Heimdal Junction – the Past

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

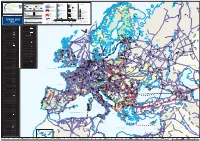

TYNDP 2017 FID Status (Final Investment Decision) White Sea PCI Status (Project of Common Interest) Submission

SHTOKMAN SNØHVIT Pechora Sea ASKELADD MELKØYA KEYS ALBATROSS Hammerfest Salekhard Cross-border points / intra-country or intra balancing zone points Transport by pipeline LNG Import Terminals Storage facilities Compressor stations Barents KILDIN N Acquifer Sea 1ACross-border interconnection point Cross-border interconnection point Pipeline diameters : LNG Terminals’ entry point within Europe within Europe Diameter < 600 mm intro transmission system Salt cavity - cavern or export point to non-EU country or export point to non-EU country Operational Under construction or Planned Diameter 600 - 900 mm Depleted (Gas) eld on shore / oshore MURMAN Diameter > 900mm Other type Unknown Cross-border interconnection point Cross-border third country (import) with third country (import) Under construction or Planned Pomorskiy Project categories : Project categories : Project categories : Project categories : Strait Intra-country or Murmansk Third country cross-border FID projects FID projects FID projects intra balancing zone points interconnection point FID projects Non-FID, advanced projects Non-FID, advanced projects Non-FID, advanced projects REYKJAVIK Non-FID, advanced projects Non-FID, non-advanced projects Non-FID, non-advanced projects Non-FID, non-advanced projects Gas Reserve areas Countries Non-FID, non-advanced projects ENTSOG Member Countries ICELAND Project is part of 2nd PCI list : Project is part of 2nd PCI list : Project is part of 2nd PCI list : Project is part of 2nd PCI list : Drilling platform ENTSOG Associated Partner P ENTSOG -

Processing Plant Like an Oasis, the Processing Plant Lights up the Coastal Landscape in Late Summer Evenings

FACTS Kollsnes Processing Plant Like an oasis, the processing plant lights up the coastal landscape in late summer evenings. The Kollsnes processing plant plays a key role in the transport of large quanti- ties of gas from fields in the Norwegian sector of the North Sea to customers in Europe. Gas from Kollsnes accounts for around 40 per cent of all Norwegian gas deliveries. The enormous quantities of gas in the Troll field started it all. Today, Kollsnes processing plant acts as goes further treatment and is fractioned Troll is the very corner- a centre for processing of gas from the into propane, butane and naphtha. stone of Norwegian Troll, Fram, Visund and Kvitebjørn fields. At Kollsnes, the gas is cleaned, dried and The processing plant itself consists gas production. When compressed before being transported as primarily of three dew point plants for dry gas through export pipes to Europe. treating gas, condensate and mono- the field was declared In addition, some gas is transported ethylene glycol (MEG) respectively. in separate pipes to Naturgassparken There is also a separate plant for the commercially viable in western Øygarden, where Gassnor production of Natural Gas Liquids in 1983, the question treats and distributes gas for domestic (NGL). In the plant, the wet gas (NGL) use. Condensate, or wet gas, which is is separated out first, and then the dry arose of what route made up of heavier components in the gas is pressurised using the six export gas, is transported via the Sture ter- compressors and sent into the transport the enormous quanti- minal through a pipeline to Mongstad system via the export pipelines Zeepipe ties of gas should take (Vestprosess). -

PIPELINES and LAND FACILITIES 145 Pipelines

Pipelines and 15 land facilities Pipelines Gassled . 146 Europipe I . 146 Europipe II . 146 Franpipe . 147 Norpipe Gas . 147 Oseberg Gas Transport (OGT) . 147 Statpipe . 147 Vesterled (formerly Frigg Transport) . 148 Zeepipe . 148 Åsgard Transport . 148 Draugen Gas Export . 149 Grane Gas Pipeline . 149 Grane Oil Pipeline . 150 Haltenpipe . 150 Heidrun Gas Export . 151 Kvitebjørn Oil Pipeline . 151 Norne Gas Transport System (NGTS) . 152 Norpipe Oil AS . 152 Oseberg Transport System (OTS) . 153 Sleipner East condensate . 154 Troll Oil Pipeline I . 154 Troll Oil Pipeline II . 155 Land facilities Bygnes traffic control centre . 156 Kollsnes gas treatment plant . 156 Kårstø gas treatment and condensate complex . 156 Kårstø metering and technology laboratory . 157 Mongstad crude oil terminal . 157 Sture terminal . 158 Tjeldbergodden industrial complex . 158 Vestprosess . 159 -12˚ -10˚ -8˚ -6˚ -4˚ -2˚ 0˚ 2˚ 4˚ 6˚ 8˚ Norne 66˚ Heidrun 62˚ Åsgard Kristin Draugen PIPE 15 FAROE TEN ISLANDS AL H 64˚ Tjeldbergodden 60˚ Trondheim ÅSGARD TRANSPORT Murchison Snorre Statfjord Visund SHETLAND Gullfaks Kvitebjørn Florø 62˚ Huldra Veslefrikk Tune Brage Troll Mongstad THE ORKNEYS Oseberg OTS Stura STA Kollsnes 58˚ Frigg TPIPE Frøy Heimdal Bergen NORWAY Grane ll B IPE ZEEPIPEEEP ll A 60˚ Brae Z Kårstø Sleipner St. Fergus STATPIPE Draupner S/E Stavanger Forties 56˚ Ula SWEDEN Gyda 58˚ Ekofisk Valhall Hod NORPIPE EUROPIPE EUROPIPE 54˚ Teesside DENMARK ll NORPIP l 56˚ E GREAT 52˚ Bacton BRITAIN ZEEPIPE l CON FRANPIPE Emden INTER- 54˚ NECTOR THE GERMANY NETHERLANDS Zeebrugge 50˚ Dunkerque Existing pipeline 52˚ BELGIUM Projected pipeline Existing oil/condensate pipeline FRANCE Projected oil/condensate pipeline 0˚ 2˚ 4˚ 6˚ 8˚ 10˚ 12˚ The map shows existing and planned pipelines in the North and Norwegian Seas. -

Facts 2002 the Norwegian Petroleum Sector

DISCLAIMER Portions of this document may be illegible in electronic image products. Images are produced from the best available original document. Facts 2002 The Norwegian petroleum sector Ministry of Petroleum and Energy Visiting address: Einar Gerhardsens plass 1 Postal address: P 0 Box 8148 Dep, N-0033 Oslo Tel c47 22 24 90 90 Fax +47 22 24 95 65 http://www.mpe.dep.no (English) http://www.oed.dep.no (Norwegian) E-mail: [email protected] Editor: Tore Fugelsnes, MPE English rditur: Rolf E Gooderhani Edition completed: March 2002 Iayout/design: Marketing Serviccs AS Illustration: Inger Farvik Photos: Q Terjc S Knudsen, Norsk Hydro ASA, 0 Oy-vind Hagm, Statoil ASA, field photos from operators’ archives. Paper: Cover: Munken Lynx 240 g. inside pages: Uni Matt 115 g. Printer: BK Vestfold Grafiskr Circulation: 14 000 Norwegian/Y 000 English ISSN-1502.5446 Foreword Even after 30 years of petroleum production from terms of both maturity and challenges between its the Norwegian continental shelf (NCS), we estimate various areas. A broad spread of companies will help that only about 24 per cent of these resources have to meet the rnnltiplicity of challenges facing 11s. been produced. Remaining recoverable resources Wiile the oil majors are relatively well represented are put at 10.6 hn scm of oil equiv;rlent, and could today, small and mediurn-sized players have a provide the basis for another 50 years of oil produc- weaker involvement. The prequalification system tion and a century of gas output. The petroleum is a new and important measure, which will make sector will thereby remain a major source of value it easier for new players to become established on creation for the Norwegian community. -

O I^ the Norwegian Petroleum Sector

O i^ H- -^ 3L o co '• ' • :.* The Norwegian Petroleum Sector ETDE-NO-20086204 32/ 32 PLEASE BE AWARE THAT ALL OF THE MISSING PAGES IN THIS DOCUMENT WERE ORIGINALLY BLANK DISCLAIMER Portions of this document may be illegible in electronic image products. Images are produced from the best available original document. Facts 2000 The Norwegian petroleum sector Ministry of Petroleum and Energy Visiting address: Einar Gerhardsen plass 1 Postal address: P O Box 8148 Dep, N-0033 Oslo Tel +47 22 24 90 90 Fax +47 22 24 95 65 http://www.oed.dep.no E-mail: [email protected] Telex: 21486 oedep n Editor: Odd Reistad Solheim, MPE English editor: Rolf E Gooderham Edition completed: March 2000 Layout/design: Fasett AS, www.fasett.no Photos: ©Leif Berge and ©0yvind Hagen.Statoil. Field photos from operators' archives. Paper: 240 g Munken Lynx/115 g Galeri Art Silk Printer: Gunnarshaug Circulation: 15 000 Norwegian/10 000 English ISSN-1501-6412 Foreword The past year was challenging for the petroleum Norwegian crude oil production averaged 2.9 industry. Oil prices at the beginning of 1999 were million barrels per day in 1999.This output will about a third of the level they reached at the end. peak in the near future, and then begin to decline. We can also expect to see big oil price fluctuations But the Norwegian continental shelf nevertheless in future. Out of consideration for a stable develop- represents a substantial resource base. That applies ment of the oil market, the Norwegian economy to fields in operation, under evaluation and yet and the administration of the country's petroleum to be discovered. -

Review of Natural Gas Pipeline Activity in Selected Regions of the World

Review of Natural Gas Pipeline Activity in Selected Regions of the World Prepared for the INOAA Foundation, Inc. by: Gaffney, CUne &: Associates Inc. 16775 Addison Road, Suite 400 DaUas,Tezas 75248 F-9704 Copyright © 1997 by the INGAA Foundation, Inc. _________________________ Gaffney, Cline & Associates TABLE OF CONTENTS Page No. EXECUTIVE SUMMARY .......•...................................... 1 INTRODUCTION .................................................... 3 DISCUSSION .•..........•..........................•.............. 4 1. EUROPE .•....•......•..........................•...•....... 4 2. FORMER SOVIET UNION ........................••......•...... 34 3. SOUTH AMERICA .•........•..........•..•.....••......•....• 50 4. ASIA PACIFIC ......••.••.....•......•......••........•...... 64 4.1 Pacific Rim (Including Australia) ...•...•.•...•...•........•.•. 65 4.2 Far East (Including China) .•.•..•.••••.•.....•••..•..•..•••• 80 4.3 Indian Subcontinent •....•...••..•.•.......••••••••••..••. 87 5. MIDDLE EAST AND AFRICA ........•...•.....•..•••..•...•...•.. 91 5.1 Middle East ....•.•...••••..•.•....••.•••..••.•.•....... 91 5.2 Africa ...•........•••......•.' •....•.....••............ 98 FIGURES 1 • Europe - Selected Gas Pipelines 2. Turkey and Adjacent Countries - Selected New Gas Pipelines 3. Former Soviet Union (FSU) - Selected New Gas Pipelines 4. South America - Selected New Pipelines 5. Trinidad - Atlantic LNG and Gas Supply Pipeline 6. Australia - Selected New Gas Pipelines 7. Indonesia - Main Gas Areas 8. West Indonesia - Selected -

Offshore Transportation of Norwegian Gas to Europe

OFFSHORE TRANSPORTATION OF NORWEGIAN GAS TO EUROPE The case of The Barents Sea Gas Infrastructure Doctor of Business Administration HENLEY BUSINESS SCHOOL Michael Ingenbleek January 2018 Declaration I confirm that this is my own work and the use of all material from other sources has been properly and fully acknowledged. Michael Ingenbleek. I At the basis of the monopoly of the Standard Oil Company in the production and distribution of petroleum products rests the pipe line. The possession of these pipelines enables the Standard to absolutely control the price which its competitor in each given locality shall pay. (ICC, 1907 cited in Boyce, 2014 pp.5) II Introduction This study is concerned with Norway’s role in supplying gas to Europe through offshore pipelines. One reason for choosing this topic is the difference in available research between the number one supplier of gas to Europe, Russia, and the number two, Norway, where there is much less published research. This study aims to bridge the gap by considering, for the Norwegian gas Sector, issues of gas supply, a competitive gas market, a sustainable effective, efficient offshore infrastructure and access for all where and when it is required. It further explores whether the regulation of the Norwegian Gas Sector, through national regulations, the Gas Target Model and three EU gas directives is meeting its goals or actually hinders development. Another reason to choose this subject is the low volume of investments in the Norwegian gas offshore infrastructure, which consequently will lead to reduced volumes of supply. In relation to the abovementioned, the third reason is to investigate whether current and anticipated prices justify further investment in Norwegian natural resources and offshore infrastructure. -

17 PIPELINES and LAND FACILITIES 149 126-193 Kap

126-193 Kap. 15-18 eng orig 20.04.01 13:03 Side 148 Pipelines and land 17 facilities Pipelines Norpipe • Frigg Transport/Vesterled • Frostpipe Sleipner East condensate • Statpipe • Zeepipe Europipe I • Troll Oil Pipeline I • Troll Oil Pipeline II Oseberg Transport System (OTS) • Oseberg Gas Transport (OGT) Haltenpipe • Franpipe • Europipe II • Åsgard Transport Norne Gas Export • Heidrun Gas Export • Draugen Gas Export Grane Oil Pipeline • Grane Gas Pipeline Land facilities Kårstø gas treatment and condensate complex Kårstø metering and technology laboratory Bygnes traffic control centre • Kollsnes gas treatment plant Tjeldbergodden industrial complex • Sture terminal • Vestprosess Mongstad crude oil terminal 126-193 Kap. 15-18 eng orig 20.04.01 13:03 Side 149 Norne Heidrun Åsgard HALTENPIPE Draugen Njord TRANSPORT Faroe Islands SGARD Å TTrondheimrondheim Tjeldbergodden Statfjord 17 Murchison Snorre Kvitebjørn Shetland Gullfaks Veslefrikk FlorFlorø Huldra Brage Troll Tune Mongstad Oseberg OTS Orkneys STATPIPE Sture Kollsnes Frigg Frøy BergenBergen Heimdal Norway II A Grane II B Kårstø ZEEPIPE Brae E St Fergus ZEEPIPE IP Sleipner STATP STAVANGERSTAVANGER Draupner S/E Forties Ula Cod Sweden Gyda Ekofisk Tommeliten G Valhall Hod PIPE NOR Teesside EUROP EUROPIPE I Denmark IP E II Great Britain NORPIPE ANPIPE ZEEPIPE I FR Bacton Emden INTER- CONNECTOR Germany The Netherlands Existing gas pipeline Projected gas pipeline Zeebrugge Dunkerque Oil/condensate pipeline Projected oil/condensate France Belgium pipeline Figure 17.1 shows existing and planned pipelines in the North and Norwegian Seas.This chapter provides a more detailed description of pipelines on the Norwegian continental shelf.The transport capacities given are based on standard assumptions about pressure ratios, energy content of the gas, buyer options for varying daily deliveries, maintenance periods and operational flexibility. -

Challenges in the Flow Measurement Engineering Study Phases

Challenges in the Flow Measurement Engineering Study Phases By Liv Marit Henne and Jean Monnet, Aker Kværner Stavanger Summary: Offshore development of marginal Oil and Gas fields can often be economically profitable if they can be tied in to existing platforms. This usually requires execution of comprehensive feasibility studies, which can often be a long and costly process. Close cooperation in a multi- discipline engineering team is necessary to assure that all possibilities and aspects of the design task have been evaluated. Integration of a new flow measurement module on an existing installation is often the simplest solution, yielding low total cost as the module can be assembled and fully tested on shore. However on many installations one is required to integrate the new equipment in existing modules. Flow measurement is a crucial element in the development of marginal fields which has to be evaluated, taking into consideration all critical aspects such as: available space, weight, location accessibility, maintenance and integration to existing metering systems. In particular, special attention should be given to the possible use of new flow measurement technologies and principles. 1. INTRODUCTION For the past 35 years the North Sea has been populated by a number of types of platforms and rigs, essential for the development of offshore oil and gas fields. This rough environment has largely contributed to technology process developments including fiscal and flow measurement. 1 During this period Aker Kværner has been at the front End in MMO (Maintenance Modification Offshore) and has acted as an Engineering Contractor involved in most Norwegian fields development. -

Pipelines and Land Facilities

Facts 2002 kap 15-18.qxd 4/10/2002 10:39 AM Side 152 17 Pipelines and land facilities Pipelines Draugen Gas Export ......................................................................................... 154 Europipe I ........................................................................................................... 154 Europipe II .......................................................................................................... 155 Franpipe .............................................................................................................. 155 Frostpipe .............................................................................................................. 156 Grane Gas Pipeline ........................................................................................... 156 Grane Oil Pipeline ............................................................................................ 157 Haltenpipe ......................................................................................................... 157 Heidrun Gas Export .......................................................................................... 158 Kvitebjørn Oil Pipeline ..................................................................................... 158 Norne Gas Transport System (NGTS) ................................................................. 159 Norpipe Oil AS ....................................................................................................... 159 Norpipe, Norsea Gas A/S ..................................................................................... -

The European Natural Gas Network

SHTOKMAN SNØHVIT Pechora Sea ASKELADD TRADING POINTS / MARKET AREAS KEYS MELKØYA ALBATROSS Hammerfest (DK) (IE) Nr Location System Operators : logos 400 NPTF Salekhard 407 IBP 01 Trading Points / Market Areas Barents (CZ-DE) KILDIN N (DK) (FR-N) 043 Waidhaus Sea 401 GTF (Bilateral Trading Point) 408 PEG NORD Cross-border interconnection point Cross-border Europe 001 1A 1A within Europe Under construction or Planned (NL) (FR-S) NET4GAS GRTgaz Deutschland B Y 11,20 11,20 402 TTF 409 PEG SUD 903,7 MURMAN Cross-border interconnection point Cross-border third country import/export Open Grid Europe 001 NET4GAS B Y 11,20 11,20 (FR-S) with third country (import/export) Under construction or Planned (DE) 410 PEG TIGF Pomorskiy 403 VHP GASPOOL LNG Terminals’ entry point LNG Import Terminal System Operators Capacity Flow GCV 0011C (IT) intro transmission system Under construction or Planned Strait 411 PSV Murmansk LNG Export Terminal LNG Export Terminal Capacity 1010,4 Max. technical physical capacity in GWh/d (ES) 1C Under construction or Planned 412 MS-ATR Where different Maximum Technical Capacities areREYKJAVIK defined by the neighbouring (HU) Small scale LNG liquefaction plant Small scale LNG liquefaction plant TSOs for the same Interconnection Point, the lesser rule is applied. 413 MGP Under construction or Planned If capacity information is available only on one side of the border ICELAND due to confidentiality reasons, the available figure is selected for publication. (AT ) 001 Intra-country or intra balancing zone points 404 VHP NetConnect -

THE NORWEGIAN PETROLEUM SECTOR Cover: the First Oil Field in the North Sea, the Ekofisk Field, Started Production in 1971

2014 2014 THE NORWEGIAN PETROLEUM SECTOR Cover: The first oil field in the North Sea, the Ekofisk field, started production in 1971. The field has been developed and expanded through- out the years. Old facilities have been removed and new ones installed in order to enable production for another 30–40 years. This picture shows the field as it emerges today, after three new facilities were installed in the summer of 2013 (Photo: Kjetil Alsvik/ConocoPhillips) New native apps for Android and Windows Phone are now available • All the fields • All the wells • All the production • All the operators • All the licenses • News, maps and more www.oilfacts.no 2014 THE NORWEGIAN PETROLEUM SECTOR What do you think about Facts 2014? Please send your comments to [email protected]. PB • FACTS 2014 Editor: Yngvild Tormodsgard, Ministry of Petroleum and Energy Design: Artdirector/Klas Jønsson Paper: Cover: Galerie art silk 250 g, Inside pages: Arctic silk 115 g Graphic production: 07 MEDIA Printing: 07 MEDIA Circulation: 13 500 New Norwegian / 12 000 English Publication number: Y-0103/15 E Cover: The Ekofisk Field in the North Sea (Photo : Kjetil Alsvik/ConocoPhillips) ISSN 1504-3398 4 • FACTS 2014 Tord Lien Minister of Petroleum and Energy Minister of Petroleum and Energy 2013 was yet another good year in the Norwegian petroleum sector. profitability of both projects and companies. The industry must take The activity level is high; the shelf is explored, resources discovered, action to control these costs. Succeeding with this will be crucial in fields developed and hydrocarbons produced and sold.