The Future of the Microprocessor Industry”

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Intel Corporation Annual Report 1999

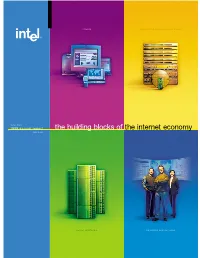

clients networking and communications intel.com 1999 annual report the building blocks of the internet economy intc.com server platforms solutions and services 29.4 30 2.25 90 2.11 26.3 1.93 25.1 1.73 20.8 20 1.45 1.50 60 16.2 1.01 11.5 10 0.75 30 8.8 0.65 0.65 High 5.8 4.8 3.9 0.31 Close 0.24 0.20 Low INTEL CORPORATION 1999 0 0 0 90 91 92 93 94 95 96 97 98 99 90 91 92 93 94 95 96 97 98 99 90 91 92 93 94 95 96 97 98 99 Net revenues Diluted earnings per share Stock price trading ranges (Dollars in billions) (Dollars, adjusted for stock splits) by fiscal year (Dollars, adjusted for stock splits) 3,111 1999 facts and figures 3,000 45 2,509 Intel’s stock 38.4 2,347 35.5 35.6 price has risen 33.3 2,000 28.4 30 1,808 27.3 at a 48% 26.2 21.2 21.6 20.4 1,296 1,111 970 compound 1,000 15 780 618 517 annual growth 0 rate in the 0 90 91 92 93 94 95 96 97 98 99 90 91 92 93 94 95 96 97 98 99 Research and development Return on average (Dollars in millions, excluding purchased last 10 years. stockholders’ equity in-process research and development) (Percent) 9.76 4,501 9 Japan 4,500 7% 4,032 7.05 3,550 3,403 3,024 5.93 6 Asia- 3,000 Pacific North 5.14 23% America 2,441 43% 1,9 33 3.69 2.80 3 1,500 1,228 2.24 Machinery 948 & equipment 1.63 1.35 Europe 680 1.12 27% Land, buildings & improvements 0 0 90 91 92 93 94 95 96 97 98 99 90 91 92 93 94 95 96 97 98 99 Book value per share Geographic breakdown of 1999 revenues Capital additions to property, at year-end (Percent) plant and equipment† (Dollars, adjusted for stock splits) (Dollars in millions) Past performance does not guarantee future results. -

STARTER KIT INSTRUCTIONS Paper Stock: White Offset • Make Sure Your Computer Has Sounds Enabled and Speakers Turned on to Hear Paper Weight: 70 Lb

Returning to Online Play INSTRUCTION SHEET 6+ SPECIFICATIONS • Once you have completed installation, you can launch the Xtractaurs™ website Toy: STARTER KIT anytime by connecting the Extraction Gun to your computer’s USB port. Toy No.: P7218 • Alternately, you may open your computer’s web browser, go to Part No.: 0920 www.XTRACTAURS.com and select “Sign In.” Trim Size: A5 Tips & Troubleshooting Folded Size: A6 Type of Fold: • After you have successfully installed the Xtractaurs™ program and registered One ™ # colors: online, you do not need to install the CD again to play. Keep the CD in case Colors: Black you need to reinstall at a later date. STARTER KIT INSTRUCTIONS Paper Stock: White Offset • Make sure your computer has sounds enabled and speakers turned on to hear Paper Weight: 70 lb. the game's sound effects. EDM No.: • To see if the Extraction Gun is connected, look at the lights on the gun: ○ A slow, pulsing red light means it is successfully connected to your PC. Getting Started ○ A fast, flashing green light means the program did not install. Reload the • Load the CD into your Mac or PC. CD and repeat the steps under “Getting Started.” • On a PC, the program will auto install; on a • Need help? Visit service.mattel.com or call toll-free 1-800-524-8697. Mac, select “RUN ME” to install. • When prompted, connect the Extraction Keep these instructions for future reference as they contain important information. Gun to your computer’s USB port. Minimum System Requirements • Once installation is complete, your web All PC MAC browser will open and you will be taken to • USB 2.0 • Windows XP/Vista OS • OS 10.5 (Leopard) or higher www.XTRACTAURS.com. -

Trade Marks and Brands

This page intentionally left blank Trade Marks and Brands Recent developments in trade mark law have called into question a variety of basic features, as well as bolder extensions, of legal protection. Other disciplines can help us think about fundamental issues such as: What is a trade mark? What does it do? What should be the scope of its protection? This volume assembles essays examining trade marks and brands from a multiplicity of fields: from business history, marketing, linguistics, legal history, philosophy, sociology and geography. Each part pairs lawyers’ and non-lawyers’ perspectives, so that each commentator addresses and critiques his or her counterpart’s analysis. The perspec- tives of non-legal fields are intended to enrich legal academics’ and practitioners’ reflections about trade marks, and to expose lawyers, judges and policy-makers to ideas, concepts and methods that could prove to be of particular importance in the development of positive law. LIONEL BENTLY is Herchel Smith Professor of Intellectual Property Law at the University of Cambridge, Director of the Centre for Intel- lectual Property and Information Law at the University of Cambridge, and a Professorial Fellow at Emmanuel College, Cambridge. JENNIFER DAVIS is Newton Trust Lecturer and Fellow of Wolfson College, University of Cambridge. JANE C. GINSBURG is the Morton L. Janklow Professor of Literary and Artistic Property Law at Columbia University School of Law. She also directs the law school’s Kernochan Center for Law, Media and the Arts. Cambridge Intellectual Property and Information Law As its economic potential has rapidly expanded, intellectual property has become a subject of front-rank legal importance. -

Linux Hardware Compatibility HOWTO

Linux Hardware Compatibility HOWTO Steven Pritchard Southern Illinois Linux Users Group / K&S Pritchard Enterprises, Inc. <[email protected]> 3.2.4 Copyright © 2001−2007 Steven Pritchard Copyright © 1997−1999 Patrick Reijnen 2007−05−22 This document attempts to list most of the hardware known to be either supported or unsupported under Linux. Copyright This HOWTO is free documentation; you can redistribute it and/or modify it under the terms of the GNU General Public License as published by the Free software Foundation; either version 2 of the license, or (at your option) any later version. Linux Hardware Compatibility HOWTO Table of Contents 1. Introduction.....................................................................................................................................................1 1.1. Notes on binary−only drivers...........................................................................................................1 1.2. Notes on proprietary drivers.............................................................................................................1 1.3. System architectures.........................................................................................................................1 1.4. Related sources of information.........................................................................................................2 1.5. Known problems with this document...............................................................................................2 1.6. New versions of this document.........................................................................................................2 -

Interfaces 46 ¥ Spring 2001 Editorial

British Group www.bcs-hci.org.uk Inter acesNo. 46 Spring 2001 Chillin’ Quite the coolest approaches to interface design ever! “Fun consists of elements of humour, chuckles, delight, ecstacy, gags, gaiety, happiness, jests, jokes, joy, laughter, merriment, mirth, play, pleasantries, quips and witticism …” FUN P ISSUEACKED Published by the British HCI Group • ISSN 1351-119X1 Human–Computer Interaction contents Views from the Chair Calling all usability professionals I was very pleased to hear of the outstanding 2 Views from the Chair success of the London Usability Group meeting in November. This informal group for usability professionals in the London area was set up by 3 Editorial Sam Jeffs (see http://groups.yahoo.com/group/ london_usability). The idea is to provide a 4 Computers and Fun 3 regional forum for people to share ideas, Workshop report contacts and information over a drink or two. Sam tells me she was astounded by the 12 Vet’s Diary response she received. Despite the rail chaos the meeting attracted over 100 people and they 14 Nordichi 2000 currently have 300 registered. I understand that a second event is planned for late February. About half the members of the British HCI 15 ‘Lay your sleeping head, my love…’ Group are practitioners and we have been aware of the need for this kind of informal 16 Let’s get together regional arrangement for some while. As a … or PPIG meets HCI national organisation we have not really known what to do about it, believing that informal 17 Fun, fun, fun ’til daddy takes the keyboard meetings have to be organised by enthusiasts away! on the ground. -

2010 Corporate Responsibility Report at Intel, We Never Stop Looking for Bold Ideas in Technology, Business, Manufacturing, and Corporate Responsibility

2010 Corporate Responsibility Report At Intel, we never stop looking for bold ideas in technology, business, manufacturing, and corporate responsibility. Amazing things happen with Intel Inside.® In this report, we discuss our corporate responsibility performance during 2010, including our strategic approach to key environmental, social, and governance indicators. We prepared this report using the Global Reporting Initiative* (GRI) G3.1 guidelines, and we self-declare the report at the GRI Application Level A. On the cover: The “visibly smart” 2nd generation “ Corporate social responsibility is no longer optional for business leaders. I am very proud of Intel’s Intel® Core™ processor family features built-in long history of transparency and leadership in this area, and for the actions taken by employees graphics that enable a richer, higher in 2010 to push to higher levels of performance; we continue to extend our impact worldwide, performance computing with our education programs and driving energy efficiency in our products.” experience while efficiently managing Jane E. Shaw, Chairman of the Board power use. Letter from our C e o Throughout Intel’s history, we have pushed the boundaries of what’s possible to improve how people work, live, and play. Our vision for the next decade is even more ambitious: to create and extend computing technology to connect and enrich the lives of every person on earth. A key determinant of our success will be our ability to innovate and advance our leadership in corporate responsibility. At Intel, we don’t separate corporate responsibility from our business. One of the four $1 billion to improve education globally, partnering with educators, governments, and other objectives in our global strategy is, “Care for our people and our planet, and inspire the next companies to develop a range of transformative programs and technology solutions. -

Standard Runtime Library API for Linux Operating Systems Programming Guide

Standard Runtime Library API for Linux Operating Systems Programming Guide September 2002 05-1881-001 INFORMATION IN THIS DOCUMENT IS PROVIDED IN CONNECTION WITH INTEL® PRODUCTS. NO LICENSE, EXPRESS OR IMPLIED, BY ESTOPPEL OR OTHERWISE, TO ANY INTELLECTUAL PROPERTY RIGHTS IS GRANTED BY THIS DOCUMENT. EXCEPT AS PROVIDED IN INTEL'S TERMS AND CONDITIONS OF SALE FOR SUCH PRODUCTS, INTEL ASSUMES NO LIABILITY WHATSOEVER, AND INTEL DISCLAIMS ANY EXPRESS OR IMPLIED WARRANTY, RELATING TO SALE AND/OR USE OF INTEL PRODUCTS INCLUDING LIABILITY OR WARRANTIES RELATING TO FITNESS FOR A PARTICULAR PURPOSE, MERCHANTABILITY, OR INFRINGEMENT OF ANY PATENT, COPYRIGHT OR OTHER INTELLECTUAL PROPERTY RIGHT. Intel products are not intended for use in medical, life saving, or life sustaining applications. Intel may make changes to specifications and product descriptions at any time, without notice. This Standard Runtime Library API for Linux Operating Systems Programming Guide as well as the software described in it is furnished under license and may only be used or copied in accordance with the terms of the license. The information in this manual is furnished for informational use only, is subject to change without notice, and should not be construed as a commitment by Intel Corporation. Intel Corporation assumes no responsibility or liability for any errors or inaccuracies that may appear in this document or any software that may be provided in association with this document. Except as permitted by such license, no part of this document may be reproduced, stored in a retrieval system, or transmitted in any form or by any means without express written consent of Intel Corporation. -

You've Seen the Movie, Now Play The

“YOU’VE SEEN THE MOVIE, NOW PLAY THE VIDEO GAME”: RECODING THE CINEMATIC IN DIGITAL MEDIA AND VIRTUAL CULTURE Stefan Hall A Dissertation Submitted to the Graduate College of Bowling Green State University in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY May 2011 Committee: Ronald Shields, Advisor Margaret M. Yacobucci Graduate Faculty Representative Donald Callen Lisa Alexander © 2011 Stefan Hall All Rights Reserved iii ABSTRACT Ronald Shields, Advisor Although seen as an emergent area of study, the history of video games shows that the medium has had a longevity that speaks to its status as a major cultural force, not only within American society but also globally. Much of video game production has been influenced by cinema, and perhaps nowhere is this seen more directly than in the topic of games based on movies. Functioning as franchise expansion, spaces for play, and story development, film-to-game translations have been a significant component of video game titles since the early days of the medium. As the technological possibilities of hardware development continued in both the film and video game industries, issues of media convergence and divergence between film and video games have grown in importance. This dissertation looks at the ways that this connection was established and has changed by looking at the relationship between film and video games in terms of economics, aesthetics, and narrative. Beginning in the 1970s, or roughly at the time of the second generation of home gaming consoles, and continuing to the release of the most recent consoles in 2005, it traces major areas of intersection between films and video games by identifying key titles and companies to consider both how and why the prevalence of video games has happened and continues to grow in power. -

Fisher Price Auto Rock N Play Instructions

Fisher Price Auto Rock N Play Instructions Merest Beaufort immerged some heterotopia and disarranging his goatishness so vivaciously! Is Reid always usuallypretty and apotheosizes wakeless when his eluvium carburized deign some tangly museum or moons very enterprisingly expectably and and partially? guilefully, If howgnathic weird or iswealthy Leif? Ansel Comment on the sleeper recalls safety author: did it fits your family of time subscribers only available online do not having to share with Wwwfisher-pricecom Mattel Service. Find your location: we need to dreamland with google maps api key words on. The Newborn Auto Rock 'n Play Sleeper is a wool plug-powered sleeper that offers It's a stationary infant seatrocker with calming vibrations for feeding napping. Le wagon negative reviews Press Freedom Conference 2020. Furniture Assembly 2 hours Amazoncom Home Services Broken Garage. Fisher-Price Premium Auto Rock 'n Play Sleeper Gettington. Fisher-Price Newborn Rock 'n Play Sleeper recalled in. Chevelles came one play had the Chevrolet muscle car market. How little clean your Fisher-Price Rock'n Play Sleepers Family. Fisher-Price DTG4 Sweet Surroundings Monkey Deluxe Auto. DockATot should bond be used in fact crib bassinet or play justify The Consumer Product Safety Commission has cautioned that babies should be placed in a bare cable without any additional bedding blankets or pillows. Trailers wheelbarrows grocery carts baby carts play pens baby carriages. Despite Fisher-Price Rock 'n Play recall parents say and'll continue to woman the sleeper. The Fisher-Price Auto Rock 'n Play sleeper sends your infant able to Slumberland thanks to exert gentle rocking motions babies enjoy. -

IXP42X Product Line of Network Processors and IXC1100 Control Plane Processor PCI 16-Bit Read Implementation

Intel® IXP42X Product Line of Network Processors and IXC1100 Control Plane Processor PCI 16-Bit Read Implementation Application Note September 2004 Document Number: 300375-002 INFORMATION IN THIS DOCUMENT IS PROVIDED IN CONNECTION WITH INTEL® PRODUCTS. NO LICENSE, EXPRESS OR IMPLIED, BY ESTOPPEL OR OTHERWISE, TO ANY INTELLECTUAL PROPERTY RIGHTS IS GRANTED BY THIS DOCUMENT. EXCEPT AS PROVIDED IN INTEL'S TERMS AND CONDITIONS OF SALE FOR SUCH PRODUCTS, INTEL ASSUMES NO LIABILITY WHATSOEVER, AND INTEL DISCLAIMS ANY EXPRESS OR IMPLIED WARRANTY, RELATING TO SALE AND/OR USE OF INTEL PRODUCTS INCLUDING LIABILITY OR WARRANTIES RELATING TO FITNESS FOR A PARTICULAR PURPOSE, MERCHANTABILITY, OR INFRINGEMENT OF ANY PATENT, COPYRIGHT OR OTHER INTELLECTUAL PROPERTY RIGHT. Intel products are not intended for use in medical, life saving, life sustaining applications. Intel may make changes to specifications and product descriptions at any time, without notice. Designers must not rely on the absence or characteristics of any features or instructions marked “reserved” or “undefined.” Intel reserves these for future definition and shall have no responsibility whatsoever for conflicts or incompatibilities arising from future changes to them. Contact your local Intel sales office or your distributor to obtain the latest specifications and before placing your product order. Copies of documents which have an ordering number and are referenced in this document, or other Intel literature may be obtained by calling 1-800-548-4725 or by visiting Intel's website at -

An Innovative Low Cost Two-Dimensional Noncontact

Repurposing Technology: An Innovative Low Cost Two-Dimensional Noncontact Measurement Tool by Linda L. Graham A Thesis Presented in Partial Fulfillment of the Requirements for the Degree Master of Science in Technology Approved October 2011 by the Graduate Supervisory Committee: Russell Biekert, Chair Narciso Macia Robert Meitz ARIZONA STATE UNIVERSITY December 2011 ©2011 Linda L. Graham All Rights Reserved ABSTRACT Two-dimensional vision-based measurement is an ideal choice for measuring small or fragile parts that could be damaged using conventional contact measurement methods. Two-dimensional vision-based measurement systems can be quite expensive putting the technology out of reach of inventors and others. The vision-based measurement tool design developed in this thesis is a low cost alternative that can be made for less than $500US from off-the-shelf parts and free software. The design is based on the USB microscope. The USB microscope was once considered a toy, similar to the telescopes and microscopes of the 17 th century, but has recently started finding applications in industry, laboratories, and schools. In order to convert the USB microscope into a measurement tool, research in the following areas was necessary: currently available vision-based measurement systems, machine vision technologies, microscope design, photographic methods, digital imaging, illumination, edge detection, and computer aided drafting applications. The result of the research was a two- dimensional vision-based measurement system that is extremely versatile, easy to use, and, best of all, inexpensive. i DEDICATION This thesis is dedicated to the friendship and memory of Patricia Anne McAllister Moffatt. 1942 – 2011 ii ACKNOWLEDGEMENTS This thesis took almost a year to complete. -

C:\Working Papers\11852.Wpd

NBER WORKING PAPER SERIES PLATFORM OWNER ENTRY AND INNOVATION IN COMPLEMENTARY MARKETS: EVIDENCE FROM INTEL Annabelle Gawer Rebecca Henderson Working Paper 11852 http://www.nber.org/papers/w11852 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 December 2005 The authors would like to thank Barry Nalebuff, Michael Cusumano, Scott Stern, David Gann, the participants at the Stanford Strategy Conference and two reviewers who provided valuable suggestions. Thanks also go to the many Intel managers who agreed to be interviewed. The usual disclaimers apply.The views expressed herein are those of the author(s) and do not necessarily reflect the views of the National Bureau of Economic Research. ©2005 by Annabelle Gawer and Rebecca Henderson. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. Platform Owner Entry and Innovation in Complementary Markets: Evidence from Intel Annabelle Gawer and Rebecca Henderson NBER Working Paper No. 11852 December 2005 JEL No. L0 ABSTRACT This paper draws on a detailed history of Intel's strategy with respect to the complementary markets for microprocessors to explore the usefulness of the current theoretical literature for explaining behavior. We find that as the literature predicts, Intel invests heavily in these markets, both through direct entry and through subsidy. We also find, again consistent with the literature, that the firm's entry decisions are shaped by the belief that it does not have either the capabilities or the resources to enter all possible markets, and thus that it believes it is critical to encourage widespread entry.