Circular to Shareholders

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SEI Global Investments Fund Plc Unaudited Condensed Financial Statements for the Half Year Ended 31 December 2020

SEI GLOBAL INVESTMENTS FUND PLC Unaudited Condensed Financial Statements for the half year ended 31 December 2020 SEI Global Investments Fund plc Unaudited Condensed Financial Statements for the half year ended 31 December 2020 CONTENTS PAGE Directory 3 General Information 4 Investment Adviser’s Report The SEI Global Select Equity Fund 6 Portfolio of Investments The SEI Global Select Equity Fund 9 Condensed Income Statement 26 Condensed Statement of Financial Position 27 Condensed Statement of Changes in Net Assets Attributable to Redeemable Participating Shareholders 29 Notes to the Condensed Financial Statements 31 Appendix I – Remuneration Disclosures 40 Appendix II – Statement of Changes in Composition of Portfolio 41 Appendix III – Securities Financing Transactions Regulation 42 2 SEI Global Investments Fund plc Unaudited Condensed Financial Statements for the half year ended 31 December 2020 DIRECTORY Board of Directors at 31 December 2020 Michael Jackson (Chairman) (Irish) Kevin Barr (American) Robert A. Nesher (American) Desmond Murray* (Irish) Jeffrey Klauder (American) *Director, independent of the Investment Adviser Manager SEI Investments Global, Limited 2nd Floor Styne House Upper Hatch Street Dublin 2 Ireland Investment Adviser SEI Investments Management Corporation 1 Freedom Valley Drive Oaks, Pennsylvania 19456 U.S.A. Depositary Brown Brothers Harriman Trustee Services (Ireland) Limited 30 Herbert Street Dublin 2 Ireland Administrator SEI Investments – Global Fund Services Limited 2nd Floor Styne House Upper Hatch Street -

20Annual Report 2020 Equiniti Group

EQUINITI GROUP PLC 20ANNUAL REPORT 2020 PURPOSEFULLY DRIVEN | DIGITALLY FOCUSED | FINANCIAL FUTURES FOR ALL Equiniti (EQ) is an international provider of technology and solutions for complex and regulated data and payments, serving blue-chip enterprises and public sector organisations. Our purpose is to care for every customer and simplify each and every transaction. Skilled people and technology-enabled services provide continuity, growth and connectivity for businesses across the world. Designed for those who need them the most, our accessible services are for everyone. Our vision is to help businesses and individuals succeed, creating positive experiences for the millions of people who rely on us for a sustainable future. Our mission is for our people and platforms to connect businesses with markets, engage customers with their investments and allow organisations to grow and transform. 2 Contents Section 01 Strategic Report Headlines 6 COVID-19: Impact And Response 8 About Us 10 Our Business Model 12 Our Technology Platforms 14 Our Markets 16 Our Strategy 18 Our Key Performance Indicators 20 Chairman’s Statement 22 Chief Executive’s Statement 24 Operational Review 26 Financial Review 34 Alternative Performance Measures 40 Environmental, Social and Governance 42 Principal Risks and Uncertainties 51 Viability Statement 56 Section 02 Governance Report Corporate Governance Report 62 Board of Directors 64 Executive Committee 66 Board 68 Audit Committee Report 78 Risk Committee Report 88 Nomination Committee Report 95 Directors' Remuneration -

Rns Over the Long Term and Critical to Enabling This Is Continued Investment in Our Technology and People, a Capital Allocation Priority

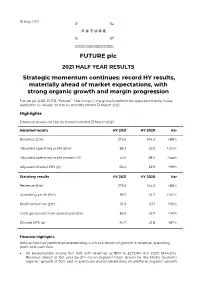

19 May 2021 FUTURE plc 2021 HALF YEAR RESULTS Strategic momentum continues: record HY results, materially ahead of market expectations, with strong organic growth and margin progression Future plc (LSE: FUTR, “Future”, “the Group”), the global platform for specialist media, today publishes its results for the six months ended 31 March 2021. Highlights Financial results for the six months ended 31 March 2021 Adjusted results HY 2021 HY 2020 Var Revenue (£m) 272.6 144.3 +89% Adjusted operating profit (£m)1 89.2 39.9 +124% Adjusted operating profit margin (%) 33% 28% +5ppt Adjusted diluted EPS (p) 65.4 32.9 +99% Statutory results HY 2021 HY 2020 Var Revenue (£m) 272.6 144.3 +89% Operating profit (£m) 59.7 24.7 +142% Profit before tax (£m) 56.9 27.1 +110% Cash generated from operations (£m) 85.9 35.7 +141% Diluted EPS (p) 40.7 21.8 +87% Financial highlights Robust first-half performance extending our track record of growth in revenue, operating profit and cash flow: An exceptionally strong first half, with revenue up 89% to £272.6m (HY 2020: £144.3m). Revenue ahead of last year by 21% on an organic2 basis, driven by the Media division’s organic2 growth of 30% and in particular digital advertising on-platform organic2 growth of 30% and eCommerce affiliates’ organic2 growth of 56%. US achieved revenue growth of 31% on an organic2 basis and UK revenues grew by 5% organically (UK has a higher mix of events and magazines revenues which were impacted more materially by the pandemic). -

GUEST LIST the Shard | 12 March A-B

GUEST LIST The Shard | 12 March A-B First Name Surname Company Name Russell Abbott Synergis Marketing April Adams-Redmond Kerry Foods Mahmood Ahmed HSBC Salim Ahmed GCS Group Rebeca Alamo Quant Marketing Charlotte Aldiss BBC Worldwide Jonathan Allan Channel 4 Television Chris Allin British Gas Tim Ambler London Business School Mark Antrobus GlaxoSmithKline Ian Armstrong Jaguar Cars Saj Arshad Vodafone Danielle Atkins Nokia Hugh Baillie Patsy Baker Bell Pottinger Group Joanna Baldwin Alistair Barr Barr Gazetas Jayne Barr Abellio Adrian Barragan Nokia Simon Bassett EMR Alex Batchelor BrainJuicer Group Katie Beard The Ultimate Experience Adam Beckett AVIVA Michael Bedingfield Royal Automobile Club John Bernard Firefox OS Mark Bernard Richard Bernholt Periproducts Joy Bhattacharya Accenture James Bidwell CASS ART Andy Bird Brand Learning John Birkbeck Capital One Viya Bishay Eurostar Group Mark Bleathman Unilever Vivian Blom TMF Group In association with With thanks to GUEST LIST The Shard | 12 March B-C First Name Surname Company Name Chris Bowry Eurostar Group Emma Bradley BBC Nick Bradley City & Guilds Colin Bradshaw Rapp Russell Braterman Vodafone Francesca Brosan Omobono Lorna Brown John Lewis Lucas Brown Total Media Group Pamela Brown British Gas Rob Bruce Whyte & Mackay Kevin Bryant E.ON UK Richard Burdett Horse & Country TV Matt Burgess Unilever Hugh Burkitt The Marketing Society Ivor Burns Camelot UK Lotteries Joanna Burton Crescent Communications Amanda Campbell Capital Shopping Centres David Campbell World Brands Limited Dominic -

The 2021 Guide to Manuscript Publishers

Publish Authors Emily Harstone Authors Publish The 2021 Guide to Manuscript Publishers 230 Traditional Publishers No Agent Required Emily Harstone This book is copyright 2021 Authors Publish Magazine. Do not distribute. Corrections, complaints, compliments, criticisms? Contact [email protected] More Books from Emily Harstone The Authors Publish Guide to Manuscript Submission Submit, Publish, Repeat: How to Publish Your Creative Writing in Literary Journals The Authors Publish Guide to Memoir Writing and Publishing The Authors Publish Guide to Children’s and Young Adult Publishing Courses & Workshops from Authors Publish Workshop: Manuscript Publishing for Novelists Workshop: Submit, Publish, Repeat The Novel Writing Workshop With Emily Harstone The Flash Fiction Workshop With Ella Peary Free Lectures from The Writers Workshop at Authors Publish The First Twenty Pages: How to Win Over Agents, Editors, and Readers in 20 Pages Taming the Wild Beast: Making Inspiration Work For You Writing from Dreams: Finding the Flashpoint for Compelling Poems and Stories Table of Contents Table of Contents .......................................................................................................... 5 Introduction ................................................................................................................. 13 Nonfiction Publishers.................................................................................................. 19 Arcade Publishing .................................................................................................. -

Page 1 of 29 Applist.Me — There's a List for That! 7/20/2012

applist.me — There's a list for that! Page 1 of 29 469 Apps 101 Science 3D Sun 4th Grade Math: Splash Centered Systems Dr. Tony Phillips, L Math Wo v.1.1 –0.5MB v.3.5 –6MB StudyPad, Inc. v.2.2.1 – 22MB THIS VERSION WILL WORK WITH OS 3.0 OR A major solar flare erupts on the sun. Splash Math is a fun and innovative way ABOVE ONLY. A BACKWARD COMPATIBLE Before long, your phone chirps in your to practice math. With 12 chapters UPDATE WILL BE RELEASED SHOR... pocket to let you know... covering over 140+ math w... View in the App Store. View in the App Store. View in the App Store. 8 Planets A Bee Sees - Learning A Bee Sees Puzzles - BrightSlide LLC Letters, Learn Sha v.2.0 –11MB Headlight Software, Headlight Software, v.1.5 –8.7MB v.1.1 –13.4MB Download the the critically acclaimed The happy, balloon popping bee helps The happy bee helps kids learn letters, educational application 8 Planets. 8 kids learn Letters, Numbers, and Colors. numbers, and shapes with fun puzzles Planets features four gam... With easy to use contr... you can customize yours... View in the App Store. View in the App Store. View in the App Store. A Phonics introduction A Sight Words Read and ABA Flash Cards & app - H Spell a Games - Emot Hetal Shah Hetal Shah Innovative Mobile Ap v.1.0 –18.6MB v.1.0 –9MB v.4.2 –26.3MB If you the parent are familiar with phonics Features: 1) 300 sight words from Dolch ★★★★★ A fun, simple, and easy way to you will immediately appreciate the way list 2) Presented by grade level 3) Two learn to recognize emotions. -

March 2019 LOCAL HERO: WHY LOCAL MEDIA MATTERS

March 2019 LOCAL HERO: WHY LOCAL MEDIA MATTERS After a month of buyouts and announcements, the dial’s interest news. Culture Secretary Jeremy Wright responded been moved on local radio. Global Radio recently announced with a rallying cry to the industry, claiming it can “overcome it would no longer air regional breakfast and drivetime shows the challenges it faces from a changing market”. in favour of national programming, while NewsUK has sold off most of its local radio stations to invest in its national stations Local media isn’t just of benefit to the public interest but can talkSPORT and Virgin Radio. be to advertisers as well. The move from Global, described as “a huge step for the A huge amount of Brits still have a strong sense of local commercial radio sector”, will see 40 of its local breakfast identity, with 90% agreeing they are proud of the area they shows replaced by national programming across the Capital, live in (“Consumer Catalyst”). Local media allows consumers Smooth and Heart networks. Drivetime, evening and to feel a part of their community – even if it’s as simple as weekend programmes will also be reduced, and ten of its 24 hearing local voices and regional accents on the radio, as local stations – including Cambridge, Norwich, Essex and Kent argued by broadcaster Mark Lawson. – will be closed. The announcement comes as part of Global’s longer-term project to bring hundreds of local stations into Brands can tap into this, ensuring they speak to consumers in several national brands – and puts over 100 jobs at risk. -

Women in Business Awards Luncheon at the Hotel Irvine, Where Aston Martin Americas President Laura Schwab Delivered the Keynote Address

10.5.20 SR_WIB.qxp_Layout 1 10/2/20 12:14 PM Page 29 WOMEN IN BUSINESS NOMINEES START ON PAGE B-60 INSIDE 2019 WINNERS GO BIG IN IRVINE, LAND NEW PARTNERS, INVESTMENTS PAGE 30 PRESENTED BY DIAMOND SPONSOR PLATINUM SPONSORS GOLD SPONSOR SILVER SPONSORS 10.5.20 SR_WIB.qxp_Layout 1 10/2/20 1:36 PM Page 30 30 ORANGE COUNTY BUSINESS JOURNAL www.ocbj.com OCTOBER 5, 2020 Winning Execs Don’t Rest on Their Laurels $1B Cancer Center Underway; Military Wins; Spanish Drug Investment Orange County’s business community last year celebrated the Business Journal’s 25th annual Women in Business Awards luncheon at the Hotel Irvine, where Aston Martin Americas President Laura Schwab delivered the keynote address. The winners, selected from 200 nominees, have not been resting on their laurels, even in the era of the coronavirus. Here are updates on what the five winners have been doing. —Peter J. Brennan Avatar Partners City of Hope Shortly after Marlo Brooke won the Busi- (AR) quality assurance solution for the U.S. As president of the City of Hope Orange employees down from Duarte. Area univer- ness Journal’s award for co-founding Hunt- Navy for aircraft wiring maintenance for the County, Annette Walker is orchestrating a sities could partner with City of Hope. ington Beach-based Avatar Partners Inc., Naval Air Systems Command’s Boeing V- $1 billion project to build one of the biggest, While the larger campus near the Orange she was accepted into the Forbes Technol- 22 Osprey aircraft. and scientifically advanced, cancer research County Great Park is being built, Walker in ogy Council, an invitation-only community Then the Air Force is using Avatar’s solu- centers in the world. -

How It Works Issue 9

NEW THE MAGAZINE THAT FEEDS MINDS INSIDE INTERVIEW DR YAN WONG TM FROM BBC’S BANG SCIENCE ■ ENVIRONMENT ■ TECHNOLOGY ■ TRANSPORT HISTORY ■ SPACE GOES THE THEORY HEART VOLCANIC BYPASSES ERUPTIONS How modern surgeons Discover the explosive save lives everyday BREAK THE 200MB BARRIER! power beneath Earth SUPERFAST BROADBAND LEARN REVEALED! THE NEXT-GENERATION ABOUT NETWORKS THAT DELIVER ■ CASSINI PROBE WARP-SPEED INTERNET ■ RAINING ANIMALS ■ PLANET MERCURY ■ BATTLE OF BRITAIN THE WORLD’S ■ PLACEBO EFFECT ■ LEANING TOWER OF PISA DEADLIEST ■ THE NERVOUS SYSTEM CHOPPER ■ ANDROID VS iPHONE Inside the Apache ■ AVALANCHES 919 AH-64D Longbow FACTS AND 9 ANSWERS 0 INSIDE £3.99 4 0 0 2 3 7 1 4 0 ISSN 2041-7322 2 7 7 ISSUE NINE ISSUE RACE TO 9 HUMAN SOLAR ROLLER 1,000MPH ALLERGIES© Imagine PublishingFLARES Ltd COASTERS Awesome engineering Why dust,No unauthorisedhair and pollen copyingHow massive or distribution explosions on Heart-stopping secrets of behind the land speed record make us sneeze the Sun affect our planet the world’s wildest rides www.howitworksdaily.com 001_HIW_009.indd 1 27/5/10 16:34:18 © Imagine Publishing Ltd No unauthorised copying or distribution Get in touch Have YOU got a question you want answered by the How It Works team? Get in touch by… Email: [email protected] Web: www.howitworksdaily.com ISSUE NINE Snail mail: How It Works Imagine Publishing, 33 Richmond Hill The magazine that feeds minds! Bournemouth, Dorset, BH2 6EZ ”FEED YOUR MIND!” Welcome to How It Meet the experts The sections explained Works issue -

Leading Music Enthusiast Content Publisher Doubles Video Output

CASE STUDY Leading Music Enthusiast Content Publisher Doubles Video Output with StorNext When a leading creator of specialized music news, enthusiast, and instructional content wanted to increase their output, they hit a major roadblock. Their aging video production SAN, an Xsan inherited through an acquisition, just wasn’t up to a faster tempo. Installing Quantum’s StorNext Pro Foundation turned their workflow from lento to prestissimo and doubled production. StorNext Pro Foundation We do not have a large IT staff, so it was really important to find a solution that would be “turn-key, that could fit in quickly and that would minimize ongoing admin. We needed something that would be easy to install and that would just work once it was in. Anthony Verbanac Director of IT, NewBay Media FEATURED PRODUCTS ” The StorNext Pro Foundation was exactly what we needed...It gives us the capacity we need today, room to grow in the future, and it is compatible with all our applications “and the latest versions of OS X. ” Anthony Verbanac - Director of IT, NewBay Media With over 13 million monthly readers in over previously released material is incorporated into 50 countries around the world, NewBay new offerings, and support has to be provided Media is the industry’s premiere publisher of for YouTube and all the latest Apple, Google, specialized enthusiast content across music, Nook, and Kindle formats. SOLUTION OVERVIEW pro-audio, video, and gaming, which it delivers ∙ StorNext Pro Foundation through a combination of traditional print and AGING SAN LIMITS GROWTH - StorNext® 5 platform new media platforms. -

FIPP Management Board As at 21 March 2019 Chairman Ralph Büchi

FIPP Management Board as at 21 March 2019 Chairman Ralph Büchi, Chief Operating Officer of the Ringier Group & CEO of Ringier Axel Springer Switzerland AG, Ringier Axel Springer Switzerland AG, Switzerland Treasurer Erwin Fidelis Reisch, President & CEO, Alfons W. Gentner Verlag GmbH & Co. KG, Germany President & CEO, James Hewes, President & CEO, FIPP - the network for global media, UK Directors Kaisa Ala-Laurila, CEO, A-lehdet Oy, Finland Srinivasan Balasubramanian, Managing Director, Ananda Vikatan Publishers Private Limited, India Natasha Christie-Miller, Divisional CEO, Ascential, Ascential, UK Enrique Micheli, Executive Director, Asociación Argentina de Editores de Revistas (AAER), Argentina Yolanda Ausín Castañeda, General Manager, Asociación de Revistas de Información (ARI), Spain Julia Raphaely, CEO, Associated Media Publishing, South Africa Jan Bayer, Member of the Executive Board & President News Media, Axel Springer SE, Germany Andrew Moultrie, Director of Consumer Products, Publishing and Web Properties, UK, BBC Studios Distribution Limited, UK Helen O'Donnell, Head of Development, TalentWorks, BBC Studios Distribution Limited, UK Alfred Heintze, COO, Burda International Holding GmbH, Germany Wu Shangzhi, President, China Periodicals Association (CPA), China Pierre Lamunière, President & Chairman, Edipresse Group, Switzerland Porfirio Sánchez Galindo, CEO, Editorial Televisa S.A. de C.V., Mexico Aaron Asadi, Chief Operations Officer, Future Publishing Ltd, UK Rolf Heinz, President & CEO Prisma Media, President G+J International -

Lofty Valuations and Massive PE and Strategic Buyer Interest Lead M&A

M&A Soundcheck – Q1’18 Lofty Valuations and Massive PE and Strategic Buyer Interest Lead M&A Activity in Q1’18 intrepidib.com | Mergers & Acquisitions | Capital Markets | Strategic Advisory 11755 Wilshire Blvd., 22nd Floor, Los Angeles, CA 90025 T 310.478.9000 F 310.478.9004 Member FINRA/SIPC Lofty Valuations and Massive PE and Strategic Buyer Interest Lead M&A Activity in Q1’18 M&A activity in 2018 is off to a very strong start, reflecting strong demand from private equity and strategic buyers as well as lofty valuations seen in both the public and private markets. It’s been particularly busy for Commercial & Consumer Technology (CCT) M&A in Southern California, where two of the larger deals in the sector occurred with Amazon acquiring Ring for over $1 billion and Foxconn affiliate FIT acquiring Belkin for over $850 million. Both home grown Los Angeles-based companies play squarely in the connected home space. Across the broader CCT markets, A/V integration remains a hot sector, with several deals occurring among mid-tier integrators and Snap AV continuing its acquisition spree following its recapitalization by Hellman & Friedman last year. Intrepid continues to be busy in this active market, closing the sale of Radial Engineering, a well-known manufacturer of accessories for professional musicians and live performance venues just in time for NAMM 2018. We are excited about the robust backlog of opportunities and continued strong interest among acquirers for high-quality assets. If you are considering options for your business or would like to discuss any of these trends, please do not hesitate to reach out.