Sustainable Investing for a Changing World Annual Report 2016 About Schroders

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Schroder Investment Fund Company Prospectus 1 September 2021

Schroder Investment Fund Company Prospectus 1 September 2021 United Kingdom (SIFCO) Schroder Investment Fund Company (SIFCO) Prospectus 1 September 2021 Schroder Unit Trusts Limited Internet Site: http://www.schroders.co.uk Important Information Prospectus of Schroder Investment Fund Company not, under any circumstances, create any implication that the affairs of the Company have not changed since the date An investment company with variable capital incorporated hereof. with limited liability and registered in England and Wales under Regulation 4 of the Open Ended Investment The distribution of this Prospectus and the offering of Shares Companies Regulations 2001, as amended or re-enacted from in certain jurisdictions may be restricted. Persons into whose time to time. possession this Prospectus comes are required by the Company to inform themselves about and to observe any This document (this Prospectus) constitutes the prospectus such restrictions. This Prospectus does not constitute an offer for Schroder Investment Fund Company (the Company), or solicitation by anyone in any jurisdiction in which such an which has been prepared in accordance with the Collective offer or solicitation is not authorised or to any person to Investment Schemes (COLL) Sourcebook of the Financial whom it is unlawful to make such offer or solicitation. Conduct Authority (FCA) made under the Financial Services and Markets Act 2000. Shares in the Company are not listed or dealt on any investment exchange. This Prospectus is dated, and is valid as at 1 September 2021. Potential investors should not treat the contents of this Copies of this Prospectus have been sent to the FCA and the Prospectus as advice relating to legal, taxation, investment or Depositary. -

Snapshot of Notable Global Financial Services CFO Moves, Appointments, Themes and Trends

Snapshot of notable global financial services CFO moves, appointments, themes and trends “Increasing examples of senior finance leaders making a move out of the tier one banking groups.” January 2016 - April 2016 CFO Themes Page 1/5 Next update due: 19/9/2016 Summary of key themes and trends Jan - Apr 2016 Growing appetite from and drive overall US banks investing heavily non-banking financial efficiency savings after in global FP&A functions services firms to five years of cross industry in a continued response significantly upgrade their investment to CCAR and augmented audit functions with a reporting requirements focus on improved Increasing examples of business partnering, senior finance leaders regulatory interface and making a move out of data analytics the tier one banking groups given the Significant activity in the increasingly challenging Audit COO space as regulatory environment large banking groups look and the role of the CFO to streamline global in it methodology, improve training & development Leathwaite: London | Zürich | Hong Kong | New York Twitter @L3athwaite www.leathwaite.com CFO Moves Page 2/5 Next update due: 19/9/2016 Key global people moves and appointments: UK market: Ekene Ezulike, CFO Infrastructure at Deutsche Christopher Hill joins Hargreaves Lansdown as Bank is made Chief Procurement Officer. His CFO. Previously he served as CFO for IG Group Insurance previous role is being covered by Neil Smith. and Travelex. Glynn Jones joins ANZ as the Head of Financial Helen Pickford is appointed UK Life CFO at Audit Planning & Analysis for the markets business. He Zurich. Helen replaces Neil Evans who joins was previously the CFO for Financial Markets at Graham Mason joins Lombard Odier as Global Aviva as the Head of Financial Reporting for the Standard Chartered. -

Chairman's Governance Letter

64 BAE Systems | Annual Report 2016 Chairman’s governance letter Contents Dear Shareholders, During the course of the year, the Financial We welcomed the FRC’s report and the Chairman’s governance letter 64 Reporting Council (FRC) published its report principles of stakeholder engagement, Governance highlights 65 on Corporate Culture and the Role of Boards. directors’ duties and the importance of Board governance 66 The report contained key observations corporate integrity and responsible behaviour that it outlined. Board of directors 68 about the value of culture in driving the right behaviours in the boardroom and at Board information 70 Towards the end of 2016, there was another all levels in the company. We were pleased important governance publication, with the Governance disclosures 71 to see that the report included a case study UK government publishing a wide-ranging Audit Committee report 72 on BAE Systems, illustrating the work we had Green Paper on Corporate Governance undertaken over a number of years to foster Reform. Both documents quote in full the Corporate Responsibility high levels of personal trust between trade Committee report 76 basic duty of a company director as detailed unions and the Company’s senior leadership. in Section 172 of the Companies Act. Nominations Committee report 78 As part of this year’s Board evaluation, we Remuneration Committee report 79 have asked Board members to reflect on the In summary, the duty is to promote the questions asked in the FRC’s report concerning success of the company and, in doing so, corporate culture and provide their thoughts have regard to, amongst other matters, the on what they see within BAE Systems. -

Chronology, 1963–89

Chronology, 1963–89 This chronology covers key political and economic developments in the quarter century that saw the transformation of the Euromarkets into the world’s foremost financial markets. It also identifies milestones in the evolu- tion of Orion; transactions mentioned are those which were the first or the largest of their type or otherwise noteworthy. The tables and graphs present key financial and economic data of the era. Details of Orion’s financial his- tory are to be found in Appendix IV. Abbreviations: Chase (Chase Manhattan Bank), Royal (Royal Bank of Canada), NatPro (National Provincial Bank), Westminster (Westminster Bank), NatWest (National Westminster Bank), WestLB (Westdeutsche Landesbank Girozentrale), Mitsubishi (Mitsubishi Bank) and Orion (for Orion Bank, Orion Termbank, Orion Royal Bank and subsidiaries). Under Orion financings: ‘loans’ are syndicated loans, NIFs, RUFs etc.; ‘bonds’ are public issues, private placements, FRNs, FRCDs and other secu- rities, lead managed, co-managed, managed or advised by Orion. New loan transactions and new bond transactions are intended to show the range of Orion’s client base and refer to clients not previously mentioned. The word ‘subsequently’ in brackets indicates subsequent transactions of the same type and for the same client. Transaction amounts expressed in US dollars some- times include non-dollar transactions, converted at the prevailing rates of exchange. 1963 Global events Feb Canadian Conservative government falls. Apr Lester Pearson Premier. Mar China and Pakistan settle border dispute. May Jomo Kenyatta Premier of Kenya. Organization of African Unity formed, after widespread decolonization. Jun Election of Pope Paul VI. Aug Test Ban Take Your Partners Treaty. -

Schroder ISF Global Recovery Management Company Schroder Investment Management (Europe) S.A

Fund objectives and investment policy The fund aims to provide capital growth in excess of the MSCI World (Net TR) Index after fees have been deducted over a three to five year period by investing in equities of companies worldwide that have suffered a severe set back in either share price or profitability. Relevant risk as associated with this Fund are shown overleaf and should be carefully considered before making any investment. Above is the Investment Objective of the fund. For details on the fund’s Investment Policy please see the KIID. Past Performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall. Share class performance (%) Fund facts Cumulative Fund manager Liam Nunn 1 month 3 months YTD 1 year 3 years 5 years Since inception Andrew Lyddon performance Simon Adler Nick Kirrage Share class (Net) 2,1 -2,2 19,1 46,4 25,2 54,3 69,8 Managed fund since 28.02.2020 ; 09.10.2013 ; Target 2,5 5,9 17,9 29,8 51,9 99,7 139,1 01.11.2018 ; 09.10.2013 Fund management Schroder Investment Comparator 1 1,6 0,8 17,3 31,4 26,5 55,9 78,3 company Management (Europe) Comparator 2 1,9 2,4 15,0 31,5 36,6 70,1 85,1 S.A. -

M&G Index Tracker Fund

M&G Index Tracker Fund a sub-fund of M&G Investment Funds (2) Annual Short Report May 2021 For the year ended 31 May 2021 M&G Index Tracker Fund Fund information The Authorised Corporate Director (ACD) of and local movement restrictions that have been enacted by M&G Investment Funds (2) presents its Annual Short Report for various governments. M&G Index Tracker Fund which contains a review of the fund’s investment activities and investment performance during the Investment objective and policy up to period. The ACD’s Annual Long Report and audited Financial 27 May 2021 Statements for M&G Investment Funds (2), incorporating all the sub-funds and a Glossary of terms is available free of charge The fund is designed to track the FTSE All-Share Index. The fund either from our website at www.mandg.co.uk/reports or by calling manager has full discretionary investment management powers M&G Customer Relations on 0800 390 390. within the confines of this investment objective of the fund. An annual assessment report is available which shows the value Investment objective from 28 May 2021 provided to investors in each of M&G’s UK-based funds. The assessment report evaluates whether M&G’s charges are justified The fund aims to track the performance of the FTSE All-Share in the context of the overall service delivered to its investors. The Index, gross of the ongoing charge figure (OCF). The return report can be found at www.mandg.co.uk/valueassessment received by shareholders will be reduced by the effects of charges. -

Accenture Retirement Savings Plan

Accenture Retirement Savings Plan Statement of Investment Principles – Default Investment Options 27 September 2019 1. Background Members who do not make an investment choice are invested in the Plan’s default investment options. The Trustee has selected the Lifestyle Strategy - Drawdown Focus as the default investment option. This is the current default arrangement for new joiners to the Plan. Prior to January 2016, new joiners to the Auto Enrolment Section were auto- enrolled into Flexicycle. Flexicycle was closed to new members in January 2016 (and most members were transferred to the Lifestyle Strategy – Drawdown Focus). However, Flexicycle continues to operate for members that were already in the de-risking phase and purchasing annuity protection funds at this date and who have not selected an alternative investment option. Members invested via Flexicycle continue to have the option to switch out to the other investment options at any time. 2. Investment Strategy 2.1 Investment Aims, Objectives and Expected Returns The Lifestyle Strategy - Drawdown Focus aims to generate capital growth over the long term. In the years prior to retirement, the lifestyle aims to reduce the volatility of the member’s expected pension pot through investing in a diversified portfolio that aims to provide a balance between risk and return. This, together with new contributions from members and the Principal Employer, will provide a fund at retirement with which to transfer to an arrangement offering the facility to drawdown an income during retirement. The Flexicycle aims to generate capital growth over the long term. In the years prior to retirement, the Flexicycle aims to reduce the volatility of the annuity income the member can secure at retirement and the value of their tax free cash lump sum. -

Morningstar Report

Report as of 02 Oct 2021 Threadneedle Monthly Extra Income Fund Retail Income GBP Morningstar® Category Morningstar® Benchmark Fund Benchmark Morningstar Rating™ Category_EUCA000916 Morningstar UK Moderately 20% ICE BofA Sterling Corp&Coll TR QQQ Adventurous Target Allocation NR GBP EUR, 80% FTSE AllSh TR GBP Used throughout report Investment Objective Performance The Fund aims to provide a monthly income with prospects 172 for capital growth over the long term. It looks to provide 154 an income yield higher than the FTSE All-Share Index over 136 rolling 3-year periods, after the deduction of charges. The 118 Fund is actively managed, and invests in a combination of 100 company shares and bonds; typically, between 70-80% in 82 UK company shares and 20%-30% in bonds. 2016 2017 2018 2019 2020 2021-08 12.39 6.59 -5.45 19.10 -5.17 11.72 Fund - - - - 4.52 9.96 Benchmark 13.23 10.00 -6.37 15.67 5.25 9.54 Category Risk Measures Trailing Returns % Fund Bmark Cat Quarterly Returns % Q1 Q2 Q3 Q4 3Y Alpha -4.50 3Y Sharpe Ratio 0.33 3 Months 1.16 0.35 0.46 2021 2.78 4.59 - - 3Y Beta 1.30 3Y Std Dev 14.34 6 Months 6.14 5.16 5.16 2020 -20.71 10.08 -0.11 8.77 3Y R-Squared 89.79 3Y Risk abv avg 1 Year 17.92 15.22 15.32 2019 6.46 2.75 4.10 4.59 3Y Info Ratio -0.54 5Y Risk abv avg 3 Years Annualised 3.80 6.62 6.12 2018 -4.05 8.69 -0.28 -9.09 3Y Tracking Error 5.57 10Y Risk abv avg 5 Years Annualised 4.71 7.20 6.49 2017 3.91 2.73 -0.15 0.01 Calculations use Morningstar UK Moderately Adventurous Target Allocation NR GBP 10 Years Annualised 8.86 8.92 8.05 -

Schroder ISF¹ Sustainable Multi-Asset Income Schroders Investment Conference

Schroder ISF¹ Sustainable Multi-Asset Income Schroders Investment Conference 19–23 October Remi Olu-Pitan Marketing material for professional Head of Multi-Asset Growth investors or advisers only. and Income ¹Schroder International Selection Fund is referred to as Schroder ISF. Covid-19 has made the hunt for income even more difficult The virus has caused a dividend crisis Dividend cuts typically follow a fall in earnings Dividend futures¹ have fallen sharply Fall in earnings/ dividends 1970s 1980s 1990s Dotcom bubble 2009 Index 0% 400 -5% -3% 350 -5% -6% -10% 300 -15% -12% 250 -20% -19% -20% -20% -25% -22% 200 -30% 150 -31% -35% 100 -40% 50 -45% -46% -50% 0 2008 2010 2012 2014 2016 2018 2020 Fall in earnings Dividend cuts Eurostoxx FTSE 100 Source: Schroders. Datastream, UBS 31 August 2020. ¹A dividend future is an exchange-traded derivative contract that allows investors to take positions on future dividend payments. 2 Incorporating ESG can help Income from sustainable companies might be less at risk of impairment Companies that cancelled dividends have worse Companies with good sustainability tend to have sustainability scores lower leverage and stronger long-term growth Average sustainability score Debt to equity¹ 0% 140% 120% -1% 100% -2% 80% -3% 60% 40% -4% IBES EPS LT growth forecast² -5% 10% -6% 8% -7% 6% -8% 4% -9% 2% Dividend cancelled Dividend continued Sustainability below sector avg Sustainability above sector avg Source: Schroders, as at 31 May 2020. The universe is MSCI World Index. Sustainability score is based on our proprietary tool, SustainEx. SustainEx is a robust, objective framework to measure the social and environmental costs companies impose, or the benefits they provide, which are not currently recognised as financial costs or benefits. -

Annual Report and Accounts 2018 01 Overview Performance Highlights for the Year to 31 March 2018

3i Group plc Overview Governance Introduction 01 Chairman’s introduction 58 Performance highlights 02 Board of Directors and Executive Committee 60 Chairman’s statement 02 Nominations Committee report 65 Chief Executive’s statement 04 Audit and Compliance Committee report 66 Action 08 Valuations Committee report 70 Directors’ remuneration report 73 Our business Relations with shareholders 83 Our business at a glance 10 Additional statutory and corporate governance information 84 Our business model 12 Our strategic objectives 14 Audited financial statements Key performance indicators 16 Private Equity 18 Consolidated statement of comprehensive income 92 Infrastructure 25 Consolidated statement of financial position 93 Performance, risk and sustainability Consolidated statement of changes in equity 94 Consolidated cash flow statement 95 Financial review 29 Company statement of financial position 96 Investment basis 35 Company statement of changes in equity 97 Reconciliation of Investment basis and IFRS 39 Company cash flow statement 98 Alternative Performance Measures 43 Significant accounting policies 99 Risk management 44 Notes to the accounts 104 Principal risks and mitigations 47 Independent Auditor’s report 139 Sustainability 52 Portfolio and other information 20 Large investments 148 Strategic report: Portfolio valuation – an explanation 150 pages 2 to 56. Information for shareholders 152 Directors’ report: pages Glossary 154 58 to 72 and 83 to 90. For definitions of our financial terms, used throughout this report, please see Directors’ remuneration our glossary on pages 154 to 156. report: pages 73 to 82. Consistent with our approach since the introduction of IFRS 10 in 2014, the financial data presented in the Overview and Strategic report is taken from the Investment basis financial statements. -

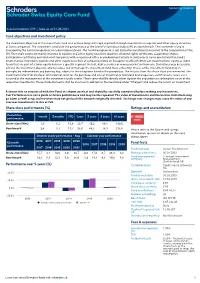

Fund Objectives and Investment Policy Share Class

Fund objectives and investment policy The investment objective of this investment fund is to achieve long-term capital growth through investments in equities and other equity securities of Swiss companies. The investment fund uses the performance of the Swiss Performance Index (SPI) as a benchmark. The investment fund is managed by the fund management on a discretionary basis. The fund management is not limited to investments pursuant to the composition of the SPI. The fund's assets are mainly invested in equities and other equity securities (equities, dividend rights certificates, cooperative shares, participation certificates and similar) of companies with a registered office or predominant activity in Switzerland. Up to one-third of the fund's assets may be invested in equities and other equity securities of companies listed on European and North American stock markets, equity or index funds that are part of a Swiss equity index or a specific segment thereof, debt securities or money market instruments. Derivatives may be used to achieve the investment objective and to reduce risk or manage the investment fund more efficiently. Shares of the investment fund may, in principle, be redeemed on any banking day, subject to the exceptions listed in the prospectus. The returns from this share class are reinvested. The investment fund shall also bear all incidental costs for the purchase and sale of investments (standard brokerage fees, commissions, taxes, etc.) incurred in the management of the investment fund's assets. These costs shall be directly offset against the acquisition or redemption value of the respective investments. These incidental costs shall be incurred in addition to the fees listed under “Charges” and reduce the return on investment. -

Standard Life Aberdeen (SLA); FTSE 100; Financial Services

Selling: Standard Life Aberdeen (SLA); FTSE 100; Financial Services Managing a portfolio is a lot like managing a garden. In gardening there are regular recurring tasks such as trimming back fast-growing plants and replacing unattractive plants with more attractive alternatives. In a portfolio this means regularly trimming back oversized positions and replacing unattractive holdings with more attractive alternatives. Average purchase price Current price Holding period (including investment in Aberdeen AM) £3.76 £2.90 Feb 2016 to Apr 2021 (5yrs 2mo) Capital gain Dividend income Annualised return (including return of capital from de-mergers) -13.4% 31.2% 4.0% “Standard Life Aberdeen is one of the world’s largest investment companies, the largest active manager in the UK and one of the largest in Europe. It has a significant global presence and the scale and expertise to help clients meet their investment goals.” Overview Standard Life Aberdeen (SLA) originally joined the model portfolio in 2016 as Aberdeen Asset Management, which was then the second largest active fund manager in the UK (second only to Schroders). This investment worked out well, with the 2017 merger of Aberdeen and Standard Life leading to annualised return of 17% at the merger date. I decided to hold on to the SLA shares post merger because Standard Life was a leading asset manager and the combined group promised additional economies of scale and a more diverse and robust business. Four years later and as a more experienced investor, I now think both companies lacked durable competitive advantages and I think that’s true of the combined business too.