The WACC for KPN and Vodafoneziggo

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Innovation in Loyalty and Customer Experience at Orange Belgium

CASE STUDY INNOVATION IN LOYALTY AND CUSTOMER EXPERIENCE AT ORANGE BELGIUM © 2019 Evolving Systems, Inc. Evolving Systems is a registered trademark of Evolving Systems, Inc. E: [email protected] I T: +1 303 802 1000 I F: +1 303 802 1420 Evolving Systems and Orange Belgium - for the continued management, enhancement and expansion of the customer loyalty program, Orange Thank You – has been recognized by the prestigious Total Telecoms World Communications Awards as a step forward in digital engagement. Evolving was initially selected by Orange to create a brand-new loyalty concept, provide the technical foundation, and deliver a shared new vision to enhance customer loyalty. SITUATION In 2013, Orange Belgium acknowledged a need to revitalise its approach to customer loyalty. Its existing programs weren’t delivering the desired outcomes and additionally were providing little, if any, brand differentiation. Plus, the appearance of aggressive new competitors in the market as well as regulatory changes relating to the mobile industry meant that a new approach was urgently needed to protect and improve the company’s market position. Orange’s initial objectives for its new approach included creating a single program for all markets - pre and postpaid. While addressing churn remained a primary goal, the company realised that traditional loyalty approaches had been ineffective at doing this in the past. “We knew we could make industry-standard offers like increasing megabytes” says Benoit Berthelot, Customer Engagement Manager at Orange Belgium, “but we also knew such offers were easily imitated and did little to really build strong relationships with our subscribers”. Instead, Orange wanted to “rewire” the entire customer relationship and in the process create something more emotionally engaging. -

Annual Financial Statements 2020

ANNUAL FINANCIAL STATEMENTS 2020 CI FIRST ASSET EXCHANGE-TRADED FUNDS DECEMBER 31, 2020 Table of Contents Independent Auditor’s Report .............................................................................................. 1 CI First Asset 1-5 Year Laddered Government Strip Bond Index ETF .......................................... 4 CI First Asset Active Canadian Dividend ETF............................................................................... 12 CI First Asset Active Credit ETF ................................................................................................... 22 CI First Asset Active Utility & Infrastructure ETF ....................................................................... 36 CI First Asset Canadian Buyback Index ETF ................................................................................. 46 CI First Asset Canadian Convertible Bond ETF ............................................................................ 55 CI First Asset Canadian REIT ETF ................................................................................................. 66 CI First Asset CanBanc Income Class ETF.................................................................................... 76 CI First Asset Core Canadian Equity Income Class ETF ............................................................... 84 CI First Asset Energy Giants Covered Call ETF ............................................................................ 93 CI First Asset Enhanced Government Bond ETF.......................................................................... -

Swisscom Sustainability Report 2018

Sustainability Report 2018 Annual Report publications Annual Report 2018 Sustainability Report 2018 2018 at a glance The Annual Report, Sustainability Report and 2018 at a glance together make up Swisscom’s reporting on 2018. The three publications are available online at: swisscom.ch/report2018 “Inspiring people” concept The networked world offers countless opportunities that we canbegin to shape today. Top quality, groundbreaking innovation, deep-rooted commitment – we feel lucky to be able to inspire people and to lead them to embrace the opportunities that a networked future offers. The images used in our reporting show how and where we inspired people in 2018: from high in the Alps to people’s homes, in business and in our Swisscom Shops. A big thank-you to all who took the time to pose for these photographs: Pius and Jeanette Jöhl with their kids at the Oberchäseren alp, a houseshare with friends in Zurich (Seraina Cadonau, Anna Spiess, Linard Baer and Johannes Schutz), Ypsomed AG in Burgdorf, Stefan Mauron, our customer Jeannette Furter, and the entire crew at House of Swisscom in Basel. Corporate Responsibility Fulfilling the expectations of our stakeholder groups in a responsible manner. Introduction Stakeholders’ letter ............................................4 Sustainable environment ......................................5 Material issues ...............................................11 Corporate Priorities and objectives up until 2020 .........................13 Responsibility strategy Priorities and objectives up until -

Mobile Data Consumption Continues to Grow – a Majority of Operators Now Rewarded with ARPU

Industry analysis #3 2019 Mobile data – first half 2019 Mobile data consumption continues to grow – a majority of operators now rewarded with ARPU Taiwan: Unlimited is so last year – Korea: 5G boosts usage Tefficient’s 24th public analysis on the development and drivers of mobile data ranks 115 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the first half of 2019. tefficient AB www.tefficient.com 5 September 2019 1 The data usage per SIM grew for all; everybody climbed our Christmas tree. More than half of the operators could turn that data usage growth into ARPU growth – for the first time a majority is in green. Read on to see who delivered on “more for more” – and who didn’t. Speaking of which, we take a closer look at the development of one of the unlimited powerhouses – Taiwan. Are people getting tired of mobile data? We also provide insight into South Korea – the world’s leading 5G market. Just how much effect did 5G have on the data usage? tefficient AB www.tefficient.com 5 September 2019 2 Fifteen operators now above 10 GB per SIM per month Figure 1 shows the average mobile data usage for 115 reporting or reported1 mobile operators globally with values for the first half of 2019 or for the full year of 2018. DNA, FI 3, AT Zain, KW Elisa, FI LMT, LV Taiwan Mobile, TW 1) FarEasTone, TW 1) Zain, BH Zain, SA Chunghwa, TW 1) *Telia, FI Jio, IN Nova, IS **Maxis, MY Tele2, LV 3, DK Celcom, MY **Digi, MY **LG Uplus, KR 1) Telenor, SE Zain, JO 3, SE Telia, DK China Unicom, CN (handset) Bite, -

Belgian Cable Observatory

Belgian Cable Observatory PRODUCED B Y IDATE O N BEHALF O F O R A N G E BELGIUM UNDER T H E ACADEMIC CONTROL OF PROF A. DE STREEL,DIRECTOR O F C R I D S , NAMUR UNIVERSITY Agenda – What are the impacts of cable opening on Belgian broadband markets so far? Cable opening scores better than copper opening in the past Price trends and competitive environment have not changed much at this stage Investments were upheld Regulatory changes have been decided recently Conclusion: Cable opening is off to an encouraging start, but it is still too early to draw definitive conclusions NGA adoption keeps increasing at a steady pace in Belgium Market shares on the Belgian Residential NGA fixed broadband Net Residential NGA lines additions per player market In number of lines In % of subscriptions Source: BIPT Source: BIPT Cable opening shows better results than copper unbundling COPPER LOCAL LOOP UNBUNDLING HAS FAILED IN BELGIUM, AS ON THE CONTRARY, AFTER ONLY TWO YEARS OF AVAILABILITY, DEMONSTRATED BY STEADILY DECREASING WHOLESALE PRODUCTS SALES BITSTREAM CABLE ADOPTION IS RAPIDLY INCREASING Sales of fully and partially unbundled lines by Proximus, 2010-2017 • Since the opening of the cable market, Orange Belgium as its main Number of lines beneficiary has gained more than 155,000 Cable subscribers in Belgium • This represents an average quarterly increase of +39% in subscribers since Q1 2016 • As a comparison, two years after the beginning of copper local loop unbundling in Belgium, the total of fully and partially unbundled copper lines activated was -

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C. In the Matter of EDGE CABLE HOLDINGS USA, LLC, File No. SCL-LIC-2020-____________ AQUA COMMS (AMERICAS) INC., AQUA COMMS (IRELAND) LIMITED, CABLE & WIRELESS AMERICAS SYSTEMS, INC., AND MICROSOFT INFRASTRUCTURE GROUP, LLC, Application for a License to Land and Operate a Private Fiber-Optic Submarine Cable System Connecting the United States, the United Kingdom, and France, to Be Known as THE AMITIÉ CABLE SYSTEM JOINT APPLICATION FOR CABLE LANDING LICENSE— STREAMLINED PROCESSING REQUESTED Pursuant to 47 U.S.C. § 34, Executive Order No. 10,530, and 47 C.F.R. § 1.767, Edge Cable Holdings USA, LLC (“Edge USA”), Aqua Comms (Americas) Inc. (“Aqua Comms Americas”), Aqua Comms (Ireland) Limited (“Aqua Comms Ireland,” together with Aqua Comms Americas, “Aqua Comms”), Cable & Wireless Americas Systems, Inc. (“CWAS”), and Microsoft Infrastructure Group, LLC (“Microsoft Infrastructure”) (collectively, the “Applicants”) hereby apply for a license to land and operate within U.S. territory the Amitié system, a private fiber-optic submarine cable network connecting the United States, the United Kingdom, and France. The Applicants and their affiliates will operate the Amitié system on a non-common-carrier basis, either by providing bulk capacity to wholesale and enterprise customers on particularized terms and conditions pursuant to individualized negotiations or by using the Amitié cable system to serve their own internal business connectivity needs. The existence of robust competition on U.S.-U.K., U.S.-France, and (more broadly) U.S.-Western Europe routes obviates any need for common-carrier regulation of the system on public-interest grounds. -

ECC REPORT 143 Electronic Communications Committee

ECC REPORT 143 Electronic Communications Committee (ECC) within the European Conference of Postal and Telecommunications Administrations (CEPT) PRACTICAL IMPROVEMENTS IN HANDLING 112 EMERGENCY CALLS: CALLER LOCATION INFORMATION Lisbon, April 2010 ECC REPORT 143 Page 2 0 EXECUTIVE SUMMARY Each year in the European Union several millions of citizens dial the emergency call number to access emergency services. Due to increasing penetration of mobile telephony in the society, the share of emergency calls emanating from mobile networks is rapidly outgrowing emergency calls for fixed networks; this causes that an emergency situation mobile callers are increasingly not able to indicate the precise location for an optimum response. Similarly, VoIP services are substituting voice calls over traditional networks, customers increasingly use VoIP for emergency calls and expecting the same reliability and completeness of the emergency calls service. Location information is normally represented by data indicating the geographic position of the terminal equipment of a user. These data vary in range, indicating in a general way where the user is or very precise, pinpointing the user’s whereabouts to within a few meters. Some location data are effectively a subset of signalling data as they are necessary for setting up a telephone connection. In the framework of Enhanced emergency call services, the availability of location information must serve three main goals: Route the calls to the right emergency call centre; Locate the caller and/or the incident site. Dispatch the most appropriate emergency response team(s); The Report identify the most relevant regulatory principles applicable to caller location requirements in the context of emergency calls and analyses the location information standards produced by ETSI as a Standard Development Organization for fixed, mobile and IP communications networks. -

Global Pay TV Operator Forecasts

Global Pay TV Operator Forecasts Table of Contents Published in October 2016, this 190-page electronically-delivered report comes in two parts: A 190-page PDF giving a global executive summary and forecasts. An excel workbook giving comparison tables and country-by-country forecasts in detail for 400 operators with 585 platforms [125 digital cable, 112 analog cable, 208 satellite, 109 IPTV and 31 DTT] across 100 territories for every year from 2010 to 2021. Forecasts (2010-2021) contain the following detail for each country: By country: TV households Digital cable subs Analog cable subs Pay IPTV subscribers Pay digital satellite TV subs Pay DTT homes Total pay TV subscribers Pay TV revenues By operator (and by platform by operator): Pay TV subscribers Share of pay TV subscribers by operator Subscription & VOD revenues Share of pay TV revenues by operator ARPU Countries and operators covered: Country No of ops Operators Algeria 4 beIN, OSN, ART, Algerie Telecom Angola 5 ZAP TV, DStv, Canal Plus, Angola Telecom, TV Cabo Argentina 3 Cablevision; Supercanal; DirecTV Australia 1 Foxtel Austria 3 Telekom Austria; UPC; Sky Bahrain 4 beIN, OSN, ART, Batelco Belarus 2 MTIS, Zala Belgium 5 Belgacom; Numericable; Telenet; VOO; Telesat/TV Vlaanderen Bolivia 3 DirecTV, Tigo, Entel Bosnia 3 Telemach, M:Tel; Total TV Brazil 5 Claro; GVT; Vivo; Sky; Oi Bulgaria 5 Blizoo, Bulsatcom, Vivacom, M:Tel, Mobitel Canada 9 Rogers Cable; Videotron; Cogeco; Shaw Communications; Shaw Direct; Bell TV; Telus TV; MTS; Max TV Chile 6 VTR; Telefonica; Claro; DirecTV; -

Monthly Industry Overview

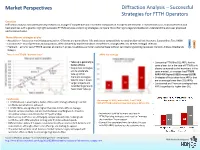

Market Perspectives Diffraction Analysis – Successful Strategies for FTTH Operators Overview Diffraction Analysis conducted primary research on a range of competitive and incumbent companies in Europe to benchmark FTTH/B services so as to analyse trends and best practices with a goal to: highlight successful FTTH/B services and pricing strategies; compare fibre offerings to legacy broadband; understand the end-user proposed and perceived value. Three different strategies at play ARPU • Acquisition – focuses on maximising penetration. Offerings are generally no frills and priced competitively to existing alternatives: Networx; Superonline; Teo; HKBN TAKE • Constrained – mix of premium and acquisition, often dictated by market condition: Rostelecom; Orange; KPN; Izzi; M-Net; Portugal Telecom - UP • Premium – aims for sexy FTTH/B services at premium prices, to address a smaller customer base without cannibalising existing revenues: Verizon; Altibox; Bredbands Bolaget There is no FTTH/B “demand issue” ARPU by strategy • Take-up is generally a • Comparing FTTH/B to DSL ARPU for the factor of time same player (or in the case of FTTH/B only • Acquisition strategies players compared to the incumbent in the aim to accelerate same market), on average has FTTH/B take-up while ARPU 46% higher (US$55 versus US$38) Premium strategies • Strategies of Acquisition have ARPUs that tend to slow it down are on average lower than DSL ARPUs • Larger projects and • Constrained and Premium strategies have incumbents generally ARPUs significantly higher than DSL -

Fritz-Handleiding-Ziggokpn-7490.Pdf

Handleiding: Hoe sluit je de FRITZ!Box aan achter een Ziggo of KPN modem Pagina | 1 Inhoudsopgave Pagina 1 - Voorblad Pagina 2 - Inhoudsopgave Pagina 3 - Voorwoord / Tips Pagina 4 - Instellen van de taal Pagina 5 - Instellen van het land Pagina 6 - Kiezen van de Annex verbinding Pagina 7 - Kiezen van het password Pagina 8 - 9 - Kiezen van de Internet Service Provider Pagina 9 - 10 - Set Up Internet Connection / Instellen snelheid DSL line Pagina 11 - 12 - Opslaan instellingen en testen internet connectie Pagina 13 - Einde van het instellen van de internetverbinding Pagina 14 - Instellen telefonie Ziggo via de FRITZ!Box Pagina 15 - Verbindingstype telefonie kiezen Pagina 16 - Ingeven telefoonnummer / Eind instellen telefonie Pagina 17 - Slotwoord / Tel.nr Helpdesk AVM / FAQ Pagina | 2 Het instellen van de FRITZ!Box als u een Ziggo of KPN modem/router heeft Allereerst bedankt voor de aanschaf van de FRITZ!Box. Wij wensen u er veel plezier mee! Via deze handleiding lopen we stap voor stap met u door wat u moet doen om de FRITZ!Box in de juiste instellingen te krijgen. Dit neemt enkele minuten in beslag. De handleiding is alleen om uw internet en telefonie in te stellen. Aan het TV signaal verandert niets en zal gewoon via uw Ziggo of KPN modem blijven gaan. Het is aan te raden om uw Ziggo of KPN modem in Bridge mode te zetten. Dit houdt in dat de Ziggo of KPN modem geen enkel signaal meer uitzendt wat storing kan geven. Hij geeft alleen nog via de LAN 1 poort internet door naar de FRITZ!Box. -

Vodafone Revolutionises Roaming Rules

VODAFONE REVOLUTIONISES ROAMING RULES VODAFONE ALLOWS CUSTOMERS TO MAKE OVERSEAS CALLS AT DOMESTIC RATES Milan, May 17, 2005 – The Vodafone Group is about to revolutionise roaming prices, responding to customers’ demands for greater transparency and clarity when making or receiving calls whilst abroad. June 1 is to see the launch of Vodafone Passport, the first price plan forming part of the Group’s new Vodafone Travel Promise package. Vodafone Passport enables Vodafone customers who access the Group’s networks to make calls at domestic rates, paying just € 1.00 at the start of each call. The new offering provides Vodafone customers with greater transparency, giving better value for money and eliminating any doubts about cost effectiveness. When overseas Vodafone customers will thus be able to: • Call Italy: at the same prices charged for domestic calls, paying an additional €1.00 per call. • Receive calls: talking free of charge having paid a connection fee of just €1.00. “The nature of the Vodafone Group enables us to offer a veritable revolution in roaming services,” claimed Pietro Guindani, CEO of Vodafone Italia. “Vodafone Passport will make the customer feel at home in any country with a Vodafone network.” The new service will be available in Germany, Greece, Italy, the Netherlands, Spain, Sweden, Fiji and Japan from June 1. Hungary, Malta, Portugal, Ireland, the UK, Albania, Australia and New Zealand will introduce the price plan during the summer. Customers who use the SFR (France), Swisscom (Switzerland) and Proximus (Belgium) networks will also subsequently gain access. Vodafone Passport is the latest innovation created by the Vodafone Group with the aim of making it easier to make mobile calls when abroad and thus increase the use of roaming services. -

Customized Area of Territory – RP126 – Sim Services

Area of Territory – RP126 Page 1 (3) Version D rel01, 2012-11-21 Appendix 2 Agreement no: M11042701 Customized Area of Territory – RP126 – Sim Services Country Operator Brand GPR S Price Grou p ALAND, FINLAND Alands Mobiltelefon AMT ALBANIA Vodafone Albania Vodafone AUSTRALIA Telstra Corporation Limited Telstra AUSTRALIA Vodafone Network Pty Ltd Vodafone AUSTRIA A1 Telekom Austria AG A1 AUSTRIA Orange Austria Orange Telecommunication GmbH AUSTRIA T-Mobile Austria GmbH T-mobile BELARUS FE “Velcom” Velcom (MDC) BELGIUM Belgacom SA/NV Belgacom (former Proximus) BELGIUM BASE (KPN Orange Belgium) BASE BELGIUM Mobistar S.A. Mobistar BULGARIA Mobiltel M-tel CHINA, PEOPLES REP. China Mobile China Mobile CHINA, PEOPLES REP. China Unicom China Unicom CROATIA Croatian Telecom Inc. Croatian Telecom (former T-Mobile) CYPRUS MTN Cyprus Ltd (Areeba) MTN CYPRUS Cyprus Telecommunications Cytamobile- Vodafone CZECH REPUBLIC Telefónica O2 (EuroTel) Telefónica O2 CZECH REPUBLIC T-Mobile Czech Rep T-mobile CZECH REPUBLIC Vodafone Czech Rep Vodafone DENMARK TDC TDC DENMARK Telenor Denmark Telenor EGYPT Etisalat Misr Etisalat EGYPT Vodafone Egypt Vodafone ESTONIA Elisa Eesti Elisa ESTONIA Estonian Mobile Telephone EMT ESTONIA Tele2 Eesti Tele2 FAROE ISLANDS, THE Faroese Telecom Faroese Telecom FINLAND DNA Finland (fd Networks DNA (Finnet) FINLAND Elisa Finland Elisa FINLAND TeliaSonera Finland TeliaSonera FRANCE Bouygues Telecom Bouygues FRANCE Orange (France Telecom) Orange FRANCE Vivendi SFR Area of Territory – RP126 Page 2 (3) Version D rel01, 2012-11-21 GERMANY E-Plus Mobilfunk E-plus GERMANY Telefonica O2 Germany O2 GERMANY Telekom Deutschland GmbH Telekom (former T-mobile) Deutschland GERMANY Vodafone D2 Vodafone GREECE Vodafone Greece (Panafon) Vodafone GREECE Wind Hellas Wind Telecommunications HUNGARY Pannon GSM Távközlési Pannon HUNGARY Vodafone Hungary Ltd.