2018 Annual Report Bank of Kunlun Corporation Limited Key Performance Indicators

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Joint Civil Society Report Submitted to the Committee on the Elimination of Racial Discrimination

Joint Civil Society Report Submitted to The Committee on the Elimination of Racial Discrimination for its Review at the 96th Session of the combined fourteenth to seventeenth periodic report of the People’s Republic of China (CERD/C/CHN/14-17) on its Implementation of the Convention on the Elimination of All Forms of Racial Discrimination Submitters: Network of Chinese Human Rights Defenders (CHRD) is a coalition of Chinese and international human rights non-governmental organizations. The network is dedicated to the promotion of human rights through peaceful efforts to push for democratic and rule of law reforms and to strengthen grassroots activism in China. [email protected] https://www.nchrd.org/ Equal Rights Initiative is a China-based NGO monitoring rights development in Western China. For the protection and security of its staff, specific identification information has been withheld. Date of Submission: July 16, 2018 Table of Contents I. Executive Summary Paras. 1-2 II. Recommendations Para. 3 III. Thematic Issues & Findings A. Legislation underpinning discriminatory counter-terrorism policies Paras. 4-7 [Articles 2 (c) and 4; List of Themes para. 8] B. Militarized policing, invasive surveillance, and constant monitoring Paras. 8-21 [Articles 3, 4, and 5 (a-b); LOT para. 22] C. Extrajudicial detention, forced disappearances, torture, and other abuses Paras. 22-28 in “Re-education” camps [Article 5 (a)(b)(d); LOT para. 21] D. Counter-terrorism used to justify arbitrary detention and discriminatory Paras. 29-34 punishment of ethnic minorities [Articles 4 and 5 (a)(b)(d); LOT paras. 6 and 21] E. Discrimination and restrictions on religious freedom Paras. -

Download Article

Advances in Economics, Business and Management Research, volume 165 Proceedings of the 6th International Conference on Economics, Management, Law and Education (EMLE 2020) Research on the Influences of Tourism on the Process of Local Urbanization in Western Regions Taking Heavenly Pond in Tianshan Scenic Spot of Xinjiang Province as an Example Min Liao1,* Tao Zhang1 1City University of Macau, Macau, China *Corresponding author. Email:[email protected] ABSTRACT In recent years, urbanization research has gradually become a research hotspot in academia, but there are few literatures on the influences of tourism development on urbanization in the western region. By consulting the relevant literature and materials of Heavenly Pond in Tianshan Scenic Spot in Xinjiang and Fukang City, this paper studies the regional and industrial reallocation of resources in Fukang City due to tourism development, the transfer of surplus rural labor force to urban employment, and the changes in space, economy and society based on the current situation of the research area by interview method. The research results show that tourism has a significant impact on population urbanization, economic urbanization, social and cultural urbanization and environmental development in Fukang City. Keywords: tourism, western region, urbanization process, Heavenly Pond in Tianshan Scenic Spot Spot on the urbanization process of Fukang City based I. INTRODUCTION on urbanization theory and stakeholder theory. In the academic circles, there is a general consensus that the development of tourism has a significant role in II. LITERATURE REVIEW promoting the process of local urbanization, which is based on the national level. However, China has a vast A. Research status in foreign countries territory, the economic development of each region is In the early 1970s, the level of urbanization in significantly different, and the development stage of developed countries in Europe and the United States urbanization process is also different. -

Major Controls on Streamflow of the Glacierized Urumqi River Basin in the Arid Region of Northwest China

water Article Major Controls on Streamflow of the Glacierized Urumqi River Basin in the Arid Region of Northwest China Muattar Saydi, Guoping Tang and Hong Fang * School of Geography and Planning, Sun Yat-Sen University, Guangzhou 510275, China; [email protected] (M.S.); [email protected] (G.T.) * Correspondence: [email protected] Received: 10 October 2020; Accepted: 27 October 2020; Published: 1 November 2020 Abstract: Understanding the main drivers of runoff availability has important implications for water-limited inland basins, where snow and ice melt provide essential input to the surface runoff. This paper presents an analysis on the runoff response to changes in climatic and other controls of water-energy balance in an inland glacierized basin, the Urumqi River basin, located in the arid region of northwest China, and identifies the major control to which runoff is sensitive across the basin’s heterogeneous subzones. The results indicate that the runoff is more sensitive to change in precipitation in the mountainous headwaters zone of the upper reach, and followed by the impact of basin characteristics. In contrast, the runoff is more sensitive to changes in the basin characteristics in the semiarid and arid zones of the mid and lower reaches. In addition, the change in basin characteristics might be represented by the distinct glacier recession in the mountainous upper reach zone and the increasing human interferences, i.e., changes in land surface condition and population growth, across the mid and lower reach zones. The glacier wasting contributed around 7% on average to the annual runoff between 1960 and 2012, with an augmentation beginning in the mid-1990s. -

46063-002: Xinjiang Tacheng Border Cities and Counties Development Project

Social Monitoring Report Project Number: 46063-002 December 2019 PRC: Xinjiang Tacheng Border Cities and Counties Development Project (EMDP Monitoring Report-ENG) Prepared by: Xinjiang Agricultural University This social monitoring report is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management or staff, and may be preliminary in nature. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. ADB-financed Project of Xinjiang Tacheng Border Cities and Counties Development Xinjiang Tacheng Border Cities and Counties Development Project External Monitoring & Evaluation Report on Ethnic Minority Development Plan (Year of 2019) Xinjiang Agricultural University December 2019 Xinjiang Tacheng Border Cities and Counties Development Project External Monitoring & Evaluation Report on Ethnic Minority Development Plan (Year of 2019) Project Leader: ZHU Meiling Component leader: Wang Jiao Compiled by: WANG Jiao Data collected & analyzed by: ZHU Meiling, Wang Jiao, MA Yongren, Liu Jiaxin, Zeng Ge Translated by: CHENG Luming Reviewed by: ZHU Meiling Table of Contents CHAPTER I PROJECT OVERVIEW ............................... 1 SECTION 1 IMPLEMENTATION OF PROJECT WORKS .................................................................. 1 -

Frontier Politics and Sino-Soviet Relations: a Study of Northwestern Xinjiang, 1949-1963

University of Pennsylvania ScholarlyCommons Publicly Accessible Penn Dissertations 2017 Frontier Politics And Sino-Soviet Relations: A Study Of Northwestern Xinjiang, 1949-1963 Sheng Mao University of Pennsylvania, [email protected] Follow this and additional works at: https://repository.upenn.edu/edissertations Part of the History Commons Recommended Citation Mao, Sheng, "Frontier Politics And Sino-Soviet Relations: A Study Of Northwestern Xinjiang, 1949-1963" (2017). Publicly Accessible Penn Dissertations. 2459. https://repository.upenn.edu/edissertations/2459 This paper is posted at ScholarlyCommons. https://repository.upenn.edu/edissertations/2459 For more information, please contact [email protected]. Frontier Politics And Sino-Soviet Relations: A Study Of Northwestern Xinjiang, 1949-1963 Abstract This is an ethnopolitical and diplomatic study of the Three Districts, or the former East Turkestan Republic, in China’s northwest frontier in the 1950s and 1960s. It describes how this Muslim borderland between Central Asia and China became today’s Yili Kazakh Autonomous Prefecture under the Xinjiang Uyghur Autonomous Region. The Three Districts had been in the Soviet sphere of influence since the 1930s and remained so even after the Chinese Communist takeover in October 1949. After the Sino- Soviet split in the late 1950s, Beijing transformed a fragile suzerainty into full sovereignty over this region: the transitional population in Xinjiang was demarcated, border defenses were established, and Soviet consulates were forced to withdraw. As a result, the Three Districts changed from a Soviet frontier to a Chinese one, and Xinjiang’s outward focus moved from Soviet Central Asia to China proper. The largely peaceful integration of Xinjiang into PRC China stands in stark contrast to what occurred in Outer Mongolia and Tibet. -

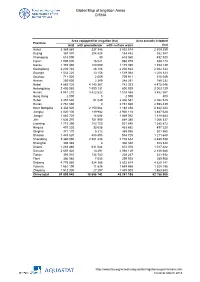

Global Map of Irrigation Areas CHINA

Global Map of Irrigation Areas CHINA Area equipped for irrigation (ha) Area actually irrigated Province total with groundwater with surface water (ha) Anhui 3 369 860 337 346 3 032 514 2 309 259 Beijing 367 870 204 428 163 442 352 387 Chongqing 618 090 30 618 060 432 520 Fujian 1 005 000 16 021 988 979 938 174 Gansu 1 355 480 180 090 1 175 390 1 153 139 Guangdong 2 230 740 28 106 2 202 634 2 042 344 Guangxi 1 532 220 13 156 1 519 064 1 208 323 Guizhou 711 920 2 009 709 911 515 049 Hainan 250 600 2 349 248 251 189 232 Hebei 4 885 720 4 143 367 742 353 4 475 046 Heilongjiang 2 400 060 1 599 131 800 929 2 003 129 Henan 4 941 210 3 422 622 1 518 588 3 862 567 Hong Kong 2 000 0 2 000 800 Hubei 2 457 630 51 049 2 406 581 2 082 525 Hunan 2 761 660 0 2 761 660 2 598 439 Inner Mongolia 3 332 520 2 150 064 1 182 456 2 842 223 Jiangsu 4 020 100 119 982 3 900 118 3 487 628 Jiangxi 1 883 720 14 688 1 869 032 1 818 684 Jilin 1 636 370 751 990 884 380 1 066 337 Liaoning 1 715 390 783 750 931 640 1 385 872 Ningxia 497 220 33 538 463 682 497 220 Qinghai 371 170 5 212 365 958 301 560 Shaanxi 1 443 620 488 895 954 725 1 211 648 Shandong 5 360 090 2 581 448 2 778 642 4 485 538 Shanghai 308 340 0 308 340 308 340 Shanxi 1 283 460 611 084 672 376 1 017 422 Sichuan 2 607 420 13 291 2 594 129 2 140 680 Tianjin 393 010 134 743 258 267 321 932 Tibet 306 980 7 055 299 925 289 908 Xinjiang 4 776 980 924 366 3 852 614 4 629 141 Yunnan 1 561 190 11 635 1 549 555 1 328 186 Zhejiang 1 512 300 27 297 1 485 003 1 463 653 China total 61 899 940 18 658 742 43 241 198 52 -

The Muslim Emperor of China: Everyday Politics in Colonial Xinjiang, 1877-1933

The Muslim Emperor of China: Everyday Politics in Colonial Xinjiang, 1877-1933 The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation Schluessel, Eric T. 2016. The Muslim Emperor of China: Everyday Politics in Colonial Xinjiang, 1877-1933. Doctoral dissertation, Harvard University, Graduate School of Arts & Sciences. Citable link http://nrs.harvard.edu/urn-3:HUL.InstRepos:33493602 Terms of Use This article was downloaded from Harvard University’s DASH repository, and is made available under the terms and conditions applicable to Other Posted Material, as set forth at http:// nrs.harvard.edu/urn-3:HUL.InstRepos:dash.current.terms-of- use#LAA The Muslim Emperor of China: Everyday Politics in Colonial Xinjiang, 1877-1933 A dissertation presented by Eric Tanner Schluessel to The Committee on History and East Asian Languages in partial fulfillment of the requirements for the degree of Doctor of Philosophy in the subject of History and East Asian Languages Harvard University Cambridge, Massachusetts April, 2016 © 2016 – Eric Schluessel All rights reserved. Dissertation Advisor: Mark C. Elliott Eric Tanner Schluessel The Muslim Emperor of China: Everyday Politics in Colonial Xinjiang, 1877-1933 Abstract This dissertation concerns the ways in which a Chinese civilizing project intervened powerfully in cultural and social change in the Muslim-majority region of Xinjiang from the 1870s through the 1930s. I demonstrate that the efforts of officials following an ideology of domination and transformation rooted in the Chinese Classics changed the ways that people associated with each other and defined themselves and how Muslims understood their place in history and in global space. -

Oirat Tobi Intonational Structure of the Oirat Language a Dissertation Submitted to the Graduate Division of the University of H

OIRAT TOBI INTONATIONAL STRUCTURE OF THE OIRAT LANGUAGE A DISSERTATION SUBMITTED TO THE GRADUATE DIVISION OF THE UNIVERSITY OF HAWAI‘I IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY IN LINGUISTICS FEBRUARY 2009 By Elena Indjieva Dissertation Committee: Kenneth Rehg (UH, Linguistics Department), Co-chairperson Victoria Andersen (UH, Linguistics Department), Co-chairperson Stefan Georg (Bonn University, Germany) William O’Grady (UH, Linguistics Department) Robert Gibson (UH, Department of Second Language Studies) SIGATURE PAGE ii DEDICATIO I humbly dedicate this work to one of the kindest person I ever knew, my mother, who passed away when I was in China collecting data for this dissertation. iii ACKOWLEDGEMET Over several years of my graduate studies at the Linguistics Department of the University of Hawai’i at Manoa my knowledge in various field of linguistics has been enhanced immensely. It has been a great pleasure to interact with my fellow students and professors at this department who have provided me with useful ideas, inspiration, and comments on particular issues and sections of this dissertation. These include Victoria Anderson, Maria Faehndrich, Valerie Guerin, James Crippen, William O’Grady, Kenneth Rehg, and Alexander Vovin. Many thanks to them all, and deepest apologies to anyone whom I may have forgotten to mention. Special thanks to Maria Faehndrich for taking her time to help me with styles and formatting of the text. I also would like to express my special thanks to Laurie Durant for proofreading my dissertation. My sincere gratitude goes to Victoria Anderson, my main supervisor, who always had time to listen to me and comment on almost every chapter of this work. -

Geology of the Petroleum and Coal Deposits in the Junggar (Zhungaer) Basin, Xinjiang Uygur Zizhiqu, Northwest China by K. Y

UNITED STATES DEPARTMENT OF THE INTERIOR GEOLOGICAL SURVEY Geology of the petroleum and coal deposits in the Junggar (Zhungaer) basin, Xinjiang Uygur Zizhiqu, northwest China By K. Y. Lee Open-File Report 85-230 This report is preliminary and has not been reviewed for conformity with U.S. Geological Survey editorial standards and stratigraphic nomenclature, 1985 CONTENTS Page ADS tract ~~ ~~ 1 T.__introduction 4_ ~» ~^ J _ _ -^ 4_ ^ *-* * _ ~~ _ _ __ jO General statement ~ 3 Regional setting ~~ 3 Purpose, scope, and method of the report 6 ot ra t ig rapriy Pre-Carboniferous 6 Lower Paleozoic _______ ^ Devonian o Upper Paleozoic Carboniferous and Permian 8 Carboniferous 8 c"D cA Ly» II1J--y. 3 allf~ _. ~~ "~ "~ ______ ____ ^1 ^1 Me so zoic ~~ 1 j T*^»iLiaysxc -I f* ft ft £ -» ^__ ____ _._ _ __ _ __ _ ^ _^ _ _ _ _ ^1 -jC JurassicT_.___J_ ±o1Q f"tjic1 'r»x.k denozoi c n^A w» ±cJ. Quaternary 2.1 Geotectonics and evolution of the basin 27 .tectonics and sedimentation 2.1 OQ "I"L. **iiI. Ut- r* -f"uUUJL v»£k C _ __ _ "~ "~ JO ^O iNOLLncrnVT -» ~» ^- l_ --. ^» _ iriaLrorm"O 1 « *- f y-k «*rn ~ oz*5 O Northern Tian Shan Foredeep 33 Jretroieum and coal deposits IT~D C£^ -I"L *V*JL (JXcULllf\ 1 A11TYI __ ~~ _________________________________________ j^O /l Source rocks 35 Reservoir rocks ~ 37 LT3f\t- \J LCllLlet Qi->4- -i n -L1 ~~ ~~ ~~ . i+/ i.1 ____________________ _ ______________________________________ /, Q uccurrence ^ ^ ^y T?jxci rt -p Crt T»^Y>JL C11L.CO /^ £1 O t-J./ » "1 t"^k^1Led K>^«*«.^«.^«. -

A Dynamic Analysis of Green Productivity Growth for Cities in Xinjiang

sustainability Article A Dynamic Analysis of Green Productivity Growth for Cities in Xinjiang Deshan Li 1,* and Rongwei Wu 2 1 College of Environmental Economics, Shanxi University of Finance and Economics, Taiyuan 030006, China 2 Xinjiang Institute of Ecology and Geography, Chinese Academy of Sciences, Urumqi 830011, China; [email protected] * Correspondence: [email protected]; Tel.: +86-351-766-6149 Received: 17 December 2017; Accepted: 8 February 2018; Published: 14 February 2018 Abstract: Improving green productivity is an important way to achieve sustainable development. In this paper, we use the Global Malmquist-Luenberger (GML) index to measure and decompose the green productivity growth of 18 cities in Xinjiang over 2000–2015. Furthermore, this study also explores factors influencing urban green productivity growth. Our results reveal that the urban green productivity in Xinjiang has slowly declined during the sample period. Technological progress is the main factor contributing to green productivity growth, while improvements in efficiency lag behind. Implementing stricter environmental regulation, improving infrastructure, and appropriately enhancing the spatial agglomeration of economic activities may improve green productivity, while the increase in the size of the industrial base in the near future will likely hinder green productivity growth. Based on these results, this paper puts forward corresponding policy suggestions for the sustainable development of the urban economy in Xinjiang. Keywords: Xinjiang; green productivity; GML index 1. Introduction Since the economic and political reforms of 1978, when China began to open up to the outside world, China’s economy has made remarkable achievements and has become the second largest economy in the world. -

Minimum Wage Standards in China August 11, 2020

Minimum Wage Standards in China August 11, 2020 Contents Heilongjiang ................................................................................................................................................. 3 Jilin ............................................................................................................................................................... 3 Liaoning ........................................................................................................................................................ 4 Inner Mongolia Autonomous Region ........................................................................................................... 7 Beijing......................................................................................................................................................... 10 Hebei ........................................................................................................................................................... 11 Henan .......................................................................................................................................................... 13 Shandong .................................................................................................................................................... 14 Shanxi ......................................................................................................................................................... 16 Shaanxi ...................................................................................................................................................... -

A Broad-Range Survey of Ticks from Livestock in Northern Xinjiang

Wang et al. Parasites & Vectors (2015) 8:449 DOI 10.1186/s13071-015-1021-0 RESEARCH Open Access A broad-range survey of ticks from livestock in Northern Xinjiang: changes in tick distribution and the isolation of Borrelia burgdorferi sensu stricto Yuan-Zhi Wang1†, Lu-Meng Mu1†, Ke Zhang2†, Mei-Hua Yang3†, Lin Zhang4†, Jing-Yun Du1†, Zhi-Qiang Liu5,6†, Yong-Xiang Li1†, Wei-Hua Lu5, Chuang-Fu Chen1,2*, Yan Wang1, Rong-Gui Chen7, Jun Xu8, Li Yuan1, Wan-Jiang Zhang1, Wei-Ze Zuo9 and Ren-Fu Shao10 Abstract Background: Borreliosis is highly prevalent in Xinjiang Uygur Autonomous Region, China. However, little is known about the presence of Borrelia pathogens in tick species in this region, in addition Borrelia pathogens have not been isolated from domestic animals. Methods: We collected adult ticks from domestic animals at 19 sampling sites in 14 counties in northern Xinjiang from 2012 to 2014. Ticks were identified to species by morphology and were molecularly analysed by sequences of mitochondrial 16S rDNA gene; 4–8 ticks of each species at every sampling site were sequenced. 112 live adult ticks were selected for each species in every county, and were used to culture Borrelia pathogens; the genotypes were then determined by sequences of the 5S-23S rRNA intergenic spacer and the outer surface protein A (ospA) gene. Results: A total of 5257 adult ticks, belonging to four genera and seven species, were collected. Compared with three decades ago, the abundance of the five common tick species during the peak ixodid tick season has changed. Certain tick species, such as Rhipicephalus turanicus (Rh.