Lloyds Banking Group PLC

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Investor Update First Half 2013 Results

Santander UK plc Investor Update First Half 2013 Results July 2013 United Kingdom Disclaimer 1 Santander UK plc (“Santander UK”) is a subsidiary of Banco Santander, S.A. (“Santander”). Santander UK and Santander both caution that this presentation may contain forward-looking statements. Such forward-looking statements are found in various places throughout this presentation. Words such as “believes”, “anticipates”, “expects”, “intends”, “aims” and “plans” and other similar expressions are intended to identify forward-looking statements, but they are not the exclusive means of identifying such statements. Forward-looking statements include, without limitation, statements concerning our future business development and economic performance. These forward-looking statements are based on management’s current expectations, estimates and projections and both Santander UK and Santander caution that these statements are not guarantees of future performance. We also caution readers that a number of important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. We have identified certain of these factors on pages 310 to 325 of the Santander UK Annual Report on Form 20-F for 2012. Investors and others should carefully consider the foregoing factors and other uncertainties and events. Undue reliance should not be placed on forward-looking statements when making decisions with rerespectspect to Santander UK, Santander and/and/oror their securities. The information in this presentation, including any forward -looking statements, speak only as of the date on which they are made, and we do not undertake any obligation to update or revise any of them, whether as a result of new information, future events or otherwise. -

18 February 2019 Solvency and Diversification in Insurance Remain Key Strengths Despite Change in Structure

FINANCIAL INSTITUTIONS ISSUER IN-DEPTH Lloyds Banking Group plc 18 February 2019 Solvency and diversification in insurance remain key strengths despite change in structure Summary RATINGS In 2018, Lloyds Banking Group plc (LBG) altered its structure to comply with the UK's ring- Lloyds Banking Group plc Baseline Credit a3 fencing legislation, which requires large banks to separate their retail and SME operations, Assessment (BCA) and deposit taking in the European Economic Area (EEA) from their other activities, including Senior unsecured A3 Stable the riskier capital markets and trading business. As part of the change, LBG designated Lloyds Bank plc as the“ring-fenced” entity housing its retail, SME and corporate banking operations. Lloyds Bank plc It also assumed direct ownership of insurer Scottish Widows Limited, previously a subsidiary Baseline Credit A3 Assessment (BCA) of Lloyds Bank. The changes had little impact on the creditworthiness of LBG and Lloyds Adjusted BCA A3 Bank, leading us to affirm the deposit and senior unsecured ratings of both entities. Scottish Deposits Aa3 Stable/Prime-1 Widows' ratings were unaffected. Senior unsecured Aa3 Stable » LBG's reorganisation was less complex than that of most UK peers. The Lloyds Lloyds Bank Corporate Markets plc Banking Group is predominantly focused on retail and corporate banking, and the Baseline Credit baa3 required structural changes were therefore relatively minor. The group created a small Assessment (BCA) separate legal entity, Lloyds Bank Corporate Markets plc (LBCM), to manage its limited Adjusted BCA baa1 Deposits A1 Stable/Prime-1 capital markets and trading operations, and it transferred its offshore subsidiary, Lloyds Issuer rating A1 Stable Bank International Limited (LBIL), to LBCM from Lloyds Bank. -

Using Replicated Ledger to Reduce Swift Costs

WHITE PAPER USING REPLICATED LEDGER TO REDUCE SWIFT COSTS Abstract Nientibus et harum la aliquos que dunt harunte nat qui assimin ctincti nimoloratur? Quis sin enim expello rescitis aliberiosam, sumendu cienimil es ab in pelibus antiunt, eatur sit volorec tetur, occus asi suntiss imporer eperis dolupta que quid quatis mo volorit quas maio. Im acest, eos si beat. Ur? Nonseque reribus. Itatium re, nissi nullupietur audis sit adis con non corrum fugias eosae nones nonsenimus Itate esto moluptatur autatis sinctota dolent labo. Sum autem reriossum eos acerestectur rem que et haribus vel etur Introduction This paper proposes an approach to build a payment product that could be deployed across units of same bank or banks which have correspondent relationships, to reduce SWIFT message costs and to conserve liquidity by reducing need for Settlement and Nostro accounts. The paper proposes an outline of a product that implements a replicated, single wrapper around existing ledgers of such bank units to enable quick, irrevocable, tamper-proof approach to managing electronic payments between correspondent bank units. Existing ledgers of the bank would not be replaced or disturbed. Instead a wrapper application would be deployed that tracks specific entries in the ledger and replicates the changes to all members. This enables each member bank to see the same ledger at the same time and also be guaranteed of its accuracy. For this purpose, it is recommended the product be built using Blockchain for established and proven security. Such a replicated ledger would reduce active, recurring costs of using SWIFT network to pass payment messages. This will also reduce the much larger passive cost of holding funds in a non- remunerative settlement a/c with the correspondent bank. -

Wholesale Banking Presentation (PDF)

Wholesale Banking Perry Pelos Senior Executive Vice President May 11, 2017 © 2017 Wells Fargo & Company. All rights reserved. Business Overview Wholesale Banking overview Wholesale Banking operates ten major lines of business, serving diverse market and customer segments including business banking, middle market, and large corporates, as well as financial institutions . 32,000+ team members Presence . 627 domestic locations . 42 countries and territories . $807.8B Average assets 1Q17 . $466.0B Average deposits . $466.3B Average loans Financials . $7.0B Revenue . $2.1B Net income Wells Fargo 2017 Investor Day Wholesale Banking 2 Revenue and income contribution Share of Wells Fargo Wholesale Revenue by Category Revenue and Net Income Investment Banking Service charges (1) 2016 Revenue Insurance Loan and Letter of Credit fees Trading gains Trust & investment fees 32% Operating leases 68% Wholesale: 32% Equity investment gains Other 2016 Net income Net interest income 62% 38% Wholesale: 38% (1) Includes Treasury Management fees. Wells Fargo 2017 Investor Day Wholesale Banking 3 Financial performance ($ in millions) Revenue $28,542 $25,398 $25,904 Net Income 2014 2015 2016 $8,199 $8,194 $8,235 Provision Expense $1,073 $27 -$382 2014 2015 2016 2014 2015 2016 Noninterest Expense $16,126 $13,831 $14,116 2014 2015 2016 Shading = Operating lease revenue and expense, respectively. Wells Fargo 2017 Investor Day Wholesale Banking 4 Continued strong credit quality Credit quality remained strong with net charge-offs of 7 bps in 1Q17, as oil and gas portfolio -

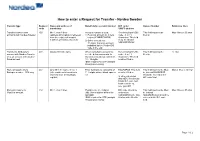

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Hsbc to Acquire Lloyds Banking Group Onshore Assets in the Uae

Ab c 29 March 2012 HSBC TO ACQUIRE LLOYDS BANKING GROUP ONSHORE ASSETS IN THE UAE HSBC Bank Middle East Ltd (‘HSBC’), an indirect wholly-owned subsidiary of HSBC Holdings plc, has entered into an agreement to acquire the onshore retail and commercial banking business of Lloyds Banking Group (‘Lloyds’) in the United Arab Emirates (‘UAE’). The value of the gross assets being acquired is US$769m as at 31 December 2011. The transaction, which is subject to regulatory approvals, is expected to complete in 2012. HSBC’s largest operations in the MENA region are based in the UAE where HSBC enjoys a market-leading trade and commercial banking presence, in addition to the largest international retail banking and wealth management business. The business being acquired from Lloyds has approximately 8,800 personal and commercial customers and a loan book of approximately US$573m as at 31 December 2011. Commenting on the acquisition, Simon Cooper, Deputy Chairman and Chief Executive Officer of HSBC in MENA, said: “HSBC is the leading international bank in the UAE and the addition of Lloyds’ strong presence in retail and commercial banking is highly complementary to our business. The acquisition underscores the strategic importance of the UAE, and of the MENA region as a whole, to HSBC.” Media enquiries to: Tim Harrison + 971 4 4235632 [email protected] Brendan McNamara +44 (0) 20 7991 0655 [email protected] ends/more Registered Office and Group Head Office: This news release is issued by 8 Canada Square, London E14 5HQ, United Kingdom Web: www.hsbc.com HSBC Holdings plc Incorporated in England with limited liability. -

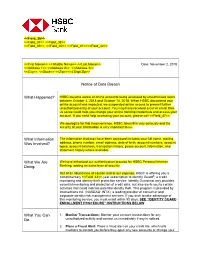

HSBC Became Aware of Online Accounts Being Accessed by Unauthorized Users Between October 4, 2018 and October 14, 2018

<<Field_36>> <<Field_37>> <<Field_38>> <<Field_39>>, <<Field_40>> <<Field_41>><<Field_42>> <<First Name>> << Middle Name>> <<Last Name>> Date: November 2, 2018 <<Address 1>> <<Address 2>> <<Address 3>> <<City>>, <<State>> <<Zip>><<4 Digit Zip>> Notice of Data Breach What Happened? HSBC became aware of online accounts being accessed by unauthorized users between October 4, 2018 and October 14, 2018. When HSBC discovered your online account was impacted, we suspended online access to prevent further unauthorized entry of your account. You may have received a call or email from us so we could help you change your online banking credentials and access your account. If you need help accessing your account, please call <<Field_47>>. We apologize for this inconvenience. HSBC takes this very seriously and the security of your information is very important to us. What Information The information that may have been accessed includes your full name, mailing Was Involved? address, phone number, email address, date of birth, account numbers, account types, account balances, transaction history, payee account information, and statement history where available. What We Are We have enhanced our authentication process for HSBC Personal Internet Doing. Banking, adding an extra layer of security. Out of an abundance of caution and at our expense, HSBC is offering you a complimentary <<Field_43>>-year subscription to Identity Guard®, a credit monitoring and identity theft protection service. Identity Guard not only provides essential monitoring and protection of credit data, but also alerts you to certain activities that could indicate potential identity theft. This program is provided by Intersections Inc. (NASDAQ: INTX), a leading provider of consumer and corporate identity risk management services. -

Natwest, Lloyds Bank and Barclays Pilot UK's First Business Banking Hubs

NatWest, Lloyds Bank and Barclays pilot UK’s first business banking hubs NatWest, Lloyds Bank and Barclays have announced that they will pilot the UK’s first shared business banking hubs. The first hub will open its door in Perry Barr, Birmingham today. The pilot will also see five other shared hubs open across the UK in the coming weeks The hubs have been specifically designed to enable businesses that manage cash and cheque transactions to pay in large volumes of coins, notes and cheques and complete cash exchange transactions. They will be available on a trial basis to pre-selected business clients in each local area and will offer extended opening times (8am to 8pm) 7 days a week, providing business and corporate customers more flexibility to manage their day-to-day finances. The hubs will be branded Business Banking Hub and they have been designed to enable business customers from Natwest, Lloyds Bank and Barclays to conduct transactions through a shared facility. Commenting on the launch of the pilot, Deputy CEO of NatWest Holdings and CEO of NatWest Commercial and Private Banking Alison Rose said: “We have listened to what our business customers really want from our cash services. It is now more important than ever that we continue to offer innovative services, and we are creating an infrastructure that allows small business owners and entrepreneurs to do what they do best - run their business. I look forward to continued working with fellow banks to ensure the UK's businesses are getting the support they deserve." Commenting on the support this will provide businesses, Paul Gordon, Managing Director of SME and Mid Corporates at Lloyds Bank Commercial Banking said: “SMEs are the lifeblood of the UK economy. -

Country Financial Institutions Swift Rma

LIST OF RMA EXCHANGED (DANH SÁCH NGÂN HÀNG TRAO ĐỔI RMA) COUNTRY FINANCIAL INSTITUTIONS SWIFT RMA Wells Fargo Bank, N.A, New York International 1 Branch PNBPUS3N 2 Wells Fargo Bank, N.A PNBPUS33 3 Wells Fargo Bank, N.A WFBIUS6W 4 JPMorgan Chase Bank, N.A CHASUS33 5 CitiBank, N.A CITIUS33 6 Woori America Bank HVBKUS3N 7 Woori America Bank, Los Angeles HVBKUS61 8 International Finance Corporate IFCWUS33 United States 9 Industrial & Commercial Bank of China ICBKUS33 10 Shinhan Bank SHBKUS33 11 First Bank FBOLUS6L 12 Bank of Tokyo-Mitsubishi UFJ, LTD, NY Branch BOTKUS33 13 Bank of Tokyo-Mitsubishi UFJ, LTD, Chicago Branch BOTKUS4C Bank of Tokyo-Mitsubishi UFJ, LTD, Los Angeles 14 Branch BOTKUS6L 15 UniCredit S.P.A UNCRITMM 16 CitiBank, N.A CITIITMX 17 Intesa Sanpaolo SPA Head Office BCITITMM 20 Commerzbank AG COBAITMM ITALY Industrial & Commercial Bank of China, Milan 21 Branch ICBKITMM 22 Bank of Tokyo-Mitsubishi UFJ, LTD, Milan Branch BOTKITMX Unicredit Bank AG Singapore Branch 23 (HypoVereinsBank AG Singapore Branch) BVBESGSG 24 United Overseas Bank Ltd. Head Office UOVBSGSG 25 JPMorgan Chase Bank, N.A. Singapore Branch CHASSGSG 26 SINGAPORE Bank of Tokyo-Mitsubishi UFJ, LTD, Singapore BranchBOTKSGSX Skandinaviska Enskilda Banken AB (PUBL). 27 Singapore Branch ESSESGSG 28 Mizuho Bank, Ltd. Singapore Branch MHCBSGSG 29 CitiBank, N.A. Singapore Branch CITISGSG 30 Industrial & Commercial Bank of China, Singapore BranchICBKSGSG 31 Deutsche Bank AG DEUTDEFF 32 BHF-BANK Aktiengesellschaft BHFBDEFF GERMANY 33 Landesbank Baden-Wuerttemberg SOLADEST -

Frequently Asked Questions

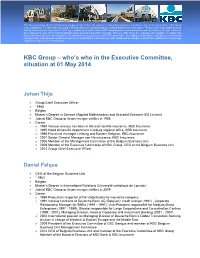

This document is provided for informational purposes only. It does not constitute a solicitation to buy/sell any product or security issued by the KBC Group or its subsidiaries. The information provided in this document is condensed and/or simplified and therefore incomplete. The document may contain forward- looking statements with respect to the strategy, earnings and capital trends of KBC, involving numerous assumptions and uncertainties. The risk exists that these statements may not be fulfilled and that future developments differ materially. Moreover, KBC does not undertake any obligation to update this document in line with new developments. The document may also contain non-IFRS information. By reading this document, each person is deemed to represent that he/she possesses sufficient expertise to understand the risks involved. KBC Group and its subsidiaries cannot be held liable for any damage resulting from the use of the information. KBC Group – who’s who in the Executive Committee, situation at 01 May 2014 Johan Thijs Group Chief Executive Officer °1965 Belgian Master’s Degree in Science (Applied Mathematics) and Actuarial Sciences (KU Leuven) Joined KBC Group or its pre-merger entities in 1988 Career o 1988 Various actuary functions in life and non-life insurance, ABB Insurance o 1995 Head of non-life department, Limburg regional office, ABB Insurance o 1998 Provincial manager Limburg and Eastern Belgium, KBC Insurance o 2001 Senior General Manager non-life insurance, KBC Insurance o 2006 Member of the Management Committee -

H1 2020 Results

H1 2020 Results 31st July 2020 Agenda Topic Presenter Performance update Alison Rose Detailed H1 & Q2 results Katie Murray Investment case Alison Rose Performance update ALISON ROSE, Chief Executive Officer 3 H1 results highlights 1 H1 2020 highlights Operating profit Impairments CET1 ratio % £2.1 billion £2.9 billion 17.2% Operating Profit before impairment Impairment charges as at H1’20 CET1 Ratio up 60bps vs Q1’20 Operating loss before tax £0.8bn losses, up 3% on H1’19 driven by net impairments of +2.6bn £2.9bn (£0.8) billion 2.9 16.6% 17.2% Robust capital position with Operating Loss before tax, down 0.3 £2.5 billion vs H1’19 Q1’20 Q2’20 strong liquidity levels H1’19 H1’20 Attributable loss Other expenses2 Liquidity Coverage ratio % (£0.7) billion £3.3 billion 166% £2.0 billion attributable profit in H1’19 Operating expenses excluding Liquidity Coverage Ratio +14p.p. vs Operating lease depreciation down Q1’20 £41m vs H1’19 -1% 152% 166% 3.34 3.30 Q1’20 Q2’20 H1’19 H1’20 1. Excluding the £990m impact of the strategic disposal (Alawwal) in Q2’19 2. Operating expenses excluding operating lease depreciation 4 H1 results highlights We have a robust absolute and relative £2.9bn 17.2% capital position versus Impairment charge CET1 ratio UK listed banks – this Q2’20 Impairment charge of £2.1bn vs We have shaped a capital generative business is underpinned by a £0.8bn in Q1’20 that in the medium to long term will operate at a resilient, capital CET1 ratio of 13%-14% generative and well Robust capital levels: Our ECL provision has increased to ‒ 320-420 bps or c.£5.8-7.6bn headroom to diversified business £6.4bn target CET1 ratio ‒ 830 bps or £15bn headroom to MDA2 ‒ UK listed banks average MDA2 headroom of 365bps1 Majority of expected FY’20 impairment charge captured in H1’20 Clear intention to return to paying dividends as soon as possible, targeting a pay-out ratio of 40% over time. -

Nordea Group Annual Report 2018

Annual Report 2018 CEO Letter Casper von Koskull, President and Group CEO, and Torsten Hagen Jrgensen, Group COO and Deputy CEO. Page 4 4 Best and most accessible advisory, with an 21 easy daily banking experience, delivered at scale. Page 13 Wholesale Banking No.1 relationship Asset & Wealth bank in the Nordics Management with operational Personal Banking 13 excellence. Page 21 Commercial & Business Banking Our vision is to become the lead- ing Asset & Wealth Manager in the 25 Nordic market by 2020. Page 25 Best-in-class advisory and digital experience, 17 ef ciency and scale with future capabilities in a disruptive market. Page 17 Annual Report 2018 Contents 4 CEO letter 6 Leading platform 10 Nordea investment case – strategic priorities 12 Business Areas 35 Our people Board of Directors’ report 37 The Nordea share and ratings 40 Financial Review 2018 46 Business area results 49 Risk, liquidity and capital management 67 Corporate Governance Statement 2018 76 Non-Financial Statement 78 Conflict of interest policy 79 Remuneration 83 Proposed distribution of earnings Financial statements 84 Financial Statements, Nordea Group 96 Notes to Group fi nancial statements 184 Financial statements Parent company 193 Notes to Parent company fi nancial statements 255 Signing of the Annual Report 256 Auditor’s report Capital adequacy 262 Capital adequacy for the Nordea Group 274 Capital adequacy for the Nordea Parent company Organisation 286 Board of Directors 288 Group Executive Management 290 Main legal structure & Group organisation 292 Annual General Meeting & Financial calendar This Annual Report contains forward-looking statements macro economic development, (ii) change in the competitive that reflect management’s current views with respect to climate, (iii) change in the regulatory environment and other certain future events and potential fi nancial performance.