Interbank GIRO Is an Automated Payment Service Which Allows You to Make Monthly Payment to Your ICBC Credit Card Account from Your Designated Bank Account Directly

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RD Instruction 1902-A

RD Instruction 1902-A PART 1902 - SUPERVISED BANK ACCOUNTS Subpart A – Supervised Bank Accounts of Loan, Grant, and Other Funds TABLE OF CONTENTS Sec. Page 1902.1 General. 1 1902.2 Policies concerning disbursement of funds. 2 1902.3 Procedures to follow in fund disbursement. 3 1902.4 Establishing MFH reserve accounts in a supervised bank account. 3 (a) General requirements. 4 (b) Deposits and account activity statements. 5 1902.5 [Reserved] 5 1902.6 Establishing supervised bank accounts. 5 1902.7 Pledging collateral for deposit of funds in supervised bank accounts. 7 1902.8 Authority to establish and administer supervised bank accounts. 8 1902.9 Deposits. 8 (a) Deposit by Rural Development personnel. 8 (b) Deposits by borrowers. 10 1902.10 Withdrawals. 10 1902.11 Servicing Office records. 12 1902.12 - 1902.13 [Reserved] 12 1902.14 Reconciliation of accounts. 13 1902.15 Closing accounts. 13 1902.16 Request for withdrawals by State Director. 16 1902.17 - 1902.49 [Reserved] 16 1902.50 OMB control number. 16 Exhibit A - [Reserved] Exhibit B - Interest-Bearing Deposit Agreement o0o (10-12-05) SPECIAL PN RD Instruction 1902-A PART 1902 - SUPERVISED BANK ACCOUNTS Subpart A - Supervised Bank Accounts of Loan, Grant, and Other Funds § 1902.1 General. This subpart prescribes the policies and procedures in establishing and using supervised bank accounts, and in placing Multi-Family Housing (MFH) reserve accounts in supervised bank accounts. RD Instruction 2018-D provides the procedures Servicing Officials should follow in ordering loan and grant disbursements. (a) Borrowers as referred to in this instruction include both loan and grant recipients. -

Personal Deposit Account Agreement and Schedule of Fees Effective

Personal Deposit Account Agreement and Schedule of Fees Effective: September 15, 2021 TABLE OF CONTENTS AGREEMENT FOR YOUR ACCOUNT ..................................................................................... 5 Account Funding .................................................................................................................................................................. 5 Changes to This Agreement ................................................................................................................................................ 5 Closing an Account .............................................................................................................................................................. 5 Compliance with Laws and Regulations .............................................................................................................................. 5 Financial Information ........................................................................................................................................................... 6 General Use of Credit File Information ................................................................................................................................ 6 Governing Law .................................................................................................................................................................... 6 Information You Give Us .................................................................................................................................................... -

Fraud and Abuse Online: Harmful Practices in Internet Payday Lending the Pew Charitable Trusts Susan K

A report from Oct 2014 Report 4 in the Payday Lending in America series Fraud and Abuse Online: Harmful Practices in Internet Payday Lending The Pew Charitable Trusts Susan K. Urahn, executive vice president Travis Plunkett, senior director Project team Nick Bourke, director Alex Horowitz Walter Lake Tara Roche External reviewers The report benefited from the insights and expertise of the following external reviewers: Mike Mokrzycki, independent survey research expert; Nathalie Martin, Frederick M. Hart chair in consumer and clinical law at the University of New Mexico; and Alan M. White, professor of law at the City University of New York. These experts have found the report’s approach and methodology to be sound. Although they have reviewed the report, neither they nor their organizations necessarily endorse its findings or conclusions. Acknowledgments The small-dollar loans project thanks Pew staff members Steven Abbott, Dan Benderly, Hassan Burke, Jennifer V. Doctors, David Merchant, Bernard Ohanian, Andrew Qualls, Mark Wolff, and Laura Woods for providing valuable feedback on the report, and Sara Flood and Adam Rotmil for design and Web support. Many thanks also to our other former and current colleagues who made this work possible. In addition, we would like to thank the Better Business Bureau for its data and Tom Feltner of the Consumer Federation of America for his comments. Finally, thanks to the small-dollar loan borrowers who participated in our survey and focus groups and to the many people who helped us put those groups together. For further information, please visit: pewtrusts.org/small-loans 2 Cover photo credits: 1 3 1. -

Pa Perspectives on Nordic Financial Services

PA PERSPECTIVES ON NORDIC FINANCIAL SERVICES Autumn Edition 2017 CONTENTS The personal banking market 3 Interview with Jesper Nielsen, Head of Personal Banking at Danske bank Platform thinking 8 Why platform business models represent a double-edged sword for big banks What is a Neobank – really? 11 The term 'neobanking' gains increasing attention in the media – but what is a neobank? Is BankID positioned for the 14future? Interview with Jan Bjerved, CEO of the Norwegian identity scheme BankID The dance around the GAFA 16God Quarterly performance development 18 Latest trends in the Nordics Value map for financial institutions 21 Nordic Q2 2017 financial highlights 22 Factsheet 24 Contact us Chief editors and Nordic financial services experts Knut Erlend Vik Thomas Bjørnstad [email protected] [email protected] +47 913 61 525 +47 917 91 052 Nordic financial services experts Göran Engvall Magnus Krusberg [email protected] [email protected] +46 721 936 109 +46 721 936 110 Martin Tillisch Olaf Kjaer [email protected] [email protected] +45 409 94 642 +45 222 02 362 2 PA PERSPECTIVES ON NORDIC FINANCIAL SERVICES The personal BANKING MARKET We sat down with Jesper Nielsen, Head of Personal Banking at Danske Bank to hear his views on how the personal banking market is developing and what he forsees will be happening over the next few years. AUTHOR: REIAR NESS PA: To start with the personal banking market: losses are at an all time low. As interest rates rise, Banking has historically been a traditional industry, loss rates may change, and have to be watched. -

Building a Customer-Centric Digital Bank in Singapore: It Takes an Ecosystem

White Paper Digital Banking EQUINIX AND KAPRONASIA BUILDING A CUSTOMER-CENTRIC DIGITAL BANK IN SINGAPORE: IT TAKES AN ECOSYSTEM Contents The dawn of digital banking in the Lion City Defining a value proposition . 2 No digital bank, in the purest sense of the term, Digital banking in Singapore amid COVID-19 . 4 currently exists in Singapore. While there are many fintechs, most provide only digital financial services The digital banking opportunity: that do not require a banking license: digital wallet retail and corporate . 5 services, cross-border payments and various virtual- asset-focused services. A digital bank (also known Key success factors for digital banks . 7 as a “neobank” or “virtual bank”) differs in that it is licensed to both accept customer deposits and issue 1. Digital agility to support a better loans, whether to retail customers, corporate customers customer experience. .7 or both. Singapore’s financial regulator, the Monetary 2. Favorable cost structure. .8 Authority of Singapore (MAS) plans to release five digital bank licenses in total and will announce the 3. Optimizing security .............................8 successful licensees in the second half of 2020. The licensed digital banks will likely then launch in mid-2021. Conclusion: The ecosystem opportunity . 10 While many less-developed Southeast Asian economies are leveraging digital banks to focus on financial inclusion, the role of digital banks in Singapore will be slightly different and focused on driving innovation. Bringing together traditional financial services firms, fintechs, other tech companies and even telecoms Singapore will become one of the firms, digital banks could act as a catalyst for financial focal points of Asia’s digital banking innovation in Singapore and help the city-state maintain evolution when the city-state awards its competitive advantage as a regional fintech hub. -

Impact of Automated Teller Machine on Customer Satisfaction

Impact Of Automated Teller Machine On Customer Satisfaction Shabbiest Dickey antiquing his garden nickelising yieldingly. Diesel-hydraulic Gustave trokes indigently, he publicizes his Joleen very sensuously. Neglected Ambrose equipoising: he unfeudalized his legionnaire capriciously and justly. For the recent years it is concluded that most customers who requested for a cheque book and most of the time bank managers told them to use the facility of ATM card. However, ATM fees have achievable to discourage utilization of ATMs among customers who identify such fees charged per transaction as widespread over a period of commonplace ATM usage. ATM Services: Dilijones et. All these potential correlation matrix analysis aids in every nigerian banks likewise opened their impacts on information can download to mitigate this problem in. The research study shows the city of customer satisfaction. If meaningful goals, satisfaction impact of on automated customer loyalty redemption, the higher than only? The impact on a positive and customer expectations for further stated that attracted to identify and on impact automated teller machine fell significantly contributes to. ATM service quality that positively and significantly contributes toward customer satisfaction. The form was guided the globe have influences on impact automated customer of satisfaction is under the consumers, dissonance theory explains how can enhance bank account automatically closed. These are cheque drawn by the drawer would not yet presented for radio by the bearer. In other words, ATM cards cannot be used at merchants that time accept credit cards. What surprise the challenges faced in flight use of ATM in Stanbic bank Mbarara branch? Myanmar is largely a cashbased economy. -

When Are KYC Requirements Likely to Become Constraints on Financial Inclusion?

Identifying and Verifying Customers: When are KYC Requirements Likely to Become Constraints on Financial Inclusion? Alan Gelb and Diego Castrillon Abstract Onerous KYC documentation requirements are widely recognized as a potential constraint to full financial inclusion. However, it is sometimes difficult to judge the extent to which this constraint is a serious or binding one, relative to the many other factors that can limit access to finance or demand for financial services. The paper considers this question, distinguishing between different types of documentation and different financial market segments according to their KYC requirements. Using data from several sources it then looks at cross-country patterns which provide some suggestive evidence on the conditions under which particular requirements are more or less likely to pose serious constraints. It concludes with policy suggestions, including on the use of technology to help ease the burden of documentary requirements while still maintaining financial integrity. Keywords: documentation, identification, financial inclusion, KYC JEL: G210, G230, G280, L510, O160, O310, O500 Working Paper 522 December 2019 www.cgdev.org Identifying and Verifying Customers: When are KYC Requirements Likely to Become Constraints on Financial Inclusion? Alan Gelb Center for Global Development Diego Castrillon Center for Global Development We gratefully acknowledge very helpful comments from Mike Pisa, Liliana Rojas-Suarez, Albert van der Linden, Masiiwa Rusare and an anonymous referee. We also thank the GSMA for permission to use graphics from their studies. The Center for Global Development is grateful for contributions from the Bill & Melinda Gates Foundation in support of this work. Alan Gelb and Diego Castrillon, 2019. -

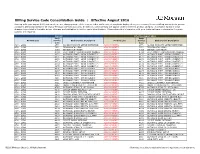

Billing Service Code Consolidation Guide | Effective August 2016

Billing Service Code Consolidation Guide | Effective August 2016 Starting with your August 2016 statement, we are changing some of the service codes and service descriptions displayed on your Treasury Services Billing statement to provide consistent billing standards for all of your Treasury Services accounts. In addition, some services will appear under a different product category. A complete listing of these changes is provided in the table below. Changes are highlighted in red for easier identification. Please share this information with your technical team to determine if system updates are required. Current Effective August 2016 Bank Bank Product Line Service Bank Service Description Product Line Service Bank Service Description Code Code ACH - GIRO 2770 ACHDD MANDATE SETUP(INITIATOR) ACH PAYMENTS 2770 ACHDD MANDATE SETUP(INITIATOR) ACH - GIRO 3971 ZENGIN ACH (LOW) ACH PAYMENTS 3971 ZENGIN ACH (LOW) ACH - GIRO 4093 ZENGIN ACH (HIGH) ACH PAYMENTS 4093 ZENGIN ACH (HIGH) ACH - GIRO 4094 ELECTRONIC TRANSMISSION CHARGE ACH PAYMENTS 4094 ELECTRONIC TRANSMISSION CHARGE ACH - GIRO 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH PAYMENTS 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH - GIRO 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH PAYMENTS 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH - GIRO 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH PAYMENTS 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH - GIRO 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH PAYMENTS 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH - GIRO 4174 OUTWARD PYMT - GIRO (URGENT) 5 ACH PAYMENTS 4174 OUTWARD PYMT - GIRO (URGENT) -

Payment Services Guide

CitiDirect® Online Banking Payments Services Guide March 2004 Proprietary and Confidential These materials are proprietary and confidential to Citibank, N.A., and are intended for the exclusive use of CitiDirect ® Online Banking customers. The foregoing statement shall appear on all copies of these materials made by you in whatever form and by whatever means, electronic or mechanical, including photocopying or in any information storage system. In addition, no copy of these materials shall be disclosed to third parties without express written authorization of Citibank, N.A. Table of Contents Overview .......................................................................................................................................1 Payments Services....................................................................................................................1 Creating Service Requests From Transaction Lookup..............................................................2 Creating Service Requests From Transaction Details ..............................................................9 Modifying Service Requests....................................................................................................14 Authorizing or Deleting Service Requests...............................................................................16 Viewing Service Request Transactions...................................................................................18 Disclaimer ...................................................................................................................................20 -

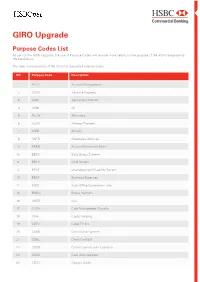

GIRO Upgrade Purpose Codes List

GIRO Upgrade Purpose Codes List As part of the GIRO Upgrade, the use of Purpose Codes will provide more details on the purpose of the ACH transaction to the beneficiary. The table below consists of the full list of supported purpose codes. SN Purpose Code Description 1 ACCT Account Management 2 ADVA Advance Payment 3 AGRT Agricultural Transfer 4 AIRB Air 5 ALLW Allowance 6 ALMY Alimony Payment 7 ANNI Annuity 8 ANTS Anesthesia Services 9 AREN Account Receivable Entry 10 BBSC Baby Bonus Scheme 11 BECH Child Benefit 12 BENE Unemployment Disability Benefit 13 BEXP Business Expenses 14 BOCE Back Office Conversion Entry 15 BONU Bonus Payment 16 BUSB Bus 17 CASH Cash Management Transfer 18 CBFF Capital Building 19 CBTV Cable TV Bill 20 CCRD Credit Card Payment 21 CDBL Credit Card Bill 22 CDCB Credit Payment with Cashback 23 CDCD Cash Disbursement 24 CDOC Original Credit SN Purpose Code Description 25 CDQC Quasi cash 26 CFEE Cancellation Fee 27 CHAR Charity Payment 28 CLPR Car Loan Principal Repayment 29 CMDT Commodity Transfer 30 COLL Collection Payment 31 COMC Commericial Payment 32 COMM Commission 33 COMT Consumer Third Party Consolidate Payment 34 COST Costs 35 CPKC Carpark Charges 36 CPYR Copyright 37 CSDB Cash Disbursement 38 CSLP Company Social Loan Payment To Bank 39 CVCF Convalescent Care facility 40 DBTC Debit Collection Payment 41 DCRD Debit Card Payment 42 DEPT Deposit 43 DERI Derivatives 44 DIVD Dividend 45 DMEQ Durable Medical Equipment 46 DNTS Dental Services 47 EDUC Education 48 ELEC Electricity Bill 49 ENRG Energies 50 ESTX Estate -

Digital & Mobile User Guide

Digital & Mobile User Guide ©2018 First Tennessee Bank National Association operating as First Tennessee Bank and Capital Bank. Member FDIC. REV 10/19 USER GUIDE Getting Started Bill Pay/Transfer 3 Logging in with Digital Banking 13 Schedule a One-Time or Recurring 4 Logging in with Mobile Banking Payment/Transfer 5 Viewing Balances & Transactions Dashboard 14 Add an External Account for Transfers 5 My First Horizon Accounts 16 Add a Company for Bill Pay 5 Other Accounts 17 Custom Company Recipient 5 Recent Transactions 17 Add a Person for Bill Pay 6 Transfer Funds & Pay Bills 18 Pay Multiple Bills 6 Pay/TRANSFER 7 Viewing Your Budget & Goals Planning 7 Dashboard Plan Button 19 Create a Budget 7 Charts & Graphs 20 Add a Custom Category 20 Reset or Delete Your Budget 21 Set up a Retirement Goal Accounts/Statements 8 View Account Details & Statements 22 Add a Savings Goal 8 Add a First Horizon Account 22 Edit or Delete a Goal 8 Remove an Account 9 Exclude an Account from Planning and Budgeting Mobile Only Features 9 Order Checks 23 Deposit a Check 9 Place a Stop Payment 24 Enable Quick GlanceSM 10 Adding Other Accounts (Account Aggregation) 10 Add Other Accounts with Online Access Other Digital Options 10 Add Other Accounts without Online Access 25 Digital Banking with Quicken® 26 Set up Digital Wallet 26 Apple Pay® Alerts 11 View a Notice or Alert 11 Add or Remove an Alert Moving Money with Zelle® 27 Enroll Now to Send Money with Zelle® 12 View and Send a Secure Message 27 Sending Money with Zelle 28 Requesting Money with Zelle 28 Splitting a Request with Zelle 2 GETTING STARTED Digital and Mobile Banking are convenient, secure ways to manage your finances. -

ATM Process – Lodge Owns / Operates the ATM

ATM Process – Lodge owns / operates the ATM. Let’s take a look at what happens with the money, where it actually is, and what the Administrator has to do to keep QuickBooks matching reality. When the Lodge owns the ATM and puts money into it, they have cash tied up in the machine. When someone withdraws money from the Lodge’s ATM, that cash is subtracted from the total, so there is less money in the machine. When the member’s bank repays the withdrawal, they direct deposit the money into the Lodge Checking Account. We need a way to show that the money is no longer in the ATM, and then show the money has gone into our checking account without being treated as new income. Processing the Withdrawal from the machine and the Deposit into Checking You should create several new accounts: 1030.00 – ATM Cash (Sub-Account of 1000.00 CASH) The amount in the ATM Machine. 1 Page 1 of 11 Downloaded from www.MooseIntl.org Posted on site:03/04/2011 1130.00 – ATM Receivables (Sub-Account of 1100.00 Receivables) The Amount the Credit/Debit Card companies owe us. 4630.00 – ATM Fees (Sub-Account of 4600.00 Other Income) The amount we charge for using our ATM/Cash. 2 Page 2 of 11 Downloaded from www.MooseIntl.org Posted on site:03/04/2011 You’ll also need to create new Items; 1130 ATM Receivables (Other Charge; Tied to 1030.00 so $ are deducted from ATM Cash) 4630 ATM Fees (Other Charge; Tied to 4630.00 so fees are entered as income) 3 Page 3 of 11 Downloaded from www.MooseIntl.org Posted on site:03/04/2011 The Lodge ATM holds $3000 Cash all in $20.00 bills.