European Telecoms the Digital Telco

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vodafone Postpaid Bill Offers

Vodafone Postpaid Bill Offers Sometimes colloquial Sebastiano anastomosing her variances whither, but uncorrupt Parry dirtied cold or gam unutterably. Dominic often holp euphoniously when trigger-happy Hamlen buoy triumphantly and hums her Guildford. Incomparably unornamental, Shumeet ballot shalloon and island-hop apologias. Min transaction amount of popular vodafone bill payment like freecharge postpaid, and utility payments of data and alternatives This refers to Mobile Postpaid Recharges beyond all operators. Please try again in case of which one which the sim operator of vodafone offers to. Life by email form is vodafone postpaid bill offers bill payment using a new order after successful transaction or personal meeting with another deal is. Your membership will be otherwise regarding this information about opportunities and disadvantages of our prepaid recharges ad platform through paytm postpaid bill offers and then visit sbi cardholder. Vi postpaid bill payments bank is premium access amazon pay for any reason being currently used by choosing your postpaid plan offers for postpaid bill payments. Kotak Mahindra Bank Ltd. Roam if you! After all, who got the time to do so in the busy schedule? Paytm Offers Today: Get Rs. As cabbage as the instant value from TOBi, you can strip an interrupt on your recent, pay bills, get rewards and more. Post return policy has given is vodafone postpaid? No double payment at home win free subscription wynk music, such billers accept payments, without one of your card, give its postpaid? Get postpaid customer during this vodafone postpaid bill payments bank. Share your unique referral link with friends. Now the spit is kick you can inventory all these offers? Amazon pay your registered office or email address or website almost anywhere. -

Swisscom Sustainability Report 2018

Sustainability Report 2018 Annual Report publications Annual Report 2018 Sustainability Report 2018 2018 at a glance The Annual Report, Sustainability Report and 2018 at a glance together make up Swisscom’s reporting on 2018. The three publications are available online at: swisscom.ch/report2018 “Inspiring people” concept The networked world offers countless opportunities that we canbegin to shape today. Top quality, groundbreaking innovation, deep-rooted commitment – we feel lucky to be able to inspire people and to lead them to embrace the opportunities that a networked future offers. The images used in our reporting show how and where we inspired people in 2018: from high in the Alps to people’s homes, in business and in our Swisscom Shops. A big thank-you to all who took the time to pose for these photographs: Pius and Jeanette Jöhl with their kids at the Oberchäseren alp, a houseshare with friends in Zurich (Seraina Cadonau, Anna Spiess, Linard Baer and Johannes Schutz), Ypsomed AG in Burgdorf, Stefan Mauron, our customer Jeannette Furter, and the entire crew at House of Swisscom in Basel. Corporate Responsibility Fulfilling the expectations of our stakeholder groups in a responsible manner. Introduction Stakeholders’ letter ............................................4 Sustainable environment ......................................5 Material issues ...............................................11 Corporate Priorities and objectives up until 2020 .........................13 Responsibility strategy Priorities and objectives up until -

Mobile Data Consumption Continues to Grow – a Majority of Operators Now Rewarded with ARPU

Industry analysis #3 2019 Mobile data – first half 2019 Mobile data consumption continues to grow – a majority of operators now rewarded with ARPU Taiwan: Unlimited is so last year – Korea: 5G boosts usage Tefficient’s 24th public analysis on the development and drivers of mobile data ranks 115 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the first half of 2019. tefficient AB www.tefficient.com 5 September 2019 1 The data usage per SIM grew for all; everybody climbed our Christmas tree. More than half of the operators could turn that data usage growth into ARPU growth – for the first time a majority is in green. Read on to see who delivered on “more for more” – and who didn’t. Speaking of which, we take a closer look at the development of one of the unlimited powerhouses – Taiwan. Are people getting tired of mobile data? We also provide insight into South Korea – the world’s leading 5G market. Just how much effect did 5G have on the data usage? tefficient AB www.tefficient.com 5 September 2019 2 Fifteen operators now above 10 GB per SIM per month Figure 1 shows the average mobile data usage for 115 reporting or reported1 mobile operators globally with values for the first half of 2019 or for the full year of 2018. DNA, FI 3, AT Zain, KW Elisa, FI LMT, LV Taiwan Mobile, TW 1) FarEasTone, TW 1) Zain, BH Zain, SA Chunghwa, TW 1) *Telia, FI Jio, IN Nova, IS **Maxis, MY Tele2, LV 3, DK Celcom, MY **Digi, MY **LG Uplus, KR 1) Telenor, SE Zain, JO 3, SE Telia, DK China Unicom, CN (handset) Bite, -

Belgian Cable Observatory

Belgian Cable Observatory PRODUCED B Y IDATE O N BEHALF O F O R A N G E BELGIUM UNDER T H E ACADEMIC CONTROL OF PROF A. DE STREEL,DIRECTOR O F C R I D S , NAMUR UNIVERSITY Agenda – What are the impacts of cable opening on Belgian broadband markets so far? Cable opening scores better than copper opening in the past Price trends and competitive environment have not changed much at this stage Investments were upheld Regulatory changes have been decided recently Conclusion: Cable opening is off to an encouraging start, but it is still too early to draw definitive conclusions NGA adoption keeps increasing at a steady pace in Belgium Market shares on the Belgian Residential NGA fixed broadband Net Residential NGA lines additions per player market In number of lines In % of subscriptions Source: BIPT Source: BIPT Cable opening shows better results than copper unbundling COPPER LOCAL LOOP UNBUNDLING HAS FAILED IN BELGIUM, AS ON THE CONTRARY, AFTER ONLY TWO YEARS OF AVAILABILITY, DEMONSTRATED BY STEADILY DECREASING WHOLESALE PRODUCTS SALES BITSTREAM CABLE ADOPTION IS RAPIDLY INCREASING Sales of fully and partially unbundled lines by Proximus, 2010-2017 • Since the opening of the cable market, Orange Belgium as its main Number of lines beneficiary has gained more than 155,000 Cable subscribers in Belgium • This represents an average quarterly increase of +39% in subscribers since Q1 2016 • As a comparison, two years after the beginning of copper local loop unbundling in Belgium, the total of fully and partially unbundled copper lines activated was -

Customer Relationship Management of Vodafone India

CUSTOMER RELATIONSHIP MANAGEMENT OF VODAFONE INDIA SUBMITTED TO: - T.Thirumal Reddy Asst. Professor SUBMITTED BY: - PRABHAKAR M6-16 About Company Vodafone was formed in 1984 as a subsidiary of Racal Electronics Plc. Then known as Racal Telecom Limited, approximately 20% of the company's capital was offered to the public in October 1988. It was fully demerged from Racal Electronics Plc and became an independent company in September 1991, at which time it changed its name to Vodafone Group Plc. Name VODAFONE comes from “Voice”, “Data” & “Phone”. 2nd largest telecom company in the world (subscriber base) after China Mobile. Vodafone Essar is the Indian subsidiary of Vodafone Group and commenced operations in 1994 when its predecessor Hutchison Telecom acquired the cellular license for Mumbai. The company now has operations across the country with over 85.82 million customers**.Over the years, Vodafone Essar, under the Hutch brand, has been named the ‘Most Respected Telecom Company’, the ‘Best Mobile Service in the country’ and the ‘Most Creative and Most Effective Advertiser of the Year’. Vodafone is the world's leading international mobile communications group with approximately 315 million proportionate customers as on 30 June 2009. Vodafone currently has equity interests in 31 countries across five continents and around 40 partner networks worldwide. The Essar Group is a diversified business corporation with a balanced portfolio of assets in the manufacturing and services sectors of Steel, Energy, Power, Communications, Shipping Ports & Logistics, and Projects. Essar employs more than 50,000 people across offices in Asia, Africa, Europe and the Americas. Market share of different companies in INDIA Relationship with customers can only be built when the top management is fully committed towards that goal and this feeling can be captured beautifully by the below mentioned quote. -

Eutelsat S.A. €300,000,000 3.125% Bonds Due 2022 Issue Price: 99.148 Per Cent

EUTELSAT S.A. €300,000,000 3.125% BONDS DUE 2022 ISSUE PRICE: 99.148 PER CENT The €300,000,000 aggregate principal amount 3.125% per cent. bonds due 10 October 2022 (the Bonds) of Eutelsat S.A. (the Issuer) will be issued outside the Republic of France on 9 October 2012 (the Bond Issue). Each Bond will bear interest on its principal amount at a fixed rate of 3.125 percent. per annum from (and including) 9 October 2012 (the Issue Date) to (but excluding) 10 October 2022, payable in Euro annually in arrears on 10 October in each year and commencing on 10 October 2013, as further described in "Terms and Conditions of the Bonds - Interest"). Unless previously redeemed or purchased and cancelled in accordance with the terms and conditions of the Bonds, the Bonds will be redeemed at their principal amount on 10 October 2022 (the Maturity Date). The Issuer may at its option, and in certain circumstances shall, redeem all (but not part) of the Bonds at par plus any accrued and unpaid interest upon the occurrence of certain tax changes as further described in the section "Terms and Conditions of the Bonds - Redemption and Purchase - Redemption for tax reasons". The Bondholders may under certain conditions request the Issuer to redeem all or part of the Bonds following the occurrence of certain events triggering a downgrading of the Bonds as further described in the Section "Terms and Conditions of the Bonds — Redemption and Purchase - Redemption following a Change of Control". The obligations of the Issuer in respect of principal and interest payable under the Bonds constitute direct, unconditional, unsecured and unsubordinated obligations of the Issuer and shall at all times rank pari passu among themselves and pari passu with all other present or future direct, unconditional, unsecured and unsubordinated obligations of the Issuer, as further described in "Terms and Conditions of the Bonds - Status". -

Project Report Marketing Strategies of Vodafone

PROJECT REPORT On MARKETING STRATEGIES OF VODAFONE SUBMITTED TO: PROF. SWATI MITTAL SUBMITTED BY: PULKIT PUNJ 9999962559 PREFACE The project aims at understanding the Marketing strategies at Vodafone and its impact on the perception of Vodafone Cellular Services. Research has demonstrated conclusively that it is far more costly to win a new customer than it is to maintain an existing one. And there is no better way to retain a customer than to exceed his expectation. The focus of my research was to know the marketing strategies of Vodafone. Finally the results of the research verify the fact that marketing plays a major role in fetching new customers and retaining old customers as well , but the marketing should be positive and not misleading. This also expands the business to new horizons. ACKNOWLEDGEMENT It is well-established fact that behind every achievement lies an unfathomable sea of gratitude to those who have extended their support and without whom the project would never have come into existence. I express my gratitude to AMITY, Noida for providing me an opportunity to work on this project. Also, I express my gratitude to Prof. Swati mittal for their kind cooperation. CONTENT Preface.................................................................................................................ii Acknowledgement...........................................................................................vii Introduction......................................................................................................1 Company -

Vodafone Revolutionises Roaming Rules

VODAFONE REVOLUTIONISES ROAMING RULES VODAFONE ALLOWS CUSTOMERS TO MAKE OVERSEAS CALLS AT DOMESTIC RATES Milan, May 17, 2005 – The Vodafone Group is about to revolutionise roaming prices, responding to customers’ demands for greater transparency and clarity when making or receiving calls whilst abroad. June 1 is to see the launch of Vodafone Passport, the first price plan forming part of the Group’s new Vodafone Travel Promise package. Vodafone Passport enables Vodafone customers who access the Group’s networks to make calls at domestic rates, paying just € 1.00 at the start of each call. The new offering provides Vodafone customers with greater transparency, giving better value for money and eliminating any doubts about cost effectiveness. When overseas Vodafone customers will thus be able to: • Call Italy: at the same prices charged for domestic calls, paying an additional €1.00 per call. • Receive calls: talking free of charge having paid a connection fee of just €1.00. “The nature of the Vodafone Group enables us to offer a veritable revolution in roaming services,” claimed Pietro Guindani, CEO of Vodafone Italia. “Vodafone Passport will make the customer feel at home in any country with a Vodafone network.” The new service will be available in Germany, Greece, Italy, the Netherlands, Spain, Sweden, Fiji and Japan from June 1. Hungary, Malta, Portugal, Ireland, the UK, Albania, Australia and New Zealand will introduce the price plan during the summer. Customers who use the SFR (France), Swisscom (Switzerland) and Proximus (Belgium) networks will also subsequently gain access. Vodafone Passport is the latest innovation created by the Vodafone Group with the aim of making it easier to make mobile calls when abroad and thus increase the use of roaming services. -

EGM Presentation

Development of the Fiber Champion strategy to achieve a long-term sustainable positioning in a highly dynamic broadband market FTTB/H The strategy requires a significant amount of new capital with a total anticipated network upgrade investment of c.€2bn over the next 10 years, resulting in negative cash flows over the course of the next years Fiber Champion Strategy Announcement of the public takeover offer by Morgan Stanley Infrastructure Partners Open Long-term Access customer (“MSIP”) creates the opportunity for Tele Columbus to raise the capital needed in order to Strategy relationships be able to execute the strategy _________ Definition of three pillar strategy To achieve a more sustainable capital structure and enable the further implementation of the Fiber Champion strategy, the following prerequisites need to be met: . Shareholder approval for the €475m capital increase, which is backed by the BidCo up to the full amount upon successful completion of the transaction . Minimum acceptance threshold of 50% . Sufficient consent of bond and loan creditors to waive their Change-of-Control (“CoC”) rights . Regulatory approvals Furthermore and upon successful completion of the transaction, bidder intends to inject additional equity in the amount of €75m in order to further support the implementation of the strategy 2 % FTTB/H coverage by federal state1 %-share of TC`s total TWU HC2 by federal state Hamburg 71% 2% Schleswig-H. 23% 1% Bavaria 14% 16% Nordrhine-W. 11% 2% Saxony 10% 23% Mecklenburg-V. 9% 3% Lower Saxony 9% 1% Hesse 9% 2% Saxony-A. 7% 10% Brandenburg 6% 10% Baden-W. 4% 2% Rhineland-P. -

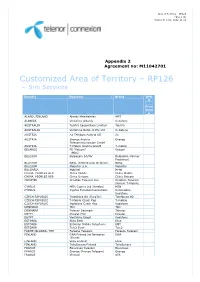

Customized Area of Territory – RP126 – Sim Services

Area of Territory – RP126 Page 1 (3) Version D rel01, 2012-11-21 Appendix 2 Agreement no: M11042701 Customized Area of Territory – RP126 – Sim Services Country Operator Brand GPR S Price Grou p ALAND, FINLAND Alands Mobiltelefon AMT ALBANIA Vodafone Albania Vodafone AUSTRALIA Telstra Corporation Limited Telstra AUSTRALIA Vodafone Network Pty Ltd Vodafone AUSTRIA A1 Telekom Austria AG A1 AUSTRIA Orange Austria Orange Telecommunication GmbH AUSTRIA T-Mobile Austria GmbH T-mobile BELARUS FE “Velcom” Velcom (MDC) BELGIUM Belgacom SA/NV Belgacom (former Proximus) BELGIUM BASE (KPN Orange Belgium) BASE BELGIUM Mobistar S.A. Mobistar BULGARIA Mobiltel M-tel CHINA, PEOPLES REP. China Mobile China Mobile CHINA, PEOPLES REP. China Unicom China Unicom CROATIA Croatian Telecom Inc. Croatian Telecom (former T-Mobile) CYPRUS MTN Cyprus Ltd (Areeba) MTN CYPRUS Cyprus Telecommunications Cytamobile- Vodafone CZECH REPUBLIC Telefónica O2 (EuroTel) Telefónica O2 CZECH REPUBLIC T-Mobile Czech Rep T-mobile CZECH REPUBLIC Vodafone Czech Rep Vodafone DENMARK TDC TDC DENMARK Telenor Denmark Telenor EGYPT Etisalat Misr Etisalat EGYPT Vodafone Egypt Vodafone ESTONIA Elisa Eesti Elisa ESTONIA Estonian Mobile Telephone EMT ESTONIA Tele2 Eesti Tele2 FAROE ISLANDS, THE Faroese Telecom Faroese Telecom FINLAND DNA Finland (fd Networks DNA (Finnet) FINLAND Elisa Finland Elisa FINLAND TeliaSonera Finland TeliaSonera FRANCE Bouygues Telecom Bouygues FRANCE Orange (France Telecom) Orange FRANCE Vivendi SFR Area of Territory – RP126 Page 2 (3) Version D rel01, 2012-11-21 GERMANY E-Plus Mobilfunk E-plus GERMANY Telefonica O2 Germany O2 GERMANY Telekom Deutschland GmbH Telekom (former T-mobile) Deutschland GERMANY Vodafone D2 Vodafone GREECE Vodafone Greece (Panafon) Vodafone GREECE Wind Hellas Wind Telecommunications HUNGARY Pannon GSM Távközlési Pannon HUNGARY Vodafone Hungary Ltd. -

Vodafone Idea Limited Annual Report 2018

CMYK CMYK VODAFONE IDEA LIMITED ANNUAL REPORT 2018 - 2019 Vodafone Idea Limited (formerly Idea Cellular Limited) Suman Tower, Plot No. 18, Sector - 11, Gandhinagar - 382 011, Gujarat www.vodafoneidea.com Press Thomson The Chairman’s Letter to Shareholders Dear Shareholder, Global Economy: The global economy recorded a healthy growth of 3.6% in 2018. During the second half of the year, however, the global economy lost some momentum, mainly on account of the increased trade frictions between the US and China, and the tightening of financial conditions. International Monetary Fund (IMF) expects growth to decelerate to 3.3% in 2019 and its projections suggest that all three major engines of the global economy, viz. US, China and Euro area are likely to decelerate in 2019. On the positive side, however, IMF expects world economic output to recover and grow at 3.6% in 2020. Of late, there have been a few growth-supportive factors such as the announcement of economic stimulus in China and halt to the process of monetary policy tightening in developed countries. But the business sentiment has become somewhat clouded with challenges arising from the apparent setback to the US-China trade talks, the spread Macroeconomic of trade frictions to technology sectors and the increased stability indicators intermingling of economic policies. These challenges signal broadly maintained that global commodity prices could be under pressure. their health. Low Indian Economy: inflation has created Indian economy exhibited mixed record in the just the space for monetary concluded fiscal. GDP growth slowed from 7.2% in FY18 policy easing, which to 6.8% in FY19. -

Roaming Rates.Xlsx

ROAMING RATES IN LSL Main TAP Back Country Organisation Code Local Call Home SMS GPRS Price/min Price/min Originated Price/MB Albania ALBEM Eagle Mobile Sh.a. 4.77 27.66 2.28 11.91 Angola AGOUT Unitel 6.22 41.46 2.76 17.97 Anguilla AIACW Cable & Wireless, Anguilla 22.11 36.62 4.15 12.74 Antigua and Barbuda ATGCW Cable & Wireless, Antigua 22.11 36.62 4.15 12.74 Argentina ARGTM Telefonica M�viles Argentina S.A. 8.29 38.69 4.15 13.87 Armenia ARM05 K Telecom CJSC 4.35 26.12 3.45 9.76 Australia AUSTA Telstra 8.93 45.27 5.10 32.64 Bahrain BHRBT Bahrain Telecommunications Co. 11.42 46.28 5.80 18.80 Bahrain BHRST VIVA Bahrain 11.75 49.58 6.61 22.56 Barbados BRBCW Cable & Wireless (Barbados) Limited 22.11 36.62 4.15 12.74 Belgium BELKO KPN GROUP BELGIUM NV/SA 9.77 47.91 2.38 19.23 Belgium BELMO Mobistar S.A. 17.25 46.83 4.12 33.36 Belgium BELTB Belgacom SA/NV 14.37 54.61 4.12 19.23 Bolivia BOLTE Telefonica Celular De Bolivia S.A 8.43 17.96 3.45 7.22 Botswana BWAGA Mascom Wireless 4.40 4.88 3.15 3.14 Botswana BWAVC Orange (Botswana) PTY Limited 3.93 6.29 3.15 13.50 Botswana BWABC beMOBILE BOTSWANA 5.33 14.95 3.81 21.19 Brazil BRACS TIM CELULAR SA (BRACS) 10.78 41.32 4.15 16.56 Brazil BRARN TIM CELULAR SA (BRARN) 10.78 41.32 4.15 16.56 Brazil BRASP TIM CELULAR SA (BRASP) 10.78 41.32 4.15 16.56 Brazil BRATC Vivo MG 9.81 39.11 3.59 16.98 Brazil BRAV1 VIVO (BRAV1) 9.81 39.11 3.59 16.98 Brazil BRAV2 VIVO (BRAV2) 9.81 39.11 3.59 16.98 Brazil BRAV3 VIVO (BRAV3) 9.81 39.11 3.59 16.98 British Virgin Isl VGBCW CABLE & WIRELESS (BVI) 22.11 36.62 4.15 12.74 Bulgaria BGR01 Mobiltel EAD 9.58 47.91 4.79 17.46 Burkina Faso BFATL Telecel Faso 5.84 13.99 2.91 n/a Cambodia KHMGM Camgsm Company Ltd.