Belgian Cable Observatory

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Innovation in Loyalty and Customer Experience at Orange Belgium

CASE STUDY INNOVATION IN LOYALTY AND CUSTOMER EXPERIENCE AT ORANGE BELGIUM © 2019 Evolving Systems, Inc. Evolving Systems is a registered trademark of Evolving Systems, Inc. E: [email protected] I T: +1 303 802 1000 I F: +1 303 802 1420 Evolving Systems and Orange Belgium - for the continued management, enhancement and expansion of the customer loyalty program, Orange Thank You – has been recognized by the prestigious Total Telecoms World Communications Awards as a step forward in digital engagement. Evolving was initially selected by Orange to create a brand-new loyalty concept, provide the technical foundation, and deliver a shared new vision to enhance customer loyalty. SITUATION In 2013, Orange Belgium acknowledged a need to revitalise its approach to customer loyalty. Its existing programs weren’t delivering the desired outcomes and additionally were providing little, if any, brand differentiation. Plus, the appearance of aggressive new competitors in the market as well as regulatory changes relating to the mobile industry meant that a new approach was urgently needed to protect and improve the company’s market position. Orange’s initial objectives for its new approach included creating a single program for all markets - pre and postpaid. While addressing churn remained a primary goal, the company realised that traditional loyalty approaches had been ineffective at doing this in the past. “We knew we could make industry-standard offers like increasing megabytes” says Benoit Berthelot, Customer Engagement Manager at Orange Belgium, “but we also knew such offers were easily imitated and did little to really build strong relationships with our subscribers”. Instead, Orange wanted to “rewire” the entire customer relationship and in the process create something more emotionally engaging. -

Annual Financial Statements 2020

ANNUAL FINANCIAL STATEMENTS 2020 CI FIRST ASSET EXCHANGE-TRADED FUNDS DECEMBER 31, 2020 Table of Contents Independent Auditor’s Report .............................................................................................. 1 CI First Asset 1-5 Year Laddered Government Strip Bond Index ETF .......................................... 4 CI First Asset Active Canadian Dividend ETF............................................................................... 12 CI First Asset Active Credit ETF ................................................................................................... 22 CI First Asset Active Utility & Infrastructure ETF ....................................................................... 36 CI First Asset Canadian Buyback Index ETF ................................................................................. 46 CI First Asset Canadian Convertible Bond ETF ............................................................................ 55 CI First Asset Canadian REIT ETF ................................................................................................. 66 CI First Asset CanBanc Income Class ETF.................................................................................... 76 CI First Asset Core Canadian Equity Income Class ETF ............................................................... 84 CI First Asset Energy Giants Covered Call ETF ............................................................................ 93 CI First Asset Enhanced Government Bond ETF.......................................................................... -

Mobile Data Consumption Continues to Grow – a Majority of Operators Now Rewarded with ARPU

Industry analysis #3 2019 Mobile data – first half 2019 Mobile data consumption continues to grow – a majority of operators now rewarded with ARPU Taiwan: Unlimited is so last year – Korea: 5G boosts usage Tefficient’s 24th public analysis on the development and drivers of mobile data ranks 115 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the first half of 2019. tefficient AB www.tefficient.com 5 September 2019 1 The data usage per SIM grew for all; everybody climbed our Christmas tree. More than half of the operators could turn that data usage growth into ARPU growth – for the first time a majority is in green. Read on to see who delivered on “more for more” – and who didn’t. Speaking of which, we take a closer look at the development of one of the unlimited powerhouses – Taiwan. Are people getting tired of mobile data? We also provide insight into South Korea – the world’s leading 5G market. Just how much effect did 5G have on the data usage? tefficient AB www.tefficient.com 5 September 2019 2 Fifteen operators now above 10 GB per SIM per month Figure 1 shows the average mobile data usage for 115 reporting or reported1 mobile operators globally with values for the first half of 2019 or for the full year of 2018. DNA, FI 3, AT Zain, KW Elisa, FI LMT, LV Taiwan Mobile, TW 1) FarEasTone, TW 1) Zain, BH Zain, SA Chunghwa, TW 1) *Telia, FI Jio, IN Nova, IS **Maxis, MY Tele2, LV 3, DK Celcom, MY **Digi, MY **LG Uplus, KR 1) Telenor, SE Zain, JO 3, SE Telia, DK China Unicom, CN (handset) Bite, -

Proximus at a Glance

Annual report 2019 group Table of content Proximus at a glance 5 Foreword from our CEO & our Chairman 1 8 Who we are & what we do 12 Key financial highlights 16 Key achievements Creating an inclusive, safe, sustainable and prosperous digital Belgium 21 Contributing to society while creating value for our stakeholders 2 23 Enabling a better digital life 32 Caring for our stakeholders 43 Contributing to society 51 Respecting our planet Governance and compliance, safeguarding long-term value 58 Corporate governance statement 75 Regulatory framework 3 79 Risk management report 88 Remuneration report 97 Proximus share Appendix 105 Overview of non-financial information 109 Transparency 4 121 Social figures 125 Environmental figures 128 GRI content index 145 KPI definition Proximus Group I Annual report 2019 2 Proximus at a glance Sustainability Governance and Compliance Appendix Non-financial reporting approach 2019 For the Non-Financial information included in this Annual Report, we followed the indications of the Global Reporting Initiative (GRI) guide (core option). We have detailed our reporting approach in the Transparency section. Proximus answers several questionnaires on Sustainable and Responsible investments such as Sustainalytics, Vigeo Eiris, MSCI, OEKOM ISS and Dow Jones Sustainability Index. Our ambition is to keep improving our performance by comparing it with that of peers. In 2019, we were listed or scored as follows on the different indices: • CDP Supplier Engagement leader board • Constituent company of the FTSE4Good Index Series • OEKOM ISS: C • DJSI: 52 • Sustainalytics: 68 • Vigeo Eiris (not included in indices). In this 2019 report, we show how we create value for our stakeholders and society, structuring the information around four strategic areas: Enabling a better digital life, Caring for our stakeholders, Contributing to society and Respecting our planet. -

Eutelsat S.A. €300,000,000 3.125% Bonds Due 2022 Issue Price: 99.148 Per Cent

EUTELSAT S.A. €300,000,000 3.125% BONDS DUE 2022 ISSUE PRICE: 99.148 PER CENT The €300,000,000 aggregate principal amount 3.125% per cent. bonds due 10 October 2022 (the Bonds) of Eutelsat S.A. (the Issuer) will be issued outside the Republic of France on 9 October 2012 (the Bond Issue). Each Bond will bear interest on its principal amount at a fixed rate of 3.125 percent. per annum from (and including) 9 October 2012 (the Issue Date) to (but excluding) 10 October 2022, payable in Euro annually in arrears on 10 October in each year and commencing on 10 October 2013, as further described in "Terms and Conditions of the Bonds - Interest"). Unless previously redeemed or purchased and cancelled in accordance with the terms and conditions of the Bonds, the Bonds will be redeemed at their principal amount on 10 October 2022 (the Maturity Date). The Issuer may at its option, and in certain circumstances shall, redeem all (but not part) of the Bonds at par plus any accrued and unpaid interest upon the occurrence of certain tax changes as further described in the section "Terms and Conditions of the Bonds - Redemption and Purchase - Redemption for tax reasons". The Bondholders may under certain conditions request the Issuer to redeem all or part of the Bonds following the occurrence of certain events triggering a downgrading of the Bonds as further described in the Section "Terms and Conditions of the Bonds — Redemption and Purchase - Redemption following a Change of Control". The obligations of the Issuer in respect of principal and interest payable under the Bonds constitute direct, unconditional, unsecured and unsubordinated obligations of the Issuer and shall at all times rank pari passu among themselves and pari passu with all other present or future direct, unconditional, unsecured and unsubordinated obligations of the Issuer, as further described in "Terms and Conditions of the Bonds - Status". -

EGM Presentation

Development of the Fiber Champion strategy to achieve a long-term sustainable positioning in a highly dynamic broadband market FTTB/H The strategy requires a significant amount of new capital with a total anticipated network upgrade investment of c.€2bn over the next 10 years, resulting in negative cash flows over the course of the next years Fiber Champion Strategy Announcement of the public takeover offer by Morgan Stanley Infrastructure Partners Open Long-term Access customer (“MSIP”) creates the opportunity for Tele Columbus to raise the capital needed in order to Strategy relationships be able to execute the strategy _________ Definition of three pillar strategy To achieve a more sustainable capital structure and enable the further implementation of the Fiber Champion strategy, the following prerequisites need to be met: . Shareholder approval for the €475m capital increase, which is backed by the BidCo up to the full amount upon successful completion of the transaction . Minimum acceptance threshold of 50% . Sufficient consent of bond and loan creditors to waive their Change-of-Control (“CoC”) rights . Regulatory approvals Furthermore and upon successful completion of the transaction, bidder intends to inject additional equity in the amount of €75m in order to further support the implementation of the strategy 2 % FTTB/H coverage by federal state1 %-share of TC`s total TWU HC2 by federal state Hamburg 71% 2% Schleswig-H. 23% 1% Bavaria 14% 16% Nordrhine-W. 11% 2% Saxony 10% 23% Mecklenburg-V. 9% 3% Lower Saxony 9% 1% Hesse 9% 2% Saxony-A. 7% 10% Brandenburg 6% 10% Baden-W. 4% 2% Rhineland-P. -

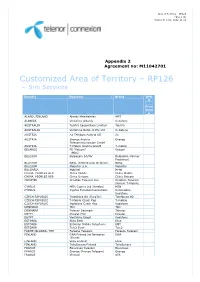

Customized Area of Territory – RP126 – Sim Services

Area of Territory – RP126 Page 1 (3) Version D rel01, 2012-11-21 Appendix 2 Agreement no: M11042701 Customized Area of Territory – RP126 – Sim Services Country Operator Brand GPR S Price Grou p ALAND, FINLAND Alands Mobiltelefon AMT ALBANIA Vodafone Albania Vodafone AUSTRALIA Telstra Corporation Limited Telstra AUSTRALIA Vodafone Network Pty Ltd Vodafone AUSTRIA A1 Telekom Austria AG A1 AUSTRIA Orange Austria Orange Telecommunication GmbH AUSTRIA T-Mobile Austria GmbH T-mobile BELARUS FE “Velcom” Velcom (MDC) BELGIUM Belgacom SA/NV Belgacom (former Proximus) BELGIUM BASE (KPN Orange Belgium) BASE BELGIUM Mobistar S.A. Mobistar BULGARIA Mobiltel M-tel CHINA, PEOPLES REP. China Mobile China Mobile CHINA, PEOPLES REP. China Unicom China Unicom CROATIA Croatian Telecom Inc. Croatian Telecom (former T-Mobile) CYPRUS MTN Cyprus Ltd (Areeba) MTN CYPRUS Cyprus Telecommunications Cytamobile- Vodafone CZECH REPUBLIC Telefónica O2 (EuroTel) Telefónica O2 CZECH REPUBLIC T-Mobile Czech Rep T-mobile CZECH REPUBLIC Vodafone Czech Rep Vodafone DENMARK TDC TDC DENMARK Telenor Denmark Telenor EGYPT Etisalat Misr Etisalat EGYPT Vodafone Egypt Vodafone ESTONIA Elisa Eesti Elisa ESTONIA Estonian Mobile Telephone EMT ESTONIA Tele2 Eesti Tele2 FAROE ISLANDS, THE Faroese Telecom Faroese Telecom FINLAND DNA Finland (fd Networks DNA (Finnet) FINLAND Elisa Finland Elisa FINLAND TeliaSonera Finland TeliaSonera FRANCE Bouygues Telecom Bouygues FRANCE Orange (France Telecom) Orange FRANCE Vivendi SFR Area of Territory – RP126 Page 2 (3) Version D rel01, 2012-11-21 GERMANY E-Plus Mobilfunk E-plus GERMANY Telefonica O2 Germany O2 GERMANY Telekom Deutschland GmbH Telekom (former T-mobile) Deutschland GERMANY Vodafone D2 Vodafone GREECE Vodafone Greece (Panafon) Vodafone GREECE Wind Hellas Wind Telecommunications HUNGARY Pannon GSM Távközlési Pannon HUNGARY Vodafone Hungary Ltd. -

MPSC Case No. U-13746 FRANCE TELECOM CORPORATE

MPSC Case No. U-13746 FRANCE TELECOM CORPORATE SOLUTIONS L.L.C. DIRECT TESTIMONY OF JEAN-SEBASTIEN FALISSE EXHIBIT 3 (A-) FINANCIAL STATEMENTS OF FRANCE ThLlkOM S.A. AND BANK STATEMENT OF FRANCE TELECOM CORPORATE SOLUTIONS L.L.C. France Telecom Corporate Solutions L.L.C. Demonstration of Financial Capability As a newly-formed company, Applicant does not have any audited financial statements. Applicant is majority owned and controlled by France T&corn S.A. (“France Telecom”), one of the largest communications companies in the world. Applicant’s financial information will be fully consolidated in the financial statements of its parent company.’ A copy of France Telecom’s consolidated audited financial statements for the last three years is attached. France Telecom is a leading integrated communications company which is publicly- traded on both the Paris Stock Exchange and the New York Stock Exchange. As indicated in its audited 2001 financial statements, France Telecom’s consolidated revenue for the year was S43.026 billon, EBITDA was E12.32 billion, and operating income was S5.2 billion.2 The attached financial documents demonstrate that France Telecom Corporate Solutions L.L.C. clearly possesses the requisite tinancial capability to provide intrastate telecommunications services in this State. ’ See Consolidated Financial Statements - France Telecom, 2001, 2000 and 1999 at p. 7 (“companies which are wholly owned or which France Telecom controls, either directly or indirectly, are fully consolidated”). 2 Id. at p. 3. As of September 12, 2002, the exchange rate between the euro and the U.S. dollar was approximately cl to US$O.98. -

APSCC Monthly E-Newsletter

APSCC Monthly e‐Newsletter October 2020 The Asia‐Pacific Satellite Communications Council (APSCC) e‐Newsletter is produced on a monthly basis as part of APSCC’s information services for members and professionals in the satellite industry. Subscribe to the APSCC monthly newsletter and be updated with the latest satellite industry news as well as APSCC activities! To renew your subscription, please visit www.apscc.or.kr. To unsubscribe, send an email to [email protected] with a title “Unsubscribe.” News in this issue has been collected from September 1 to Septmebr 30. INSIDE APSCC APSCC 2020 Conference Series Season 2 Starts from October 7: LIVE Every Wednesday 9AM HK l Singapore Time from October 7 to November 25 APSCC 2020 is the largest annual event of the Asia Pacific satellite community, which incorporates industry veterans, local players as well as new players into a single platform in order to reach out to a wide-ranging audience. Organized by the Asia Pacific Satellite Communications Council (APSCC), APSCC 2020 this year is even stretching further by going virtual and live. Every Wednesday mornings at 9 AM Hong Kong and Singapore time, new installments in APSCC 2020 will be presented live - in keynote speeches, panel discussions, and in presentations followed by Q&A format. Topics will range across a selection of issues the industry is currently grappling with globally, as well as in the Asia-Pacific region. Register now and get access to the complete APSCC 2020 Series with a single password. To register go to https://apsccsat.com. SATELLITE BUSINESS Nelco and Telesat Partner to Bring Advanced LEO Satellite Network to India September 30, 2020 - Nelco has entered into a cooperation agreement with Telesat, a leading global satellite operator that has been addressing complex connectivity challenges for over 50 years. -

Telenet Interkabel Presentatie

Keynote Presentation Duco Sickinghe, CEO At the heart of your digital lifestyle. Investor & Analyst Conference 2008 Mechelen, Belgium May 13, 2008 1 Agenda – Keynote MORNING SESSION 1. Our Company 2. Broadband internet 3. Telephony 4. Digital TV 5. Packs – bringing it all together 6. Telenet Solutions 7. Marketing, sales & care AFTERNOON SESSION 8. Our vision on mobile 9. Operational long-term projections & Strategy 2 Part 1 Our company 3 A fast evolving company We started with broadband and telephony HDTV & Hosting Telenet Mobile Launch iDTV PayTV Analogue TV BB Internet Telephony 1996 Aug 1997 Aug 2002 Dec 2003 Sep 2005 Aug 2006 Dec 2007 4 Our footprint + 1/3rd of Brussels Telenet Network Partner Network ▪ Our footprint equals Flanders region ▪ One language = characteristics of national market ▪ 2.8 million homes passed for broadband, telephony and mobile (= 55% of Belgium) ▪ 1.9 million homes passed for analog and digital television (= 38% of Belgium) 5 Our shareholders ▪ Listed on Euronext Brussels (TNET) ▪ Average daily volume: 273,608 ▪ Market cap: 1.7bn EUR 6 Strong brand image High-visibility campaigns Brand presence 7 Leading individual products Internet Telephony Television Broadband Fixed & Mobile Analog & Digital Transparent and competitive Superior and innovative Strong market position flat fee rate plans product with unique set of Speed leadership versus DSL Combined portfolio of fixed features, content and image and mobile quality 8 Care about our customers 100+ managers receive their annual incentive based on: 40% customer -

European Telecoms the Digital Telco

European Telecoms The Digital Telco - a Big Data ‘re-rater’? Industry Overview Equity | 04 September 2017 New opportunities for Telco in a Digital World Europe Telecommunications So far Telco has been the facilitator of the digital revolution. But telco too must adapt as customer demands change, digital applications proliferate and new disruptive technologies and companies threaten traditional profits. However telco is well positioned to do so, in our view, thanks to its Big Data commodity. New processes, tools and techniques could see telco exploit Big Data to defend and upsell existing revenue streams, driving cost and capex efficiencies. Analysis suggests up to 30% value upside to Euro telco as a potential mid-term re-rating catalyst. Big Data questionnaire indicates Euro Telco progress We asked questions of 13 Euro Telcos on the subject of Big Data. Responses indicate to David Wright >> Research Analyst us that progress could already be significant; the majority of telcos who answered our MLI (UK) +44 20 7995 6355 questions shifted over the past 12m from inconclusive projects to NPV +ve results. Most [email protected] focus at this stage is on Customer Care and Sales & Marketing. However there is still a Haim Israel >> long way to go with most projects still regional and not yet coordinated at Group level. Research Analyst Merrill Lynch (Israel) [email protected] Boosting revenues through data growth and new avenues Frederic Boulan, CFA >> Digitalisation fuelled by Big Data analytics provides telco with a means to better offset Research Analyst MLI (UK) legacy revenue decline and upsell existing customer relationships, while exploring new [email protected] growth opportunities. -

Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017

Report of Activities Pursuant to Act 44 of 2010 Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017 Appendix D: Securities Held by Funds The Four Funds hold thousands of publicly and privately traded securities. Act 44 directs the Four Funds to publish “a list of all publicly traded securities held by the public fund.” For consistency in presenting the data, a list of all holdings of the Four Funds is obtained from Pennsylvania Treasury Department. The list includes privately held securities. Some privately held securities lacked certain data fields to facilitate removal from the list. To avoid incomplete removal of privately held securities or erroneous removal of publicly traded securities from the list, the Four Funds have chosen to report all publicly and privately traded securities. The list below presents the securities held by the Four Funds as of June 30, 2017. 1345 AVENUE OF THE A 1 A3 144A AAREAL BANK AG ABRY MEZZANINE PARTNERS LP 1721 N FRONT STREET HOLDINGS AARON'S INC ABRY PARTNERS V LP 1-800-FLOWERS.COM INC AASET 2017-1 TRUST 1A C 144A ABRY PARTNERS VI L P 198 INVERNESS DRIVE WEST ABACUS PROPERTY GROUP ABRY PARTNERS VII L P 1MDB GLOBAL INVESTMENTS L ABAXIS INC ABRY PARTNERS VIII LP REGS ABB CONCISE 6/16 TL ABRY SENIOR EQUITY II LP 1ST SOURCE CORP ABB LTD ABS CAPITAL PARTNERS II LP 200 INVERNESS DRIVE WEST ABBOTT LABORATORIES ABS CAPITAL PARTNERS IV LP 21ST CENTURY FOX AMERICA INC ABBOTT LABORATORIES ABS CAPITAL PARTNERS V LP 21ST CENTURY ONCOLOGY 4/15