Mobile Data Consumption Continues to Grow – a Majority of Operators Now Rewarded with ARPU

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CRM System in VODAFONE AGENDA

CRM System in VODAFONE AGENDA I. Introduction – Vodafone III. Benefits to Vodafone from CRM a. Company Profile b. Vodafone in India IV. Issues Faced in CRM Implementation c. Market Shares in India a. Program b. People II. Gartner’s Eight Building Blocks c. Processes a. CRM Vision d. Technology b. CRM Strategy c. Valued Customer Experiences V. Consumer Research d. Collaborative Efforts e. CRM Process VI. Best CRM Practices in the Industry f. CRM Information g. CRM Technology h. CRM Metrics I. INTRODUCTION COMPANY PROFILE Name VODAFONE comes from “Voice”, “Data” & “Phone” Largest telecom company in the world (turnover) 2nd largest telecom company in the world (subscriber base) after China Mobile Public limited company Operations in 31 countries & partner networks in another 40 countries Listed on NYSE Founded : 1983 as RACAL TELECOM, Demerged from Racal Electronics (parent company) in 1991 and named VODAFONE HQ : Newbury, England Revenues : US $ 69 bn (2008) Profits : US $ 6.75 bn (2008) Employees : ~ 79,000 Source : WIKINVEST Important Subsidiaries : Vodafone UK Vodafone Spain Vodafone Essar Vodafone Portugal Vodafone Australia Vodafone Turkey Vodafone Ireland Vodafone Germany Vodafone New Zealand Vodafone Netherlands Vodafone Egypt Vodafone Hungary Vodafone Italy Vodafone Sweden VODAFONE IN INDIA 2005 : Acquired a 10 % stake in Bharti Airtel 2007 : Acquired a controlling 67 % stake in Hutchinson Essar for US $ 11.1 bn. Sold back 5.6% of its Airtel stake back to the Mittals & retained 4.4% In September, Hutch was rebranded to Vodafone in India. Source : WIKINVEST MARKET SHARE IN INDIA Others 1% Reliance Airtel 19% 24% Aircel 5% Idea 11% Vodafone 18% Tata 9% BSNL / MTNL 13% Source : TRAI Report JUN’09 VODAFONE’S OFFERINGS Global Managed Enterprise Telecom Device Mobility Central1 Management2 3 4 Portfolio Services Mobile Vodafone Vodafone Vodafone Money Connect to 5 Live6 Mobile7 8 Transfer Connect Friends Vodafone Vodafone At Vodafone Vodafone9 Freedom10 11 12 Passport Home Media Packs Systems Source : vodafone.com II. -

Innovation in Loyalty and Customer Experience at Orange Belgium

CASE STUDY INNOVATION IN LOYALTY AND CUSTOMER EXPERIENCE AT ORANGE BELGIUM © 2019 Evolving Systems, Inc. Evolving Systems is a registered trademark of Evolving Systems, Inc. E: [email protected] I T: +1 303 802 1000 I F: +1 303 802 1420 Evolving Systems and Orange Belgium - for the continued management, enhancement and expansion of the customer loyalty program, Orange Thank You – has been recognized by the prestigious Total Telecoms World Communications Awards as a step forward in digital engagement. Evolving was initially selected by Orange to create a brand-new loyalty concept, provide the technical foundation, and deliver a shared new vision to enhance customer loyalty. SITUATION In 2013, Orange Belgium acknowledged a need to revitalise its approach to customer loyalty. Its existing programs weren’t delivering the desired outcomes and additionally were providing little, if any, brand differentiation. Plus, the appearance of aggressive new competitors in the market as well as regulatory changes relating to the mobile industry meant that a new approach was urgently needed to protect and improve the company’s market position. Orange’s initial objectives for its new approach included creating a single program for all markets - pre and postpaid. While addressing churn remained a primary goal, the company realised that traditional loyalty approaches had been ineffective at doing this in the past. “We knew we could make industry-standard offers like increasing megabytes” says Benoit Berthelot, Customer Engagement Manager at Orange Belgium, “but we also knew such offers were easily imitated and did little to really build strong relationships with our subscribers”. Instead, Orange wanted to “rewire” the entire customer relationship and in the process create something more emotionally engaging. -

Discussienota Over Stralingsrisico's in De Publieke Ruimte

Discussienota over stralingsrisico’s in de publieke ruimte 1 Inhoudsopgave 1. Samenvatting ........................................................................................................................... - 4 - 2. Advies voor gemeenten ........................................................................................................... - 4 - 3. Inleiding discussienota over stralingsrisico’s in de publieke ruimte ....................................... - 5 - 4. Bespreken introductie 5G in Papendrecht, oproep tot een maatschappelijke discussie ....... - 7 - 5. Wat is het kernvraagstuk? ....................................................................................................... - 8 - 6. Waarom is het belangrijk? ...................................................................................................... - 9 - 7. Waarom moet het nu besproken worden? ........................................................................... - 10 - 8. Om welke politieke keuzes vraagt het kernvraagstuk? ......................................................... - 10 - 9. Welke informatie is nodig voor beeldvorming, oordeelsvorming en besluitvorming? ........ - 10 - 10. Welke eisen willen wij aan het proces stellen? ................................................................. - 10 - 11. Welke financiële aspecten spelen een rol? ....................................................................... - 11 - 12. Big Brother is watching ..................................................................................................... -

Annual Financial Statements 2020

ANNUAL FINANCIAL STATEMENTS 2020 CI FIRST ASSET EXCHANGE-TRADED FUNDS DECEMBER 31, 2020 Table of Contents Independent Auditor’s Report .............................................................................................. 1 CI First Asset 1-5 Year Laddered Government Strip Bond Index ETF .......................................... 4 CI First Asset Active Canadian Dividend ETF............................................................................... 12 CI First Asset Active Credit ETF ................................................................................................... 22 CI First Asset Active Utility & Infrastructure ETF ....................................................................... 36 CI First Asset Canadian Buyback Index ETF ................................................................................. 46 CI First Asset Canadian Convertible Bond ETF ............................................................................ 55 CI First Asset Canadian REIT ETF ................................................................................................. 66 CI First Asset CanBanc Income Class ETF.................................................................................... 76 CI First Asset Core Canadian Equity Income Class ETF ............................................................... 84 CI First Asset Energy Giants Covered Call ETF ............................................................................ 93 CI First Asset Enhanced Government Bond ETF.......................................................................... -

Swisscom Sustainability Report 2018

Sustainability Report 2018 Annual Report publications Annual Report 2018 Sustainability Report 2018 2018 at a glance The Annual Report, Sustainability Report and 2018 at a glance together make up Swisscom’s reporting on 2018. The three publications are available online at: swisscom.ch/report2018 “Inspiring people” concept The networked world offers countless opportunities that we canbegin to shape today. Top quality, groundbreaking innovation, deep-rooted commitment – we feel lucky to be able to inspire people and to lead them to embrace the opportunities that a networked future offers. The images used in our reporting show how and where we inspired people in 2018: from high in the Alps to people’s homes, in business and in our Swisscom Shops. A big thank-you to all who took the time to pose for these photographs: Pius and Jeanette Jöhl with their kids at the Oberchäseren alp, a houseshare with friends in Zurich (Seraina Cadonau, Anna Spiess, Linard Baer and Johannes Schutz), Ypsomed AG in Burgdorf, Stefan Mauron, our customer Jeannette Furter, and the entire crew at House of Swisscom in Basel. Corporate Responsibility Fulfilling the expectations of our stakeholder groups in a responsible manner. Introduction Stakeholders’ letter ............................................4 Sustainable environment ......................................5 Material issues ...............................................11 Corporate Priorities and objectives up until 2020 .........................13 Responsibility strategy Priorities and objectives up until -

Belgian Cable Observatory

Belgian Cable Observatory PRODUCED B Y IDATE O N BEHALF O F O R A N G E BELGIUM UNDER T H E ACADEMIC CONTROL OF PROF A. DE STREEL,DIRECTOR O F C R I D S , NAMUR UNIVERSITY Agenda – What are the impacts of cable opening on Belgian broadband markets so far? Cable opening scores better than copper opening in the past Price trends and competitive environment have not changed much at this stage Investments were upheld Regulatory changes have been decided recently Conclusion: Cable opening is off to an encouraging start, but it is still too early to draw definitive conclusions NGA adoption keeps increasing at a steady pace in Belgium Market shares on the Belgian Residential NGA fixed broadband Net Residential NGA lines additions per player market In number of lines In % of subscriptions Source: BIPT Source: BIPT Cable opening shows better results than copper unbundling COPPER LOCAL LOOP UNBUNDLING HAS FAILED IN BELGIUM, AS ON THE CONTRARY, AFTER ONLY TWO YEARS OF AVAILABILITY, DEMONSTRATED BY STEADILY DECREASING WHOLESALE PRODUCTS SALES BITSTREAM CABLE ADOPTION IS RAPIDLY INCREASING Sales of fully and partially unbundled lines by Proximus, 2010-2017 • Since the opening of the cable market, Orange Belgium as its main Number of lines beneficiary has gained more than 155,000 Cable subscribers in Belgium • This represents an average quarterly increase of +39% in subscribers since Q1 2016 • As a comparison, two years after the beginning of copper local loop unbundling in Belgium, the total of fully and partially unbundled copper lines activated was -

Customer Insight Development in Vodafone Italy

Customer Insight development in Vodafone Italy Emanuele Baruffa – Vodafone Seugi - Vienna, 17-19 June 2003 Seugi 21_Vienna Pag. 1 ContentsContents:: 1. Introduction 2. Customer Base Management 3. Customer Insight 4. Data Environment 5. Conclusions Seugi 21_Vienna Pag. 2 1. Introduction 2. Customer Base Management 3. Customer Insight 4. Data Environment 5. Conclusions Seugi 21_Vienna Pag. 3 MobileMobile telephonytelephony isis oneone ofof thethe fastestfastest growinggrowing industriesindustries inin thethe worldworld Worldwide growth in subscribers (millions) ! 1 billion subscribers 1480 around the world 1321 ! Over 120 1152 countries have 958 mobile networks 727 ! Further acceleration 479 expected 206 87 14 34 Source: EITO 1991 1993 1995 1997 1999 2000 2001 2002 2003e 2004e Seugi 21_Vienna Pag. 4 Italy:Italy: Europe’sEurope’s secondsecond biggestbiggest mobilemobile marketmarket Country Subscribers Penetration Western European TLC market % growth by country (%) 10 9,1 9 Germany 60,300,000 84% 8 6,8 6,8 7 6,2 6,1 5,7 5,8 Italy 54,000,000 98% 6 5,6 5,6 5,4 5,0 5 UK 50,900,000 92% 4,0 4 France 39,000,000 77% 3 Spain 34,000,000 88% 2 1 0 Germany Italy UK France Spain Western Europe Sources: internal sources for Italy, Yankee Group for Source: EITO other European countries 2001/2002 2002/2003 Seugi 21_Vienna Pag. 5 PenetrationPenetration raterate inin thethe ItalianItalian marketmarket 60,000 96% 98% 100% 91% Subscribers (,000) 90% 50,000 Penetration Rate 80% 74% 70% 40,000 60% 53% 30,000 50% 36% 40% 20,000 30% 21% 20% 10,000 11% 10% 0 0% 1996 1997 1998 1999 2000 2001 2002 2003 Seugi 21_Vienna Pag. -

News Release

news release 31 January 2007 VODAFONE REACHES 200 MILLION CUSTOMERS Vodafone Group Plc (“Vodafone”) today announces key performance indicators for the quarter ended 31 December 2006. The main highlights are: • Organic growth of 6.1% for the quarter in proportionate mobile revenue, with proportionate growth of 0.9% in Europe and 14.4% in EMAPA. Nine months year to date organic growth in proportionate mobile revenue of 6.1% • On a statutory basis, growth in total revenue for the quarter was 5.1%, with organic service revenue growth of 4.8% • 8.7 million proportionate organic net mobile additions for the quarter. Total proportionate mobile customer base at 198.6 million at the end of the quarter after a net reduction of 1.7 million mobile customers from other movements, principally business disposals • Total proportionate mobile customer base over 200 million by the end of January • 2.5 million 3G devices added, bringing total 3G device base to 13.6 million. 3G Broadband through HSDPA available across 21 of the Group’s markets and partner networks • Completed disposal of interests in Proximus and Swisscom Mobile with net proceeds of £3.1 billion • Continued execution on revenue stimulation and total communications objectives with Vodafone At Home now launched in seven markets, including five offering DSL services, and Vodafone Office available in 11 markets • Execution of core cost reduction programmes, including IT outsourcing, data centre consolidation, supply chain management and network sharing, all on track • Vodafone re-iterates its current year outlook with the financial performance for the quarter and year to date in line with expectations Arun Sarin, Chief Executive, commented: “These KPIs are very much in line with expectations and show that we are continuing to make progress in executing our strategy. -

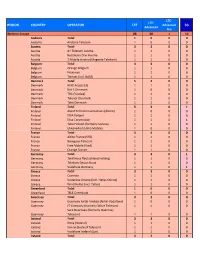

Prepared for Upload GCD Wls Networks

LTE‐ LTE‐ REGION COUNTRY OPERATOR LTE Advanced 5G Advanced Pro Western Europe 88 68 1 10 Andorra Total 10 0 0 Andorra Andorra Telecom 10 0 0 Austria Total 33 0 0 Austria A1 Telekom Austria 11 0 0 Austria Hutchison Drei Austria 11 0 0 Austria T‐Mobile Austria (Magenta Telekom) 11 0 0 Belgium Total 33 0 0 Belgium Orange Belgium 11 0 0 Belgium Proximus 11 0 0 Belgium Telenet (incl. BASE) 11 0 0 Denmark Total 54 0 0 Denmark Hi3G Access (3) 11 0 0 Denmark Net 1 Denmark 10 0 0 Denmark TDC (YouSee) 11 0 0 Denmark Telenor Denmark 11 0 0 Denmark Telia Denmark 11 0 0 Finland Total 53 0 1 Finland Aland Telecommunications (Alcom) 10 0 0 Finland DNA Finland 11 0 0 Finland Elisa Corporation 11 0 1 Finland Telia Finland (formerly Sonera) 11 0 0 Finland Ukkoverkot (Ukko Mobile) 10 0 0 France Total 44 0 0 France Altice France (SFR) 11 0 0 France Bouygues Telecom 11 0 0 France Free Mobile (Iliad) 11 0 0 France Orange France 11 0 0 Germany Total 33 0 1 Germany Telefonica Deutschland Holding 11 0 0 Germany Telekom Deutschland 11 0 0 Germany Vodafone Germany 11 0 1 Greece Total 33 0 0 Greece Cosmote 11 0 0 Greece Vodafone Greece (incl. Hellas Online) 11 0 0 Greece Wind Hellas (incl. Tellas) 11 0 0 Greenland Total 10 0 0 Greenland TELE Greenland 10 0 0 Guernsey Total 32 0 0 Guernsey Guernsey Airtel Limited (Airtel‐Vodafone) 10 0 0 Guernsey JT Guernsey (formerly Wave Telecom) 11 0 0 Sure Guernsey (formerly Guernsey Guernsey Telecom) 11 0 0 Iceland Total 33 0 0 Iceland Nova (Iceland) 11 0 0 Iceland Siminn (Iceland Telecom) 11 0 0 Iceland Vodafone Iceland (Syn) -

Zero-Rating Practices in Broadband Markets

Zero-rating practices in broadband markets Report by Competition EUROPEAN COMMISSION Directorate-General for Competition E-mail: [email protected] European Commission B-1049 Brussels [Cataloguenumber] Zero-rating practices in broadband markets Final report February 2017 Europe Direct is a service to help you find answers to your questions about the European Union. Freephone number (*): 00 800 6 7 8 9 10 11 (*) The information given is free, as are most calls (though some operators, phone boxes or hotels may charge you). LEGAL NOTICE The information and views set out in this report are those of the author(s) and do not necessarily reflect the official opinion of the Commission. The Commission does not guarantee the accuracy of the data included in this study. Neither the Commission nor any person acting on the Commission’s behalf may be held responsible for the use which may be made of the information contained therein. Les informations et opinions exprimées dans ce rapport sont ceux de(s) l'auteur(s) et ne reflètent pas nécessairement l'opinion officielle de la Commission. La Commission ne garantit pas l’exactitude des informations comprises dans ce rapport. La Commission, ainsi que toute personne agissant pour le compte de celle-ci, ne saurait en aucun cas être tenue responsable de l’utilisation des informations contenues dans ce rapport. More information on the European Union is available on the Internet (http://www.europa.eu). Luxembourg: Publications Office of the European Union, 2017 Catalogue number: KD-02-17-687-EN-N ISBN 978-92-79-69466-0 doi: 10.2763/002126 © European Union, 2017 Reproduction is authorised provided the source is acknowledged. -

Lists of Current Accreditations for Operators (Networks)

Rich Communications Services Interoperability and Testing / Accreditation Lists of current accreditations for Operators (networks) Lists of current accreditations for Operators (networks) Accreditation List of services/service # Company name Network brand name Country Accreditation level Accreditation status type clusters UP-Framework, UP- Approved (valid until 1 Evolve Cellular Inc. Evolve Cellular USA Provisional Messaging, UP- Universal Profile 1.0 4.12.2018) EnrichedCalling China Mobile Communication UP-Framework, UP- Approved (valid until 2 China Mobile China Provisional Universal Profile 1.0 Co. Ltd. Messaging 25.02.2019) UP-Framework, UP- Universal Profile Approved (valid until 3 Vodafone Group Vodafone-Spain Spain Provisional Messaging, UP- Transition – Phase 1 20.12.2018) EnrichedCalling UP-Framework, UP- Universal Profile Approved (valid until 4 Vodafone Group Vodafone-Deutschland Germany Provisional Messaging, UP- Transition – Phase 1 20.12.2018) EnrichedCalling UP-Framework, UP- Vodafone Albania Sh. Universal Profile Approved (valid until 5 Vodafone Group Albania Provisional Messaging, UP- A Transition – Phase 1 20.12.2018) EnrichedCalling 29 January 2018 Rich Communications Services Interoperability and Testing / Accreditation Lists of current accreditations for Operators (networks) Accreditation List of services/service # Company name Network brand name Country Accreditation level Accreditation status type clusters UP-Framework, UP- Vodafone Czech Czech Universal Profile Approved (valid until 6 Vodafone Group Provisional -

Vodafone Revolutionises Roaming Rules

VODAFONE REVOLUTIONISES ROAMING RULES VODAFONE ALLOWS CUSTOMERS TO MAKE OVERSEAS CALLS AT DOMESTIC RATES Milan, May 17, 2005 – The Vodafone Group is about to revolutionise roaming prices, responding to customers’ demands for greater transparency and clarity when making or receiving calls whilst abroad. June 1 is to see the launch of Vodafone Passport, the first price plan forming part of the Group’s new Vodafone Travel Promise package. Vodafone Passport enables Vodafone customers who access the Group’s networks to make calls at domestic rates, paying just € 1.00 at the start of each call. The new offering provides Vodafone customers with greater transparency, giving better value for money and eliminating any doubts about cost effectiveness. When overseas Vodafone customers will thus be able to: • Call Italy: at the same prices charged for domestic calls, paying an additional €1.00 per call. • Receive calls: talking free of charge having paid a connection fee of just €1.00. “The nature of the Vodafone Group enables us to offer a veritable revolution in roaming services,” claimed Pietro Guindani, CEO of Vodafone Italia. “Vodafone Passport will make the customer feel at home in any country with a Vodafone network.” The new service will be available in Germany, Greece, Italy, the Netherlands, Spain, Sweden, Fiji and Japan from June 1. Hungary, Malta, Portugal, Ireland, the UK, Albania, Australia and New Zealand will introduce the price plan during the summer. Customers who use the SFR (France), Swisscom (Switzerland) and Proximus (Belgium) networks will also subsequently gain access. Vodafone Passport is the latest innovation created by the Vodafone Group with the aim of making it easier to make mobile calls when abroad and thus increase the use of roaming services.