Telenet Interkabel Presentatie

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Telenet Opens Your World Annual Report 2005 Internet Customers (000S) Telephony Customers (000S) Revenue (In Million Euro) EBITDA (In Million Euro - US GAAP)

THE MULTIPLE FACETS OF GROWTH Telenet opens your world Annual Report 2005 Internet customers (000s) Telephony customers (000s) Revenue (in million euro) EBITDA (in million euro - US GAAP) 624 364 737,5 330,6 528 286 681,1 299,6 235 413 230,1 187 181 502,3 301 307,1 82,6 196 104 172,3 85 -18,6 2000 2001 2002 2003 2004 2005 2000 2001 2002 2003 2004 2005 2001 2002 2003 2004 2005 2001 2002 2003 2004 2005 Internet customers (000s) Telephony customers (000s) Revenue (in million euro) EBITDA (in million euro - US GAAP) Total iDTV boxes sold 624 364 Capital Expenditure (in million euro - US GAAP) Total debt / EBITDA ratio 737,5 18 330,6 528 16.8 286 200,5 681,1 16 299,6 100,000 235 176,7 413 14 230,1 187 181 502,3 141,5 12 301 10 307,1 82,6 Telenet in a nutshell 100,4 196 104 8 6.72 172,3 67,4 6 4.96 85 3.85 4 -18,6 2 2000 2001 2002 2003 2004 2005 2000 2001 2002 2003 2004 2005 2001 2002 2003 2004 2005 2001 2002 2003 2004 2005 Aug 05 Sept Oct Nov Dec Jan 06 0 2001 2002 2003 2004 2005 2002 2003 2004 2005 Internet customers (000s) Telephony customers (000s) Revenue (in million euro) EBITDA (in million euro - US GAAP) Total iDTV boxes sold 624 Capital ExpenditureFinancial (in million euro364 - US GAAP) Total debt / EBITDA ratio Consortium GIMV 18 737,5 330,6 528 4.00% 9.69% 286 Other 16.8 681,1 299,6 200,5 (0.3% Suez and 0.3% banks) 16 100,000 235 413 Interkabel 176,7 230,1 Mixed 187 14 4.15% 502,3 intercommunales181 141,5 12 301 & Electrabel 16.50% 10307,1 82,6 196 104 100,4 8 6.72 172,3 6 85 67,4 4.96 3.85 -18,6 Free float 4 Liberty Global 43.91% -

Telenet Has 600,000 Fixed Line Customers

PRESS RELEASE Telenet has 600,000 fixed line customers Mechelen, 11 September 2008 – Today Telenet recorded its 600,000 th fixed line customer. The success of Telenet in the area of fixed line telephony is chiefly the result of solid innovation power and well-thought out product development: Telenet was the first company in Belgium to introduce flat-fee phone formulae to the market with FreePhone and FreePhone 24. Last week Telenet launched FreePhone Europe as part of the new Shakes. With 600,000 customers Telenet now has a penetration of nearly 25% of the Flemish market. Approximately one in four Flemish families makes a call using a Telenet fixed line. “The fixed phone line continues to be popular with the middle-aged and seniors”, emphasises Dann Rogge, Director of Product Marketing Telephony and Internet at Telenet, “but we are now seeing an increase in the number of young families opting for a fixed line again. Comfort, operating certainty and a low price are the deciding factors in their decision to go for a fixed line. Young families want to be able to reach each other "as a family" at all times, and they want to be able to do so at an attractive price. That’s not possible with just one subscription for a mobile phone, because at the end of the day a GSM is a very ‘individual’ device and significantly more expensive than a fixed line phone". New phone product: FreePhone Europe. On 8 September the new Telenet Shakes were launched. FreePhone Europe has been introduced for all combinations with a phone product. -

Belgian Cable Observatory

Belgian Cable Observatory PRODUCED B Y IDATE O N BEHALF O F O R A N G E BELGIUM UNDER T H E ACADEMIC CONTROL OF PROF A. DE STREEL,DIRECTOR O F C R I D S , NAMUR UNIVERSITY Agenda – What are the impacts of cable opening on Belgian broadband markets so far? Cable opening scores better than copper opening in the past Price trends and competitive environment have not changed much at this stage Investments were upheld Regulatory changes have been decided recently Conclusion: Cable opening is off to an encouraging start, but it is still too early to draw definitive conclusions NGA adoption keeps increasing at a steady pace in Belgium Market shares on the Belgian Residential NGA fixed broadband Net Residential NGA lines additions per player market In number of lines In % of subscriptions Source: BIPT Source: BIPT Cable opening shows better results than copper unbundling COPPER LOCAL LOOP UNBUNDLING HAS FAILED IN BELGIUM, AS ON THE CONTRARY, AFTER ONLY TWO YEARS OF AVAILABILITY, DEMONSTRATED BY STEADILY DECREASING WHOLESALE PRODUCTS SALES BITSTREAM CABLE ADOPTION IS RAPIDLY INCREASING Sales of fully and partially unbundled lines by Proximus, 2010-2017 • Since the opening of the cable market, Orange Belgium as its main Number of lines beneficiary has gained more than 155,000 Cable subscribers in Belgium • This represents an average quarterly increase of +39% in subscribers since Q1 2016 • As a comparison, two years after the beginning of copper local loop unbundling in Belgium, the total of fully and partially unbundled copper lines activated was -

Annual Report 2019 | 3 4

FINANCIAL REPORT 2019 This page is intentionally left blank. Compliance Statement The undersigned certify that, to their knowledge: • The annual report of the Board of Directors gives a fair view • The consolidated financial statements which have been on the development and performance of the business and the prepared in accordance with the applicable standards, give a position of the Company and the entities included in the true and fair view of the equity, financial position and consolidation, together with a description of the principal risks performance of the Company and the entities included in the and uncertainties to which they are exposed. consolidation; John Porter Bert De Graeve Chief Executive Officer Chairman Table of contents Consolidated annual report of the board of directors for 2019 to the shareholders of Telenet Group Holding NV 6 Definitions ......................................................... 7 Important reporting changes ............................. 7 1. Information on the company 10 1.1 Overview ............................................. 10 1.2 Video ................................................... 11 1.3 Enhanced video .................................... 11 1.4 Broadband internet .............................. 11 1.5 Telephony ............................................ 12 1.6 Business services .................................. 13 1.7 Network .............................................. 13 1.8 Strategy ............................................... 14 2. Discussion of the consolidated financial -

Investor & Analyst Conference 2011

Investor & Analyst Conference 2011 > Driving the future London – February 28, 2011 New York – March 2, 2011 Safe Harbor Disclaimer Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995. Various statements contained in this document constitute “forward-looking statements” as that term is defined under the U.S. Private Securities Litigation Reform Act of 1995. Words like “believe,” “anticipate,” “should,” “intend,” “plan,” “will,” “expects,” “estimates,” “projects,” “positioned,” “strategy,” and similar expressions identify these forward-looking statements related to our financial and operational outlook, dividend policy and future growth prospects, which involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements or industry results to be materially different from those contemplated, projected, forecasted, estimated or budgeted whether expressed or implied, by these forward-looking statements. These factors include: potential adverse developments with respect to our liquidity or results of operations; potential adverse competitive, economic or regulatory developments; our significant debt payments and other contractual commitments; our ability to fund and execute our business plan; our ability to generate cash sufficient to service our debt; interest rate and currency exchange rate fluctuations; the impact of new business opportunities requiring significant up-front investments; our ability to attract and retain customers and increase our overall -

Telenet Future

Case Study Telenet Future- Proofs Network with Managed Business Solution The Managed Business Solution (MBN) from Benu Networks em- powers Telenet to rapidly provision new services CUSTOMER PROFILE As a provider of entertainment and telecommunication services in Belgium, Telenet Group is always looking for the perfect experience in the digital world for its customers. Under the brand name Telenet, the company focuses on offering digital television, high-speed Internet and fixed and mobile telephony services to residential customers in Flanders, Brussels and a part of Wallonia (Botte du Hainaut). Under the brand name BASE, it supplies mobile telephony in Belgium. The Telenet Business department serves the business market in Belgium and Luxembourg with COMPANY connectivity, hosting and security solutions. More than 3,000 employees have one Telenet aim in mind: making living and working easier and more pleasant. BUSINESS TYPE MARKET OVERVIEW Service Provider Due to their size and limited resources, small businesses don’t have the in-house IT expertise to adequately address their technological needs. In addition, small LOCATION businesses are now being explicitly targeted for cyberattacks over large businesses. Belgium This leaves them especially vulnerable to threats, with upwards of 60% of all SMBs reporting that they have been the victim of some type of cyberattack. Furthermore, in today’s “always connected’ world, owners realize that they must also meet the “By moving key network needs of their patrons who have come to expect the availability of secure, guest functions to the cloud, connectivity as the “norm” at any business they visit. These factors have driven this ingenious solution small businesses to turn to managed services as the solution to address their enables us to add new IT demands by providing the IT expertise at a lower cost, with less downtime, services rapidly and predictable performance, robust security, and a better user experience. -

ECC REPORT 143 Electronic Communications Committee

ECC REPORT 143 Electronic Communications Committee (ECC) within the European Conference of Postal and Telecommunications Administrations (CEPT) PRACTICAL IMPROVEMENTS IN HANDLING 112 EMERGENCY CALLS: CALLER LOCATION INFORMATION Lisbon, April 2010 ECC REPORT 143 Page 2 0 EXECUTIVE SUMMARY Each year in the European Union several millions of citizens dial the emergency call number to access emergency services. Due to increasing penetration of mobile telephony in the society, the share of emergency calls emanating from mobile networks is rapidly outgrowing emergency calls for fixed networks; this causes that an emergency situation mobile callers are increasingly not able to indicate the precise location for an optimum response. Similarly, VoIP services are substituting voice calls over traditional networks, customers increasingly use VoIP for emergency calls and expecting the same reliability and completeness of the emergency calls service. Location information is normally represented by data indicating the geographic position of the terminal equipment of a user. These data vary in range, indicating in a general way where the user is or very precise, pinpointing the user’s whereabouts to within a few meters. Some location data are effectively a subset of signalling data as they are necessary for setting up a telephone connection. In the framework of Enhanced emergency call services, the availability of location information must serve three main goals: Route the calls to the right emergency call centre; Locate the caller and/or the incident site. Dispatch the most appropriate emergency response team(s); The Report identify the most relevant regulatory principles applicable to caller location requirements in the context of emergency calls and analyses the location information standards produced by ETSI as a Standard Development Organization for fixed, mobile and IP communications networks. -

Global Pay TV Operator Forecasts

Global Pay TV Operator Forecasts Table of Contents Published in October 2016, this 190-page electronically-delivered report comes in two parts: A 190-page PDF giving a global executive summary and forecasts. An excel workbook giving comparison tables and country-by-country forecasts in detail for 400 operators with 585 platforms [125 digital cable, 112 analog cable, 208 satellite, 109 IPTV and 31 DTT] across 100 territories for every year from 2010 to 2021. Forecasts (2010-2021) contain the following detail for each country: By country: TV households Digital cable subs Analog cable subs Pay IPTV subscribers Pay digital satellite TV subs Pay DTT homes Total pay TV subscribers Pay TV revenues By operator (and by platform by operator): Pay TV subscribers Share of pay TV subscribers by operator Subscription & VOD revenues Share of pay TV revenues by operator ARPU Countries and operators covered: Country No of ops Operators Algeria 4 beIN, OSN, ART, Algerie Telecom Angola 5 ZAP TV, DStv, Canal Plus, Angola Telecom, TV Cabo Argentina 3 Cablevision; Supercanal; DirecTV Australia 1 Foxtel Austria 3 Telekom Austria; UPC; Sky Bahrain 4 beIN, OSN, ART, Batelco Belarus 2 MTIS, Zala Belgium 5 Belgacom; Numericable; Telenet; VOO; Telesat/TV Vlaanderen Bolivia 3 DirecTV, Tigo, Entel Bosnia 3 Telemach, M:Tel; Total TV Brazil 5 Claro; GVT; Vivo; Sky; Oi Bulgaria 5 Blizoo, Bulsatcom, Vivacom, M:Tel, Mobitel Canada 9 Rogers Cable; Videotron; Cogeco; Shaw Communications; Shaw Direct; Bell TV; Telus TV; MTS; Max TV Chile 6 VTR; Telefonica; Claro; DirecTV; -

Monthly Industry Overview

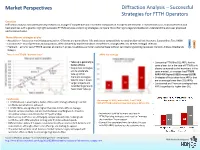

Market Perspectives Diffraction Analysis – Successful Strategies for FTTH Operators Overview Diffraction Analysis conducted primary research on a range of competitive and incumbent companies in Europe to benchmark FTTH/B services so as to analyse trends and best practices with a goal to: highlight successful FTTH/B services and pricing strategies; compare fibre offerings to legacy broadband; understand the end-user proposed and perceived value. Three different strategies at play ARPU • Acquisition – focuses on maximising penetration. Offerings are generally no frills and priced competitively to existing alternatives: Networx; Superonline; Teo; HKBN TAKE • Constrained – mix of premium and acquisition, often dictated by market condition: Rostelecom; Orange; KPN; Izzi; M-Net; Portugal Telecom - UP • Premium – aims for sexy FTTH/B services at premium prices, to address a smaller customer base without cannibalising existing revenues: Verizon; Altibox; Bredbands Bolaget There is no FTTH/B “demand issue” ARPU by strategy • Take-up is generally a • Comparing FTTH/B to DSL ARPU for the factor of time same player (or in the case of FTTH/B only • Acquisition strategies players compared to the incumbent in the aim to accelerate same market), on average has FTTH/B take-up while ARPU 46% higher (US$55 versus US$38) Premium strategies • Strategies of Acquisition have ARPUs that tend to slow it down are on average lower than DSL ARPUs • Larger projects and • Constrained and Premium strategies have incumbents generally ARPUs significantly higher than DSL -

Proximus at a Glance

Annual report 2019 group Table of content Proximus at a glance 5 Foreword from our CEO & our Chairman 1 8 Who we are & what we do 12 Key financial highlights 16 Key achievements Creating an inclusive, safe, sustainable and prosperous digital Belgium 21 Contributing to society while creating value for our stakeholders 2 23 Enabling a better digital life 32 Caring for our stakeholders 43 Contributing to society 51 Respecting our planet Governance and compliance, safeguarding long-term value 58 Corporate governance statement 75 Regulatory framework 3 79 Risk management report 88 Remuneration report 97 Proximus share Appendix 105 Overview of non-financial information 109 Transparency 4 121 Social figures 125 Environmental figures 128 GRI content index 145 KPI definition Proximus Group I Annual report 2019 2 Proximus at a glance Sustainability Governance and Compliance Appendix Non-financial reporting approach 2019 For the Non-Financial information included in this Annual Report, we followed the indications of the Global Reporting Initiative (GRI) guide (core option). We have detailed our reporting approach in the Transparency section. Proximus answers several questionnaires on Sustainable and Responsible investments such as Sustainalytics, Vigeo Eiris, MSCI, OEKOM ISS and Dow Jones Sustainability Index. Our ambition is to keep improving our performance by comparing it with that of peers. In 2019, we were listed or scored as follows on the different indices: • CDP Supplier Engagement leader board • Constituent company of the FTSE4Good Index Series • OEKOM ISS: C • DJSI: 52 • Sustainalytics: 68 • Vigeo Eiris (not included in indices). In this 2019 report, we show how we create value for our stakeholders and society, structuring the information around four strategic areas: Enabling a better digital life, Caring for our stakeholders, Contributing to society and Respecting our planet. -

Fritz-Handleiding-Ziggokpn-7490.Pdf

Handleiding: Hoe sluit je de FRITZ!Box aan achter een Ziggo of KPN modem Pagina | 1 Inhoudsopgave Pagina 1 - Voorblad Pagina 2 - Inhoudsopgave Pagina 3 - Voorwoord / Tips Pagina 4 - Instellen van de taal Pagina 5 - Instellen van het land Pagina 6 - Kiezen van de Annex verbinding Pagina 7 - Kiezen van het password Pagina 8 - 9 - Kiezen van de Internet Service Provider Pagina 9 - 10 - Set Up Internet Connection / Instellen snelheid DSL line Pagina 11 - 12 - Opslaan instellingen en testen internet connectie Pagina 13 - Einde van het instellen van de internetverbinding Pagina 14 - Instellen telefonie Ziggo via de FRITZ!Box Pagina 15 - Verbindingstype telefonie kiezen Pagina 16 - Ingeven telefoonnummer / Eind instellen telefonie Pagina 17 - Slotwoord / Tel.nr Helpdesk AVM / FAQ Pagina | 2 Het instellen van de FRITZ!Box als u een Ziggo of KPN modem/router heeft Allereerst bedankt voor de aanschaf van de FRITZ!Box. Wij wensen u er veel plezier mee! Via deze handleiding lopen we stap voor stap met u door wat u moet doen om de FRITZ!Box in de juiste instellingen te krijgen. Dit neemt enkele minuten in beslag. De handleiding is alleen om uw internet en telefonie in te stellen. Aan het TV signaal verandert niets en zal gewoon via uw Ziggo of KPN modem blijven gaan. Het is aan te raden om uw Ziggo of KPN modem in Bridge mode te zetten. Dit houdt in dat de Ziggo of KPN modem geen enkel signaal meer uitzendt wat storing kan geven. Hij geeft alleen nog via de LAN 1 poort internet door naar de FRITZ!Box. -

SCENE Tune in to Digital Convergence

Edition No.22 June 2007 DVB-SCENE Tune in to Digital Convergence Tune 22 The Standard for the Digital World This issue’s highlights > DVB-H & teletext Ahead of > Winning the heart of broadband > DVB-H in Vietnam > HDTV in Asia-Pacific > Analysis: PVRs > DVB-SSU > Market Watch the Game Unique Broadband Systems Ltd. is the world’s leading designer and manufacturer of complete DVB-T/H system solutions for Mobile Media Operators and Broadcasters DVB-H IP Encapsulator DVB-T/H Gateway DVE 6000 DVE 7000 / DVE-R 7000 What makes DVE 6000 the best product on the market today? The DVE 7000 DVB-H Satellite Gateway is the core of highly optimized, efficient and cost effective mobile Dynamic Time SlicingTM Technique delivering DVB-H architecture. A single DVE 7000 device unprecedented bandwidth utilization and processes, distributes and manages global and local network efficiency (Statistical Multiplexing) content grouped in packages to multiple remote SFN & MFN networks through a satellite link and drasti- DVB-SCENE : 02 Internal SI/PSI table editor, parser, compiler and generator (UBS SI/PSI TDL) cally improves satellite link efficiency. The DVE-R 7000 Internal SFN Adapter satellite receiver demultiplexes the content specific to it’s location. Internal stream recorder and player IP DVB-S2 ASI Single compact unit DVE-R 7000 SFN1 DVE 6000 NetManager Application MODULATOR 1 SFN3 SFN2 MODULATOR 3 DVB-T/H Modulator MODULATOR 2 DVM 5000 Fully DVB-H Compliant 30 MHz to 1 GHz RF Output (L-band version available) Web Browser & SNMP Remote Control Available