Banking Crisis Resolution Policy - Different Country Experiences

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SC13-2384 Exhibit D (Lavalle)

EXHIBIT D REPORT ON NYE LAVALLE’S INVESTIGATIONS, RESEARCH BACKGROUND, BONA FIDES, EXPERTISE, & EXPERIENCE IN PREDATORY MORTGAGE SECURITIZATION, SERVICING, FORECLOSURE & ROBO-SIGNING PRACTICES INTRODUCTION 1. My name is Aneurin Adlai Lavalle. I am most commonly referred to as Nye Lavalle. I am a resident of the State of Florida. 2. I provide this report based upon facts and information personally known by me and to me and gathered from my research and investigation over a period of more than twenty-years. 3. I have a research background and as a consumer and shareholder advocate, I have developed a series of skills, procedures, and protocols over 20-years that has led me to be an expert in predatory mortgage securitization, servicing, and foreclosure fraud issues with a specialty in robo-signing.1 4. I have been accepted by Courts as an expert in matters relating to predatory mortgage securitization, servicing, and foreclosure fraud issues. 5. My findings, analyses, opinions, and many of my protocols, opinions, and conclusions have been reviewed, corroborated, and adopted by state and Federal regulatory agencies such as the Federal Reserve, Office of Comptroller of the Currency; Federal Deposit Insurance Corporation, Federal Housing Financing Agency, U.S. Attorney General and Attorneys General from all 50 states, FILED, 02/04/2015 12:11 am, JOHN A. TOMASINO, CLERK, SUPREME COURT including Florida, but especially by those in New York, Delaware, Nevada, and California. 1 http://en.wikipedia.org/wiki/Nye_Lavalle 1 6. In addition, numerous state and federal courts, including the Supreme and highest courts of the states of Massachusetts,2 Maryland,3 and Kansas4 have agreed with some of my opinions, findings, conclusions, and analyses I have developed over the last twenty-years. -

The Role of Financial Deregulation in the Geographical Restructuring Of

I 1¡ . t r'1,1 GLOBAL FINA¡ICEILOCAL CRISIS Tm Ror,n or Fnv.l¡tcrAL Dnnpcu¡,.tuoN IN rm GnocRApErcAL RnsrnucruRrNc or Ausrn¡,r.lx F¡,nn,mrc AI\D F,mu cnpurr: Tm c¿.sn or Ke¡vclRoo Isr,,lxo by Neil Argent BA Hons The University of Adelaide A Thesis submitted for the degree of Doctor of Philosophy at The University of Adelaide June 1997 tt TABLE OF CONTENTS Page Title Page I Table of Contents ü List of Tables vi List ofFigures vll Abstract )o Deolaration )(lr Aoknowledgements )qu CIIAPTER ONE: INTRODUCTION I l.l Introduction I 1.2 Research Aims and Objectives and Author's Motives J 1.3 Thesis Outline 6 1.4 Conclusion I PART ONE CHAPTER TWO: GLOBALISATION, REGI]LATION AND TTIE RI,RAL: TOWARDS A TIIEORETICAL A}IALYSIS OF CONTEMPORARY RI.'RAL AI.ID AGRICI ]LTTJRAL CITANGE 9 2.1 Introduction 9 2.2 Scalng Change: The Rural in the Global and the Global in the Rural? l0 2.3 Rural and Agrarian Restruoturing: Evohing Scales and Dimensions of Change t4 2.3.1 Introduction t4 2.3.2Peasant, Proletariat and the Fin de Siécle: l9th and 20th Century Perqpectives l5 2.3.3 Structure and Contingency, Stability and Crisis: Regulationist Approaches to Agrarian Change 26 2.3.4 T\e Political Eoonomy of Farm Credit 38 2.3.5T\e Man on the Land and the Invisible Farmer: psmini politioal st Critiques of the Eoonomy of Agrioultrue 42 2.3.6T\e Cubist State: Towards a Non-Esse,lrtialist Account ofthe Capitalist State 45 2.4 Conclusion 49 CHAPTER THREE: THE AGRICTJLTIJRE.FINA}ICE RELATION: A REALIST APPROACH 52 3.1 Introduction 52 3.2 Critical Realism: A Philosophical and Theoretical Exploration 52 3.2.1To Be Is Not To Be Perceived: A Realist Philosophy for the Social Soiences 52 3.2.2T\e Critical Realist Mode of Conceptualisation 62 3. -

Intermediate Elder Law Update

INTERMEDIATE ELDER LAW UPDATE Tuesday, November 1, 2016 New York City Wednesday, November 2, 2016 Westchester Wednesday, November 9, 2016 Buffalo/Amherst Thursday, November 10, 2016 Albany Wednesday, November 16, 2016 Long Island NYSBA Co-Sponsors: Elder Law and Special Needs Section Committee on Continuing Legal Education This program is offered for education purposes. The views and opinions of the faculty expressed during this program are those of the presenters and authors of the materials. Further, the statements made by the faculty during this program do not constitute legal advice. Copyright ©2016 All Rights Reserved New York State Bar Association Lawyer Assistance Program 1.800.255.0569 Q. What is LAP? A. The Lawyer Assistance Program is a program of the New York State Bar Association established to help attorneys, judges, and law students in New York State (NYSBA members and non-members) who are affected by alcoholism, drug abuse, gambling, depression, other mental health issues, or debilitating stress. Q. What services does LAP provide? A. Services are free and include: • Early identification of impairment • Intervention and motivation to seek help • Assessment, evaluation and development of an appropriate treatment plan • Referral to community resources, self-help groups, inpatient treatment, outpatient counseling, and rehabilitation services • Referral to a trained peer assistant – attorneys who have faced their own difficulties and volunteer to assist a struggling colleague by providing support, understanding, guidance, and good listening • Information and consultation for those (family, firm, and judges) concerned about an attorney • Training programs on recognizing, preventing, and dealing with addiction, stress, depression, and other mental health issues Q. -

Housing and the Financial Crisis

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Housing and the Financial Crisis Volume Author/Editor: Edward L. Glaeser and Todd Sinai, editors Volume Publisher: University of Chicago Press Volume ISBN: 978-0-226-03058-6 Volume URL: http://www.nber.org/books/glae11-1 Conference Date: November 17-18, 2011 Publication Date: August 2013 Chapter Title: The Future of the Government-Sponsored Enterprises: The Role for Government in the U.S. Mortgage Market Chapter Author(s): Dwight Jaffee, John M. Quigley Chapter URL: http://www.nber.org/chapters/c12625 Chapter pages in book: (p. 361 - 417) 8 The Future of the Government- Sponsored Enterprises The Role for Government in the US Mortgage Market Dwight Jaffee and John M. Quigley 8.1 Introduction The two large government- sponsored housing enterprises (GSEs),1 the Federal National Mortgage Association (“Fannie Mae”) and the Federal Home Loan Mortgage Corporation (“Freddie Mac”), evolved over three- quarters of a century from a single small government agency, to a large and powerful duopoly, and ultimately to insolvent institutions protected from bankruptcy only by the full faith and credit of the US government. From the beginning of 2008 to the end of 2011, the two GSEs lost capital of $266 billion, requiring draws of $188 billion under the Treasured Preferred Stock Purchase Agreements to remain in operation; see Federal Housing Finance Agency (2011). This downfall of the two GSEs was primarily a question of “when,” not “if,” given that their structure as a public/private Dwight Jaffee is the Willis Booth Professor of Banking, Finance, and Real Estate at the University of California, Berkeley. -

Primers Federal Home Loan Banks Feb. 8, 2021

The NAIC’s Capital Markets Bureau monitors developments in the capital markets globally and analyzes their potential impact on the investment portfolios of U.S. insurance companies. Please see the Capital Markets Bureau website at INDEX. Federal Home Loan Banks Analyst: Jennifer Johnson Executive Summary • The Federal Home Loan Bank (FHLB) system was established in 1932 for the purpose of providing liquidity and transparency to the capital markets. • It is comprised of 11 regional banks that are government-sponsored entities (GSEs) and support the market for homes. These FHLB regional banks provide low-cost financing to member financial institutions, which in turn make loans to individuals. • Each FHLB regional bank is structured as a cooperative of mortgage lenders, or members, which sets its credit standards and lending policies. To become a member, a financial institution must purchase shares of the regional bank. • FHLB regional bank members may apply for a loan or “advance” based on required credit limits and borrowing capacity. Each loan or advance is secured by eligible collateral, and lending capacity is based on applicable discount rates on the eligible collateral. The more liquid and easily valued the collateral, the lower the discount rate. • Eligible collateral may include U.S. government or government agency securities; residential mortgage loans; residential mortgage-backed securities (RMBS); multifamily mortgage loans; cash; deposits in an FHLB regional bank; and other real estate-related assets such as commercial What is thereal FHLB estate? loans. • U.S. insurers interact with the FHLB system via borrowing, investing in FHLB debt and owning stock in FHLB regional banks. -

Beyond Guardianship: Toward Alternatives That Promote Greater Self-Determination

Beyond Guardianship: Toward Alternatives That Promote Greater Self-Determination National Council on Disability March 22, 2018 National Council on Disability (NCD) 1331 F Street NW, Suite 850 Washington, DC 20004 Beyond Guardianship: Toward Alternatives That Promote Greater Self-Determination National Council on Disability, March 22, 2018 Celebrating 30 years as an independent federal agency This report is also available in alternative formats. Please visit the National Council on Disability (NCD) website (www.ncd.gov) or contact NCD to request an alternative format using the following information: [email protected] Email 202-272-2004 Voice 202-272-2022 Fax The views contained in this report do not necessarily represent those of the Administration, as this and all NCD documents are not subject to the A-19 Executive Branch review process. National Council on Disability An independent federal agency making recommendations to the President and Congress to enhance the quality of life for all Americans with disabilities and their families. Letter of Transmittal March 22, 2018 President Donald J. Trump The White House 1600 Pennsylvania Avenue NW Washington, DC 20500 Dear Mr. President: The National Council on Disability (NCD) is pleased to submit its report, Beyond Guardianship: Toward Alternatives That Promote Greater Self-Determination for People with Disabilities, which provides a comprehensive review of guardianship against the backdrop of the civil rights advancements of individuals with disabilities in the past several decades. While people with a variety of disabilities may face guardianship, the burgeoning aging population in America has forced issues surrounding guardianship to the fore in national media coverage and policy debates in recent years, making NCD’s report a timely contribution to policy discussions. -

Credit Risk Retention Rules

DEPARTMENT OF THE TREASURY Office of the Comptroller of the Currency 12 CFR Part 43 Docket No. OCC-2013-0010 RIN 1557-AD40 FEDERAL RESERVE SYSTEM 12 CFR Part 244 Docket No. R-1411 RIN 7100-AD70 FEDERAL DEPOSIT INSURANCE CORPORATION 12 CFR Part 373 RIN 3064-AD74 FEDERAL HOUSING FINANCE AGENCY 12 CFR Part 1234 RIN 2590-AA43 SECURITIES AND EXCHANGE COMMISSION 17 CFR Part 246 Release No. 34-73407; File No. S7-14-11 RIN 3235-AK96 DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT 24 CFR Part 267 RIN 2501-AD53 Credit Risk Retention AGENCIES: Office of the Comptroller of the Currency, Treasury (OCC); Board of Governors of the Federal Reserve System (Board); Federal Deposit Insurance Corporation (FDIC); U.S. Securities and Exchange Commission (Commission); Federal Housing Finance Agency (FHFA); and Department of Housing and Urban Development (HUD). ACTION: Final rule. SUMMARY: The OCC, Board, FDIC, Commission, FHFA, and HUD (the agencies) are adopting a joint final rule (the rule, or the final rule) to implement the credit risk retention requirements of section 15G of the Securities Exchange Act of 1934 (15. U.S.C. 78o-11), as added by section 941 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the Act or Dodd-Frank Act). Section 15G generally requires the securitizer of asset- backed securities to retain not less than 5 percent of the credit risk of the assets collateralizing the asset-backed securities. Section 15G includes a variety of exemptions from these requirements, including an exemption for asset-backed securities that are collateralized exclusively by residential mortgages that qualify as “qualified residential mortgages,” as such term is defined by the agencies by rule. -

Financial Crises and Policy Responses

Financial Crises and Policy Responses A MARKET-BASED VIEW FROM THE SHADOW FINANCIAL REGULATORY COMMITTEE, 1986–2015 ROBERT LITAN NOVEMBER 2016 AMERICAN ENTERPRISE INSTITUTE Financial Crises and Policy Responses A MARKET-BASED VIEW FROM THE SHADOW FINANCIAL REGULATORY COMMITTEE, 1986–2015 ROBERT LITAN NOVEMBER 2016 AMERICAN ENTERPRISE INSTITUTE © 2016 by the American Enterprise Institute. All rights reserved. The American Enterprise Institute (AEI) is a nonpartisan, nonprofit, 501(c)(3) educational organization and does not take institutional posi- tions on any issues. The views expressed here are those of the author(s). Table of Contents Preface ................................................................................................................................................................................... v I. Financial Crises and Challenges: The Origins of the Shadow Financial Regulatory Committee ..... 1 II. A Brief 30-Year History of Finance ..................................................................................................................... 5 III. The S&L Crises of the 1980s ................................................................................................................................. 7 IV. The Banking Crises of the 1980s and Policy Responses .............................................................................. 11 V. Deposit Insurance and Safety-Net Reform .................................................................................................... 17 VI. Banking Regulation -

Fannie Mae and Freddie Mac in Conservatorship: Frequently Asked Questions

Fannie Mae and Freddie Mac in Conservatorship: Frequently Asked Questions Updated May 31, 2019 Congressional Research Service https://crsreports.congress.gov R44525 Fannie Mae and Freddie Mac in Conservatorship: Frequently Asked Questions Summary Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and promote homeownership for underserved groups and locations. The GSEs purchase mortgages, retain the credit risk (for a fee), and package them into mortgage-backed securities (MBSs) that they either keep as investments or sell to institutional investors. In the years following the housing and mortgage market turmoil that began around 2007, the GSEs experienced financial difficulty. By 2008, the GSEs’ financial condition had weakened, generating concerns over their ability to meet their combined obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed at the time. In response, the Federal Housing Finance Agency (FHFA), the GSEs’ primary regulator, took control of them in a process known as conservatorship. Subject to the terms of the Senior Preferred Stock Purchase Agreements (PSPAs) between the U.S. Treasury and the GSEs, Treasury provided funds to keep the GSEs solvent. The GSEs initially agreed to pay Treasury a 10% cash dividend on funds received, and dividends were suspended for all other GSE stockholders. If the GSEs had enough profit at the end of the quarter, the dividend came out of the profit. When the GSEs did not have enough cash to pay their dividend to Treasury, they asked for additional cash to make the payment instead of issuing additional stock. -

Elizabeth a Duke: a Framework for Analyzing Bank Lending

Elizabeth A Duke: A framework for analyzing bank lending Speech by Ms Elizabeth A Duke, Member of the Board of Governors of the US Federal Reserve System, at the 13th Annual University of North Carolina Banking Institute, Charlotte, North Carolina, 30 March 2009. The original speech, which contains figures and various links to the documents mentioned, can be found on the US Federal Reserve System’s website. * * * In August 2008 I joined the Board of Governors of the Federal Reserve System, leaving behind a 30-year career as a commercial banker to become a central banker. My time as a commercial banker spanned numerous business cycles. It also encompassed at least one severe financial system crisis, in the late 1980s through the early 1990s, albeit one that was not as severe as the current one. From my time as a commercial banker, I already understood the factors considered by bankers in the initial lending decision as well as those in loss mitigation when collecting those same loans. As a central banker, I have come to appreciate even more fully the role of credit in our economic well-being. So I thought it would be appropriate for me to provide my perspective on credit conditions in our economy and the current crisis. Today, I would like to discuss a three-dimensional view of the flow of credit to households and businesses and describe the evolving role of banks in the U.S. economy. I will begin by taking a look at recent trends in aggregate borrowing by households and by the nonfinancial business sector. -

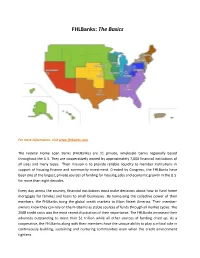

Fhlbanks: the Basics

FHLBanks: The Basics For more information, visit www.fhlbanks.com. The Federal Home Loan Banks (FHLBanks) are 11 private, wholesale banks regionally based throughout the U.S. They are cooperatively owned by approximately 7,000 financial institutions of all sizes and many types. Their mission is to provide reliable liquidity to member institutions in support of housing finance and community investment. Created by Congress, the FHLBanks have been one of the largest, private sources of funding for housing, jobs and economic growth in the U.S. for more than eight decades. Every day across the country, financial institutions must make decisions about how to fund home mortgages for families and loans to small businesses. By harnessing the collective power of their members, the FHLBanks bring the global credit markets to Main Street America. Their member- owners know they can rely on the FHLBanks as stable sources of funds through all market cycles. The 2008 credit crisis was the most recent illustration of their importance. The FHLBanks increased their advances outstanding to more than $1 trillion while all other sources of funding dried up. As a cooperative, the FHLBanks along with their members have the unique ability to play a critical role in continuously building, sustaining and nurturing communities even when the credit environment tightens. 2 FHLBanks are regionally focused and controlled. This structure allows each FHLBank to be responsive to the specific community credit needs in its geography. At the same time, the FHLBanks collectively use their combined size and strength to obtain funding at the lowest possible cost for their members. -

European and Best Practice Bank Resolution Mechanisms

70152 Public Disclosure Authorized Public Disclosure Authorized EUROPEAN AND BEST PRACTICE BANK RESOLUTION MECHANISMS AN ASSESSMENT AND RECOMMENDATIONS FOR POLICY AND LEGAL REFORMS Public Disclosure Authorized OVERVIEW REPORT Private & Financial Sector Development Department Public Disclosure Authorized Central Europe and the Baltics Country Department Europe and Central Asia Region The World Bank March 30, 2012 TABLE OF CONTENTS EXECUTIVE SUMMARY 3 SECTION I: BACKGROUND 8 SECTION II: BANK RESOLUTION – KEY PRINCIPLES 10 SECTION III: THE FUTURE EU RESOLUTION FRAMEWORK 13 Intervention Triggers 15 Resolution Tools 16 Resolution Powers 18 Funding of Resolution 18 The Cross-Border Dimension 19 RECOMMENDATIONS REGARDING THE EC PROPOSALS 20 SECTION IV: FINANCIAL MECHANISMS AND INSTRUMENTS FOR RESOLUTION 27 Mechanisms and Instruments for Implementing the Resolution Process 27 Categorization and Ranking of Bank Liabilities by Creditor 29 SECTION V: ANALYSIS OF SELECTED COUNTRIES’ RESOLUTION REGIMES 33 POLAND 33 CZECH REPUBLIC 38 GERMANY 42 SPAIN 45 UNITED KINGDOM 52 CROATIA 57 CANADA 61 UNITED STATES 66 SECTION VI: OBSERVATIONS BASED ON REVIEWS OF EU COUNTRIES’ LAWS 68 Importance of the Resolution Regime 68 Observations on Country Frameworks 71 Key Legal Provisions for Credit Institution Resolution 73 Criteria for Supervisory Intervention 73 The Objective of a Proceeding 74 The Governmental Authority Responsible for a Proceeding 75 The Powers of the Administrator of a Resolution Proceeding 75 The Mechanisms that could be used to Resolve an Institution 76 The Effect on Corporate Governance of the Affected Institution 77 CONCLUSIONS 79 This report on European Bank Resolution Mechanisms and proposals for reform, was jointly written by a team comprising John Pollner (Lead Financial Officer, ECSPF, World Bank), Henry N.