Functional Specification for Payments Corporate Egateway

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

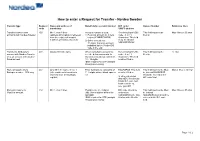

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Chronology, 1963–89

Chronology, 1963–89 This chronology covers key political and economic developments in the quarter century that saw the transformation of the Euromarkets into the world’s foremost financial markets. It also identifies milestones in the evolu- tion of Orion; transactions mentioned are those which were the first or the largest of their type or otherwise noteworthy. The tables and graphs present key financial and economic data of the era. Details of Orion’s financial his- tory are to be found in Appendix IV. Abbreviations: Chase (Chase Manhattan Bank), Royal (Royal Bank of Canada), NatPro (National Provincial Bank), Westminster (Westminster Bank), NatWest (National Westminster Bank), WestLB (Westdeutsche Landesbank Girozentrale), Mitsubishi (Mitsubishi Bank) and Orion (for Orion Bank, Orion Termbank, Orion Royal Bank and subsidiaries). Under Orion financings: ‘loans’ are syndicated loans, NIFs, RUFs etc.; ‘bonds’ are public issues, private placements, FRNs, FRCDs and other secu- rities, lead managed, co-managed, managed or advised by Orion. New loan transactions and new bond transactions are intended to show the range of Orion’s client base and refer to clients not previously mentioned. The word ‘subsequently’ in brackets indicates subsequent transactions of the same type and for the same client. Transaction amounts expressed in US dollars some- times include non-dollar transactions, converted at the prevailing rates of exchange. 1963 Global events Feb Canadian Conservative government falls. Apr Lester Pearson Premier. Mar China and Pakistan settle border dispute. May Jomo Kenyatta Premier of Kenya. Organization of African Unity formed, after widespread decolonization. Jun Election of Pope Paul VI. Aug Test Ban Take Your Partners Treaty. -

Svenska Handelsbanken AB

OFFERING CIRCULAR Svenska Handelsbanken AB (publ) (Incorporated as a public limited liability banking company in The Kingdom of Sweden) U.S.$50,000,000,000 Euro Medium Term Note Programme for the issue of Notes with a minimum maturity of one month On 26th June, 1992 Svenska Handelsbanken AB (publ) (the “Issuer” or the “Bank”) entered into a U.S.$1,500,000,000 Euro Medium Term Note Programme (the “Programme”) and issued an offering circular on that date describing the Programme. This Offering Circular supersedes any previous offering circular and supplements therein prepared in connection with the Programme. Any Notes (as defined below) issued under the Programme on or after the date of this Offering Circular are issued subject to the provisions described herein. This does not affect any Notes already in issue. Under the Programme, the Bank may from time to time issue Notes (the “Notes”), which expression shall include Notes (i) issued on a senior preferred basis as described in Condition 3 (“Senior Preferred Notes”), (ii) issued on a senior non-preferred basis as described in Condition 4 (“Senior Non-Preferred Notes”), (iii) issued on a subordinated basis and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 5 (“Subordinated Notes”) and (iv) issued on a subordinated basis with no fixed maturity and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 6 (“Additional Tier 1 Notes”). The Outstanding Principal Amount (as defined in Condition 2) of each Series (as defined below) of Additional Tier 1 Notes will be subject to Write Down (as defined in Condition 2) if the Common Equity Tier 1 Capital Ratio (as defined in Condition 2) of the Bank and/or the Handelsbanken Group (as defined Condition 2) is less than the relevant Trigger Level (as defined in Condition 2). -

Nordea Group Annual Report 2018

Annual Report 2018 CEO Letter Casper von Koskull, President and Group CEO, and Torsten Hagen Jrgensen, Group COO and Deputy CEO. Page 4 4 Best and most accessible advisory, with an 21 easy daily banking experience, delivered at scale. Page 13 Wholesale Banking No.1 relationship Asset & Wealth bank in the Nordics Management with operational Personal Banking 13 excellence. Page 21 Commercial & Business Banking Our vision is to become the lead- ing Asset & Wealth Manager in the 25 Nordic market by 2020. Page 25 Best-in-class advisory and digital experience, 17 ef ciency and scale with future capabilities in a disruptive market. Page 17 Annual Report 2018 Contents 4 CEO letter 6 Leading platform 10 Nordea investment case – strategic priorities 12 Business Areas 35 Our people Board of Directors’ report 37 The Nordea share and ratings 40 Financial Review 2018 46 Business area results 49 Risk, liquidity and capital management 67 Corporate Governance Statement 2018 76 Non-Financial Statement 78 Conflict of interest policy 79 Remuneration 83 Proposed distribution of earnings Financial statements 84 Financial Statements, Nordea Group 96 Notes to Group fi nancial statements 184 Financial statements Parent company 193 Notes to Parent company fi nancial statements 255 Signing of the Annual Report 256 Auditor’s report Capital adequacy 262 Capital adequacy for the Nordea Group 274 Capital adequacy for the Nordea Parent company Organisation 286 Board of Directors 288 Group Executive Management 290 Main legal structure & Group organisation 292 Annual General Meeting & Financial calendar This Annual Report contains forward-looking statements macro economic development, (ii) change in the competitive that reflect management’s current views with respect to climate, (iii) change in the regulatory environment and other certain future events and potential fi nancial performance. -

Interim Report January – September 2020 Q3

Interim Report January – September 2020 Q3 Financial summary Third quarter First nine months • Net sales amounted to EUR 27k (0) • Net sales amounted to EUR 126k (21k) • Operating loss (EBIT) increased to EUR 4,790k • Operating loss (EBIT) increased to EUR 7,291k (748k) driven by listing costs (3,490k) driven by listing costs • Loss after tax amounted to EUR 4,730k (815k) • Loss after tax amounted to EUR 7,127k (3,602k) • Basic and diluted loss per Class A share amounted to EUR 0.10 (0.02) • Basic and diluted loss per Class A share amounted to EUR 0.16 (0.08) • Liquid funds as at end of the period amounted to EUR 90.5m • Cash flow from operating activities amounted to EUR -1,824k (-3,014k) • No interest-bearing debt at end of the period Figures within parentheses refer to the preceding year. Significant events • Enlisted Inselspital Bern, the largest In the third quarter of 2020 university hospital in Switzerland, to be the lead hospital in our upcoming RefluxStop™ • Completed listing on Nasdaq First North Premier Growth Market raising SEK 1.1 Registry clinical trial to be focused primarily billion, with trading of Implantica's Swedish in Germany and Switzerland. Depository Receipts commencing on September 21, 2020. The offering was After the end of the period substantially oversubscribed. • Exercised overallotment option raising an additional SEK 165 million. • Increased our shareholder base with highly reputable shareholders such as Swedbank • Implantica’s RefluxStop™ trial showed Robur Ny Teknik, Handelsbanken Fonder, exceptional three-year follow-up results. TIN Fonder, Skandia and Nordea Investment None of the 47 patients in the study were in Management. -

Fitch Ratings ING Groep N.V. Ratings Report 2020-10-15

Banks Universal Commercial Banks Netherlands ING Groep N.V. Ratings Foreign Currency Long-Term IDR A+ Short-Term IDR F1 Derivative Counterparty Rating A+(dcr) Viability Rating a+ Key Rating Drivers Support Rating 5 Support Rating Floor NF Robust Company Profile, Solid Capitalisation: ING Groep N.V.’s ratings are supported by its leading franchise in retail and commercial banking in the Benelux region and adequate Sovereign Risk diversification in selected countries. The bank's resilient and diversified business model Long-Term Local- and Foreign- AAA emphasises lending operations with moderate exposure to volatile businesses, and it has a Currency IDRs sound record of earnings generation. The ratings also reflect the group's sound capital ratios Country Ceiling AAA and balanced funding profile. Outlooks Pandemic Stress: ING has enough rating headroom to absorb the deterioration in financial Long-Term Foreign-Currency Negative performance due to the economic fallout from the coronavirus crisis. The Negative Outlook IDR reflects the downside risks to Fitch’s baseline scenario, as pressure on the ratings would Sovereign Long-Term Local- and Negative increase substantially if the downturn is deeper or more prolonged than we currently expect. Foreign-Currency IDRs Asset Quality: The Stage 3 loan ratio remained sound at 2% at end-June 2020 despite the economic disruption generated by the lockdowns in the countries where ING operates. Fitch Applicable Criteria expects higher inflows of impaired loans from 4Q20 as the various support measures mature, driven by SMEs and mid-corporate borrowers and more vulnerable sectors such as oil and gas, Bank Rating Criteria (February 2020) shipping and transportation. -

2019 Annual and Sustainability Report

2019 Annual and Sustainability Report Contents Swedbank in brief 2 Income, balance sheet and notes, Group The year in brief 4 Income statement 54 CEO statement 6 Statement of comprehensive income 55 Goals and results 8 Balance sheet 56 Value creation 10 Statement of changes in equity 57 Business model 12 Statement of cash flow 58 Sustainability 14 Notes 59 The share and owners 24 Income, balance sheet and notes, Parent company Board of Directors’ report Income statement 154 Financial analysis 26 Statement of comprehensive income 154 Swedish Banking 30 Balance sheet 155 Baltic Banking 31 Statement of changes in equity 156 Large Corporates & Institutions 32 Statement of cash flow 157 Group Functions & Other 33 Notes 158 Corporate governance report 34 Alternative performance measures 192 Board of Directors 46 Group Executive Committee 50 Sustainability Disposition of earnings 52 Sustainability report 194 Materiality analysis 195 Sustainability management 197 Notes 199 GRI Standards Index 212 Signatures of the Board of Directors and the CEO 217 Auditors’ report 218 Sustainability report – assurance report 222 Annual General Meeting 223 Market shares 224 Five-year summary – Group 225 Three-year summary – Business segments 228 Definitions 231 Contacts 233 Financial information 2020 Annual General Meeting 2020 Q1 Interim report 23 April The Annual General Meeting will be held on Thursday, 26 March at 11 am (CET) at Cirkus, Djurgårdsslätten Q2 Interim report 17 July 43–45, Stockholm, Sweden. The proposed record day for the dividend is 30 March 2020. The last day for Q3 Interim report 20 October trading in Swedbank’s shares including the right to the dividend is 26 March 2020. -

Swedbank Economic Outlook Is Available At

Completed: January 20, 2021, 06:30 Distributed: January 20, 2021, 07:00 Mattias Persson Global Head of Macro Research and Group Chief Economist [email protected] +46 8 5859 59 74 Andreas Wallström Axel Zetherström Liis Elmik Head of Forecasting Assistant Senior Economist Deputy Head of Macro Research Sweden [email protected] [email protected] andreas.wallströ[email protected] +46 8 5859 57 75 +372 888 72 06 +46 8 700 93 07 Marianna Rõbinskaja Robin Ahlén Øystein Børsum Economist Economist Chief Economist Norway [email protected] [email protected] +372 888 79 25 +46 8 700 93 08 Chief Credit Strategist [email protected] Cathrine Danin +47 91 18 56 35 Senior Economist Līva Zorgenfreija [email protected] Jon Espen Riiser Chief Economist Latvia +46 8 700 92 97 Analyst [email protected] [email protected] +371 6744 58 44 Jana Eklund +47 90 98 17 49 Senior Econometrician Agnese Buceniece [email protected] Marlene Skjellet Granerud Senior Economist +46 8 5859 46 04 Economist [email protected] [email protected] +371 6744 58 75 Knut Hallberg +47 94 30 53 32 Senior Economist Laura Orleāne [email protected] Economist +46 8 700 93 17 [email protected] Heidi Schauman +371 6744 42 13 Pernilla Johansson Chief Economist Finland Senior Economist [email protected] [email protected] +358 503 281 229 +46 40 24 23 31 Nerijus Mačiulis Sonja Liukkonen Deputy Group Chief Economist Maija Kaartinen Junior Economist Chief -

Pa Perspectives on Nordic Financial Services

PA PERSPECTIVES ON NORDIC FINANCIAL SERVICES Autumn Edition 2017 CONTENTS The personal banking market 3 Interview with Jesper Nielsen, Head of Personal Banking at Danske bank Platform thinking 8 Why platform business models represent a double-edged sword for big banks What is a Neobank – really? 11 The term 'neobanking' gains increasing attention in the media – but what is a neobank? Is BankID positioned for the 14future? Interview with Jan Bjerved, CEO of the Norwegian identity scheme BankID The dance around the GAFA 16God Quarterly performance development 18 Latest trends in the Nordics Value map for financial institutions 21 Nordic Q2 2017 financial highlights 22 Factsheet 24 Contact us Chief editors and Nordic financial services experts Knut Erlend Vik Thomas Bjørnstad [email protected] [email protected] +47 913 61 525 +47 917 91 052 Nordic financial services experts Göran Engvall Magnus Krusberg [email protected] [email protected] +46 721 936 109 +46 721 936 110 Martin Tillisch Olaf Kjaer [email protected] [email protected] +45 409 94 642 +45 222 02 362 2 PA PERSPECTIVES ON NORDIC FINANCIAL SERVICES The personal BANKING MARKET We sat down with Jesper Nielsen, Head of Personal Banking at Danske Bank to hear his views on how the personal banking market is developing and what he forsees will be happening over the next few years. AUTHOR: REIAR NESS PA: To start with the personal banking market: losses are at an all time low. As interest rates rise, Banking has historically been a traditional industry, loss rates may change, and have to be watched. -

POSTAL SAVINGS Reaching Everyone in Asia

POSTAL SAVINGS Reaching Everyone in Asia Edited by Naoyuki Yoshino, José Ansón, and Matthias Helble ASIAN DEVELOPMENT BANK INSTITUTE Postal Savings - Reaching Everyone in Asia Edited by Naoyuki Yoshino, José Ansón, and Matthias Helble ASIAN DEVELOPMENT BANK INSTITUTE © 2018 Asian Development Bank Institute All rights reserved. First printed in 2018. ISBN: 978 4 89974 083 4 (Print) ISBN: 978 4 89974 084 1 (PDF) The views in this publication do not necessarily reflect the views and policies of the Asian Development Bank Institute (ADBI), its Advisory Council, ADB’s Board or Governors, or the governments of ADB members. ADBI does not guarantee the accuracy of the data included in this publication and accepts no responsibility for any consequence of their use. ADBI uses proper ADB member names and abbreviations throughout and any variation or inaccuracy, including in citations and references, should be read as referring to the correct name. By making any designation of or reference to a particular territory or geographic area, or by using the term “recognize,” “country,” or other geographical names in this publication, ADBI does not intend to make any judgments as to the legal or other status of any territory or area. Users are restricted from reselling, redistributing, or creating derivative works without the express, written consent of ADBI. ADB recognizes “China” as the People’s Republic of China. Note: In this publication, “$” refers to US dollars. Asian Development Bank Institute Kasumigaseki Building 8F 3-2-5, Kasumigaseki, Chiyoda-ku Tokyo 100-6008, Japan www.adbi.org Contents List of illustrations v List of contributors ix List of abbreviations xi Introduction 1 Naoyuki Yoshino, José Ansón, and Matthias Helble PART I: Global Overview 1. -

Interbank GIRO Is an Automated Payment Service Which Allows You to Make Monthly Payment to Your ICBC Credit Card Account from Your Designated Bank Account Directly

Interbank GIRO Frequently Asked Questions: 1. What is Interbank GIRO? Interbank GIRO is an automated payment service which allows you to make monthly payment to your ICBC Credit Card account from your designated bank account directly. The amount will be deducted from your designated bank account and paid to ICBC every month. All you need to do is to ensure that the designated bank account has sufficient funds every month. 2. What is the benefit of using Interbank GIRO? Interbank GIRO is a convenient, paperless and cashless payment method. It enables you to make hassle-free monthly payments to ICBC through your designated bank account. There are also no fees charged for the setup. 3. Are there any additional charges for signing up for Interbank GIRO? There are no fees charged for the setup of Interbank GIRO. 4. How can I apply for Interbank GIRO? Simply fill up the Interbank GIRO form, and submit to Credit Card Department. 5. Which banks can I use for Interbank GIRO? You can use any bank that supports Interbank GIRO. 6. How long is the Interbank GIRO application Processing Time? Interbank GIRO applications may take up to 60 days to process, including the processing time required by the deducting bank. We will notify you of your application status as soon as possible. 7. How do I submit the Interbank GIRO form to ICBC Credit Card Department? You can mail the duly signed Original Interbank GIRO form to ICBC Credit Card Department by using the Business Reply Service Envelope attached. Please do not fax the Interbank GIRO form or email the scanned copy of the Interbank GIRO form as the designated bank requires the original signature for verification. -

Building a Customer-Centric Digital Bank in Singapore: It Takes an Ecosystem

White Paper Digital Banking EQUINIX AND KAPRONASIA BUILDING A CUSTOMER-CENTRIC DIGITAL BANK IN SINGAPORE: IT TAKES AN ECOSYSTEM Contents The dawn of digital banking in the Lion City Defining a value proposition . 2 No digital bank, in the purest sense of the term, Digital banking in Singapore amid COVID-19 . 4 currently exists in Singapore. While there are many fintechs, most provide only digital financial services The digital banking opportunity: that do not require a banking license: digital wallet retail and corporate . 5 services, cross-border payments and various virtual- asset-focused services. A digital bank (also known Key success factors for digital banks . 7 as a “neobank” or “virtual bank”) differs in that it is licensed to both accept customer deposits and issue 1. Digital agility to support a better loans, whether to retail customers, corporate customers customer experience. .7 or both. Singapore’s financial regulator, the Monetary 2. Favorable cost structure. .8 Authority of Singapore (MAS) plans to release five digital bank licenses in total and will announce the 3. Optimizing security .............................8 successful licensees in the second half of 2020. The licensed digital banks will likely then launch in mid-2021. Conclusion: The ecosystem opportunity . 10 While many less-developed Southeast Asian economies are leveraging digital banks to focus on financial inclusion, the role of digital banks in Singapore will be slightly different and focused on driving innovation. Bringing together traditional financial services firms, fintechs, other tech companies and even telecoms Singapore will become one of the firms, digital banks could act as a catalyst for financial focal points of Asia’s digital banking innovation in Singapore and help the city-state maintain evolution when the city-state awards its competitive advantage as a regional fintech hub.