Fitch Ratings ING Groep N.V. Ratings Report 2020-10-15

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Network Risk and Key Players: a Structural Analysis of Interbank Liquidity∗

Network Risk and Key Players: A Structural Analysis of Interbank Liquidity∗ Edward Denbee Christian Julliard Ye Li Kathy Yuan June 4, 2018 Abstract We estimate the liquidity multiplier and individual banks' contribution to systemic liquidity risk in an interbank network using a structural model. Banks borrow liquid- ity from neighbours and update their valuation based on neighbours' actions. When the former (latter) motive dominates, the equilibrium exhibits strategic substitution (complementarity) of liquidity holdings, and a reduced (increased) liquidity multi- plier dampening (amplifying) shocks. Empirically, we find substantial and procyclical network-generated risks driven mostly by changes of equilibrium type rather than net- work topology. We identify the banks that generate most systemic risk and solve the planner's problem, providing guidance to macro-prudential policies. Keywords: financial networks; liquidity; interbank market; key players; systemic risk. ∗We thank the late Sudipto Bhattacharya, Yan Bodnya, Douglas Gale, Michael Grady, Charles Khan, Seymon Malamud, Farzad Saidi, Laura Veldkamp, Mark Watson, David Webb, Anne Wetherilt, Kamil Yilmaz, Peter Zimmerman, and seminar participants at the Bank of England, Cass Business School, Duisenberg School of Finance, Koc University, the LSE, Macro Finance Society annual meeting, the Stockholm School of Economics, and the WFA for helpful comments and discussions. Denbee (ed- [email protected]) is from the Bank of England; Julliard ([email protected]) and Yuan ([email protected]) are from the London School of Economics, SRC, and CEPR; Li ([email protected]) is from the Ohio State University. This research was started when Yuan was a senior Houblon-Norman Fellow at the Bank of England. -

Third Supplemental Information Memorandum Dated 23 July 2019

Third Supplemental Information Memorandum dated 23 July 2019 LVMH FINANCE BELGIQUE SA (incorporated as société anonyme / naamloze vennootschap) under the laws of Belgium, with enterprise number 0897.212.188 RPR/RPM (Brussels)) EUR 4,000,000,000 Belgian Multi-currency Short-Term Treasury Notes Programme Irrevocably and unconditionally guaranteed by LVMH Moët Hennessy - Louis Vuitton SE (incorporated as European company under the laws of France, and registered under number 775 670 417 (R.C.S. Paris)) The Programme is rated A-1 by Standard & Poor’s Ratings Services, a division of the McGraw-Hill Companies, Inc. and, Arranger Dealers Banque Fédérative du Crédit Mutuel BNP Paribas BRED Banque Populaire Crédit Agricole Corporate and Investment Bank Crédit Industriel et Commercial BNP Paribas Fortis SA/NV Natixis Société Générale ING Belgium SA/NV ING Bank N.V. Belgian Branch Issuing and Paying Agent BNP Paribas Fortis SA/NV This third supplemental information memorandum is dated 23 July 2019 (the “Third Supplemental Information Memorandum”) and is supplemental to, and shall be read in conjunction with, the information memorandum dated 20 October 2015 as supplemented on 21 April 2016 and on 28 April 2017 (the “Information Memorandum”). Unless otherwise defined herein, terms defined in the Information Memorandum have the same respective meanings when used in this Third Supplemental Information Memorandum. As of the date of this Third Supplemental Information Memorandum: (i) The Issuer herby makes the following additional disclosure: Moody's assigned on 3 July 2019 a first-time A1 long-term issuer rating and Prime-1 (P-1) short-term rating to LVMH Moët Hennessy Louis Vuitton SE.; (ii) The paragraph 1.17 “Rating(s) of the Programme” of the section entitled “1. -

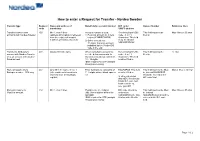

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Effective Credit Risk-Rating Systems

INTERNAL RISK RATINGS Credit Risk-Rating Systems by Tom Yu, Tom Garside, and Jim Stoker n this first of two articles, the authors describe the capabilities, desired attributes, and potential accruing benefits of effective credit risk-rating systems. The practical issues arising in an over- haul, the main theme of the second article, will be shown through a case study of one regional bank’s initiative to upgrade its credit risk man- agement process. redit risk ratings provide a models cannot be improved but portfolios. For corporate lending, common language for that the process of implementation credit scoring has been an impor- describing credit risk is challenging. Ratings are so tight- tant accelerator for securitization. exposure within an organization ly woven into the fabric of most and, increasingly, with parties out- institutions that they are part of the Justification for Change side the organization. As such, they culture. And any significant change A decade of advancements in drive a wide range of credit to the culture is difficult. quantitative measures of credit risk processes—from origination to However, the pressures to have led to better risk management monitoring to securitization to change are mounting from both at the transaction level as well as workout—and it is logical that bet- internal and external sources. the portfolio level. Lenders can ter credit risk ratings can lead to Internally, it may be the desire to actively manage their portfolio better credit risk management. Yet price loans more aggressively or to risks and returns relative to the many lenders are using ratings sys- support a more economically institution’s risk appetite and per- tems that were put in place 10 or attractive CLO structure. -

Testimony of Jamie Dimon Chairman and CEO, Jpmorgan Chase & Co

Testimony of Jamie Dimon Chairman and CEO, JPMorgan Chase & Co. Before the Financial Crisis Inquiry Commission January 13, 2010 Chairman Angelides, Vice-Chairman Thomas, and Members of the Commission, my name is Jamie Dimon, and I am Chairman and Chief Executive Officer of JPMorgan Chase & Co. I appreciate the invitation to appear before you today. The charge of this Commission, to examine the causes of the financial crisis and the collapse of major financial institutions, is of paramount importance, and it will not be easy. The causes of the crisis and its implications are numerous and complex. If we are to learn from this crisis moving forward, we must be brutally honest about the causes and develop an understanding of them that is realistic, and is not – as we are too often tempted – overly simplistic. The FCIC’s contribution to this debate is critical as policymakers seek to modernize our financial regulatory structure, and I hope my participation will further the Commission’s mission. The Commission has asked me to address a number of topics related to how our business performed during the crisis, as well as changes implemented as a result of the crisis. Some of these matters are addressed at greater length in our last two annual reports, which I am attaching to this testimony. While the last year and a half was one of the most challenging periods in our company’s history, it was also one of our most remarkable. Throughout the financial crisis, JPMorgan Chase never posted a quarterly loss, served as a safe haven for depositors, worked closely with the federal government, and remained an active lender to consumers, small and large businesses, government entities and not-for-profit organizations. -

Company Presentation

ATRIUM – COMPANY PRESENTATION THE LEADING OWNER & MANAGER OF CENTRAL EASTERN EUROPEAN SHOPPING CENTRES May 2017 / Based on 2016 full-year results ATRIUM – LEADING OWNER & MANAGER OF CEE SHOPPING CENTRES A UNIQUE INVESTMENT OPPORTUNITY Strong management team with a proven track record Central European focus with dominant presence in the most mature & stable countries Robust balance sheet: 28.7% net LTV/ €104m cash Investment grade rating with a “Stable” outlook by Fitch and S&P Balance between solid income producing platform & opportunities for future growth KEY FIGURES 60 properties with a MV of c.€2.6bn and over 1.1 million m² GLA Focus on shopping centres, primarily food-anchored FY16 GRI: €195.8m, NRI: €188.8m Adjusted EPRA EPS: 31.4 €cents, EPRA NAV per share: €5.39* Special dividend of 14 €cents paid in September Board-approved dividend of 27 €cents per share for 2017**, dividend yield >11.5% Research coverage by Bank of America Merrill Lynch, Baader Bank, HSBC, Kempen, Raiffeisen and Wood & co * Including the special dividend. **Subject to any legal and regulatory requirements and restrictions of commercial viability All numbers in this presentation as reported in the 12M results to 31 December 2016 unless explicitly stated otherwise, incl. a 75% stake in Arkady Pankrac 2 FOCUS ON THE MOST MATURE AND STABLE MARKETS IN CEE 100% focus on Central and Eastern Europe (CEE) Poland, Czech Republic, Slovakia: 84% of MV/ 75% of NRI Exposure to investment-grade countries: 89%* 88% of 12M16 GRI is denominated in Euros, 6% in Polish Zlotys, 2% in Czech Korunas, 1% in USD and 3% in other currencies SLOVAKIA 3 POLAND RUSSIA 7 21 HUNGARY 22 ROMANIA GEOGRAPHIC MIX OF THE PORTFOLIO 1 11% 1618%% CentralCentral European European countries countries 5% (PL, CZ, SK) CZECH REP. -

Nordea Group Annual Report 2018

Annual Report 2018 CEO Letter Casper von Koskull, President and Group CEO, and Torsten Hagen Jrgensen, Group COO and Deputy CEO. Page 4 4 Best and most accessible advisory, with an 21 easy daily banking experience, delivered at scale. Page 13 Wholesale Banking No.1 relationship Asset & Wealth bank in the Nordics Management with operational Personal Banking 13 excellence. Page 21 Commercial & Business Banking Our vision is to become the lead- ing Asset & Wealth Manager in the 25 Nordic market by 2020. Page 25 Best-in-class advisory and digital experience, 17 ef ciency and scale with future capabilities in a disruptive market. Page 17 Annual Report 2018 Contents 4 CEO letter 6 Leading platform 10 Nordea investment case – strategic priorities 12 Business Areas 35 Our people Board of Directors’ report 37 The Nordea share and ratings 40 Financial Review 2018 46 Business area results 49 Risk, liquidity and capital management 67 Corporate Governance Statement 2018 76 Non-Financial Statement 78 Conflict of interest policy 79 Remuneration 83 Proposed distribution of earnings Financial statements 84 Financial Statements, Nordea Group 96 Notes to Group fi nancial statements 184 Financial statements Parent company 193 Notes to Parent company fi nancial statements 255 Signing of the Annual Report 256 Auditor’s report Capital adequacy 262 Capital adequacy for the Nordea Group 274 Capital adequacy for the Nordea Parent company Organisation 286 Board of Directors 288 Group Executive Management 290 Main legal structure & Group organisation 292 Annual General Meeting & Financial calendar This Annual Report contains forward-looking statements macro economic development, (ii) change in the competitive that reflect management’s current views with respect to climate, (iii) change in the regulatory environment and other certain future events and potential fi nancial performance. -

Moody's Investor Service. Rating Symbols and Definitions

Rating Symbols and Definitions JANUARY 2011 MARCH 2008 Table of Contents Preface 2 Other Rating Services 29 Moody’s Standing Committee on Internal Ratings ...................................................................29 Rating Systems & Practices 3 Insured Ratings ...................................................................29 General Credit Rating Services 4 Enhanced Ratings ...............................................................29 Long-Term Obligation Ratings ............................................4 Underlying Ratings .............................................................29 Long-Term Issuer Ratings..................................................... 5 Other Rating Symbols 30 Hybrid Indicator (hyb) ......................................................... 5 Expected ratings - e ............................................................30 Medium-Term Note Program Ratings ............................... 5 Provisional Ratings - (P) .....................................................30 Short-Term Obligation Ratings ........................................... 5 Refundeds - # ......................................................................30 Short-Term Issuer Ratings ...................................................6 Withdrawn - WR .................................................................30 Sector Specific Credit Rating Services 7 Not Rated - NR ...................................................................30 US Municipal Short-Term Debt and Demand Not Available - NAV ...........................................................30 -

PUBLIC SECTION BNP Paribas 165(D)

PUBLIC SECTION OCTOBER 1, 2014 PUBLIC SECTION BNP Paribas 165(d) Resolution Plan Bank of the West IDI Resolution Plan This document contains forward-looking statements. BNPP may also make forward-looking statements in its audited annual financial statements, in its interim financial statements, in press releases and in other written materials and in oral statements made by its officers, directors or employees to third parties. Statements that are not historical facts, including statements about BNPP’s beliefs and expectations, are forward-looking statements. These statements are based on current plans, estimates and projections, and therefore undue reliance should not be placed on them. Forward-looking statements speak only as of the date they are made, and BNPP undertakes no obligation to update publicly any of them in light of new information or future events. CTOBER O 1, 2014 PUBLIC SECTION TABLE OF CONTENTS 1. Introduction ........................................................................................................................4 1.1 Overview of BNP Paribas ....................................................................................... 4 1.1.1 Retail Banking ....................................................................................... 5 1.1.2 Corporate and Investment Banking ....................................................... 5 1.1.3 Investment Solutions ............................................................................. 6 1.2 Overview of BNPP’s US Presence ........................................................................ -

Bank Resolution Concepts, Trade-Offs, and Changes in Practices

Phoebe White and Tanju Yorulmazer Bank Resolution Concepts, Trade-offs, and Changes in Practices • As the 2007-08 financial crisis demonstrated, 1. Introduction the failure or near-failure of banks entails heavy costs for customers, the financial During the recent crisis, some of the world’s largest and sector, and the overall economy. most prominent financial institutions failed or nearly failed, requiring intervention and assistance from regulators. Measures • Methods used to resolve failing banks range included extended access to lender-of-last-resort facilities, debt from private-sector solutions such as mergers guarantees, and injection of capital to mitigate the distress.1 and acquisitions to recapitalization through Chart 1 shows some of the largest financial institutions the use of public funds. that failed and/or received government support during the recent crisis. As we can see, these institutions were • The feasibility and cost of these methods large and systemically important. For example, for a brief will depend on whether the bank failure is period in 2009, Royal Bank of Scotland (RBS) was the idiosyncratic or part of a systemic crisis, and largest company by both assets and liabilities in the world. on factors such as the size, complexity, and Table 1 summarizes the interventions and resolutions of interconnectedness of the institution in distress. major financial institutions that experienced difficulties during the recent crisis. The chart and the table indicate • This study proposes a simple analytical the extraordinary levels of distress throughout the system framework—useful to firms and regulators and the unprecedented range of actions taken by resolution alike—for assessing these issues and determining the optimal resolution policy 1 For a discussion of the disruptions and the policy responses during the in the case of particular bank failures. -

SAP® SOLUTIONS and ACCOUNTING STRATEGIES © Copyright 2007 SAP AG

SAP Solution in Detail SAP for Banking ACCOUNTING IN BANKS: SAP® SOLUTIONS AND ACCOUNTING STRATEGIES © Copyright 2007 SAP AG. All rights reserved. HTML, XML, XHTML and W3C are trademarks or registered trademarks of W3C®, World Wide Web Consortium, No part of this publication may be reproduced or transmitted in Massachusetts Institute of Technology. any form or for any purpose without the express permission of SAP AG. The information contained herein may be changed Java is a registered trademark of Sun Microsystems, Inc. without prior notice. JavaScript is a registered trademark of Sun Microsystems, Inc., Some software products marketed by SAP AG and its distributors used under license for technology invented and implemented contain proprietary software components of other software by Netscape. vendors. MaxDB is a trademark of MySQL AB, Sweden. Microsoft, Windows, Excel, Outlook, and PowerPoint are registered trademarks of Microsoft Corporation. SAP, R/3, mySAP, mySAP.com, xApps, xApp, SAP NetWeaver, Duet, PartnerEdge, and other SAP products and services IBM, DB2, DB2 Universal Database, OS/2, Parallel Sysplex, mentioned herein as well as their respective logos are trademarks MVS/ESA, AIX, S/390, AS/400, OS/390, OS/400, iSeries, pSeries, or registered trademarks of SAP AG in Germany and in several xSeries, zSeries, System i, System i5, System p, System p5, System x, other countries all over the world. All other product and System z, System z9, z/OS, AFP, Intelligent Miner, WebSphere, service names mentioned are the trademarks of their respective Netfinity, Tivoli, Informix, i5/OS, POWER, POWER5, POWER5+, companies. Data contained in this document serves informational OpenPower and PowerPC are trademarks or registered purposes only. -

ING Pressrelease

Press release Corporate Communications Amsterdam, 25 February 2021 ING appoints Anne-Sophie Castelnau global head of Sustainability Anne-Sophie Castelnau has been appointed ING’s global head of Sustainability per 1 April 2021. She will succeed Amin Mansour, who fulfilled the role on an interim basis. Anne-Sophie is currently head of Wholesale Banking for ING in France. Anne-Sophie Castelnau (French) joined ING in France in 2005. Before she became head of Wholesale Banking in France, she held various senior management positions, including head of Corporate Lending and head of Client Coverage. Before she joined ING, Anne-Sophie worked for French banks Natixis and Crédit Industriel et Commercial. Since she became head of ING Wholesale Banking in France in 2017, Anne-Sophie has had a strong focus on sustainable finance. She has been involved in bringing over 25 sustainability deals to fruition, including the first sustainability linked loan in France in 2017. Announcements on Anne-Sophie’s successor as head of Wholesale Banking in France will be made as and when appropriate. Note for editors For further information on ING, please visit www.ing.com. Frequent news updates can be found in the Newsroom or via the @ING_news Twitter feed. Photos of ING operations, buildings and its executives are available for download at Flickr. ING presentations are available at SlideShare. Press enquiries Investor enquiries Daan Wentholt ING Group Investor Relations +31 20 576 6386 +31 20 576 6396 [email protected] [email protected] ING PROFILE ING is a global financial institution with a strong European base, offering banking services through its operating company ING Bank.