Annual Report 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

8347 Interserve AR 2011 Introduction 4 Ifc-P1 Tp.Indd

Interserve Plc 2011 Annual Report and Financial Statements Interserve Plc Every day, we’re planning, creating and managing the world around you. 2011 Annual Report and Financial2011 Statements INTERSERVE ANNUAL REPORT 2011 OVERVIEW HIGHLIGHTS Across the world, people wake to a new day. We help make it a great day. PROUD OF THE Every day people wake to put We help build and look after this their plans, dreams and goals world and we do this through the VALUE WE CREATE IN into action. lasting relationships our people have built with a range of partners PLANNING, CREATING, To make this happen they need the and clients worldwide to ensure we places around them – their schools, AND MANAGING THE create value for everyone involved. their workplace, hospitals, shops WORLD AROUND YOU and infrastructure – to function well, to support, inspire and add value to their lives. FINANCIAL HIGHLIGHTS HEADLINE EPS* PROFIT BEFORE TAX FULL-YEAR DIVIDEND 49.3p £ 67.1m 19.0p + 15% + 5% + 6% VIEW 2011 ANNUAL REPORT ONLINE: HTTP://AR2011.INTERSERVE.COM INTERSERVE ANNUAL REPORT 2011 OVERVIEW HIGHLIGHTS Across the world, people wake to a new day. We help make it a great day. PROUD OF THE Every day people wake to put We help build and look after this their plans, dreams and goals world and we do this through the VALUE WE CREATE IN into action. lasting relationships our people have built with a range of partners PLANNING, CREATING, To make this happen they need the and clients worldwide to ensure we places around them – their schools, AND MANAGING THE create value for everyone involved. -

ITE – a First for Singapore and Bbcap the Transform Grand Prix Spotlight On… Submissions WELCOME & UPDATE

SPRING 2008 THE QUARTERLY MAGAZINE OF BALFOUR BEATTY CAPITAL IN THIS EDITION ITE – a fIRST FOR SiNGAPORE AND BBCAP The Transform Grand Prix Spotlight on… submissions WELCOME & UPDATE Welcome to the Spring edition of capital Q. The year has got off to a good start. In new business bids for Southwark, Derbyshire Schools and Enniskillen Hospital have been submitted and work continues towards achieving financial close on Islington, Fife and CNDR. Decisions are also pending for the M80 and M25 and we hope to hear on these soon. It has been an exciting time internationally with the purchase of GMH Win America, prequalification on the Etoile Project in France, and in Singapore work has started on the ground at ITE. A fantastic effort was made by the “Hard Way Up Club” who tackled the physically and mentally demanding challenge of the Haute Route. Money is still coming in but at the time of going to press, the team had raised over £14,000 for NCH. Well done to all involved. It has been an exciting time internationally SPRING 2008 with the purchase of GMH in America... THE QUARTERLY MAGAZINE OF BALFOUR BEATTY CAPITAL IN THIS EDITION 4-7 News review Learning and development remains a high priority for us all and I ITE – a first for Singapore and BBCap would ask that you make the most of the performance development Elsewhere in the world... reviews that are coming up in May. In addition Capital College is a Six word memoirs fantastic resource and new courses are being added all the time. -

Interserve Modern Slavery Statement

Interserve Modern Slavery statement We have a workforce of c 45,000 in the UK, c5,000 in our overseas subsidiaries and c22,000 in our Middle East associate companies, delivering construction, support services, and frontline services covering a range of sectors, worldwide.1 In addition to our directly employed workforce there are many people employed in our supply chain. Our values and our culture guide us to operate ethically and transparently. Consequently, we are committed to ensuring that Modern Slavery2 does not exist in our workforce or our supply chain. This statement should be read in conjunction with our Human Rights policy, http://www.interserve.com/docs/default-source/about/policies/human-rights-policy.pdf and with the policies and the supplier codes of conduct of our operating companies which state our position on human rights and the ethical standards we set for our own business activities and expect of our supply chain. Our whistle blowing policy and procedures http://www.interserve.com/docs/defaultsource/about/policies/whistle-blowing- policy.pdf?sfvrsn=14 provide clear guidance for our own employees and those employed in our supply chain on what to do should they suspect modern slavery is taking place. The main Modern Slavery risk within our subsidiaries’ operations stems from bringing workers employed by other companies on to our own or our customers’ sites, particularly agency workers. There are also potential risks in our supply chain in relation to goods and services at tiers 1 and below. Our suppliers and sub-contractors are required to comply with our business practices and ethical supply policies and our site induction processes extend to sub-contractors’ workers operating on our sites. -

Langdon Innovates in Tight Budget with Procure21 Procure21 Used to Get Medium-Secure Mental Health Build up and Running While Saving on a Tight Budget

Room The design specification Operating development policy process Supplier Literature/ development research review + Repeatable Standardisation ProCure21 provides Post-project 4 Evidence 9 room evaluation matrix design of components and room “open-book” ethos at designs saves money Barrow-in-Furness mental for NHS Trusts health facility Patient Implemen– focus tation group Clinical Previous review scheme designs Peer review FOLLOW US ON TWITTER @DHP21PLUS Langdon innovates in tight budget with ProCure21 ProCure21 used to get medium-secure mental health build up and running while saving on a tight budget April saw the completion of approved by the local Strategic Langdon Hospital’s men-only Health Authority with a budget medium-secure mental health of £45m – but Devon Partnership facility, a 60-bed unit replacing NHS Foundation Trust felt this was a smaller facility that had become unaffordable. Instead, ProCure21 was unfit for purpose. The new facility employed to bring the entire project includes extensive therapy facilities, within budget constraints. with a computer lab, art and music therapy rooms, a gym, shop, café and Although Trust project director Jim library, and is situated on a 110-acre Masters had some experience of the above Main entrance at site with an external sports barn and framework, project manager Craig Langdon Hospital’s men- multi-use games area. The original O’Dwyer was new to it, and the Trust only medium-secure mental project was a PFI new-build, officially health unit right An external courtyard continued on -

Completed Acquisition by Interserve Plc of the Facilities Management Business of Rentokil Initial Plc (Initial Facilities)

Completed acquisition by Interserve plc of the facilities management business of Rentokil Initial plc (Initial Facilities) ME/6432-14 The CMA’s decision on clearance under section 33(1) given on 29 May 2014. Full text of the decision published on 11 June 2014. Please note that the square brackets indicate figures or text which have been deleted or replaced in ranges at the request of the parties for reasons of commercial confidentiality. Summary 1. On 18 March 2014, Interserve plc (Interserve) acquired the facilities management (FM) business (Initial Facilities) of Rentokil Initial plc (Rentokil) through the purchase of a combination of shares and assets. The Competition and Markets Authority (CMA) considers that the parties have ceased to be distinct and that the turnover test in section 23(1)(b) of the Enterprise Act 2002 (the Act) is met. The CMA therefore believes that it is or may be the case that a relevant merger situation has been created. 2. The parties notified the completed merger to the Office of Fair Trading (OFT)1 on 31 March 2014. The administrative deadline for the CMA to make a decision on whether or not to refer the merger to a phase II investigation is 29 May 2014. 3. The parties overlapped in the provision of FM services in the UK. The CMA analysed the effects of the merger on the provision of FM services in the UK as a whole, and also taking into account the information received by it on how competition varies across certain segments and geographies. 1 The Competition and Markets Authority (CMA) was established on 1 October 2013. -

Housing Regeneration Projects

Briefing Paper to the Riverside Area Committee Wards: Newington and Gypsyville, 10 June 2020 St Andrews and Docklands, Drypool Riverside Regeneration Projects Briefing Paper of the Assistant City Manager, Housing Strategy and Renewal 1. Purpose of the Paper and Summary The purpose of this briefing paper is to update Members of Riverside Area Committee on the regeneration projects delivered by Housing Strategy and Renewal. 2. Background 2.1 Housing regeneration activities across the city are focused in the Council’s priority renewal areas. These areas include Newington and St Andrew’s, the Holderness Road Corridor, Orchard Park and North Bransholme. 2.2 This briefing paper outlines the progress made within the Riverside area, including an update on developments currently on site and new programmes being brought forward as a result of successful funding bids. The report also summarises the approach being taken by the Housing Strategy and Renewal section to secure additional funding and build upon the progress made to date. 3. Issues for Consideration Newington & St Andrew’s – Hawthorn Avenue Regional Growth Fund Acquisition Programme 3.12 All properties are now in Council ownership following acquisition by General Vesting Declaration. Demolition Programme 3.13 All properties have now been demolished and land assembly for the redevelopment of Hawthorn East is now complete. Access to the land via Pretoria and Seymour Street has now been secured and the land will be maintained until transferred to the developer. Local Labour 3.14 The figures for Q2 2019 / 20 for the whole of the West Hull development show that Keepmoat are achieving 71% HU based labour which is a 14% decrease on the previous quarter. -

Report: Extension of the Mitie (Interserve) Facilities Contract , Item

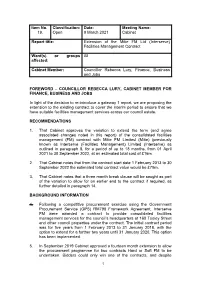

Item No. Classification: Date: Meeting Name: 19. Open 9 March 2021 Cabinet Report title: Extension of the Mitie FM Ltd (Interserve) Facilities Management Contract Ward(s) or groups All affected: Cabinet Member: Councillor Rebecca Lury, Finance, Business and Jobs FOREWORD – COUNCILLOR REBECCA LURY, CABINET MEMBER FOR FINANCE, BUSINESS AND JOBS In light of the decision to re-introduce a gateway 1 report, we are proposing the extension to the existing contract to cover the interim period to ensure that we have suitable facilities management services across our council estate. RECOMMENDATIONS 1. That Cabinet approves the variation to extend the term (and agree associated changes noted in this report) of the consolidated facilities management (FM) contract with Mitie FM Limited (Mitie) (previously known as Interserve (Facilities Management) Limited (Interserve) as outlined in paragraph 8, for a period of up to 18 months, from 01 April 2021 to 30 September 2022, at an estimated total cost of £16m. 2. That Cabinet notes that from the contract start date 1 February 2013 to 30 September 2022 the estimated total contract value would be £79m. 3. That Cabinet notes that a three month break clause will be sought as part of the variation to allow for an earlier end to the contract if required, as further detailed in paragraph 14. BACKGROUND INFORMATION 4. Following a competitive procurement exercise using the Government Procurement Service (GPS) RM798 Framework Agreement, Interserve FM were awarded a contract to provide consolidated facilities management services for the council’s headquarters at 160 Tooley Street and other council properties under the contract. -

Suppliers Recognised at Agency Awards

14 HIGHWAYS AGENCY JAN/FEB 2015 www.highways.gov.uk Suppliers recognised at Agency awards The Highways Agency has saluted the suppliers making a difference on national roads – and calls for more as it moves towards being a government-owned company Small and medium-sized enterprises, partnership with Recycling Lives which innovation, and customer and led to two homeless people securing worker care all emerged as employment placements. But there was winners as the Highways Agency still room for the first tier suppliers as Costain won three awards – including announced the results of its Supplier one in ‘Customer experience’ for its Recognition Scheme. work on the M1 junction 28-31 smart The awards for 2014, which were motorway scheme. The company announced in Birmingham in January, had implemented measures including saw small and medium-sized enterprises an ANPR system to give drivers live (SMEs) make their mark by picking up a journey time information as they travel quarter of the honours. through roadworks. The Agency was already celebrating Interserve Construction won the a record number of entries across the ‘Delivering sustainable value and seven categories – with 118 flooding in solutions’ category for its beyond from 50 companies. 2020 sustainability framework; while The annual recognition scheme Carillion impressed judges for its highlights the vital contribution made customer service solutions on the A23 by the Agency’s suppliers who help Handcross to Warninglid scheme. There it operate, maintain and improve the company not only made public England’s network of motorways and liaison available 24/7 for any complaints A roads. In fact more than 90 per cent or queries, it also visited schools for of the work delivered on Agency roads educational talks, raised funds for local is down to the supply chain. -

Business Name D/B/A Name #1A LIFESAFER of COLORADO LLC

Business Name D/B/A Name #1A LIFESAFER OF COLORADO LLC 101 PARK AVENUE PARTNERS INC 1-800 CONTACTS INC 3 DAY BLINDS LLC 303 FURNITURE INC 303 TACTICAL LLC 303 TACTICAL 360 RAIL SERVICES LLC 3BB INC GREAT CLIPS 3D AUTOGLASS 3D STAINLESS LLC 3FORM LLC 3R Technology Solutions Inc 3SI SECURITY SYSTEMS INC 3T CULINARY INC THREE TOMATOES CATERING 4 FRONT ENGINEERED SOL INC 4283929 DELAWARE LLC ROCKY MTN PET CREMATION SERVICES 48FORTY SOLUTIONS LLC PALLET COMPANIES LLC 4imprint, Inc. 4LIFE RESEARCH CSA LLC 4LIFE RESEARCH USA LLC 50 IN 52 JOURNEY INC THE JOURNEY INSTITUTE 5071 INC 50-80 MASSAGE 5280 Contract Flooring 5280 HEATING COOLING & REFRIGERATION 5280 MAINTENANCE INC 5280 Stone Company, LLC 5280 Stone Company, LLC 5280 Telecom, LLC 5280 TOWING LLC 52Eighty Customs 5850 EAST 58TH AVENUE LLC 5850 EAST 58TH AVENUE LLC 6 ITALIAN WOLF SECURITY LLC 6171 LLC THE HIDEAWAY TAVERN 7-ELEVEN INC 7-ELEVEN STORE #38170 7-ELEVEN INC 7-ELEVEN STORE 37570 7-ELEVEN INC / JC INC 35828A 7-ELEVEN STORE 35828A 7-ELEVEN INC 23829 7-ELEVEN STORE 23829 7-ELEVEN INC 23829B 7-ELEVEN STORE 23829B 7-ELEVEN INC 34087 7-ELEVEN STORE 34087 7-ELEVEN INC 35828 7-ELEVEN STORE 35828 7-ELEVEN INC 35864 7-ELEVEN STORE 35864 7-ELEVEN INC 36013 7-ELEVEN STORE 36013 7-ELEVEN INC 36013 7-ELEVEN STORE 36013 7-ELEVEN INC 36464 7-ELEVEN STORE 36464 7-ELEVEN INC 36775 7-ELEVEN STORE 36775 7-ELEVEN INC 37291 7-ELEVEN STORE 37291 7-ELEVEN STORE 34087A 7-ELEVEN INC / S&As STORE INC 34087A 7-ELEVEN STORE 36013A EMHT INC & 7-ELEVEN INC 800-FLOWERS INC 8X8 INC A & A QUALITY APPLIANCE A & B Engineering Services LLC A CUSTOM COACH A CUT ABOVE LANDSCAPE LLC A GOOD LIL TRANNY SHOP LLC A GOOD SHOP INC A HOLE IN THE WALL CONSTRUCTIO AHW CONSTRUCTION A MAN WITH A VAN INC A SIMPLEE GORGEOUS BOUTIQUE A TO Z RENTAL CENTER, INC. -

The-End-Of-Privatisation

THE END OF PRIVATISATION David Boyle is a writer and think-tanker, co-director of the New Weather Institute, and has been at the heart of the effort to develop co-production and introduce time banks to Britain as a critical element of public service reform. He was the government’s independent reviewer on Barriers to Public Service Choice (2012-13). He is the author of The Tyranny of Numbers (2001). He also writes history books. Lindsay Mackie is chair of the New Weather Institute. She is a writer and campaigner who worked as a journalist on the Guardian and has run a number of campaigning charities. Andrew Simms is an author, political economist and campaigner. He is co-director of the New Weather Institute, co-ordinator of the Rapid Transition Alliance, a research associate at the University of Sussex, and a fellow of the New Economics Foundation. His books include Tescopoly, Cancel the Apocalypse, Ecological Debt, and Economics: A Crash Course. The End of Privatisation Profit in the time of covid New Weather pamphlet #3 David Boyle, Lindsay Mackie and Andrew Simms NEW WEATHER INSTITUTE/THE REAL PRESS www.newweather.org/www.therealpress.co.uk Published in 2020 by the Real Press and the New Weather Institute, www.newweather.org www.therealpress.co.uk © New Weather CIC The moral right of David Boyle and Lindsay Mackie to be identified as the author of this work has been asserted in accordance with the Copyright, Designs and Patents Acts of 1988. Some rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical or photocopying, recording, or otherwise for commercial purposes without the prior permission of the publisher. -

Climate Action Group Meeting Thursday 18Th May 2021, Online Date

Climate Action Group Meeting Thursday 18th May 2021, online Date: Thursday 18th March 2021, online Attendees: Martin Gettings (Canary Wharf Group) James Cadman (Action Sustainability), Stefania Chica-Jacome (Action Sustainability), Tony Vozniak (Ardent Hire), Sarah-Jane Davies (Sisk), Lucy Neville (Transport for London), William McDowell (Brett Martin), Scott Gregory (Morgan Sindall), Michelle McAteer (Balfour Beatty), Katherine Rusack (Balfour Beatty), James Geraghty (Kier), Jamie Bursnell (Bellway Homes), Stephen Weldon (Bellway Homes), Anna Shillitoe (CHAS), Jonathan Ayton (Willmott Dixon), Amy Twist (Countryside Properties), Maria Gkonou (Redrow Homes), Sila Danik Dirihan (Saint Gobain), Sarah Burki (Interserve), Oana Caltia (Kilnbridge), Natalie Wilkinson (NG Bailey), Rebecca Segal (NG Bailey), Stewart Jones (Hanson Biz), Gigi Kvashilava (Hanson Biz), Kirsty Dunne (Osborne), Gemma Tovey (Lovell Partnership) Summary of Actions and Notes from the Climate Action Group Meeting Climate Action Group – Introductions and outstanding actions No Action/Notes Owner 1 Welcome and Intros Martin Gettings & James Cadman 2 Update on Progress: engagement and tool use, support available. We gave an overview of where we are now in terms of engagement. Stefania Chica- • There are 197 participating companies between partners and Jacome suppliers: 32% are Partner organizations and the remaining 68% are suppliers. • Partner organisations: 56% are actively engaging with the group. This is a 3% increase versus the last group meeting in March 2021. • Supplier organisations: 55% are actively engaging. • School continues to provide monthly webinars to support suppliers. Next session is on the 26th May, please forward invites to suppliers. Partners Contact [email protected] for further details. 3 What’s coming. • E-learning modules: The School will be publishing modules 1 (Climate Change & Carbon) & 2 (Carbon Footprinting and Measurement) on School the website this week. -

Largest Ever Single Span Pedestrian Bridge

UK ISSUE 17 LARGEST EVER SINGLE SPAN PEDESTRIAN BRIDGE ALSO IN THIS ISSUE... TRAPAGARÁN VIADUCT, YAS HOTEL, CARILLION BRIDGE SLIDE, ROYAL VISIT AND TIGER BRENNAN DRIVE www.rmdkwikform.com SUBSCRIBE NOW EXCLUSIVE CONTENT Get the latest stories and features with added exclusive content VIEW OUR VIDEOS See RMD Kwikform’s equipment in action on a range of projects from around the world SUBSCRIBE Subscribe to Formula Online to receive regular updates and get the latest copy of Formula magazine delivered direct to your door BACK ISSUES Read all the news on RMD Kwikform’s past projects by viewing back issues of Formula on your desktop RMD Kwikform TV and Formula Online! RMD Kwikform’s online TV and news portals Visit our TV channel for exciting videos of projects across the globe or read all about our latest stories on Formula Online. +44 (0)1922 743 743 www.rmdkwikform.tv [email protected] www.rmdkwikform.com/formula_online www.rmdkwikform.com EDITOR VIEWPOINT IN THIS ISSUE Welcome to this, the 17th edition of our Formula UK magazine. Since our last edition, RMD Kwikform has been involved in some extremely interesting projects across the UK and the rest of the world, even breaking some of our own longstanding records! ROYAL VISIT 4 In this edition it is great to see that even though the UK and global construction industry has and continues to have a challenging time, our innovative engineering solutions and programme time saving systems are making a significant contribution to a whole range of projects. TRAPAGARÁN VIADUCT 6 With our attendance at the Infrastructure show at the NEC on the 18th-20th October 2010 now booked, we have taken the opportunity in this edition to highlight some interesting infrastructure projects.