVE INDIVIDUALS CREDIT FOR & COMPANIES INSTITUTIONS INSURERS 2 Setting the scene – Cambridge Gas • Isle of Man company’s shareholders dispossessed of shares under chapter 11 plan – plan recognised in Isle of Man (Privy Council) • Shares asset of Cayman parent who was not subject to US chapter 11 and had not submitted to the US jurisdiction • Traditional “litigation” rules for the recognition and enforcement of judgments did not apply – insolvency concerns the enforcement of collective rights • Principle of modified universalism – “the domestic court must at least be able to provide assistance by doing whatever it could have done in the case of a domestic insolvency.” • The idea of a single insolvency having universal effect • The golden thread of common law principles of insolvency assistance since 18th century 3 Setting the scene - litigation common law Dicey & Morris Rule 43: English court will allow enforcement of foreign monetary judgment in personam if the defendant: 1) was present in the foreign country when the foreign proceedings were instituted; or 2) was a claimant or counterclaimed in the foreign proceedings; or 3) submitted to the foreign jurisdiction; or 4) agreed, in respect of the subject matter of the proceedings, to submit to the jurisdiction of that court or courts of the country. -

1 Modified Universalisms & the Role of Local Legal Culture in the Making of Cross-Border Insolvency Law Adrian Walters*

MODIFIED UNIVERSALISMS & THE ROLE OF LOCAL LEGAL CULTURE IN THE MAKING OF CROSS-BORDER INSOLVENCY LAW ADRIAN WALTERS* Cross-border insolvency law scholars have devoted much attention to theoretical questions of international system design. There is a general consensus in the literature that the ideal system would be a universalist system in which cross-border insolvencies would be administered in a single forum under a single governing law But scholars have paid less systematic attention to how a universalist system can be implemented in the real world by institutional actors such as legislatures and judges. This article seeks to redress the balance by discussing the reception of the UNCITRAL Model Law on Cross-Border Insolvency in the United States and the United Kingdom and exploring the role that judges play in harmonizing cross-border insolvency law. As the Model Law is choice-of-law neutral, domestic enactments typically contain no express choice-of-law rules. Universalists urge judges to take their cue from modified universalism and interpret Model Law enactments in a manner that approximates to universalism’s ideal “one court, one law” approach. But comparative analysis of Anglo- American judicial practice reveals that the contours of modified universalism are contested. “Modified universalism” as it is understood in the United States implies that judges should presumptively defer to the law of the foreign insolvency proceeding (lex concursus). American universalists tend therefore to favor a strong, centralizing version of modified universalism. By contrast, British modified universalism has a forum law (lex fori) choice-of-law orientation. British modified universalism supports effective coordination of insolvency proceedings with one court having a primary coordinating role. -

Federal Housing Finance Agency's FY 2019 and FY 2018 Financial

441 G St. N.W. Washington, DC 20548 November 19, 2019 The Honorable Michael Crapo Chairman The Honorable Sherrod Brown Ranking Member Committee on Banking, Housing, and Urban Affairs United States Senate The Honorable Maxine Waters Chairwoman The Honorable Patrick McHenry Ranking Member Committee on Financial Services House of Representatives Financial Audit: Federal Housing Finance Agency’s FY 2019 and FY 2018 Financial Statements This report transmits the GAO auditor’s report on the results of our audits of the fiscal years 2019 and 2018 financial statements of the Federal Housing Finance Agency (FHFA), which is incorporated in the enclosed Federal Housing Finance Agency Performance and Accountability Report for Fiscal Year 2019. As discussed more fully in the auditor’s report that begins on page 75 of the enclosed agency performance and accountability report, we found • the FHFA financial statements as of and for the fiscal years ended September 30, 2019, and 2018, are presented fairly, in all material respects, in accordance with U.S. generally accepted accounting principles; • FHFA maintained, in all material respects, effective internal control over financial reporting as of September 30, 2019; and • no reportable noncompliance for fiscal year 2019 with provisions of applicable laws, regulations, contracts, and grant agreements we tested. The Housing and Economic Recovery Act of 2008 established FHFA as an independent agency empowered with supervisory and regulatory oversight of the housing-related government- sponsored enterprises: the Federal National Mortgage Association (Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), the 11 Federal Home Loan Banks, and the Office of Finance.1 This act requires FHFA to annually prepare financial statements and requires GAO to audit the agency’s financial statements.2 In accordance with the act, we have audited FHFA’s financial statements. -

Beyond Carve-Outs and Toward Reliance: a Normative Framework for Cross-Border Insolvency Choice of Law John A

University of Michigan Law School University of Michigan Law School Scholarship Repository Articles Faculty Scholarship 2014 Beyond Carve-Outs and Toward Reliance: A Normative Framework for Cross-Border Insolvency Choice of Law John A. E. Pottow University of Michigan Law School, [email protected] Available at: https://repository.law.umich.edu/articles/1513 Follow this and additional works at: https://repository.law.umich.edu/articles Part of the Bankruptcy Law Commons, Conflict of Laws Commons, and the European Law Commons Recommended Citation Pottow, John A. E. "Beyond Carve-Outs and Toward Reliance: A Normative Framework for Cross-Border Insolvency Choice of Law." Brook. J. Corp. Fin. & Com. L. 9, no. 1 (2014): 197-220. This Article is brought to you for free and open access by the Faculty Scholarship at University of Michigan Law School Scholarship Repository. It has been accepted for inclusion in Articles by an authorized administrator of University of Michigan Law School Scholarship Repository. For more information, please contact [email protected]. BEYOND CARVE-OUTS AND TOWARD RELIANCE: A NORMATIVE FRAMEWORK FOR CROSS-BORDER INSOLVENCY CHOICE OF LAW John A. E. Pottow • The title of this Article purports to develop a normative framework for cross-border insolvency choice of law. That can be a task of varying scope, so at the outset any pretense of ambition for a wholly new choice of law model should be dispelled. Indeed, at the most generalized level, bankruptcy choice of law theory has already been fully ventilated in the well-rehearsed universalism versus territorialism debates. 1 And it has been settled. -

The Impact of Judicial Discretion for Disabled Individuals in the American Guardianship System

Macalester College DigitalCommons@Macalester College Political Science Honors Projects Political Science Department 1-18-2017 Finding Autonomy: The mpI act of Judicial Discretion for Disabled Individuals in the American Guardianship System Katherine Davis [email protected] Follow this and additional works at: http://digitalcommons.macalester.edu/poli_honors Part of the Disability Law Commons, Family Law Commons, and the Political Science Commons Recommended Citation Davis, Katherine, "Finding Autonomy: The mpI act of Judicial Discretion for Disabled Individuals in the American Guardianship System" (2017). Political Science Honors Projects. 70. http://digitalcommons.macalester.edu/poli_honors/70 This Honors Project is brought to you for free and open access by the Political Science Department at DigitalCommons@Macalester College. It has been accepted for inclusion in Political Science Honors Projects by an authorized administrator of DigitalCommons@Macalester College. For more information, please contact [email protected]. Finding Autonomy: The Impact of Judicial Discretion for Disabled Individuals in the American Guardianship System Katherine Davis Patrick Schmidt Political Science January 18, 2017 1 Abstract This study examines the conflict between guardianship and the American disability rights movement, specifically the shift from a medical to a capability model of disability. Legal guardianship presents judges with a dilemma of favoring individual autonomy or societal protection. This dichotomy manifests in the construction of state statutes where legislators can influence judicial discretion and sway decisions. Through analysis of state statutes, case law, and interviews with judges in Connecticut and Minnesota, this study found that higher levels of discretion do not necessarily translate to increased protection of individual autonomy or the use of alternatives to guardianship. -

A Lack of Resolution

Emory Law Journal Volume 60 Issue 1 2010 A Lack of Resolution David Zaring Follow this and additional works at: https://scholarlycommons.law.emory.edu/elj Recommended Citation David Zaring, A Lack of Resolution, 60 Emory L. J. 97 (2010). Available at: https://scholarlycommons.law.emory.edu/elj/vol60/iss1/2 This Article is brought to you for free and open access by the Journals at Emory Law Scholarly Commons. It has been accepted for inclusion in Emory Law Journal by an authorized editor of Emory Law Scholarly Commons. For more information, please contact [email protected]. ZARING GALLEYSFINAL 10/5/2010 11:42 AM A LACK OF RESOLUTION David Zaring* [T]here is a clear need for a new “resolution authority.” —Paul A. Volcker1 How few there are who have courage enough to own their Faults, or resolution enough to mend them! 2 —Benjamin Franklin ABSTRACT The failure to resolve—that is, impose a quick death penalty on—enormous financial intermediaries such as Lehman Brothers and AIG damaged the ability of the government to respond to the financial crisis. But expanding resolution authority to cover new systemically significant institutions—which is one of the lynchpins of financial regulatory reform—poses a problem of legitimacy with constitutional implications, as resolution authority is usually exercised with almost no predeprivation process and little postdeprivation compensation. At the same time, banking regulators have failed, every time they have been given more resolution authority, to exercise that authority when it is needed. This Article reassesses resolution authority. It proposes (1) domestic solutions to protect against government overreach and (2) an international context to deal with the problem of underreach. -

Federal Register/Vol. 85, No. 133/Friday, July 10, 2020/Proposed

41716 Federal Register / Vol. 85, No. 133 / Friday, July 10, 2020 / Proposed Rules BUREAU OF CONSUMER FINANCIAL transition away from the Temporary Steven Wrone, Senior Counsels, Office PROTECTION GSE QM loan definition and to ensure of Regulations, at 202–435–7700. If you access to responsible, affordable require this document in an alternative 12 CFR Part 1026 mortgage credit upon its expiration. electronic format, please contact CFPB_ [Docket No. CFPB–2020–0020] DATES: Comments must be received on [email protected]. or before September 8, 2020. SUPPLEMENTARY INFORMATION: RIN 3170–AA98 ADDRESSES: You may submit comments, I. Summary of the Proposed Rule Qualified Mortgage Definition Under identified by Docket No. CFPB–2020– 0020 or RIN 3170–AA98, by any of the The Ability-to-Repay/Qualified the Truth in Lending Act (Regulation Mortgage Rule (ATR/QM Rule or Rule) Z): General QM Loan Definition following methods: • Federal eRulemaking Portal: requires a creditor to make a reasonable, good faith determination of a AGENCY: Bureau of Consumer Financial https://www.regulations.gov. Follow the Protection. instructions for submitting comments. consumer’s ability to repay a residential • Email: 2020-NPRM-ATRQM- mortgage loan according to its terms. ACTION: Proposed rule with request for Loans that meet the Rule’s requirements public comment. [email protected]. Include Docket No. CFPB–2020–0020 or RIN 3170– for qualified mortgages (QMs) obtain SUMMARY: With certain exceptions, AA98 in the subject line of the message. certain protections from liability. The Regulation Z requires creditors to make • Mail/Hand Delivery/Courier: Rule defines several categories of QMs. One QM category defined in the Rule a reasonable, good faith determination Comment Intake—General QM is the General QM loan category.