Svenska Handelsbanken

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

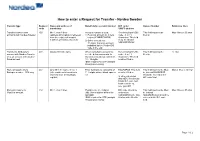

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Chronology, 1963–89

Chronology, 1963–89 This chronology covers key political and economic developments in the quarter century that saw the transformation of the Euromarkets into the world’s foremost financial markets. It also identifies milestones in the evolu- tion of Orion; transactions mentioned are those which were the first or the largest of their type or otherwise noteworthy. The tables and graphs present key financial and economic data of the era. Details of Orion’s financial his- tory are to be found in Appendix IV. Abbreviations: Chase (Chase Manhattan Bank), Royal (Royal Bank of Canada), NatPro (National Provincial Bank), Westminster (Westminster Bank), NatWest (National Westminster Bank), WestLB (Westdeutsche Landesbank Girozentrale), Mitsubishi (Mitsubishi Bank) and Orion (for Orion Bank, Orion Termbank, Orion Royal Bank and subsidiaries). Under Orion financings: ‘loans’ are syndicated loans, NIFs, RUFs etc.; ‘bonds’ are public issues, private placements, FRNs, FRCDs and other secu- rities, lead managed, co-managed, managed or advised by Orion. New loan transactions and new bond transactions are intended to show the range of Orion’s client base and refer to clients not previously mentioned. The word ‘subsequently’ in brackets indicates subsequent transactions of the same type and for the same client. Transaction amounts expressed in US dollars some- times include non-dollar transactions, converted at the prevailing rates of exchange. 1963 Global events Feb Canadian Conservative government falls. Apr Lester Pearson Premier. Mar China and Pakistan settle border dispute. May Jomo Kenyatta Premier of Kenya. Organization of African Unity formed, after widespread decolonization. Jun Election of Pope Paul VI. Aug Test Ban Take Your Partners Treaty. -

Svenska Handelsbanken AB

OFFERING CIRCULAR Svenska Handelsbanken AB (publ) (Incorporated as a public limited liability banking company in The Kingdom of Sweden) U.S.$50,000,000,000 Euro Medium Term Note Programme for the issue of Notes with a minimum maturity of one month On 26th June, 1992 Svenska Handelsbanken AB (publ) (the “Issuer” or the “Bank”) entered into a U.S.$1,500,000,000 Euro Medium Term Note Programme (the “Programme”) and issued an offering circular on that date describing the Programme. This Offering Circular supersedes any previous offering circular and supplements therein prepared in connection with the Programme. Any Notes (as defined below) issued under the Programme on or after the date of this Offering Circular are issued subject to the provisions described herein. This does not affect any Notes already in issue. Under the Programme, the Bank may from time to time issue Notes (the “Notes”), which expression shall include Notes (i) issued on a senior preferred basis as described in Condition 3 (“Senior Preferred Notes”), (ii) issued on a senior non-preferred basis as described in Condition 4 (“Senior Non-Preferred Notes”), (iii) issued on a subordinated basis and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 5 (“Subordinated Notes”) and (iv) issued on a subordinated basis with no fixed maturity and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 6 (“Additional Tier 1 Notes”). The Outstanding Principal Amount (as defined in Condition 2) of each Series (as defined below) of Additional Tier 1 Notes will be subject to Write Down (as defined in Condition 2) if the Common Equity Tier 1 Capital Ratio (as defined in Condition 2) of the Bank and/or the Handelsbanken Group (as defined Condition 2) is less than the relevant Trigger Level (as defined in Condition 2). -

The Environmental and Rural Development Plan for Sweden

0LQLVWU\RI$JULFXOWXUH)RRGDQG )LVKHULHV 7KH(QYLURQPHQWDODQG5XUDO 'HYHORSPHQW3ODQIRU6ZHGHQ ¤ -XO\ ,QQHKnOOVI|UWHFNQLQJ 7,7/(2)7+(585$/'(9(/230(173/$1 0(0%(567$7($1'$'0,1,675$7,9(5(*,21 *(2*5$3+,&$/',0(16,2162)7+(3/$1 GEOGRAPHICAL AREA COVERED BY THE PLAN...............................................................................7 REGIONS CLASSIFIED AS OBJECTIVES 1 AND 2 UNDER SWEDEN’S REVISED PROPOSAL ...................7 3/$11,1*$77+(5(/(9$17*(2*5$3+,&$//(9(/ 48$17,),(''(6&5,37,212)7+(&855(176,78$7,21 DESCRIPTION OF THE CURRENT SITUATION...................................................................................10 (FRQRPLFDQGVRFLDOGHYHORSPHQWRIWKHFRXQWU\VLGH The Swedish countryside.................................................................................................................... 10 The agricultural sector........................................................................................................................ 18 The processing industry...................................................................................................................... 37 7KHHQYLURQPHQWDOVLWXDWLRQLQWKHFRXQWU\VLGH Agriculture ......................................................................................................................................... 41 Forestry............................................................................................................................................... 57 6XPPDU\RIVWUHQJWKVDQGZHDNQHVVHVWKHGHYHORSPHQWSRWHQWLDORIDQG WKUHDWVWRWKHFRXQWU\VLGH EFFECTS OF CURRENT -

Interim Report January – September 2020 Q3

Interim Report January – September 2020 Q3 Financial summary Third quarter First nine months • Net sales amounted to EUR 27k (0) • Net sales amounted to EUR 126k (21k) • Operating loss (EBIT) increased to EUR 4,790k • Operating loss (EBIT) increased to EUR 7,291k (748k) driven by listing costs (3,490k) driven by listing costs • Loss after tax amounted to EUR 4,730k (815k) • Loss after tax amounted to EUR 7,127k (3,602k) • Basic and diluted loss per Class A share amounted to EUR 0.10 (0.02) • Basic and diluted loss per Class A share amounted to EUR 0.16 (0.08) • Liquid funds as at end of the period amounted to EUR 90.5m • Cash flow from operating activities amounted to EUR -1,824k (-3,014k) • No interest-bearing debt at end of the period Figures within parentheses refer to the preceding year. Significant events • Enlisted Inselspital Bern, the largest In the third quarter of 2020 university hospital in Switzerland, to be the lead hospital in our upcoming RefluxStop™ • Completed listing on Nasdaq First North Premier Growth Market raising SEK 1.1 Registry clinical trial to be focused primarily billion, with trading of Implantica's Swedish in Germany and Switzerland. Depository Receipts commencing on September 21, 2020. The offering was After the end of the period substantially oversubscribed. • Exercised overallotment option raising an additional SEK 165 million. • Increased our shareholder base with highly reputable shareholders such as Swedbank • Implantica’s RefluxStop™ trial showed Robur Ny Teknik, Handelsbanken Fonder, exceptional three-year follow-up results. TIN Fonder, Skandia and Nordea Investment None of the 47 patients in the study were in Management. -

Kvinnliga Pionjärer I Villastaden Djursholm Och Danderyds Kommun Inger Ström-Billing

Kvinnliga pionjärer i villastaden Djursholm och Danderyds kommun inger Ström-Billing Danderyds kommunvapen, tidigare Djursholms stadsvapen. I vapnet ingår de tre fälten från släkten Banérs vapensköld, de tre rosorna överst symboliserar trädgårdsstaden Djursholm. När det gamla Banérgodset började sälja ut sin mark i slutet av 1800-talet köptes området närmast slottet av Djursholm AB för att där anlägga Sveri- ges första villa- och trädgårdsstad. Bland aktieinnehavarna fanns flera kvin- nor med relativt stora aktieposter, men ingen av dem satt i bolagets styrelse.1 Bolaget delade upp marken i tomter och skötte även under de första åren sådana tekniska angelägenheter som väganläggningar, vattenledning och elverk, men deltog även i finansieringen av diverse sociala ärenden som att bekosta en barnmorskas lön och ett fattighus. År 1890 övertog municipal- samhället Djursholm det mesta av bolagets tillgångar och åtaganden och 1901 övergick området till att bli Djursholms köping med ett innevånarantal av ca 1 400 personer.2 Ännu fanns ingen kvinna med bland de styrande i kommunalstämman, men i underliggande nämnder hittar vi nu den första kvinnliga ledamoten. Helena Svedelius Helena Svedelius, lärare vid Djursholms Samskola, hade kommit in i det kommunala arbetet när en särskild styrelse för epidemisjukvården valdes i januari 1901 och när en sjukhusstyrelse bildades senare samma år, valdes hon in även där. Helena Svedelius var även den första kvinna som nio år senare, 1910, kom in i en av de högre politiska instanserna som suppleant i kommunalnämnden. Hon hade vid valet 1910 kandiderat till kommunal- 123 lay Moderata UA.indd 123 09-09-29 13.19.18 moderata kvinnor från umeå till trelleborg fullmäktige i detta första val där kvinnor kunde väljas in i denna församling. -

Regeltillämpning På Kommunal Nivå Undersökning Av Sveriges Kommuner 2020

Regeltillämpning på kommunal nivå Undersökning av Sveriges kommuner 2020 Kronobergs län Handläggningstid i veckor (Serveringstillstånd) Kommun Handläggningstid 2020 Handläggningstid 2016 Serveringstillstånd Markaryd 5 8 Älmhult 5 6 Alvesta 6 8 Lessebo 6 7 Ljungby 6 6 Medelvärde Tingsryd 6 6 handläggningstid 2020 Växjö 8 Sverige: 5,7 veckor Uppvidinge 9 Gruppen: 6,4 veckor Medelvärde handläggningstid 2016 Sverige: 6,0 veckor Gruppen: 6,8 veckor Handläggningstid i veckor (Bygglov) Kommun Handläggningstid 2020 Handläggningstid 2016 Bygglov Uppvidinge 1 2 Älmhult 3 1 Lessebo 4 1 Ljungby 4 1 Växjö 4 4 Medelvärde Markaryd 6 2 handläggningstid 2020 Alvesta 4 Sverige: 4,0 veckor Tingsryd Gruppen: 4,2 veckor Medelvärde handläggningstid 2016 Sverige: 4,0 veckor Gruppen: 2 veckor Servicegaranti (Bygglov) Servicegaranti Dagar Digitaliserings- Servicegaranti Dagar Kommun Bygglov 2020 2020 grad 2020 2016 2016 Alvesta Nej Lessebo Nej 0 Ja Ljungby Ja 14 0 Ja 21 Markaryd Ja 70 Ja 7 Servicegaranti 2020 Sverige: 19 % Ja Tingsryd Gruppen: 50 % Ja Uppvidinge Ja 28 0 Ja Växjö Nej 1 Nej Digitaliseringsgrad 2020 Sverige: 0,52 Älmhult Nej 0 Ja 28 Gruppen: 0,2 Servicegaranti 2016 Sverige: 30 % Ja Gruppen: 71 % Ja Tillståndsavgifter (Serveringstillstånd) Kommun Tillståndsavgift 2020 Tillståndsavgift 2016 Serveringstillstånd Lessebo 4 500 Uppvidinge 5 000 Alvesta 6 000 6 000 Ljungby 6 000 6 000 Tingsryd 6 000 Medelvärde tillstånds- Markaryd 7 500 6 000 avgift 2020 Älmhult 7 500 3 000 Sverige: 9 513 kr Gruppen: 6 437 kr Växjö 9 000 Medelvärde tillstånds- avgift 2016 -

Welcome to Tingsryd Municipality!

Welcome to Tingsryd Municipality! Välkommen! Welcome! !بيحرت soo dhawow! khosh maden! Contents Tingsryd municipality p. 1 Citizens’ advice bureau p. 1 Meeting places p. 2 Schools and childcare p. 3 Finances p. 4 Healthcare p. 5 Housing p. 6 Societies, clubs and activities p. 7 Authorities p. 8-9 Good to know p. 10 Contact p. 11-12 Tingsryd Municipality About our municipality Tingsryd is a vibrant, attractive and care for children and the and modern rural municipality, elderly. The district is character- in the midst of a strong region of ized by a small-scale agricultural growth. Here we have engaged landscape with over 200 lakes. citizens, active industry, rich societal life and ample opportu- Within an hour’s radius of nities for human interactions. Tingsryd municipality is home to nearly 300,000 people and within More than a third of the popu- two hours is one of Europe’s lation of Tingsryd live in rural regions of growth: Malmö / areas. In each of the seven lo- Copenhagen. Also nearby are calities of Konga, Linneryd, Ryd, Linnaeus University in Växjö, Rävemåla, Tingsryd, Urshult and and Blekinge Institute of Väckelsång are found basic serv- Technology, and The University ices including schools, businesses of Karlskrona and Karlshamn. Citizens’ advice bureau If you have questions about school, accommodation, or need help filling in forms we can help you! At the Citizens’ Advice Bureau in Tingsryd municipality (Torggatan 12) you can get help with most things, and find out where to turn should we be unable to help. Please call 0477 441 00 The Citizens’ Advice Bureau opening hours: Mon 08:00 to 18:00 Tue-Fri 8:00 to 16:30 Open at lunchtime every day 1 Tingsryd Municipality Meeting places There are different kinds of meet- retired, youth or immigrant, or You can also register your interest ing places in Tingsryd whose goal have lived a long time in Sweden. -

Welcome out – Into the Nature of Kronoberg!

Welcome out – into the nature of Kronoberg! – Your guide to 35 beautiful nature reserves Production: The County Council Administrative Board, Kronoberg County, 2019. Cover picture: Tobias Ivarsson. Photographers: Tobias Ivarsson: golden plover, pg. 9; black grouse lekking, pg. 11; witch’s hair lichen, pg. 32; wood grouse, pg. 36; fritillary, pg. 44; common tern, pg. 54; osprey, pg. 92; black-throated loon, pg. 96. Ljungby Municipality: pine plant, pg. 98. Småland pictures: Kronoskogen, pg. 97; outdoor gym, pg. 98; coffee break “fika”, pg. 99.The County Administrative Board: Eva Elfgren: cross-leaf heath, pg. 12; leafy verdure, pg. 81; Per Ekerholm: marsh gentian, pg. 18; Thomas Hultquist: crane, pg. 39; Magnus Strindell: ox-tongue fungus, pg. 47; Elin Åkelius: cowslip, pg. 51; The County Council Administrative Board: dalmatian spot, pg. 53; Peter Mattiasson: Mörrumsån, ppg. 56–57; Börge Pettersson: soprano pipistrelles, pg. 65; Mats Wilhelm Pettersson: hay meadow, pg. 69; Emil Persson: scarlet waxcap, pg. 75; Peter Wredin: hazel dormouse nest, pg. 80; Heléne Petterson: view over Toftasjön, pg. 87; Martin Unell: fireplace, pg. 92.Other photos: Ellen Flygare and Martin Wargren, The County Council Administrative Board. Text: Ellen Flygare, except Kronoskogen, where the author is Naturcentrum AB. Maps: Peter Mattiasson. Background map: © Lantmäteriet Geodatasamverkan. The guide is available at the County Council web site, www.lansstyrelsen.se/kronoberg Welcome out into nature! The book you are holding in your hand is a guide to the nature of Kronoberg. We have chosen 35 nature reserves with beautiful scenery, well worth a visit, and present them in words and pictures. The book also includes a cultural reserve, Linneaus’ Råshult. -

Lease Versus Buy Decision of Real Estate for Foreign Diplomatic Missions in Stockhom, Sweden

KTH Architecture and The Built Environment Department of Real Estate and Construction Management Master Of Science In Real Estate Management Thesis no. 396 LEASE VERSUS BUY DECISION OF REAL ESTATE FOR FOREIGN DIPLOMATIC MISSIONS IN STOCKHOM, SWEDEN Author: Supervisor: Ruby Bleppony Prof. Hans Lind Stockholm 2015 ABSTRACT Purpose - The purpose of this study is to present a general view on the real estate situation for diplomatic missions in Stockholm, Sweden, and thus identifying factors affecting the lease versus buy decision of their office space and residential facilities, examining the significance of these factors on their decisions. Design/methodology/approach - This paper takes an empirical approach, with questionnaire presented to the 105 embassies in Stockholm. The results were presented coupled with the experience of working in an embassy, bearing on the analysis of this paper. Findings - The results shows that other factors outweigh the financial factor, which has been the bedrock in the decision process to lease or buy real estate for diplomatic mission. The non- financial factor, mainly functionality in the aspects of security, size of the real estate facility and location were more significant in the decision process for DMs. The demand and supply dynamics in the local markets has been demonstrated as also being significant in the LVB decision for DMs, but not as strong as the functionality factor. On the other hand, factors such as bi-lateral relations / institutional factor and cultural factors that affect local market practices were rather insignificant in the decision process. Research limitations/implications - Even though all the 105 diplomatic missions were presented with the questionnaire, the outcome of the empirical survey is however limited to a few embassies and due to the small number of embassies involved in this study, there could be limitations on the statistical generalizability of results due to the small number of embassies involved in the study. -

Våga Visa Observationsrapport 2016

Viktor Rydberg Gymnasium Djursholm Danderyds kommun Monica Ernbo, Nacka Marita Kallur, Nacka Jenny Segerberg, Nacka Vecka 6-7, 2016 Innehållsförteckning VÅGA VISA _____________________________________________________________ 3 FAKTADEL _____________________________________________________________ 4 Fakta om enheten .......................................................................................................................................... 4 Statistik .......................................................................................................................................................... 5 Organisation /Ledning................................................................................................................................... 5 OBSERVATIONENS METOD _____________________________________________ 6 SAMMANFATTNING ____________________________________________________ 7 Sammanfattande slutsats ............................................................................................................................... 7 Starka sidor ................................................................................................................................................... 7 Förbättringsområden .................................................................................................................................... 8 MÅLOMRÅDEN ________________________________________________________ 9 Normer och värden ....................................................................................................................................... -

CREATING SUSTAINABLE SERVICE RELATIONSHIPS in the POST-MODERN CONTEXT a Case Study of Svenska Handelsbanken

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Göteborgs universitets publikationer - e-publicering och e-arkiv International Business Programme Master Thesis No 2003:53 CREATING SUSTAINABLE SERVICE RELATIONSHIPS IN THE POST-MODERN CONTEXT A case study of Svenska Handelsbanken David Kling-Wahlby & Ana Lulic Graduate Business School School of Economics and Commercial Law Göteborg University ISSN 1403-851X Printed by Elanders Novum ABSTRACT Today it is arguably so that we live in a post-modern society. This is said to have effects on the customers’ behaviour and, if so, the companies must adapt to this. At the same time it can be seen that the service sector is becoming larger and sometimes mature and over- supplied. Further, new technology has also increased the possibilities for service companies to offer their service through impersonal communication channels. All this has led to companies adapting a more relational, rather than transactional, approach towards the customer. Consequently, the purpose of the study is to develop a model that explains how and in what ways a service company can create sustainable relationships and illustrate how service offerings could be delivered to customers within a post-modern context. In order to visualise this relationship process a theoretical model has been developed. Our model is based on theories regarding post-modernism, service marketing, relationships, resources & capabilities and service quality. This model indicates that the prerequisite for a relationship to exist is that the customers perceive that there is service quality in the company’s offering. This will in turn enable the customer to feel the existence of relationship quality, which in turn leads to loyalty and consequently, a sustainable relationship.