Chips with Everything Lessons for Effective Government Support for Clusters from the South West Semiconductor Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Semiconductor Industry Social Media Review

Revealed SOCIAL SUCCESS White Paper Who’s winning the social media battle in the semiconductor industry? Issue 2, September 3, 2014 The contents of this White Paper are protected by copyright and must not be reproduced without permission © 2014 Publitek Ltd. All rights reserved Who’s winning the social media battle in the semiconductor industry? Issue 2 SOCIAL SUCCESS Who’s winning the social media battle in the semiconductor industry? Report title OVERVIEW This time, in the interest of We’ve combined quantitative balance, we have decided to and qualitative measures to This report is an update to our include these companies - Intel, reach a ranking for each original white paper from channel. Cross-channel ranking Samsung, Sony, Toshiba, Nvidia led us to the overall index. September 2013. - as well as others, to again analyse the following channels: As before, we took a company’s Last time, we took the top individual “number semiconductor companies 1. Blogs score” (quantitative measure) (according to gross turnover - 2. Facebook for a channel, and multiplied main source: Wikipedia), of this by its “good practice score” 3. Google+ which five were ruled out due (qualitative measure). 4. LinkedIn to the diversity of their offering 5. Twitter The companies were ranked by and the difficulty of segmenting performance in each channel. 6. YouTube activity relating to An average was then taken of semiconductors. ! their positions in each to create the final table. !2 Who’s winning the social media battle in the semiconductor industry? Issue 2 Due to the instantaneous nature of social media, this time we decided to analyse a narrower time frame, and picked a single month - August 2014. -

Silicon Cities Silicon Cities Supporting the Development of Tech Clusters Outside London and the South East of England

Policy Exchange Policy Silicon Cities Cities Silicon Supporting the development of tech clusters outside London and the South East of England Eddie Copeland and Cameron Scott Silicon Cities Supporting the development of tech clusters outside London and the South East of England Eddie Copeland and Cameron Scott Policy Exchange is the UK’s leading think tank. We are an educational charity whose mission is to develop and promote new policy ideas that will deliver better public services, a stronger society and a more dynamic economy. Registered charity no: 1096300. Policy Exchange is committed to an evidence-based approach to policy development. We work in partnership with academics and other experts and commission major studies involving thorough empirical research of alternative policy outcomes. We believe that the policy experience of other countries offers important lessons for government in the UK. We also believe that government has much to learn from business and the voluntary sector. Trustees Daniel Finkelstein (Chairman of the Board), David Meller (Deputy Chair), Theodore Agnew, Richard Briance, Simon Brocklebank-Fowler, Robin Edwards, Richard Ehrman, Virginia Fraser, David Frum, Edward Heathcoat Amory, Krishna Rao, George Robinson, Robert Rosenkranz, Charles Stewart-Smith and Simon Wolfson. About the Authors Eddie Copeland – Head of Unit @EddieACopeland Eddie joined Policy Exchange as Head of the Technology Policy Unit in October 2013. Previously he has worked as Parliamentary Researcher to Sir Alan Haselhurst, MP; Congressional intern to Congressman Tom Petri and the Office of the Parliamentarians; Project Manager of global IT infrastructure projects at Accenture and Shell; Development Director of The Perse School, Cambridge; and founder of web startup, Orier Digital. -

Timeline of the Semiconductor Industry in South Portland

Timeline of the Semiconductor Industry in South Portland Note: Thank you to Kathy DiPhilippo, Executive Director/Curator of the South Portland Historical Society and Judith Borelli, Governmental Relations of Texas Inc. for providing some of the information for this timeline below. Fairchild Semiconductor 1962 Fairchild Semiconductor (a subsidiary of Fairchild Camera and Instrument Corp.) opened in the former Boland's auto building (present day Back in Motion) at 185 Ocean Street in June of 1962. They were there only temporarily, as the Western Avenue building was still being constructed. 1963 Fairchild Semiconductor moves to Western Avenue in February 1963. 1979 Fairchild Camera and Instrument Corp. is acquired/merged with Schlumberger, Ltd. (New York) for $363 million. 1987 Schlumberger, Ltd. sells its Fairchild Semiconductor Corp. subsidiary to National Semiconductor Corp. for $122 million. 1997 National Semiconductor sells the majority ownership interest in Fairchild Semiconductor to an investment group (made up of Fairchild managers, including Kirk Pond, and Citcorp Venture Capital Ltd.) for $550 million. Added Corporate Campus on Running Hill Road. 1999 In an initial public offering in August 1999, Fairchild Semiconductor International, Inc. becomes a publicly traded corporation on the New York Stock Exchange. 2016 Fairchild Semiconductor International, Inc. is acquired by ON Semiconductor for $2.4 billion. National Semiconductor 1987 National Semiconductor acquires Fairchild Semiconductor Corp. from Schlumberger, Ltd. for $122 million. 1995 National Semiconductor breaks ground on new 200mm factory in December 1995. 1996 National Semiconductor announces plans for a $600 million expansion of its facilities in South Portland; construction of a new wafer fabrication plant begins. 1997 Plant construction for 200mm factory completed and production starts. -

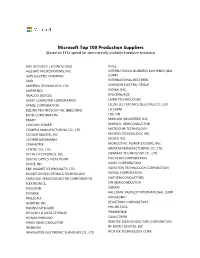

Microsoft Top 100 Production Suppliers (Based on FY14 Spend for Commercially Available Hardware Products)

Microsoft Top 100 Production Suppliers (Based on FY14 spend for commercially available hardware products) AAC ACOUSTIC TECHNOLOGIES INTEL ALLEGRO MICROSYSTEMS, INC. INTERNATIONAL BUSINESS MACHINES (IBM ALPS ELECTRIC COMPANY CORP.) AMD INTERNATIONAL RECTIFIER AMPEREX TECHNOLOGY, LTD. JOHNSON ELECTRIC GROUP AMPHENOL KIONIX, INC. ANALOG DEVICES KYOCERA/AVX ASKEY COMPUTER CORPORATION LAIRD TECHNOLOGIES ATMEL CORPORATION LELON ELECTRONICS (SUZHOU) CO., LTD BIZLINK TECHNOLOGY INC (BIZCONN) LG CHEM BOYD CORPORATION LITE-ON BRADY MARLOW INDUSTRIES, INC. CHICONY POWER MARVELL SEMICONDUCTOR COMPEQ MANUFACTURING CO., LTD. MICROCHIP TECHNOLOGY COOLER MASTER, INC. MICRON TECHNOLOGY, INC. COOPER BUSSMANN MOLEX, INC. CYMMETRIK MONOLITHIC POWER SYSTEMS, INC. CYNTEC CO., LTD. MURATA MANUFACTURING CO., LTD. DELTA ELECTRONICS, INC. NEWMAX TECHNOLOGY CO., LTD. DIGITAL OPTICS VISTA POINT NICHICON CORPORATION DIODE, INC. NIDEC CORPORATION E&E MAGNETICS PRODUCTS, LTD. NUVOTON TECHNOLOGY CORPORATION ELLINGTON ELECTRONICS TECHNOLOGY NVIDIA CORPORATION FAIRCHILD SEMICONDUCTOR CORPORATION NXP SEMICONDUCTORS FLEXTRONICS ON SEMICONDUCTOR FOXCONN OSRAM FOXLINK PALCONN, PALPILOT INTERNATIONAL CORP. FREESCALE PANASONIC GOERTEK, INC. PEGATRON CORPORATION HANNSTAR BOARD PHILIPS PLDS HITACHI-LG DATA STORAGE PRIMESENSE HONDA PRINTING QUALCOMM HYNIX SEMICONDUCTOR REALTEK SEMICONDUCTOR CORPORATION INFINEON RF MICRO DEVICES, INC. INNOVATOR ELECTRONIC SHENZHEN CO., LTD RICHTEK TECHNOLOGY CORP. ROHM CORPORATION SAMSUNG DISPLAY SAMSUNG ELECTRONICS SAMSUNG SDI SAMSUNG SEMICONDUCTOR SEAGATE SHEN ZHEN JIA AI MOTOR CO., LTD. SHENZHEN HORN AUDIO CO., LTD. SHINKO ELECTRIC INDUSTRIES CO., LTD. STARLITE PRINTER, LTD. STMICROELECTRONICS SUNG WEI SUNUNION ENVIRONMENTAL PACKAGING CO., LTD TDK TE CONNECTIVITY TEXAS INSTRUMENTS TOSHIBA TPK TOUCH SOLUTIONS, INC. UNIMICRON TECHNOLOGY CORP. UNIPLAS (SHANGHAI) CO., LTD. UNISTEEL UNIVERSAL ELECTRONICS INCORPORATED VOLEX WACOM CO., LTD. WELL SHIN TECHNOLOGY WINBOND WOLFSON MICROELECTRONICS, LTD. X-CON ELECTRONICS, LTD. YUE WAH CIRCUITS CO., LTD. -

A Playbook for Place Leaders

April 2021 Hubs of Innovation A Playbook for Place Leaders Connec ted Places 2 Hubs of Innovation: A Playbook for Place Leaders Hubs of Innovation: A Playbook for Place Leaders 3 The UK is now home to a smorgasbord of more than 100 established and aspiring hubs of innovation. Some of the world’s finest research and technology has clustered in a relatively small number of locations, often without strong place-intentional efforts to Executive Summary amplify the collaboration benefits. Meanwhile several vanguard places have begun their The Innovation Economy after Covid-19 journey towards becoming (once again) a genuine hub of innovation and optimising innovation’s economic and social returns. Many others are aware of the potential but have not yet been supported to truly assess the value or Innovation will be at the forefront of the UK’s strategy viability of embedding innovation in place. for competitiveness through the 2020s. Innovation The UK is now attempting an ambitious feat happens in places. This paper is about the pathfinding - to expand and redistribute its innovation journeys that places pursue in order to host and deliver economy rapidly across a large number of hub locations, sectors and institutions. This the kind of innovation that can underpin national ambition – in a post-pandemic context which demands an inclusive recovery – relies on productivity and local well-being. more consciously joined up and sequenced approaches. There is a widely perceived need to share learning and scale insight among more For centuries innovation places have been Yet in the UK these bonds between place and places – be they city centres seeing a chance central to the UK’s economic story and success. -

Discrete Semiconductor Products Fairchild@50

Fairchild Oral History Panel: Discrete Semiconductor Products Fairchild@50 (Panel Session # 3) Participants: Jim Diller Bill Elder Uli Hegel Bill Kirkham Moderated by: George Wells Recorded: October 5, 2007 Mountain View, California CHM Reference number: X4208.2008 © 2007 Computer History Museum Fairchild Semiconductor: Discrete Products George Wells: My name's George Wells. I came to Fairchild in 1969, right in the midst of the Hogan's Heroes, shall we say, subculture, at the time. It was difficult to be in that environment as a bystander, as someone watching a play unfold. It was a difficult time, but we got through that. I came to San Rafael, Wilf asked me to get my ass up to San Rafael and turn it around or shut it down. So I was up in San Rafael for a while, and then I made my way through various different divisions, collecting about 15 of them by the time I was finished. I ended up as executive vice president, working for Wilf, and left the company about a year and a half after the Schlumberger debacle. That's it in a nutshell. Let me just turn over now to Uli Hegel, who was with Fairchild for 38 years, one of the longest serving members, I believe, in the room. Maybe the longest serving member. Uli, why don't you tell us what you did when you came, when you came and what jobs you had when you were there. Uli Hegel: I came to Fairchild in 1959, September 9, and hired into R&D as a forerunner to the preproduction days. -

Occam User Group

for all users of occam and the transputer N912 January 1990 Contents EDITORIAL 2 Contributions to the newsletter 3 Occam user group publications 3 North American transputer users group publications 4 FORTHCOMING 4 Twelfth occam user group technical meeting 4 North American transputer users group spring meeting 5 Third Japanese transputer/ occam international conference 5 Thirteenth occam user group technical meeting 6 North American transputer users group fall meeting 6 Transputing 1991 7 REPORTS 9 Inaugural meeting of the occam user group: Latin America 9 Eleventh occam user group technical meeting 10 Why did the transputer cross The Pond? 14 Second seminar of the Swedish transputer user group 15 continued on back cover Meiko In-Sun Computing Surface Hardware (see page 98) occam is a trade mark of the INMOS Group of Companies 2 occam user group newsletteT EDITORIAL ~ ~ New groups seem to be springing up all around the world; this issue of nan the newsletter carries contact addresses for the first time for groups in U:E ~ Sweden and Latin America. We have contributions from as far afield as Brazil, the Basque country, and Bristol. It is all here: from exotic hardware (see for example pages 19, 82, 98 and many of the product announcements) to expressions of concern that software should be as unexciting as possible (see pages 22, 27). I would particularly like to draw your attention to the initiative to promote the occam language (see page 84); and to the CODE system from C-DAC (see pages 86 and18), an impromptu presentation of which stole the show in the exhibition at the OUG technical meeting in Edinburgh. -

Fairchild Singapore Story

The Fairchild Singapore Story 1968 - 1987 “Fairchild Singapore Pte Ltd started in 1968. In 1987, it was acquired by National Semiconductor and ceased to exist. The National Semiconductor site at Lower Delta was shutdown and operations were moved to the former Fairchild site at Lorong 3, Toa Payoh. This book is an attempt to weave the hundreds of individual stories from former Fairchild employees into a coherent whole.” 1 IMPORTANT NOTE This is a draft. The final may look significantly different. Your views are welcome on how we can do better. 2 CONTENTS WHAT THIS BOOK IS ABOUT FOREWORD ?? ACKNOWLEDGEMENTS INTRODUCTION How Fairchild Singapore Came About CHAPTER 1 The Managing Directors CHAPTER 2 Official Opening 1969 CHAPTER 3 1975: Official Opening of Factory Two CHAPTER 4 1977 - 79: Bruce’s Leadership CHAPTER 5 1979: A Schlumberger Company 3 CHAPTER 6 1986: Sold to Fujitsu CHAPTER 7 1987: Sold to National Semiconductor CHAPTER 8 Birth of the Semiconductor Industry in Singapore CHAPTER 9 Aerospace & Defence Division CHAPTER 10 Memory & High Speed Logic Division CHAPTER 11 Digital Integrated Circuit Division CHAPTER 12 Design Centre CHAPTER 13 The Ceramic Division CHAPTER 14 The Quality & Reliability Division CHAPTER 15 The Mil-Aero Division CHAPTER 16 The Standard Ceramic Division CHAPTER 17 The Plastic Leaded Chip Carrier Division 4 CHAPTER 18 Retrenchments CHAPTER 19 The Expats CHAPTER 20 Personnel Department CHAPTER 21 IT Group CHAPTER 22 Life After Fairchild APPENDICES _______________________ ?? INDEX 5 What this Book is About “Fairchild Singapore plant together with other multinational corporations in Singapore have allowed the country to move from Third World to First within one generation” ingapore’s first generation of leaders did what was good for the country. -

Fairchild Symbol Computer

Anecdotes Fairchild Symbol Computer Stanley Mazor IEEE, Sr. Member Editor: Anne Fitzpatrick In 1965, Gordon Moore of Fairchild Semiconductor As it happened, Gordon Moore’s R&D computer published what is known as Moore’s law: his observation development group wanted a practicing programmer to and prediction about the growing density of IC chips, and join their staff, so I transferred to R&D in 1966.13 Our the precursor to large-scale integration.1 Moore’s predic- project team developed a new language, Symbol, and the tions about LSI chips raised questions about how complex hardware for directly executing it. The Symbol computer chips would be designed and used.2–6 As the Fairchild overcame the data handling problems that I’d encoun- R&D director, he initiated several research projects tered with the sales order entry software. At the expense addressing the following LSI design and use issues: of extra hardware, the Symbol computer removed ‘‘artifacts’’—introduced to improve execution speed— N computer-aided design tools (CAD) for LSI chips of conventional computing languages. Undesirable N cellular logic chips using standard cells programming artifacts, for example, included static data N gate array logic chips types and type declaration. N packaging for LSI chips N semiconductor memory chips Computer design project N computer design with LSI chips One of Moore’s R&D groups, Digital Systems Research (see Figure 1) under the direction of Rex Rice, focused on As testimony to Moore’s vision, most of these Fairchild chip and system packaging. This group had developed projects subsequently spawned new industries and the original Dual In-line Package (DIP). -

FAN6100Q Secondary-Side Constant Voltage and Constant Current Controller Compatible with Qualcomm® Quick Charge 2.0

Is Now Part of To learn more about ON Semiconductor, please visit our website at www.onsemi.com ON Semiconductor and the ON Semiconductor logo are trademarks of Semiconductor Components Industries, LLC dba ON Semiconductor or its subsidiaries in the United States and/or other countries. ON Semiconductor owns the rights to a number of patents, trademarks, copyrights, trade secrets, and other intellectual property. A listing of ON Semiconductor’s product/patent coverage may be accessed at www.onsemi.com/site/pdf/Patent-Marking.pdf. ON Semiconductor reserves the right to make changes without further notice to any products herein. ON Semiconductor makes no warranty, representation or guarantee regarding the suitability of its products for any particular purpose, nor does ON Semiconductor assume any liability arising out of the application or use of any product or circuit, and specifically disclaims any and all liability, including without limitation special, consequential or incidental damages. Buyer is responsible for its products and applications using ON Semiconductor products, including compliance with all laws, regulations and safety requirements or standards, regardless of any support or applications information provided by ON Semiconductor. “Typical” parameters which may be provided in ON Semiconductor data sheets and/or specifications can and do vary in different applications and actual performance may vary over time. All operating parameters, including “Typicals” must be validated for each customer application by customer’s technical experts. ON Semiconductor does not convey any license under its patent rights nor the rights of others. ON Semiconductor products are not designed, intended, or authorized for use as a critical component in life support systems or any FDA Class 3 medical devices or medical devices with a same or similar classification in a foreign jurisdiction or any devices intended for implantation in the human body. -

Indigenous Circuits: Navajo Women and the Racialization of Early Electronic Manufacture

Indigenous Circuits: Navajo Women and the Racialization of Early Electronic Manufacture Lisa Nakamura American Quarterly, Volume 66, Number 4, December 2014, pp. 919-941 (Article) Published by Johns Hopkins University Press DOI: https://doi.org/10.1353/aq.2014.0070 For additional information about this article https://muse.jhu.edu/article/563663 Access provided by Georgia Institute of Technology (4 Aug 2017 15:02 GMT) Indigenous Circuits | 919 Indigenous Circuits: Navajo Women and the Racialization of Early Electronic Manufacture Lisa Nakamura onna Haraway’s foundational cyberfeminist essay “A Cyborg Mani- festo” is followed by an evocative subtitle: “An Ironic Dream of a DCommon Language for Women in the Integrated Circuit.” She writes, “The nimble fingers of ‘Oriental’ women, the old fascination of little Anglo-Saxon Victorian girls with doll’s houses, women’s enforced attention to the small take on quite new dimensions in this world. There might be a cyborg Alice taking account of these new dimensions. Ironically, it might be the un- natural cyborg women making chips in Asia and spiral dancing in Santa Rita jail whose constructed unities will guide effective oppositional strategies.”1 In this passage Haraway draws our attention to the irony that some must labor invisibly for others of us to feel, if not actually be, free and empowered through technology use: technoscience is, indeed, an integrated circuit, one that both separates and connects laborers and users, and while both genders benefit from cheap computers, it is the flexible labor of women of color, either outsourced or insourced, that made and continue to make this possible.2 Haraway’s critical perspective on digital technology’s possibilities and op- portunities for intersectional feminism expresses itself in this essay by standing readerly expectation on its head. -

DE TECH SECTOR in HET VK Opportuniteiten En Clusters Oktober 2017

DE TECH SECTOR IN HET VERENIGD KONINKRIJK FLANDERS INVESTMENT & TRADE MARKTSTUDIE Paper /////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// DE TECH SECTOR IN HET VK Opportuniteiten en clusters Oktober 2017 //////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// www.flandersinvestmentandtrade.com INHOUD 1. Inleiding ............................................................................................................................................................................................. 3 2. Beknopt overzicht ...................................................................................................................................................................... 4 3. Opportuniteiten per regio: clusters ................................................................................................................................ 4 3.1 Engeland 4 3.1.1 Londen 4 3.1.2 Manchester 5 3.1.3 Oxford & Reading 6 3.1.4 Liverpool 7 3.1.5 Birmingham 8 3.1.6 Cambridge 9 3.1.7 Exeter 9 3.1.8 Bristol & Bath 10 3.1.9 Bournemouth & Poole 10 3.1.10 Brighton 12 3.2 Schotland 13 3.2.1 Edinburgh 13 3.2.2 Glasgow 14 3.2.3 Dundee 14 3.3 Noord-Ierland 15 3.3.1 Belfast 15 3.4 Wales 16 3.4.1 Cardiff & Swansea 16 4. Interessante bronnen ..............................................................................................................................................................17