News Release

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mobile Data Consumption Continues to Grow – a Majority of Operators Now Rewarded with ARPU

Industry analysis #3 2019 Mobile data – first half 2019 Mobile data consumption continues to grow – a majority of operators now rewarded with ARPU Taiwan: Unlimited is so last year – Korea: 5G boosts usage Tefficient’s 24th public analysis on the development and drivers of mobile data ranks 115 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the first half of 2019. tefficient AB www.tefficient.com 5 September 2019 1 The data usage per SIM grew for all; everybody climbed our Christmas tree. More than half of the operators could turn that data usage growth into ARPU growth – for the first time a majority is in green. Read on to see who delivered on “more for more” – and who didn’t. Speaking of which, we take a closer look at the development of one of the unlimited powerhouses – Taiwan. Are people getting tired of mobile data? We also provide insight into South Korea – the world’s leading 5G market. Just how much effect did 5G have on the data usage? tefficient AB www.tefficient.com 5 September 2019 2 Fifteen operators now above 10 GB per SIM per month Figure 1 shows the average mobile data usage for 115 reporting or reported1 mobile operators globally with values for the first half of 2019 or for the full year of 2018. DNA, FI 3, AT Zain, KW Elisa, FI LMT, LV Taiwan Mobile, TW 1) FarEasTone, TW 1) Zain, BH Zain, SA Chunghwa, TW 1) *Telia, FI Jio, IN Nova, IS **Maxis, MY Tele2, LV 3, DK Celcom, MY **Digi, MY **LG Uplus, KR 1) Telenor, SE Zain, JO 3, SE Telia, DK China Unicom, CN (handset) Bite, -

Customer Insight Development in Vodafone Italy

Customer Insight development in Vodafone Italy Emanuele Baruffa – Vodafone Seugi - Vienna, 17-19 June 2003 Seugi 21_Vienna Pag. 1 ContentsContents:: 1. Introduction 2. Customer Base Management 3. Customer Insight 4. Data Environment 5. Conclusions Seugi 21_Vienna Pag. 2 1. Introduction 2. Customer Base Management 3. Customer Insight 4. Data Environment 5. Conclusions Seugi 21_Vienna Pag. 3 MobileMobile telephonytelephony isis oneone ofof thethe fastestfastest growinggrowing industriesindustries inin thethe worldworld Worldwide growth in subscribers (millions) ! 1 billion subscribers 1480 around the world 1321 ! Over 120 1152 countries have 958 mobile networks 727 ! Further acceleration 479 expected 206 87 14 34 Source: EITO 1991 1993 1995 1997 1999 2000 2001 2002 2003e 2004e Seugi 21_Vienna Pag. 4 Italy:Italy: Europe’sEurope’s secondsecond biggestbiggest mobilemobile marketmarket Country Subscribers Penetration Western European TLC market % growth by country (%) 10 9,1 9 Germany 60,300,000 84% 8 6,8 6,8 7 6,2 6,1 5,7 5,8 Italy 54,000,000 98% 6 5,6 5,6 5,4 5,0 5 UK 50,900,000 92% 4,0 4 France 39,000,000 77% 3 Spain 34,000,000 88% 2 1 0 Germany Italy UK France Spain Western Europe Sources: internal sources for Italy, Yankee Group for Source: EITO other European countries 2001/2002 2002/2003 Seugi 21_Vienna Pag. 5 PenetrationPenetration raterate inin thethe ItalianItalian marketmarket 60,000 96% 98% 100% 91% Subscribers (,000) 90% 50,000 Penetration Rate 80% 74% 70% 40,000 60% 53% 30,000 50% 36% 40% 20,000 30% 21% 20% 10,000 11% 10% 0 0% 1996 1997 1998 1999 2000 2001 2002 2003 Seugi 21_Vienna Pag. -

Prepared for Upload GCD Wls Networks

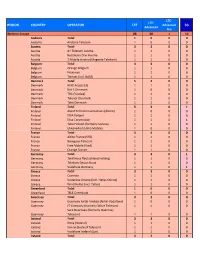

LTE‐ LTE‐ REGION COUNTRY OPERATOR LTE Advanced 5G Advanced Pro Western Europe 88 68 1 10 Andorra Total 10 0 0 Andorra Andorra Telecom 10 0 0 Austria Total 33 0 0 Austria A1 Telekom Austria 11 0 0 Austria Hutchison Drei Austria 11 0 0 Austria T‐Mobile Austria (Magenta Telekom) 11 0 0 Belgium Total 33 0 0 Belgium Orange Belgium 11 0 0 Belgium Proximus 11 0 0 Belgium Telenet (incl. BASE) 11 0 0 Denmark Total 54 0 0 Denmark Hi3G Access (3) 11 0 0 Denmark Net 1 Denmark 10 0 0 Denmark TDC (YouSee) 11 0 0 Denmark Telenor Denmark 11 0 0 Denmark Telia Denmark 11 0 0 Finland Total 53 0 1 Finland Aland Telecommunications (Alcom) 10 0 0 Finland DNA Finland 11 0 0 Finland Elisa Corporation 11 0 1 Finland Telia Finland (formerly Sonera) 11 0 0 Finland Ukkoverkot (Ukko Mobile) 10 0 0 France Total 44 0 0 France Altice France (SFR) 11 0 0 France Bouygues Telecom 11 0 0 France Free Mobile (Iliad) 11 0 0 France Orange France 11 0 0 Germany Total 33 0 1 Germany Telefonica Deutschland Holding 11 0 0 Germany Telekom Deutschland 11 0 0 Germany Vodafone Germany 11 0 1 Greece Total 33 0 0 Greece Cosmote 11 0 0 Greece Vodafone Greece (incl. Hellas Online) 11 0 0 Greece Wind Hellas (incl. Tellas) 11 0 0 Greenland Total 10 0 0 Greenland TELE Greenland 10 0 0 Guernsey Total 32 0 0 Guernsey Guernsey Airtel Limited (Airtel‐Vodafone) 10 0 0 Guernsey JT Guernsey (formerly Wave Telecom) 11 0 0 Sure Guernsey (formerly Guernsey Guernsey Telecom) 11 0 0 Iceland Total 33 0 0 Iceland Nova (Iceland) 11 0 0 Iceland Siminn (Iceland Telecom) 11 0 0 Iceland Vodafone Iceland (Syn) -

+60% +42% +11% 2000+ +9% How Vodafone Italy Raised Conversions +42% by Developing Creative in a Radically New

+ CASE STUDY TELECOM SERVICES How Vodafone Italy Raised Conversions +42% by Developing Creative in a Radically New Way For Vodafone, Words Matter. The Impact of Persado AI Vodafone Italy approaches every marketing Since 2012, Vodafone has used Persado’s message as an opportunity to design exceptional unique AI platform to machine-generate customer experiences, win customer loyalty, and marketing creative, gain customer analytics, and increase lifetime value. elevate the success of their chief campaigns. Mobile push notifications and SMS are their primary digital communication channels and major CAMPAIGNS growth engines for key business initiatives, 2000+ OPTIMIZED making the messaging even more crucial. When words fall flat, Vodafone loses business. *To date Their Goals % LIFT IN +42 CONVERSION RATE INCREASE LTV with upsell and cross- sell campaigns that suggest additional *CRM Campaigns services to current customers. PREVENT CHURN with lock-in % LIFT IN CONVERSION RATE campaigns that offer high-value, hard-to- +9 get customers convenient and exclusive *Winback Campaigns packages. WIN BACK FORMER CUSTOMERS % AVG LIFT in with winback campaigns critical to +60 REDEMPTION RATE growing market share. Loyalty Campaigns ENHANCE CUSTOMER SATISFACTION with loyalty campaigns that encourage % TOTAL SALES subscribers to engage with Vodafone’s +11 DRIVEN BY PERSADO loyalty program and weekly prize draws. *On SMS and PUSH www.persado.com [email protected] AI in Action Powered by machine learning, Persado’s platform uncovers key trends and rich insights -

Vodafone Group Plc

1 June 2016 Vodafone Group plc BUY Telecommunications Dividend risk reducing Paul Marsch Analyst +44 20 3207 7857 [email protected] Laura Janssens Analyst +44 20 3465 2639 [email protected] Julia Thannheiser Specialist Sales +44 20 3465 2676 [email protected] ATLAS ALPHA • THOUGHT LEADERSHIP • ACCESS • SERVICE Vodafone Group plc Telecommunications THE TEAM Paul Marsch has been with Berenberg since 2009. He was previously head of telecoms research at Morgan Stanley, where he was consistently very highly ranked. Paul has 20 years' experience in telecoms research, as well as having worked for five years in the telecoms industry for Cable & Wireless. Laura Janssens joined Berenberg in September 2011 and was previously head of global telecoms research at UBS and head of European telecoms research at Merrill Lynch. She has also worked at telecoms consultancy Analysys, and at BT. She has 17 years of telecommunications experience. Laura has been a top-ranked individual analyst in the Extel survey on several occasions. Julia Thannheiser joined the Berenberg specialist sales desk in May 2013. Prior to this, she spent over three years as a telecoms analyst at UBS. Julia holds a BSc from the University of Maastricht and a MSc from Cass Business School. For our disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG) and our disclaimer please see the end of this document. Please note that the use of this research report is subject to the conditions and restrictions set forth in the disclosures and the disclaimer at the end of this document. -

Vodafone Group Plc Plc Vodafone Group

Vodafone Group Plc Group Vodafone Plc Registered Office Vodafone Group Plc Vodafone House The Connection Annual Report Newbury Berkshire For the year ended 31 March 2010 RG14 2FN England Registered in England No. 1833679 Tel: +44 (0) 1635 33251 2010 March 31 ended year the Report for Annual Fax: +44 (0) 1635 45713 www.vodafone.com We are one of the world’s largest Contact details mobile communications companies Investor Relations by revenue, operating across the Telephone: +44 (0) 1635 33251 globe providing a wide range of Media Relations communications services. Our vision Telephone: +44 (0) 1635 664444 is to be the communications leader Corporate Responsibility in an increasingly connected world. Fax: +44 (0) 1635 674478 E-mail: [email protected] Website: www.vodafone.com/responsibility This constitutes the annual report of Vodafone Group Plc (the ‘Company’) for the year Contents ended 31 March 2010 and is dated 18 May 2010. The content of the Group’s website (www.vodafone.com) should not be considered to form part of this annual report or the Executive summary# Company’s annual report on Form 20-F. 1 Highlights 2 Chairman’s statement In the discussion of the Group’s reported financial position, operating results and cash flow 4 Telecommunications industry for the year ended 31 March 2010, information is presented to provide readers with additional financial information that is regularly reviewed by management. However this 6 Chief Executive’s review additional information is not uniformly defined by all companies, including those in the 10 Global presence Group’s industry. Accordingly, it may not be comparable with similarly titled measures and # disclosures by other companies. -

Vodafone Italy a History of Commitment3

Diversity and Inclusion: Vodafone Italia, a history of commitment Vodafone Group Vodafone is a leading telecommunications company in Europe and Africa. It is the largest mobile and fixed network operator in Europ e, is the world’s largest IoT connectivity provider, and our M-Pesa technology platform in Africa enables over 42 million people to benefit from access to mobile payments and financial services. We operate mobile and fixed networks in 22 countries and partner with mobile networks in 48 more. 2 26 November 2020 C2 General Vodafone Italy Vodafone offers its customers products and services based on the quality and power of the GigaNetwork TM Vodafone's fiber services reach over 24.2 million households and businesses. The 5G network is available in 5 cities (Milan, Turin, Bologna, Rome, Naples) and in 28 municipalities in the Milan metropolitan area. 6,000 employees . 3 26 November 2020 C2 General 1. D&I in Vodafone Italy • Our commitment started years ago… 2. Our Inclusion Agenda • “Un Passo Avanti” Roadshow 3. Gender equality • Maternity and parental leave policies • Smartworking “Mum&Dad” and Workshifts Agenda for Mums • Managerial Positions +1 Females & Reconnect 4. Domestic Violence and Abuse • 25th November International Day against Women's Violence 5. Q&A C2 General Our Commitment D&I in Vodafone started Italy years ago… C2 General D&I in Vodafone Italy Our commitment started years ago… 2015 2016 6 C2 General “Un Passo Inclusion AVANTI” Agenda Roadshow C2 General Inclusion Agenda “Un Passo AVANTI” Roadshow 2016 8 C2 General Inclusion Agenda “Un Passo AVANTI” Roadshow 2016 Four inclusion’s areas • Gender : gender equality between men and women. -

Pressing Forward

Pressing forward Vodafone Group Plc Sustainability Report For the year ending 31 March 2010 About our reporting About us This is Vodafone’s 10th annual Group report detailing the environmental and Contents social impacts of our business and covers the financial year ended 31 March 2010. About our reporting 1 Previously known as our Corporate Responsibility Report, in 2009/10 we changed the Customers change Climate Operations chain Supply Foundations Report scope Assurance against objectives Progress CEO message 2 title to Sustainability Report. We believe this shift in terminology better reflects the role Vodafone can play in promoting a more sustainable society (see our approach, page 5). About Vodafone 3 Our approach 5 This Report outlines our performance in 2009/10 on each of the environmental and social issues most material to our business. It also includes links to our sustainability Customers 15 website, where we provide more general information about our approach to each issue, Climate change 31 our policies and management processes. See www.vodafone.com/responsibility. Operations 40 Scope Supply chain 54 The scope of this Report includes sustainability data and activities from all local markets Foundations 59 managed by Vodafone for the full 2009/10 financial year, with the exception of Vodafone Report scope 61 Ghana and Vodafone Qatar (for more information see page 61). However, these markets are included in the discussion of issues where they are particularly material and we have Assurance 63 also included separate pullouts on both these markets to outline our progress there Progress against objectives 65 during 2009/10 (see pages 12–13). -

Delivering on Our Strategic Objectives

Vodafone Group Plc Group Vodafone Annual Report for the year ended 31 March 2007 ended 31 March the year Annual Report for Delivering on our strategic objectives Vodafone Group Plc Registered office: Vodafone House The Connection Newbury Berkshire RG14 2FN England Registered in England No.1833679 Tel: +44 (0) 1635 33251 Vodafone Group Plc Fax: +44 (0) 1635 45713 Annual Report www.vodafone.com For the year ended 31 March 2007 WorldReginfo - 62747ee2-b1f8-4204-9590-ec1516ef53cb Contact Details Our goal is to be the Investor Relations: Telephone: +44 (0) 1635 664447 Media Relations: communications leader Telephone: +44 (0) 1635 664444 Corporate Responsibility: Fax: +44 (0) 1635 674478 E-mail: [email protected] in an increasingly Website: www.vodafone.com/responsibility connected world This constitutes the Annual Report of Vodafone Group Plc (the “Company”) in accordance with In presenting and discussing the Group’s reported financial position, operating results and cash flows, International Financial Reporting Standards (“IFRS”) and with those parts of the Companies Act 1985 certain information is derived from amounts calculated in accordance with IFRS but this information applicable to companies reporting under IFRS and is dated 29 May 2007. References to IFRS refer to is not itself an expressly permitted GAAP measure. Such non-GAAP measures should not be viewed in IFRS as issued by the IASB and IFRS as adopted for use in the European Union (“EU”). This document also isolation or as an alternative to the equivalent GAAP measure. An explanation as to the use of these contains information set out within the Company’s Annual Report on Form 20-F in accordance with the measures and reconciliations to their nearest equivalent GAAP measures can be found on requirements of the United States (“US”) Securities and Exchange Commission (the “SEC”). -

Network Economics: Vodafone Case Study

Network Economics: Vodafone case study Battery Theft September 2018 GSM Association Non - Confidential Case Study – Vodafone: GPS Battery Anti-Theft Table of Contents Executive Summary 4 1 Introduction 5 2 Business Imperative 5 3 Vodafone: The Solution 6 4 Economic benefits 7 4.1 Assumptions: Error! Bookmark not defined. 4.2 CapEX avoidance Error! Bookmark not defined. 4.3 OpEX avoidance Error! Bookmark not defined. 5 Market Context 8 6 Conclusion 9 V1.0 Page 3 of 8 GSM Association Non - Confidential Case Study – Vodafone: GPS Battery Anti-Theft Executive Summary As part of the Future Networks Programme, Network Economics workstream, a series of case studies exploring areas where Operators can potentially reduce their Operational Expenditure (OpEx) and Capital Expenditure (CapEX) have been developed. This case study focuses on a key issue that affects mobile operators irrespective of their geographic location base station battery pilferage. In recent years, Vodafone Italia has suffered a significant series of break-ins at base station sites – with peaks of over a thousand in a year. Aside from the clear CapEX investment required for re-securing the site and battery replacements, interrupting the battery replenishment cycle creates greater maintenance requirements, leading to increased OpEX. To combat theft, Vodafone in conjunction with the Vodafone Automotive team and their battery suppliers, have installed concealed GPS devices within the battery casing and is indistinguishable from standard non-GPS enabled batteries. When unauthorised movements or vibrations above a certain threshold are detected, the GPS sensors are activated, and movements are monitored in real time, remotely from Vodafone’s Security Operations Centre (SOC). -

Juhtmevaba Suveaega!

suvi 2008 suvi kliendileht Juhtmevaba suveaega! M-INTERNETI PAKETIGA suurim valik kiire andmeühendusega telefone! Mobiilne internet võidab järjest enam poolehoidu ja meie M-interneti paketid järjest enam kasutajaid. Just seepärast tahame sulle, hea klient, pakkuda võimalust ka oma valitud M-interneti paketilt kasu lõigata. Kuidas? Mai keskpaigast alates aitab valitud M-interneti pakett kaasa võimalusele leida meie soodustelefo- Kui kasutad lisaks kõnepake- nide hulgast just sinu maitsele ja vajadustele vastav tile ka M-interneti paketti, on telefon, sest kui kasutad lisaks kõnepaketile ka ”soodushinnaga telefonide valik M-interneti paketti, on soodushinnaga telefonide sinu jaoks suurem. valik sinu jaoks suurem. Soodushinnaga telefonide valikut tehes aga on omakorda suurim rõhk sellel, et vastavalt valitud ” M-interneti paketile saaksid soodushinnaga soetada ka telefoni, mis M-interneti paketis võimaldatavat kiirust toetab ehk siis kui kasutad 3,5G kiirusega paketti M-internet 349, leiad kindlasti soodustelefonide hulgast ka telefoni, mis antud kiirust kasutada võimaldab. Juba käesolevas SOODUSHIND: kliendilehes on Näiteks! soodushinnad välja 0.- – 99 199 349 Soodushind kehtib, toodud risttabelina, kui kasutad paketti kus siis sinu kasutatava Elisa 150 / Pere 300 / Äri 300 M-internet 349 ja kõnepaketi rea ja Elisa 250 / Pere 500 / Äri 600 kõnepaketti alates M-interneti paketi Elisa 500 / Pere 1000 / Äri 1200 Elisa 150, Elisa Pere 300 veeru ristumislahtris või Elisa Äri 300. olev punktike annab Elisa 1000 / Pere 2000 / Äri 2400 sulle märku, et just sulle selle telefoni Näiteks! Soodushind kehtib, kui Sul M-interneti soodushind kehtibki. paketti ei ole, aga kasutad paketti Elisa 1000, Elisa Pere 2000 või Elisa Äri 2400. Elisa M-interneti pakettide kohta saad lähemalt lugeda Kliendilehe leheküljelt 16. -

Vodafone K.K. to Offer Japan's First 3G Data Card Roaming Service

Notice 26 July 2005 Vodafone K.K. to offer Japan’s first 3G data card roaming service Upgraded VC701SI can be used on W-CDMA networks in 18 countries & regions Vodafone K.K. announces today that from early September 2005 it will market a new version of its currently available VC701SI Vodafone Connect Card (manufactured by SII) with upgraded firmware*1 to let customers roam on W-CDMA networks overseas at high packet transmission speeds of up to 384kbps for downlinks (on a best effort basis*2). Marking a first in Japan*3, this upgrade will enable customers to enjoy mobile internet access abroad on PCs or PDAs using 3G data cards. The Vodafone Connect Card, which is currently available as the W-CDMA (3G) compatible VC701SI CompactFlash® (Type II) data card terminal, was launched in April 2004 exclusively for data usage in Japan, is popular among individuals and business customers in particular. With this upgrade, Vodafone Connect Card can be used on W-CDMA networks in 18 countries and regions in Europe and Asia (on the networks of 20 mobile operators), to support the mobile communications of customers going abroad for business trips. For easy connections while roaming abroad and enhanced ease-of-use, the upgraded Vodafone Connect Card comes bundled with Roaming Tool software (which supports Windows® 98SE/Me/2000/XP and Mac OS X). From early September 2005, Vodafone K.K. will send CD-ROM upgrades, which contain the Firmware Upgrade Tool and Roaming Tool, to all customers currently using the VC701SI. The same software tools are also scheduled to be available for download from SII’s website in early September.