Chronology, 1963–89

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sustainable Investing for a Changing World Annual Report 2016 About Schroders

Sustainable investing for a changing world Annual Report 2016 About Schroders At Schroders, asset management is our only business and our goals are completely aligned with those of our clients: the creation of long-term value to assist them in meeting their future financial requirements. We have responsibility for £397.1 billion As responsible investors and signatories (€465.2 billion/$490.6 billion) on behalf to the UN’s Principles for Responsible of institutional and retail investors, Investment (PRI) we consider the long-term financial institutions and high net worth risks and opportunities that will affect the clients from around the world, invested resilience of the assets in which we invest. across equities, fixed income, multi-asset, This approach is supported by our alternatives and real estate. Environmental, Social and Governance (ESG) Policy and our Responsible Real Estate Investment Policy. Presence in 41 offices P 27 countries globally £397.1 bn assets 4,100+ under management employees and administration 15% 15% 4% 4% 10% 10% 39% 39% 40% 40% 21% 21% by client by client By product domicile domicile By product 21% 21% 25% 25% 25% 25% United KingdomUnited Kingdom Asia Pac ific Asia Pacific uities uities ultiasset ultiasset urope iddleurope ast and iddle frica ast and fricamericas mericas Wealth manaementWealth manaementied income ied income merin maretmerin debt commoditiesmaret debt andcommodities real estate and real estate Source: Schroders, as at 31 December 2016 1 The companies and sectors mentioned herein are for illustrative purposes only and are not to be considered a recommendation to buy or sell. % W P X AA AAA 2016 has shown that the social and environmental backdrop facing companies is changing quickly and pressures are coming to a head. -

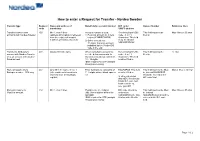

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Northern Rock Plc - HM Treasury

[ARCHIVED CONTENT] Northern Rock plc - HM Treasury This snapshot, taken on 07/04/2010, shows web content acquired for preservation by The National Archives. External links, forms and search may not work in archived websites and contact details are likely to be out of date. More about the UK Government Web Archive See all dates available for this archived website The UK Government Web Archive does not use cookies but some may be left in your browser from archived websites. More about cookies 16/08 Help | Contact us | Access keys | Site map | A-Z 17 February 2008 Northern Rock plc Newsroom & speeches Home > Newsroom & speeches > Press notices > 2008 Press Notices > February > Northern Rock plc 1. The Government has today decided to bring forward legislation that will enable Northern Rock plc to be taken into a period of temporary Home public ownership. The Government has taken this decision after full consultation with the Bank of England and the Financial Services Authority. The Government's financial adviser, Goldman Sachs, has concluded from a financial point of view that a temporary period of Budget public ownership better meets the Government's objective of protecting taxpayers. 2. Northern Rock will be open for business as usual tomorrow morning and thereafter. Branches will be open; internet and call centre Pre-Budget Report services will operate as normal. All Northern Rock employees remain employed by the company. Depositors' money remains absolutely safe and secure. The Government's guarantee arrangements remain in place and will continue to do so. Borrowers will continue to make their payments in the normal way. -

The Headquarters of National Provincial Bank of England

Symbolism in bank marketing and architecture: the headquarters of National Provincial Bank of England Article Published Version Creative Commons: Attribution 4.0 (CC-BY) Open Access Barnes, V. and Newton, L. (2019) Symbolism in bank marketing and architecture: the headquarters of National Provincial Bank of England. Management and Organizational History, 14 (3). pp. 213-244. ISSN 1744-9359 doi: https://doi.org/10.1080/17449359.2019.1683038 Available at http://centaur.reading.ac.uk/86938/ It is advisable to refer to the publisher’s version if you intend to cite from the work. See Guidance on citing . To link to this article DOI: http://dx.doi.org/10.1080/17449359.2019.1683038 Publisher: Taylor and Francis All outputs in CentAUR are protected by Intellectual Property Rights law, including copyright law. Copyright and IPR is retained by the creators or other copyright holders. Terms and conditions for use of this material are defined in the End User Agreement . www.reading.ac.uk/centaur CentAUR Central Archive at the University of Reading Reading’s research outputs online Management & Organizational History ISSN: 1744-9359 (Print) 1744-9367 (Online) Journal homepage: https://www.tandfonline.com/loi/rmor20 Symbolism in bank marketing and architecture: the headquarters of National Provincial Bank of England Victoria Barnes & Lucy Newton To cite this article: Victoria Barnes & Lucy Newton (2019) Symbolism in bank marketing and architecture: the headquarters of National Provincial Bank of England, Management & Organizational History, 14:3, 213-244, DOI: 10.1080/17449359.2019.1683038 To link to this article: https://doi.org/10.1080/17449359.2019.1683038 © 2019 The Author(s). -

The London School of Economics and Political Science

The London School of Economics and Political Science Thesis Foreign Government Loan Issues on the London Capital Market, 1870 - 1913, with Special Reference to Japan by Toshio SUZUKI A Thesis submitted to the University of London for the Degree of Doctor of Philosophy, 1991 February UMI Number: U050B50 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. Dissertation Publishing UMI U050B50 Published by ProQuest LLC 2014. Copyright in the Dissertation held by the Author. Microform Edition © ProQuest LLC. All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code. ProQuest LLC 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106-1346 F 6&'F- x6( I o 7<>c Abstract This thesis examines foreign government loan issues on the London capital market in the period from 1870 to 1913, with special reference to Japan. Chapter One provides an overview of foreign government loan issues in London. Chapter Two deals with a number of more specific topics: the development of the loan issue organisations on the market, and the role and involvement of various types of financial institutions in loan issue business. Later Chapters mainly take up the detailed history of Japanese government loan issues, referring to domestic Japanese financial conditions. Chapters Three to Seven examine the development of Japanese government loan issues on the international capital markets. -

Societe Generale Private Banking Hambros

SOCIETE GENERALE PRIVATE BANKING HAMBROS SPRING/SUMMER 2016 – N°9 James Welling – Choreograph, 2014-2015, Ink jet print, 160x107cm. New acquisition 02 02 04 04 06 06 08 ECONOMICECONOMIC OUTLOOK OUTLOOK EXPERTISE EXPERTISE PORTRAIT PORTRAITPRIVATE BANKING OIL, AOIL, DIFFERENT A DIFFERENT HEDGE FUNDSHEDGE FUNDS IGNACE IGNACEOUR REGIONAL ENVIRONMENTENVIRONMENTA TIME OF RENEWALA TIME OF RENEWALVAN DOORSELAEREVAN DOORSELAEREEXPANSION CEO, VAN DE VELDE CEO, VAN DE VELDE WE ARE PROUD SPONSOR OF THE V&A’S MAJOR EXHIBITION BOTTICELLI REIMAGINED MARCH 5 – JULY 3, 2016 VICTORIA AND ALBERT MUSEUM, LONDON SOCIETEGENERALE.CO.UK Societe Generale is a French credit institution (Bank) authorised and supervised by the European Central Bank (ECB) and the Autorité de Contrôle Prudentiel et de Résolution (ACPR) (the French Prudential Control and Resolution Authority) and regulated by the Autorité des marchés financiers (the French financial markets regulator) (AMF). Societe Generale, London Branch is authorised by the ECB, the ACPR and the Prudential Regulation Authority (PRA) and subject to limited regulation by the Financial Conduct Authority (FCA) and the PRA. Details about the extent of our authorisation, supervision and regulation by the above mentioned authorities are available from us on request. FFGROUP © MICHEL LABELLE ANDY PARADISE ‘PARADISE T/AS PHOTO’ WelcomeA RENOVATED to the EUROPEAN Spring issue ORGANISATION of La Lettre. The transformation of private banks is gaining pace under the impulse of regulatory changes,The transformation the revolution of private in information banks istechnologies gaining pace and under changes the impulsein behaviour. These upheavalsof regulatory changes, are often the presented revolution as in constraints, information but technologies we see them and as changes an excellent inopportunity behaviour. -

Svenska Handelsbanken AB

OFFERING CIRCULAR Svenska Handelsbanken AB (publ) (Incorporated as a public limited liability banking company in The Kingdom of Sweden) U.S.$50,000,000,000 Euro Medium Term Note Programme for the issue of Notes with a minimum maturity of one month On 26th June, 1992 Svenska Handelsbanken AB (publ) (the “Issuer” or the “Bank”) entered into a U.S.$1,500,000,000 Euro Medium Term Note Programme (the “Programme”) and issued an offering circular on that date describing the Programme. This Offering Circular supersedes any previous offering circular and supplements therein prepared in connection with the Programme. Any Notes (as defined below) issued under the Programme on or after the date of this Offering Circular are issued subject to the provisions described herein. This does not affect any Notes already in issue. Under the Programme, the Bank may from time to time issue Notes (the “Notes”), which expression shall include Notes (i) issued on a senior preferred basis as described in Condition 3 (“Senior Preferred Notes”), (ii) issued on a senior non-preferred basis as described in Condition 4 (“Senior Non-Preferred Notes”), (iii) issued on a subordinated basis and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 5 (“Subordinated Notes”) and (iv) issued on a subordinated basis with no fixed maturity and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 6 (“Additional Tier 1 Notes”). The Outstanding Principal Amount (as defined in Condition 2) of each Series (as defined below) of Additional Tier 1 Notes will be subject to Write Down (as defined in Condition 2) if the Common Equity Tier 1 Capital Ratio (as defined in Condition 2) of the Bank and/or the Handelsbanken Group (as defined Condition 2) is less than the relevant Trigger Level (as defined in Condition 2). -

Banknews Reprints of Articles About Your Community Bank • • 703.584.0840

Member BankNews Reprints of articles about your community bank • www.JohnMarshallBank.com • 703.584.0840 In 1992, he was hired by Chase Manhattan Personal John Marshall Financial Services as a Second Vice President originating and underwriting jumbo mortgages. In 1995, he Bank Expands returned to commercial lending and until 2002, he held AVP and VP commercial lending positions at Citibank, to Alexandria FSB, First Virginia Bank and F&M Bank of Northern Virginia. From 2002 until 2009, Mr. Johnson was Senior Vice President of commercial lending for Virginia Commerce Bank, where he was responsible for growing a small By Bob Tagert / reprinted from OldTownCrier.com commercial loan portfolio of $5 million into a $90 mil- lion portfolio with approximately $80 million in corre- As today’s banking world appears to be one acquisition sponding deposit and cash management relationships. In after another, it is nice to see a local bank, founded by 2009, he accepted the position as Chief Lending Officer people who are local to the area and employing profes- of 1st Commonwealth Bank of Virginia. sionals who know and live in the community. As the names of banks change as much as the weather, it is Johnson is the current Chairman of the Arlington refreshing to see a local bank making its presence felt. Industrial Loan Authority and has served on this board The bank was founded in 2006 and has their corporate since 2008. Mr. Johnson has been an active member of offices in Reston. John Marshall Bank is a strong commu- nity bank that is well capitalized and is one of the fastest growing banks in the DC Metro area. -

Cohen & Steers Preferred Securities and Income Fund

Cohen & Steers Preferred Securities and Income Fund As of 06/30/2021 Current % of Total Security Name Sector Market Value Market Value Wells Fargo & Company Flt Perp Banking $219,779,776.15 1.81 % Charles Schwab Corp Flt Perp Sr:I Banking $182,681,675.00 1.51 % Bp Capital Markets Plc Flt Perp Energy $158,976,029.00 1.31 % Bank of America 6.25% Banking $148,052,279.38 1.22 % Bank of Amrica 6.10% Banking $144,075,863.52 1.19 % Citigroup Inc Flt Perp Banking $139,736,756.25 1.15 % Emera 6.75% 6/15/76-26 Utilities $134,370,096.24 1.11 % Transcanada Trust 5.875 08/15/76 Pipeline $116,560,837.50 0.96 % JP Morgan 6.75% Banking $116,417,211.75 0.96 % JP Morgan 6.1% Banking $115,050,549.38 0.95 % Credit Suisse Group AG 7.5 Perp Banking $112,489,090.00 0.93 % Enbridge Inc Flt 07/15/80 Sr:20-A Pipeline $101,838,892.50 0.84 % Charles Schwab Corp Flt Perp Sr:G Banking $101,715,980.40 0.84 % Bank of America Corp 5.875% Perp Banking $99,269,540.97 0.82 % Sempra Energy Flt Perp Utilities $97,680,337.50 0.81 % BNP Paribas 7.375% Banking $96,328,288.48 0.79 % Jpmorgan Chase & Co Flt Perp Sr:Kk Banking $95,672,863.00 0.79 % Metlife Capital Trust IV 7.875% Insurance $94,971,600.00 0.78 % Citigroup 5.95% 2025 Call Banking $89,482,599.30 0.74 % Transcanada Trust Flt 09/15/79 Pipeline $88,170,468.75 0.73 % Ally Financial Inc Flt Perp Sr:C Banking $86,422,336.00 0.71 % Banco Santander SA 4.75% Flt Perp Banking $83,189,000.00 0.69 % American Intl Group 8.175% 5/15/58 Insurance $82,027,104.20 0.68 % Prudential Financial 5.625% 6/15/43 Insurance $80,745,314.60 0.67 -

Morningstar Report

Report as of 02 Oct 2021 Threadneedle Monthly Extra Income Fund Retail Income GBP Morningstar® Category Morningstar® Benchmark Fund Benchmark Morningstar Rating™ Category_EUCA000916 Morningstar UK Moderately 20% ICE BofA Sterling Corp&Coll TR QQQ Adventurous Target Allocation NR GBP EUR, 80% FTSE AllSh TR GBP Used throughout report Investment Objective Performance The Fund aims to provide a monthly income with prospects 172 for capital growth over the long term. It looks to provide 154 an income yield higher than the FTSE All-Share Index over 136 rolling 3-year periods, after the deduction of charges. The 118 Fund is actively managed, and invests in a combination of 100 company shares and bonds; typically, between 70-80% in 82 UK company shares and 20%-30% in bonds. 2016 2017 2018 2019 2020 2021-08 12.39 6.59 -5.45 19.10 -5.17 11.72 Fund - - - - 4.52 9.96 Benchmark 13.23 10.00 -6.37 15.67 5.25 9.54 Category Risk Measures Trailing Returns % Fund Bmark Cat Quarterly Returns % Q1 Q2 Q3 Q4 3Y Alpha -4.50 3Y Sharpe Ratio 0.33 3 Months 1.16 0.35 0.46 2021 2.78 4.59 - - 3Y Beta 1.30 3Y Std Dev 14.34 6 Months 6.14 5.16 5.16 2020 -20.71 10.08 -0.11 8.77 3Y R-Squared 89.79 3Y Risk abv avg 1 Year 17.92 15.22 15.32 2019 6.46 2.75 4.10 4.59 3Y Info Ratio -0.54 5Y Risk abv avg 3 Years Annualised 3.80 6.62 6.12 2018 -4.05 8.69 -0.28 -9.09 3Y Tracking Error 5.57 10Y Risk abv avg 5 Years Annualised 4.71 7.20 6.49 2017 3.91 2.73 -0.15 0.01 Calculations use Morningstar UK Moderately Adventurous Target Allocation NR GBP 10 Years Annualised 8.86 8.92 8.05 -

The Global Financial Crisis: Is It Unprecedented?

Conference on Global Economic Crisis: Impacts, Transmission, and Recovery Paper Number 1 The Global Financial Crisis: Is It Unprecedented? Michael D. Bordo Professor of Economics, Rutgers University, and National Bureau of Economic Research and John S. Landon-Lane Associate Professor of Economics, Rutgers University 1. Introduction A financial crisis in the US in 2007 spread to Europe and led to a recession across the world in 2007-2009. Have we seen patterns like this before or is the recent experience novel? This paper compares the recent crisis and recent recession to earlier international financial crises and global recessions. First we review the dimensions of the recent crisis. We then present some historical narrative on earlier global crises in the nineteenth and twentieth centuries. The description of earlier global crises leads to a sense of déjà vu. We next demarcate several chronologies of the incidence of various kinds of crises: banking, currency and debt crises and combinations of them across a large number of countries for the period from 1880 to 2010. These chronologies come from earlier work of Bordo with Barry Eichengreen, Daniela Klingebiel and Maria Soledad Martinez-Peria and with Chris Meissner (Bordo et al (2001), Bordo and Meissner ( 2007)) , from Carmen Reinhart and Kenneth Rogoff’s recent book (2009) and studies by the IMF (Laeven and Valencia 2009,2010).1 Based on these chronologies we look for clusters of crisis events which occur in a number of countries and across continents. These we label global financial crises. 1 There is considerable overlap in the different chronologies as Reinhart and Rogoff incorporated many of our dates and my coauthors and I used IMF and World Bank chronologies for the period since the early 1970s. -

Name of Deceased

Date before which Name of Deceased Address, description and date of death of Deceased Names, addresses and descriptions of Persons to whom notices of claims are to be given notices of claim (Surname first) • and names, in parentheses, of Personal Representatives ' ' to be given LLOYD, May Emily Kenwyn Lodge, Western Road, Fortis Green, National Provincial Bank Limited, 8 Howland Street, Tottenham Court Road, London 28th August 1964 Middlesex, Spinster. 8th June 1964. W.I. (092) PHILLIPS, Mary Flat 3, St. John's Court, Westcliff Parade, Westcliff- Howard Kennedy & Co., 23 Harcourt House, 19 Cavendish Square, London W.I. 3rd September 1964 on-Sea, Essex, Widow. 14th October 1963. (David Crystall and Harry Howard, LL.B.) (093) WARD, Constance Annie 8 Calverley Park, Tunbridge Wells, Kent, Widow, Burton & Ramsden, 81 Piccadilly, London W.I, Solicitors. (James Hildebrand'Ramsden 28th August 1964 Henrietta. llth November 1963. and Jack Bridgeland.) (094) H W SCHOFIELD, William 35 Fitzmauriae Road, Christchurch, Hampshire, Barrington Myers & Partners, Lloyds Bank Chambers, Christchurch, Hampshire, 28th August 1964 1 Arthur. Pilot. 18th February 1964. Solicitors. (Mary Dorothy Anne Schofield.) (095) r o TURNER, Maud Violet The Nosegay, Abersoch, Caernarvonshire, Spinster. Robyns Owen & Son, 36 High Street, Pwllheli, Caernarvonshire, Solicitors. (National 29th August 1964 Breen. 26th May 1964. Provincial Bank Limited.) (096) THOMPSON, Thojnas ... 108 Ponteland Road, Newcastle upon Tyne, General National Provincial Bank Limited, Trustee Branch, 26 Mosley Street, Newcastle upon 27th August 1964 Dealer. 6th June 1964. Tyne. (097) NEILLY, William John... 95 St. Ladoc Road, Keynsham, Bristol, Retired National Provincial Bank Limited, Trustee Branch, 36 Corn Street, Bristol 1, or 27th August 1964 I Clerk.