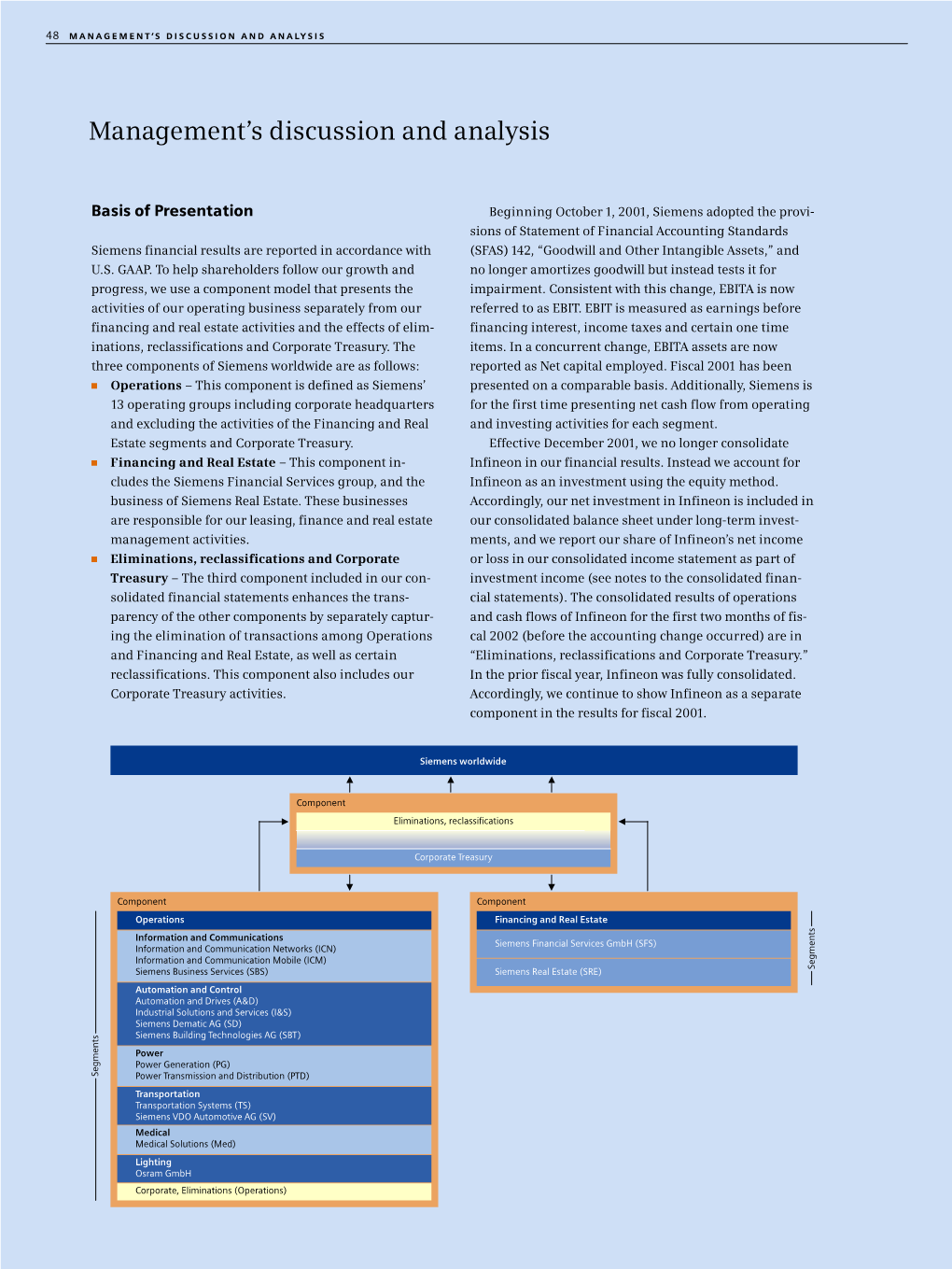

Management's Discussion and Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Siemens Share Price

Siemens share price Stock market trend (XETRA closing prices, Frankfurt, in euros) indexed Low: 32.05 High*: 68.60 200 Siemens 180 DAX Dow Jones Stoxx 160 140 120 100 80 Nov. Jan. March May July Sept. Nov. Jan. 2003 2004 *as of January 19, 2004 Key figures – Fiscal 2003 in billions of euros Percentage 2003 2002 change Net income 2.445 1.661* + 47 Group profit 4.295 3.756 + 14 New orders 75.056 86.214 -5** Sales 74.233 84.016 -4** Net cash provided by operating activities 5.712 5.564 + 3 * excl. €936 million from sales of Infineon shares ** Adjusted for currency effects and portfolio activities Employees (I) 2003* 2002* Change Worldwide 417,000 426,000 - 9,000 Germany 170,000 175,000 - 5,000 Outside 247,000 251,000 - 4,000 Germany * September 30 Employees (II) 2% reduction worldwide Success in training and placement 5,000 new hires in Germany 12,000 in training programs Operation 2003 (I) 8 of 9 Groups Margin targets achieved targets Q4 03 FY 03 Target PG Power Generation 11.3 16.8 10 – 13 Med Medical Solutions 14.0 15.1 11 – 13 A&D Automation & Drives 10.5 9.6 11 – 13 Osram 10.3 9.8 10 – 11 PTD Power Transmission and Distr. 7.4 6.1 5 – 7 TS Transportation Systems 5.5 6.0 5 – 7 SV Siemens VDO Automotive 5.8 5.0 5 – 6 SFS* Siemens Financial Services 20.5 24.9 18 – 22 SBT Siemens Building Technologies 2.7 2.0 7 – 9 *) Return on shareholders' equity before income taxes Operation 2003 (II) Power Generation Demag Delaval successfully integrated Alstom industrial turbines round out product range Offerings for oil & gas industry expanded Operation -

2013 Customer Success Stories

Customer Success Stories 2013 Edition Stories Success Customer Customer Success Stories Proven Solutions for Every Industry ICONICS World Headquarters 100 Foxborough Blvd. Foxborough, MA 02035 Tel: 508 543 8600 Email: [email protected] ICONICS Europe ICONICS Asia Czech Republic Australia Tel: 420 377 183 420 Tel: 61 2 9727 3411 Email: [email protected] Email: [email protected] France China Tel: 33 4 50 19 11 80 Tel: 86 10 8494 2570 Email: [email protected] Email: [email protected] Germany India Tel: 49 2241 16 508 0 Tel: 91 22 67291029 Email: [email protected] Email: [email protected] Italy Tel: 39 010 46 0626 ICONICS UK Email: [email protected] United Kingdom Tel: 44 1384 246 700 Netherlands Email: [email protected] Tel: 31 252 228 588 Email: [email protected] WWW.ICONICS.COM Visualize YourYour Enterprise™Enterprise™ Customers & Partners Featured ICONICS Thanks Our Loyal Customers from Around the World ICONICS is a leading provider of award-winning real-time visualization, SCADA and operational management software for manufacturing intelligence and building automation. ICONICS software delivers significant cost reductions in design, building, deployment and maintenance for a wide variety of manufacturing companies, building owners and government organizations. ICONICS solutions have helped our users to be more agile and productive and to achieve sustained profitability. Our products are installed in over 250,000 applications worldwide, continuously delivering value to more than 70% of the Fortune 1000. © 2013 ICONICS, Inc. All rights reserved. Specifications are subject to change without notice. AnalytiX and its respective modules are registered trademarks of ICONICS, Inc. -

Annual Report 2004 2

s Annual Report 2004 2 Contents 4 let t er to our shareholders 13 at a glance 18 business areas 28 siemens one 32 report of the supervisory board 40 Corporate Governance Report 48 Compensation Report 54 information for shareholders * 56 Management’s discussion and analysis 96 Consolidated financial statements 174 Statement of the Managing Board 175 Independent auditors’ report 178 Supervisory Board 180 Managing Board 186 Siemens financial calendar corporat e structure ** * With separate table of contents ** See foldou2004t inside back cover. 3 Siemens – a global network of innovation comprising more than 400,000 people – offers innovative products, solutions and services spanning the entire field of electronics and electrical engineering. Our innovations are shaping tomorrow’s world, giving our cus- tomers a competitive edge and improving the lives of people every- where. We aim to capture leading market positions in all our busi- nesses and to achieve profitable growth now and in the future. Our success is based on a well-focused business portfolio, a truly global presence and an international workforce of highly qualified and highly motivated managers and employees. key figures in millions of euros 2004 (1) 2003 (1) New orders 80,830 75,056 Sales 75,167 74,233 Net income 3,405 2,445 Effects related to Infineon share sale and a goodwill impairment(2) 403 3,002 Net cash from operating and investing activities 3,262 1,773 Research and development expenses 5,063 5,067 Shareholders’ equity (September 30) 26,855 23,715 Employees (September 30, in thousands) 430 417 (1) Fiscal year: October 1 to September 30 (2) Pretax gain of €590 million on sale of Infineon shares plus related €246 million reversal of deferred tax liability, less a goodwill impairment of €433 million. -

Ausgabe 01/2006

01 _Together_0106.indd 3 06.04.2006 13:52:27 Uhr Gewinnspiel Inhalt Editorial Gewinnen Sie mit together! Inhalt Stilvolle Tage in Prag 4 Cover: Auf den Megatrends surfen Liebe Mitarbeiterinnen, Brigitte Ederer, Vorstandsvorsitzende von Die Goldene Stadt Prag ist eine Reise wert. Beginnen Sie Siemens Österreich, beschreibt ihre Vorstel- liebe Mitarbeiter Ihren Rundgang mit der weltberühmten Burg, besich- lungen von der Zukunft des Unternehmens, tigen Sie die Paläste und faszinierenden Jugendstil- Eine neue Chefin – das ist für viele Siemens- das zur vitalen Denkfabrik werden soll. bauten, lassen Sie sich von den Vorführungen auf der MitarbeiterInnen ein Grund nachzudenken, 8 Die Folgen des Hydro-Verkaufs Karlsbrücke bezaubern, entspannen Sie in einem Alt- was sich nun ändern wird, wie Siemens Was sich für PTD/PG und SAT durch den stadtcafé, und genießen Sie die Atmosphäre der Klein- Österreich in einigen Jahren aussehen wird. seite (Mala Strana). Am besten wohnen können Sie Verkauf der Hydro ändert. Ich habe eine klare Vorstellung von Siemens im Crowne Plaza Prague, das selbst ein nationales Bau- 10 Gelungener Start Österreich im Jahr 2010. Wir wollen bis denkmal ist, mitten im Botschafterviertel in unmittel- Die Industriebereiche von Siemens Elin dahin ein Unternehmen sein, das in einem barer Nähe zur Prager Burg. profitieren bereits von der Integration. zentraleuropäischen Wirtschaftsraum mit 65 Mio. Einwohnern agiert, als wäre dieser 12 Aufbruch in eine neue Struktur Raum ein Land. Ich werde in den nächsten Das Gebäudeprojektgeschäft wird zu einem Jahren von Ihnen verlangen, Grenzen in den eigenen Unternehmen. Köpfen zu beseitigen, auch zwischen den 14 Nummer 1 am Markt 12 Bereichen. -

Siemens Management Innovation at the Corporate Level Case Study Reference No 310-114-1

Siemens Management Innovation at the Corporate Level Case study Reference no 310-114-1 This case was written by Dr Markus Menz and Professor Dr Guenter Mueller-Stewens, University of St Gallen, Switzerland. It is intended to be used as the basis for class discussion rather than to illustrate either effective or ineffective handling of a management situation. The case was written with the support of a Philip Law Scholarship awarded by ecch. The case was made possible by the co-operation of Siemens AG and from published sources. © 2010, University of St Gallen, Switzerland. No part of this publication may be copied, stored, transmitted, reproduced or distributed in any form or medium whatsoever without the permission of the copyright owner. Distributed by ecch, UK and USA North America Rest of the world www.ecch.com t +1 781 239 5884 t +44 (0)1234 750903 ecch the case for learning All rights reserved f +1 781 239 5885 f +44 (0)1234 751125 Printed in UK and USA e [email protected] e [email protected] 310-114-1 MARKUS MENZ GÜNTER MÜLLER-STEWENS SIEMENS: MANAGEMENT INNOVATION AT THE CORPORATE LEVEL INTRODUCTION At the Annual Shareholders’ Meeting in February 1998, Siemens announced disappointing overall results for fiscal 1997. While the firm’s sales growth met shareholder expectations, net income remained largely stable. During the following weeks and months, Siemens’ top management not only faced increased pressure from its shareholders, but also higher environmental uncertainty and stronger global competition than during the early and mid-1990s. The challenge for the top management team was to optimize the business portfolio in a way that promised to add substantial shareholder value over the next years. -

Solutions for Airports

Solutions for Airports Cleared for take off. Siemens Airports Flight security – currently the topic on everyone’s lips and a highly controversial one at that. Safety on the ground and in the air is top of every list of priorities. And a lot of hard work is going on behind the scenes to guarantee it. All over the world, airport security regulations are stricter than ever before. Complying with them demands a partner who is thoroughly familiar with all the ins and outs of air traffic. A partner with the expertise to integrate all essential activities in a powerful network. Proof that safety and cost-effectiveness in the aviation industry are not mutually exclusive. Siemens Airports – your partner for airport solutions A task that we are glad to shoulder at Siemens Airports. Firmly embedded in Siemens, we can provide you with all the benefits of one of the world’s leading suppliers of electrical engineering and electronics technology while being able to tap into the huge potential that a global organization has to offer. This potential as well as the innovativity and the extensive know-how of Siemens Airports benefits all aspects of airport ground traffic. As an experienced and capable partner, we know all the technical and logistical aspects of airport solutions and have been equipping airlines, airports, and flight safety authorities for decades. For projects large or small, we can assume turnkey responsibility for the construction of a complete airport or supply just the runway lighting system. Or the flight safety technology. Or the information technology. Or the communications technology. -

We Are on the Right Track for Ensuring Our Success

s »We have made great progress in »We are on the right track for networking our internal value ensuring our success as the chain electronically and in linking it to our customers, suppliers and Global network of innovation.« partners. This is enabling us to accelerate processes and cut costs.« Annual Report 2001 Annual s Annual Report 2001 Siemens Aktiengesellschaft Order No. A19100-F-V055-X-7600 Siemens Siemens is a network encompassing well over 400,000 people in 190 countries. information on contents for external orders We take pride in possessing in-depth knowledge of customers' requirements, the Telephone +49 89 636-33032 (Press Office) e-mail [email protected] expertise to create innovative solutions in electrical engineering and electronics, and +49 89 636-32474 (Investor Relations) Internet http://www.siemens.de/geschaeftsbericht_2001/order Fax +49 89 636-32825 (Press Office) Telephone +49 89 636-32910 the experience to successfully navigate even rough economic waters. But our greatest +49 89 636-32830 (Investor Relations) Fax +49 89 636-32908 e-mail [email protected] asset is undoubtedly our people, with their unparalleled motivation and their passion [email protected] for outperforming our competitors. Linked via a global network that enables them address for internal orders to exchange ideas with colleagues around the world, Siemens employees strive Siemens AG Wittelsbacherplatz 2 LZF, Fürth-Bislohe continuously to increase company value. D-80333 Munich Intranet http://c4bs.spls.de/ We at Siemens do not measure value solely in terms of short-term profitability. For Federal Republic of Germany Fax +49 911 654-4271 Internet http://www.siemens.com German Order no. -

Universidade Estadual De Campinas Instituto De Economia Matheus De Oliveira Erhardt Brito Diversificação Como Estratégia De E

UNIVERSIDADE ESTADUAL DE CAMPINAS INSTITUTO DE ECONOMIA MATHEUS DE OLIVEIRA ERHARDT BRITO DIVERSIFICAÇÃO COMO ESTRATÉGIA DE EXPANSÃO DO GRUPO SIEMENS CAMPINAS 2014 MATHEUS DE OLIVEIRA ERHARDT BRITO DIVERSIFICAÇÃO COMO ESTRATÉGIA DE EXPANSÃO DO GRUPO SIEMENS Trabalho de Conclusão de Curso apresentado à Graduação do Instituto de Economia da Universidade Estadual de Campinas para a obtenção do título de Bacharel em Ciências Econômicas, sob orientação do Prof. Dr. Rodrigo Lanna Franco da Silveira. CAMPINAS 2014 FOLHA DE APROVAÇÃO Monografia intitulada “DIVERSIFICAÇÃO COMO ESTRATÉGIA DE EXPANSÃO DO GRUPO SIEMENS”, área de concentração: Estratégias, custos, finanças e desempenho das empresas de autoria de MATHEUS DE OLIVEIRA ERHART BRITO, acadêmico do curso de Ciências Econômicas da Universidade Estadual de Campinas, aprovada pela banca examinadora constituída pelos professores abaixo especificados. ___________________________________________________ Prof. Dr. Rodrigo Lanna Franco da Silveira - Orientador Universidade Estadual de Campinas ___________________________________________________ Profª. Drª. Maria Carolina Azevedo Ferreira de Souza Universidade Estadual de Campinas Campinas 2014 DEDICATÓRIA Ao meu falecido pai, Rubens Erhardt Brito, que nos deixou precocemente, mas que vive eternamente em nossos corações e à minha mãe Eliana de Oliveira Erhardt Brito, que está ao meu lado todo o tempo. AGRADECIMENTOS Agradeço à minha mãe Eliana e ao meu pai Rubens, à minha avó Vicentina e ao meu tio Cleiton, que estiveram ao meu lado todas as fases da minha vida, por me apoiarem nas minhas decisões e por acreditarem em mim como pessoa. Não posso deixar de agradecer também ao meu irmão Miguel e à minha irmã Flávia, que me ensinaram aos poucos o irmão fraterno, assim como aos meu queridos sobrinhos Leonardo, Maria Paula, Beatriz e Felipe, que me proporcionam tantos momentos de felicidade. -

International Corporate Investment in Ohio Operations June 2020

Research Office A State Affiliate of the U.S. Census Bureau International Corporate Investment in Ohio Operations 20 September 2007 June 20 June 2020 Table of Contents Introduction and Explanations Section 1: Maps Section 2: Alphabetical Listing by Company Name Section 3: Companies Listed by Country of Ultimate Parent Section 4: Companies Listed by County Location International Corporate Investment in Ohio Operations June 2020 THE DIRECTORY OF INTERNATIONAL CORPORATE INVESTMENT IN OHIO OPERATIONS is a listing of international enterprises that have an investment or managerial interest within the State of Ohio. The report contains graphical summaries of international firms in Ohio and alphabetical company listings sorted into three categories: company name, country of ultimate parent, and county location. The enterprises listed in this directory have 5 or more employees at individual locations. This directory was created based on information obtained from Dun & Bradstreet. This information was crosschecked against company Websites and online corporate directories such as ReferenceUSA®. There is no mandatory state filing of international status. When using this directory, it is important to recognize that global trade and commerce are dynamic and in constant flux. The ownership and location of the companies listed is subject to change. Employment counts may differ from totals published by other sources due to aggregation, definition, and time periods. Research Office Ohio Development Services Agency P.O. Box 1001, Columbus, Ohio 43266-1001 Telephone: (614) 466-2116 http://development.ohio.gov/reports/reports_research.htm International Investment in Ohio - This survey identifies 4,303 international establishments employing 269,488 people. - Companies from 50 countries were identified as having investments in Ohio. -

Estudio Del Departamento De Servicios De Siemens S.A

2011 Estudio del Departamento de Servicios de Siemens S.A. Autor: Borja Calatayud Soriano Director: Bernardo Tormos Martínez 22/06/2011 1 Borja Calatayud Soriano Prefacio Este es un Trabajo para la Universidad Politécnica de Valencia de final del Máster en la Ingeniería del Mantenimiento, cursado después de haber obtenido la diplomatura de Ingeniero Técnico Industrial Especializado en Mecánica. Se ha realizado el periodo de prácticas en la empresa SIEMENS S.A. la cual y teniendo en cuenta la situación económica actual, se plantea diversas estrategias administrativas, entre ellas centralizar el departamento de organización y gestión del servicio técnico, de la parte de industrias, para toda España. Con estas premisas se decidió realizar este estudio para proponer mejoras en la misma, en el sector de servicio técnico y mantenimiento, estudiando su eficiencia. Pudiendo demostrar así, los conocimientos sobre todo a nivel organizativo adquiridos a lo largo de la formación del máster. Teniendo en cuenta que la empresa ya dispone de sistema organizativo altamente eficiente, sería importante aclarar hasta qué punto se puede mejorar o no la eficicácia del departamento, para que la dirección pueda tener un punto de vista enfocado hacia la correcta gestión del mantenimiento, que no es más que encontrar el equilibrio entre el correcto control y funcionamiento de las instalaciones y el coste del mantenimiento. 2 Borja Calatayud Soriano 1.Índice Prefacio ............................................................................................................................ -

Go for Profit and Growth Heinz-Joachim Neubürger, CFO

Go for profit and growth Heinz-Joachim Neubürger, CFO MAY-04 Key figures – Second quarter in billions of euros Q204 Q203 New orders 19.7 19.1 Sales 17.8 18.2 Group profit from Operations 1.076 1.073 Net income 1.210 0.568 EPS (in euros) 1.36 0.64 Net cash from operating and investing activities 3.565 1.398 MAY-04 2 Key figures – First six months in billions of euros HY04 HY03 New orders 40.2 39.2 Sales 36.1 37.1 Group profit from Operations 2.437 2.170 Net income 1.936 1.089 EPS (in euros) 2.17 1.22 Net cash from operating and investing activities 2.374 0.261 MAY-04 3 Key features HY04 Growth achieved ! In line with expectations, reflecting “flat” - tish global market for turnkey systems ! Stronger growth in the product business, notably Medical and A&D on comparable basis, indicating market share gaining in certain sectors Strong cash flow ! Proceeds from sale of Infineon shares cover special contribution to pension plans ! Ongoing tight control of Capex relative to Depreciation indicating underline changes within the value added structure Transportation Systems ! Frustrating and embarrassing development MAY-04 4 Ongoing improvement in the I&C segment ICN – Information and Communication Networks ! Profit driven by restructuring in 03 and new products ! Carrier and Enterprise business in the black ! Demand situation “flat” - tish ICM – Information and Communication Mobile ! Solid performance on mobile networks ! Unit volume of handsets sharply up on YoY comparison, however marginally down over seasonally strong Christmas quarter ! ASP challenging - improvement expected with 65 series MAY-04 5 Sustainable success A&D – Automation and Drives ! Market share gain in all businesses across the globe ! Better performance in the U.S. -

Annual Report 2005 Key Figures

s Annual Report 2005 Key figures in millions of euros 2005 (1) 2004 (1) New orders(2) 83,791 75,789 Sales(2) 75,445 70,237 Income from continuing operations 3,058 3,450 Loss from discontinued operations, net of income taxes (810) (45) Net income 2,248 3,405 Net cash from operating and investing activities(2) (1,489) 3,015 therein: Net cash provided by operating activities 4,217 4,704 Net cash used in investing activities (5,706) (1,689) Supplemental contributions to pension trusts (included in net cash provided by (used in) operating activities) (1,496) (1,255) Net proceeds from the sale of Infineon shares (included in net cash provided by (used in) investing activities) – 1,794 Research and development expenses(2) 5,155 4,650 Shareholders’ equity (September 30) 27,117 26,855 Employees(2) (September 30, in thousands) 461 424 (1) Fiscal year from October 1 to September 30 (2) Continuing operations (excluding the discontinued mobile devices activities) Contents Letter to our Shareholders 6 Managing Board 12 Fit4More Performance and Portfolio 14 Operational Excellence 18 People Excellence 22 Corporate Responsibility 26 Group Presidents 30 Business Areas 32 Megatrends 48 Report of the Supervisory Board 64 Corporate Governance Report 72 Compensation Report 78 Information for shareholders* 88 Management’s discussion and analysis 90 Consolidated Financial Statements 136 Statement of the Managing Board 214 Independent auditors’ report 215 Supervisory Board 220 Managing Board 222 Siemens financial calendar 228 Corporate Structure** * With separate