Pa Perspectives on Nordic Financial Services

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Neobank Varo on Serving Customers' Needs As P2P Payments See A

AUGUST 2021 Neobank Varo on serving customers’ needs as P2P payments see Nigerian consumers traded $38 million worth of bitcoin on P2P platforms within the past month a rapid rise in usage — Page 12 (News and Trends) — Page 8 (Feature Story) How P2P payments are growing more popular for a range of use cases, and why interoperability will be needed to keep growth robust — Page 16 (Deep Dive) © 2021 PYMNTS.com All Rights Reserved 1 DisbursementsTracker® Table Of Contents WHATʼS INSIDE A look at recent disbursements developments, including why P2P payments are becoming more valuable 03 to consumers and businesses alike and how these solutions are poised to grow even more popular in the years ahead FEATURE STORY An interview with with Wesley Wright, chief commercial and product officer at neobank Varo, on the rapid 08 rise of P2P payments adoption among consumers of all ages and how leveraging internal P2P platforms and partnerships with third-party providers can help FIs cater to customer demand NEWS AND TRENDS The latest headlines from the disbursements space, including recent survey results showing that almost 12 80 percent of U.S. consumers used P2P payments last year and how the U.K. government can take a page from the U.S. in using instant payments to help SMBs stay afloat DEEP DIVE An in-depth look at how P2P payments are meeting the needs of a growing number of consumers, how 16 this shift has prompted consumers to expand how they leverage them and why network interoperability is key to helping the space grow in the future PROVIDER DIRECTORY 21 A look at top disbursement companies ABOUT 116 Information on PYMNTS.com and Ingo Money ACKNOWLEDGMENT The Disbursements Tracker® was produced in collaboration with Ingo Money, and PYMNTS is grateful for the companyʼs support and insight. -

Interbank GIRO Is an Automated Payment Service Which Allows You to Make Monthly Payment to Your ICBC Credit Card Account from Your Designated Bank Account Directly

Interbank GIRO Frequently Asked Questions: 1. What is Interbank GIRO? Interbank GIRO is an automated payment service which allows you to make monthly payment to your ICBC Credit Card account from your designated bank account directly. The amount will be deducted from your designated bank account and paid to ICBC every month. All you need to do is to ensure that the designated bank account has sufficient funds every month. 2. What is the benefit of using Interbank GIRO? Interbank GIRO is a convenient, paperless and cashless payment method. It enables you to make hassle-free monthly payments to ICBC through your designated bank account. There are also no fees charged for the setup. 3. Are there any additional charges for signing up for Interbank GIRO? There are no fees charged for the setup of Interbank GIRO. 4. How can I apply for Interbank GIRO? Simply fill up the Interbank GIRO form, and submit to Credit Card Department. 5. Which banks can I use for Interbank GIRO? You can use any bank that supports Interbank GIRO. 6. How long is the Interbank GIRO application Processing Time? Interbank GIRO applications may take up to 60 days to process, including the processing time required by the deducting bank. We will notify you of your application status as soon as possible. 7. How do I submit the Interbank GIRO form to ICBC Credit Card Department? You can mail the duly signed Original Interbank GIRO form to ICBC Credit Card Department by using the Business Reply Service Envelope attached. Please do not fax the Interbank GIRO form or email the scanned copy of the Interbank GIRO form as the designated bank requires the original signature for verification. -

Online Or Neobanks: Convenience Could Cost You!

Online Or Neobanks: Convenience Could Cost You! As if choosing a property isn’t hard enough, there is also the The main difference between an online/digital bank and a added challenge of selecting the right lender and home loan Neobank is that a Neobank is completely online and does not use from the vast number of options available. any existing infrastructure or systems to operate2. Whether it is your first home, upgraded next home, investment ING and ME are examples of banks using existing banking property or a refinance, deciding where to finance your home infrastructure to offer online finance but they are not Neobanks. loan can be a tough decision – and rightly so. There are over 130 lenders in Australia!1. Plus, there is the added trend of online Online and Neobank lending sound too good to be and Neobank lending. true? More and more Australians are turning to online lenders when Probably because for many, it could be. taking out a loan. Why? Because of convenience, self-service Why? and low interest rates. • Less personalised service – There is less focus on personal Online banks relationships and recommending loans suited to your specific An online bank is an organisation that operates solely, or mostly, situation. online. Emerging fintech lenders promise streamlined home loans • Limited range – Online lenders generally offer a limited range as easy as 1-2-3 through the digital platform. of products – no frills to keep the interest rates down! Do you Some online banks are backed by larger more well-known really know the product that suits you best? traditional banks. -

Building a Customer-Centric Digital Bank in Singapore: It Takes an Ecosystem

White Paper Digital Banking EQUINIX AND KAPRONASIA BUILDING A CUSTOMER-CENTRIC DIGITAL BANK IN SINGAPORE: IT TAKES AN ECOSYSTEM Contents The dawn of digital banking in the Lion City Defining a value proposition . 2 No digital bank, in the purest sense of the term, Digital banking in Singapore amid COVID-19 . 4 currently exists in Singapore. While there are many fintechs, most provide only digital financial services The digital banking opportunity: that do not require a banking license: digital wallet retail and corporate . 5 services, cross-border payments and various virtual- asset-focused services. A digital bank (also known Key success factors for digital banks . 7 as a “neobank” or “virtual bank”) differs in that it is licensed to both accept customer deposits and issue 1. Digital agility to support a better loans, whether to retail customers, corporate customers customer experience. .7 or both. Singapore’s financial regulator, the Monetary 2. Favorable cost structure. .8 Authority of Singapore (MAS) plans to release five digital bank licenses in total and will announce the 3. Optimizing security .............................8 successful licensees in the second half of 2020. The licensed digital banks will likely then launch in mid-2021. Conclusion: The ecosystem opportunity . 10 While many less-developed Southeast Asian economies are leveraging digital banks to focus on financial inclusion, the role of digital banks in Singapore will be slightly different and focused on driving innovation. Bringing together traditional financial services firms, fintechs, other tech companies and even telecoms Singapore will become one of the firms, digital banks could act as a catalyst for financial focal points of Asia’s digital banking innovation in Singapore and help the city-state maintain evolution when the city-state awards its competitive advantage as a regional fintech hub. -

Designing a Sustainable Digital Bank Learning from the Digital Pioneers

IBM Sales and Distribution Banking White Paper Executive Summary Designing a sustainable digital bank Learning from the digital pioneers In an era of unprecedented change, technology offers banking clients greater access to information than ever before. Out of this revolutionary advance, a new class of smarter and more demanding customers has emerged. In tandem, new financial players are moving quickly to offer new compelling digital services. As with every major change triggered by technological advancement, there are clear winners and those who are unable to adapt. Banks that embrace digitization have an opportunity to generate new business value and better engage with their customers. The surge of new entrants riding the digital wave Banking has traditionally been a conservative industry that enjoys rela- tively high barriers to entry due to regulations that restrain access for non-bank competitors. New digital technologies—driven by cloud, mobile, social and analytics—have drastically lower entry barriers. Regulators in many countries have also relaxed regulations to encourage innovations in the banking industry. As a result, many new all-digital financial services firms, unencumbered by older less agile systems are aggressively pursuing customers by addressing their needs in new and dis- tinct ways. For instance, Chinese internet giant Tencent created WeBank hoping to capitalize on its vast user base of microblogging and peer-to- peer chatting services. E-commerce leaders such as Tesco in Europe, Rakuten in Asia-Pacific and Walmart in the US have also entered the IBM Sales and Distribution Banking White Paper Executive Summary banking sector. Globally, entrepreneurs and even traditional ●● Model C, a digital bank subsidiary: Many banking innovators banks are creating digital-only banks or neobanks. -

Latin America: Global Investors' New Fintech Frontier

Co-authored by WHITE PAPER Latin America: Global Investors’ New Fintech Frontier Insights from Leading Banks, Venture Capital and Private Equity Investors 1 LATIN AMERICA: GLOBAL INVESTORS’ NEW FINTECH FRONTIER WHITE PAPER EXECUTIVE OVERVIEW CONTENTS Mega-deals and marquee global 1. A Market Inflection: Global investors are making headlines in Latin Investment in Latin American American fintech. The region is digitally- Fintech .................................................... 3 connected and rife with underbanked populations and a burgeoning talent 2. Insight into LatAm’s Fintech pool. Available early and later-stage Arrival ...................................................... 5 growth capital from both local and global venture capital, private equity and corporate ventures, rounds out 3. Dynamics Driven by Outside the situational factors essential for a Investors ................................................. 8 thriving fintech hub – and accelerates opportunities for founders and funders. 4. Factors for Long Term Success ....12 This paper captures the global investor point-of-view, while exploring the trend 5. Key Questions for the Future ........16 of ecosystem improvements that have led to LatAm’s breakout, including the emergence of new talent, early startup 6. Appendix: Research Sources .........17 successes and ambitious regulatory reform. The paper showcases how these sector changes have invited deeper investor participation – and examines the outside influence of global investors’ new practices and perspectives. It concludes with an exploration of the opportunities and challenges these marketplace shifts create. The insights in this report are based on interviews with leading, active global investors as well as fintech sector trend research. The paper is intended for global investors pursuing or considering the Latin American fintech sector; fintechs in the region open to funding from investors based outside the region; and all others interested in trends and data behind the growth story that is LatAm fintech. -

French Fintech Ecosystem

About Exton Consulting Exton Consulting is a strategy and management consulting firm, founded in 2006 and specializing in financial services: insurance, retail banking, cards and payments, CIB & Asset Management. As a key player in this field, Exton Consulting provides executive boards with the advice and support needed to manage company growth, transformation and innovation. The firm is represented in France, Italy, Germany and Morocco and employs 150 consultants with a high level of expertise and competence. With more than 10 years of experience, Exton Consulting has become a privileged partner in addressing the challenges and opportunities of digital transformation in financial services. In direct contact with the FinTech and entrepreneurial ecosystem, to better support its clients in their innovation projects, Exton Consulting is a founding member of Le Swave, the first French acceleration platform for FinTechs, and a partner of Finance Innovation, an active member of its FinTechs banking and insurance projects labelling committee. For more information: www.extonconsulting.com [email protected] FOREWORD Some observers predicted that the FinTech phenomenon would slow down worldwide at competitive advantages and accelerate their digital transformation. the end of 2016. However, financial start-ups continue to attract investors and 2018 is already proving to be a record year. These are just some of the factors that lead to attractive development opportunities for FinTechs in France. Europe is the region with the strongest growth in 2017 (+121%) and in third place after North America and Asia in terms of invested amounts. The continent has a regulatory In this context, Exton Consulting and the Finance Innovation cluster wanted to framework that favours the emergence of FinTechs (with the European financial passport combine their expertise in order to: and the entry into force of PSD2, which paves the way for open banking). -

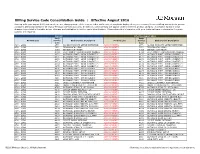

Billing Service Code Consolidation Guide | Effective August 2016

Billing Service Code Consolidation Guide | Effective August 2016 Starting with your August 2016 statement, we are changing some of the service codes and service descriptions displayed on your Treasury Services Billing statement to provide consistent billing standards for all of your Treasury Services accounts. In addition, some services will appear under a different product category. A complete listing of these changes is provided in the table below. Changes are highlighted in red for easier identification. Please share this information with your technical team to determine if system updates are required. Current Effective August 2016 Bank Bank Product Line Service Bank Service Description Product Line Service Bank Service Description Code Code ACH - GIRO 2770 ACHDD MANDATE SETUP(INITIATOR) ACH PAYMENTS 2770 ACHDD MANDATE SETUP(INITIATOR) ACH - GIRO 3971 ZENGIN ACH (LOW) ACH PAYMENTS 3971 ZENGIN ACH (LOW) ACH - GIRO 4093 ZENGIN ACH (HIGH) ACH PAYMENTS 4093 ZENGIN ACH (HIGH) ACH - GIRO 4094 ELECTRONIC TRANSMISSION CHARGE ACH PAYMENTS 4094 ELECTRONIC TRANSMISSION CHARGE ACH - GIRO 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH PAYMENTS 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH - GIRO 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH PAYMENTS 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH - GIRO 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH PAYMENTS 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH - GIRO 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH PAYMENTS 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH - GIRO 4174 OUTWARD PYMT - GIRO (URGENT) 5 ACH PAYMENTS 4174 OUTWARD PYMT - GIRO (URGENT) -

Payment Services Guide

CitiDirect® Online Banking Payments Services Guide March 2004 Proprietary and Confidential These materials are proprietary and confidential to Citibank, N.A., and are intended for the exclusive use of CitiDirect ® Online Banking customers. The foregoing statement shall appear on all copies of these materials made by you in whatever form and by whatever means, electronic or mechanical, including photocopying or in any information storage system. In addition, no copy of these materials shall be disclosed to third parties without express written authorization of Citibank, N.A. Table of Contents Overview .......................................................................................................................................1 Payments Services....................................................................................................................1 Creating Service Requests From Transaction Lookup..............................................................2 Creating Service Requests From Transaction Details ..............................................................9 Modifying Service Requests....................................................................................................14 Authorizing or Deleting Service Requests...............................................................................16 Viewing Service Request Transactions...................................................................................18 Disclaimer ...................................................................................................................................20 -

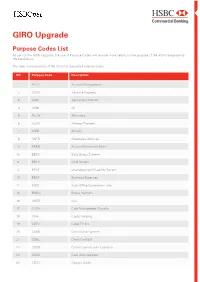

GIRO Upgrade Purpose Codes List

GIRO Upgrade Purpose Codes List As part of the GIRO Upgrade, the use of Purpose Codes will provide more details on the purpose of the ACH transaction to the beneficiary. The table below consists of the full list of supported purpose codes. SN Purpose Code Description 1 ACCT Account Management 2 ADVA Advance Payment 3 AGRT Agricultural Transfer 4 AIRB Air 5 ALLW Allowance 6 ALMY Alimony Payment 7 ANNI Annuity 8 ANTS Anesthesia Services 9 AREN Account Receivable Entry 10 BBSC Baby Bonus Scheme 11 BECH Child Benefit 12 BENE Unemployment Disability Benefit 13 BEXP Business Expenses 14 BOCE Back Office Conversion Entry 15 BONU Bonus Payment 16 BUSB Bus 17 CASH Cash Management Transfer 18 CBFF Capital Building 19 CBTV Cable TV Bill 20 CCRD Credit Card Payment 21 CDBL Credit Card Bill 22 CDCB Credit Payment with Cashback 23 CDCD Cash Disbursement 24 CDOC Original Credit SN Purpose Code Description 25 CDQC Quasi cash 26 CFEE Cancellation Fee 27 CHAR Charity Payment 28 CLPR Car Loan Principal Repayment 29 CMDT Commodity Transfer 30 COLL Collection Payment 31 COMC Commericial Payment 32 COMM Commission 33 COMT Consumer Third Party Consolidate Payment 34 COST Costs 35 CPKC Carpark Charges 36 CPYR Copyright 37 CSDB Cash Disbursement 38 CSLP Company Social Loan Payment To Bank 39 CVCF Convalescent Care facility 40 DBTC Debit Collection Payment 41 DCRD Debit Card Payment 42 DEPT Deposit 43 DERI Derivatives 44 DIVD Dividend 45 DMEQ Durable Medical Equipment 46 DNTS Dental Services 47 EDUC Education 48 ELEC Electricity Bill 49 ENRG Energies 50 ESTX Estate -

Deal Or No Deal: Do Eu Challenger Banks Have a Future in the Uk (And How to Best Prepare for It)?

DEAL OR NO DEAL: DO EU CHALLENGER BANKS HAVE A FUTURE IN THE UK (AND HOW TO BEST PREPARE FOR IT)? By Dora Knezevic In October 2018, N26, a European, digital-only, challenger bank or briefly, neobank, launched in the United Kingdom. With up to one in four British millennials banking with a challenger bank and the market attractive to other digital-only challengers, the Berlin-based neobank’s UK expansion was hardly surprising.1 N26 had already successfully launched across Europe and embarked on an ambitious marketing campaign in the UK, positive about achieving similar success in this new market. A mere year-and-a-half later however, the neobank announced it will be leaving the UK and closing all UK accounts, citing overwhelming uncertainty about the future of its banking license in the UK following the end of the Brexit transition period. Although uncertainty surrounding the Brexit deal outcome is undeniable, Brexit itself was a certainty already when N26 entered the market in 2018. In the year-and-a-half the neobank spent in the UK market however, they did not action a particular contingency plan for addressing it. In fact, behind the scenes, N26 was already dealing with several other challenges, including compliance, a failure to differentiate from competitors and to capture a sufficient customer base. The challenges faced by N26 in the UK are not exclusive to N26 – they are general challenges any European neobank will likely encounter as they enter UK and should consider during the planning of their potential UK expansion. This article will further elaborate on these challenges, beginning with Brexit and subsequently the additional market challenges, overlooked by N26, relating to UK expansion with the goal of providing actionable insight for any European neobank considering entering the attractive UK market. -

The First Swiss Digital Account for Smes

Press Release SIX FinTech Ventures and HTGF invest CHF 0.7 million in fintech Relio. The first Swiss digital account for SMEs. Zurich, 26.04.2021: Challenger banks such as Revolut, Neon and Yapeal have already won over many private customers in Switzerland. The startup Relio will soon launch the first Swiss digital account tailored to SMEs. The fintech is founded by Lav Odorovic, who previously built the neobank Penta in Germany as CEO and founder. Relio is aiming for a fintech license and is now announcing a pre-seed financing round of CHF 0.7 million with SIX FinTech Ventures and High-Tech Gründerfonds (HTGF). Turning the concept of a business account on its head. Everyone who starts a new venture needs a company account. While this can be set up quickly, the process can last for weeks. This is because every bank is required by law to check the identity of a new customer, how the business model works and the source of funds. This is more complicated for SMEs than for retail customers. Companies with foreign founders, from regulated industries, or that have holding structures raise complex compliance issues. Some customers report up to 20 interactions with banks before an account can be opened. The compliance department is generally positioned as a limiting factor around banking. Relio is turning this model on its head and building its digital business account around compliance at its core. "Our promise is compliance without complications," says Lav Odorovic, founder and CEO of Relio. Thanks to the new approach, even complex SMEs will be able to obtain an account with a Swiss IBAN quickly and without red tape.