Base Telenet 10 Jaar Timeline-V12 FR

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TV Channel Distribution in Europe: Table of Contents

TV Channel Distribution in Europe: Table of Contents This report covers 238 international channels/networks across 152 major operators in 34 EMEA countries. From the total, 67 channels (28%) transmit in high definition (HD). The report shows the reader which international channels are carried by which operator – and which tier or package the channel appears on. The report allows for easy comparison between operators, revealing the gaps and showing the different tiers on different operators that a channel appears on. Published in September 2012, this 168-page electronically-delivered report comes in two parts: A 128-page PDF giving an executive summary, comparison tables and country-by-country detail. A 40-page excel workbook allowing you to manipulate the data between countries and by channel. Countries and operators covered: Country Operator Albania Digitalb DTT; Digitalb Satellite; Tring TV DTT; Tring TV Satellite Austria A1/Telekom Austria; Austriasat; Liwest; Salzburg; UPC; Sky Belgium Belgacom; Numericable; Telenet; VOO; Telesat; TV Vlaanderen Bulgaria Blizoo; Bulsatcom; Satellite BG; Vivacom Croatia Bnet Cable; Bnet Satellite Total TV; Digi TV; Max TV/T-HT Czech Rep CS Link; Digi TV; freeSAT (formerly UPC Direct); O2; Skylink; UPC Cable Denmark Boxer; Canal Digital; Stofa; TDC; Viasat; You See Estonia Elion nutitv; Starman; ZUUMtv; Viasat Finland Canal Digital; DNA Welho; Elisa; Plus TV; Sonera; Viasat Satellite France Bouygues Telecom; CanalSat; Numericable; Orange DSL & fiber; SFR; TNT Sat Germany Deutsche Telekom; HD+; Kabel -

Telenet Opens Your World Annual Report 2005 Internet Customers (000S) Telephony Customers (000S) Revenue (In Million Euro) EBITDA (In Million Euro - US GAAP)

THE MULTIPLE FACETS OF GROWTH Telenet opens your world Annual Report 2005 Internet customers (000s) Telephony customers (000s) Revenue (in million euro) EBITDA (in million euro - US GAAP) 624 364 737,5 330,6 528 286 681,1 299,6 235 413 230,1 187 181 502,3 301 307,1 82,6 196 104 172,3 85 -18,6 2000 2001 2002 2003 2004 2005 2000 2001 2002 2003 2004 2005 2001 2002 2003 2004 2005 2001 2002 2003 2004 2005 Internet customers (000s) Telephony customers (000s) Revenue (in million euro) EBITDA (in million euro - US GAAP) Total iDTV boxes sold 624 364 Capital Expenditure (in million euro - US GAAP) Total debt / EBITDA ratio 737,5 18 330,6 528 16.8 286 200,5 681,1 16 299,6 100,000 235 176,7 413 14 230,1 187 181 502,3 141,5 12 301 10 307,1 82,6 Telenet in a nutshell 100,4 196 104 8 6.72 172,3 67,4 6 4.96 85 3.85 4 -18,6 2 2000 2001 2002 2003 2004 2005 2000 2001 2002 2003 2004 2005 2001 2002 2003 2004 2005 2001 2002 2003 2004 2005 Aug 05 Sept Oct Nov Dec Jan 06 0 2001 2002 2003 2004 2005 2002 2003 2004 2005 Internet customers (000s) Telephony customers (000s) Revenue (in million euro) EBITDA (in million euro - US GAAP) Total iDTV boxes sold 624 Capital ExpenditureFinancial (in million euro364 - US GAAP) Total debt / EBITDA ratio Consortium GIMV 18 737,5 330,6 528 4.00% 9.69% 286 Other 16.8 681,1 299,6 200,5 (0.3% Suez and 0.3% banks) 16 100,000 235 413 Interkabel 176,7 230,1 Mixed 187 14 4.15% 502,3 intercommunales181 141,5 12 301 & Electrabel 16.50% 10307,1 82,6 196 104 100,4 8 6.72 172,3 6 85 67,4 4.96 3.85 -18,6 Free float 4 Liberty Global 43.91% -

Telenet Has 600,000 Fixed Line Customers

PRESS RELEASE Telenet has 600,000 fixed line customers Mechelen, 11 September 2008 – Today Telenet recorded its 600,000 th fixed line customer. The success of Telenet in the area of fixed line telephony is chiefly the result of solid innovation power and well-thought out product development: Telenet was the first company in Belgium to introduce flat-fee phone formulae to the market with FreePhone and FreePhone 24. Last week Telenet launched FreePhone Europe as part of the new Shakes. With 600,000 customers Telenet now has a penetration of nearly 25% of the Flemish market. Approximately one in four Flemish families makes a call using a Telenet fixed line. “The fixed phone line continues to be popular with the middle-aged and seniors”, emphasises Dann Rogge, Director of Product Marketing Telephony and Internet at Telenet, “but we are now seeing an increase in the number of young families opting for a fixed line again. Comfort, operating certainty and a low price are the deciding factors in their decision to go for a fixed line. Young families want to be able to reach each other "as a family" at all times, and they want to be able to do so at an attractive price. That’s not possible with just one subscription for a mobile phone, because at the end of the day a GSM is a very ‘individual’ device and significantly more expensive than a fixed line phone". New phone product: FreePhone Europe. On 8 September the new Telenet Shakes were launched. FreePhone Europe has been introduced for all combinations with a phone product. -

Results and Presentations

March 18, 2014 Full Year 2013 Results 1 An International Cable Operator in Attractive Markets 9 Territories Belgium Luxembourg 14m Homes Passed Western Europe Switzerland France 3m Cable Customers Portugal 6.6m Cable RGUs Israel Dominican Republic Guadeloupe & Overseas Martinique Territories French Guiana Mayotte La Réunion Note: figures above include Orange Dominicana and Tricom 2 Altice SA Full Year Results - Highlights Financials Recent Strategic Initiatives Liquidity & Capital Full-year pro forma1 revenue up 0.7% Successful IPO creates equity IPO raised c€750m primary proceeds to €3.2bn currency for future opportunities & created 26% free float • mainly driven by Israel & France, partially offset by Portugal and Increased Numericable stake to 40% Altice SA consolidated net debt of ODO €6,255bn Closed Tricom acquisition in Full-year pro forma EBITDA up 6.0% Dominican Republic; Orange to follow Altice VII net debt of €3,509bn to €1.36bn €384m consolidated cash and • Mainly driven by Israel & Portugal undrawn revolvers of €163m Full-year proforma OpFCF2 up 27% to €667m Triple-play penetration up 5% pts to 61% Notes: 1 These results reflect the pro forma results of the Altice S.A. group, including the planned acquisition of Orange Dominicana, but excluding Tricom and Mobius. 2 Defined here and throughout presentation as EBITDA - Capex 3 Altice S.A Key Operational Highlights Israel France Reorganization program finished 5% cable customer growth 3.6% ARPU growth driven by strong triple-play and high 2% ARPU growth speed -

Annual Report 2019 | 3 4

FINANCIAL REPORT 2019 This page is intentionally left blank. Compliance Statement The undersigned certify that, to their knowledge: • The annual report of the Board of Directors gives a fair view • The consolidated financial statements which have been on the development and performance of the business and the prepared in accordance with the applicable standards, give a position of the Company and the entities included in the true and fair view of the equity, financial position and consolidation, together with a description of the principal risks performance of the Company and the entities included in the and uncertainties to which they are exposed. consolidation; John Porter Bert De Graeve Chief Executive Officer Chairman Table of contents Consolidated annual report of the board of directors for 2019 to the shareholders of Telenet Group Holding NV 6 Definitions ......................................................... 7 Important reporting changes ............................. 7 1. Information on the company 10 1.1 Overview ............................................. 10 1.2 Video ................................................... 11 1.3 Enhanced video .................................... 11 1.4 Broadband internet .............................. 11 1.5 Telephony ............................................ 12 1.6 Business services .................................. 13 1.7 Network .............................................. 13 1.8 Strategy ............................................... 14 2. Discussion of the consolidated financial -

Investor & Analyst Conference 2011

Investor & Analyst Conference 2011 > Driving the future London – February 28, 2011 New York – March 2, 2011 Safe Harbor Disclaimer Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995. Various statements contained in this document constitute “forward-looking statements” as that term is defined under the U.S. Private Securities Litigation Reform Act of 1995. Words like “believe,” “anticipate,” “should,” “intend,” “plan,” “will,” “expects,” “estimates,” “projects,” “positioned,” “strategy,” and similar expressions identify these forward-looking statements related to our financial and operational outlook, dividend policy and future growth prospects, which involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements or industry results to be materially different from those contemplated, projected, forecasted, estimated or budgeted whether expressed or implied, by these forward-looking statements. These factors include: potential adverse developments with respect to our liquidity or results of operations; potential adverse competitive, economic or regulatory developments; our significant debt payments and other contractual commitments; our ability to fund and execute our business plan; our ability to generate cash sufficient to service our debt; interest rate and currency exchange rate fluctuations; the impact of new business opportunities requiring significant up-front investments; our ability to attract and retain customers and increase our overall -

Telenet Future

Case Study Telenet Future- Proofs Network with Managed Business Solution The Managed Business Solution (MBN) from Benu Networks em- powers Telenet to rapidly provision new services CUSTOMER PROFILE As a provider of entertainment and telecommunication services in Belgium, Telenet Group is always looking for the perfect experience in the digital world for its customers. Under the brand name Telenet, the company focuses on offering digital television, high-speed Internet and fixed and mobile telephony services to residential customers in Flanders, Brussels and a part of Wallonia (Botte du Hainaut). Under the brand name BASE, it supplies mobile telephony in Belgium. The Telenet Business department serves the business market in Belgium and Luxembourg with COMPANY connectivity, hosting and security solutions. More than 3,000 employees have one Telenet aim in mind: making living and working easier and more pleasant. BUSINESS TYPE MARKET OVERVIEW Service Provider Due to their size and limited resources, small businesses don’t have the in-house IT expertise to adequately address their technological needs. In addition, small LOCATION businesses are now being explicitly targeted for cyberattacks over large businesses. Belgium This leaves them especially vulnerable to threats, with upwards of 60% of all SMBs reporting that they have been the victim of some type of cyberattack. Furthermore, in today’s “always connected’ world, owners realize that they must also meet the “By moving key network needs of their patrons who have come to expect the availability of secure, guest functions to the cloud, connectivity as the “norm” at any business they visit. These factors have driven this ingenious solution small businesses to turn to managed services as the solution to address their enables us to add new IT demands by providing the IT expertise at a lower cost, with less downtime, services rapidly and predictable performance, robust security, and a better user experience. -

Results from the Third Quarterly

Euskaltel – Third Quarter 2015 Results 28 October 2015 Executive summary (i/iv) 241 247 118 173 Main figures for the business for the periods ended September 30th, 2015 and 2014 28 119 Key financials for the 9-month period ended September 30th, 2015 and 2014 177 132 177 143 177 159 3Q15 adjusted vs 0 41 3Q15 3Q15 Adjusted (**) 3Q14 3Q14 % 3Q14 102 184 Total Revenue 244.4 244.4 239.0 5.4 2.3% 153 255 Residential 151.5 151.5 146.1 5.4 3.7% 123 178 151 199 Business 69.0 69.0 70.4 (1.4) -2.0% 73 139 Wholesale & Other 17.3 17.3 17.3 0.0 0.1% 194 218 Others (*) 6.6 6.6 5.2 1.4 27.3% 172 205 141 187 Ebitda 103.9 116.7 112.3 4.4 3.9% 206 Ebitda Margin 42.5% 47.7% 47.0% 0.8 pp 52 OpFCF 75.3 88.1 86.3 1.8 2.0% 3 conversion rate 72.5% 75.5% 76.9% -1.4 pp Net Income (3.3) 36.0 25.6 10.4 40.7% Net Financial Debt 449.8 266.6 183.2 68.7% Net Debt / Ebitda 2.8x 1.7x 1.1x (*) Profit neutral operations (**) Excluded costs related to the IPO process, debt cancellation and the acquisition of R Cable. 1 Executive summary (ii/iv) Business: Inflexion point in revenue 241 247 118 173 28 119 • Total revenue for the period ended September 30th, 2015, have been €244.4mn vs €239.0mn, +€5.4mn (+2.3% YoY). -

ECC REPORT 143 Electronic Communications Committee

ECC REPORT 143 Electronic Communications Committee (ECC) within the European Conference of Postal and Telecommunications Administrations (CEPT) PRACTICAL IMPROVEMENTS IN HANDLING 112 EMERGENCY CALLS: CALLER LOCATION INFORMATION Lisbon, April 2010 ECC REPORT 143 Page 2 0 EXECUTIVE SUMMARY Each year in the European Union several millions of citizens dial the emergency call number to access emergency services. Due to increasing penetration of mobile telephony in the society, the share of emergency calls emanating from mobile networks is rapidly outgrowing emergency calls for fixed networks; this causes that an emergency situation mobile callers are increasingly not able to indicate the precise location for an optimum response. Similarly, VoIP services are substituting voice calls over traditional networks, customers increasingly use VoIP for emergency calls and expecting the same reliability and completeness of the emergency calls service. Location information is normally represented by data indicating the geographic position of the terminal equipment of a user. These data vary in range, indicating in a general way where the user is or very precise, pinpointing the user’s whereabouts to within a few meters. Some location data are effectively a subset of signalling data as they are necessary for setting up a telephone connection. In the framework of Enhanced emergency call services, the availability of location information must serve three main goals: Route the calls to the right emergency call centre; Locate the caller and/or the incident site. Dispatch the most appropriate emergency response team(s); The Report identify the most relevant regulatory principles applicable to caller location requirements in the context of emergency calls and analyses the location information standards produced by ETSI as a Standard Development Organization for fixed, mobile and IP communications networks. -

THE E-HEALTH OPPORTUNITY for the TELECOMMUNICATION INDUSTRY and PORTUGAL TELECOM – a CASE STUDY Cover

THE E-HEALTH OPPORTUNITY FOR THE TELECOMMUNICATION INDUSTRY AND PORTUGAL TELECOM – A CASE STUDY Cover Francisco Borges d’Almeida Nascimento Master of Science in Business Administration Orientador: Prof. Jorge Lengler, ISCTE Business School, Departamento de Marketing, Operações e Gestão Geral April 2015 THE E-HEALTH OPPORTUNITY FOR THE TELECOMMUNICATION INDUSTRY AND PORTUGAL TELECOM – A CASE STUDY Francisco Borges d’Almeida Nascimento Case Study – E-Health in the telecommunication industry and at PT Abstract Electronic-Health (e-health) is a recent answer to some pressing challenges on health. Aging of western societies and treatments’ rising costs raised doubts about health systems’ sustainability. Individuals, companies and public administration alike are looking for technology to find aid in addressing these challenges. Several industries are tacking those issues offering innovative solutions among which Telecommunication’s. Nonetheless, this industry is facing challenges from over- the-top players menacing its business model. Portugal Telecom shares these challenges and is looking to diversify to guarantee future growth, namely, by developing in e-health solutions. This case study follows two important threads in strategy literature: diversification and the resource-based view, applied Portugal Telecom and the e-health opportunity. As a case study, it aims providing readers a tool to better understand and employ strategic management concepts and frameworks in an applied business context. E-health as an opportunity for growth to Telecommunication companies and Portugal Telecom is described from three points of view: i) an actual market need ii) that may be addressed by Telecommunication companies and iii) should be addressed by those companies as they need to grow. -

Global Pay TV Operator Forecasts

Global Pay TV Operator Forecasts Table of Contents Published in October 2016, this 190-page electronically-delivered report comes in two parts: A 190-page PDF giving a global executive summary and forecasts. An excel workbook giving comparison tables and country-by-country forecasts in detail for 400 operators with 585 platforms [125 digital cable, 112 analog cable, 208 satellite, 109 IPTV and 31 DTT] across 100 territories for every year from 2010 to 2021. Forecasts (2010-2021) contain the following detail for each country: By country: TV households Digital cable subs Analog cable subs Pay IPTV subscribers Pay digital satellite TV subs Pay DTT homes Total pay TV subscribers Pay TV revenues By operator (and by platform by operator): Pay TV subscribers Share of pay TV subscribers by operator Subscription & VOD revenues Share of pay TV revenues by operator ARPU Countries and operators covered: Country No of ops Operators Algeria 4 beIN, OSN, ART, Algerie Telecom Angola 5 ZAP TV, DStv, Canal Plus, Angola Telecom, TV Cabo Argentina 3 Cablevision; Supercanal; DirecTV Australia 1 Foxtel Austria 3 Telekom Austria; UPC; Sky Bahrain 4 beIN, OSN, ART, Batelco Belarus 2 MTIS, Zala Belgium 5 Belgacom; Numericable; Telenet; VOO; Telesat/TV Vlaanderen Bolivia 3 DirecTV, Tigo, Entel Bosnia 3 Telemach, M:Tel; Total TV Brazil 5 Claro; GVT; Vivo; Sky; Oi Bulgaria 5 Blizoo, Bulsatcom, Vivacom, M:Tel, Mobitel Canada 9 Rogers Cable; Videotron; Cogeco; Shaw Communications; Shaw Direct; Bell TV; Telus TV; MTS; Max TV Chile 6 VTR; Telefonica; Claro; DirecTV; -

Monthly Industry Overview

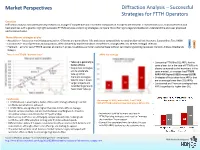

Market Perspectives Diffraction Analysis – Successful Strategies for FTTH Operators Overview Diffraction Analysis conducted primary research on a range of competitive and incumbent companies in Europe to benchmark FTTH/B services so as to analyse trends and best practices with a goal to: highlight successful FTTH/B services and pricing strategies; compare fibre offerings to legacy broadband; understand the end-user proposed and perceived value. Three different strategies at play ARPU • Acquisition – focuses on maximising penetration. Offerings are generally no frills and priced competitively to existing alternatives: Networx; Superonline; Teo; HKBN TAKE • Constrained – mix of premium and acquisition, often dictated by market condition: Rostelecom; Orange; KPN; Izzi; M-Net; Portugal Telecom - UP • Premium – aims for sexy FTTH/B services at premium prices, to address a smaller customer base without cannibalising existing revenues: Verizon; Altibox; Bredbands Bolaget There is no FTTH/B “demand issue” ARPU by strategy • Take-up is generally a • Comparing FTTH/B to DSL ARPU for the factor of time same player (or in the case of FTTH/B only • Acquisition strategies players compared to the incumbent in the aim to accelerate same market), on average has FTTH/B take-up while ARPU 46% higher (US$55 versus US$38) Premium strategies • Strategies of Acquisition have ARPUs that tend to slow it down are on average lower than DSL ARPUs • Larger projects and • Constrained and Premium strategies have incumbents generally ARPUs significantly higher than DSL