Richmond Resilient Economy Strategy Technical Report #1 Richmond's

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

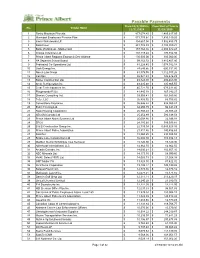

06-Payables Payments Report June-2021.Xlsx

Payables Payments From 6/1/2021 to From Start of Year to No. Vendor Name 6/30/2021 6/30/2021 1 PCL Construction Management Inc. $1,432,098.00 $4,202,885.16 2 Municipal Employees Pension Plan $865,122.32 $3,933,810.39 3 B & B Construction Group Inc. $413,794.41 $794,413.84 4 McDougall Gauley LLP $380,625.00 $380,625.00 5 JM Cuelenaere Library $355,457.00 $1,236,287.50 6 Raymax Equipment Sales Ltd. $294,232.28 $300,742.28 7 Saskatchewan Public Safety Agency $257,934.39 $812,357.75 8 Bank of Montreal - Mastercard $235,761.82 $1,144,650.98 9 SaskPower $191,693.85 $1,372,551.60 10 PA Separate School Board $137,484.12 $1,042,959.53 11 Emco Corporation $130,617.21 $279,969.15 12 AECOM Canada Ltd. $105,243.91 $433,914.10 13 Federated Co-Operatives Ltd. $102,688.03 $523,979.85 14 Community Service Centre $101,201.68 $354,205.88 15 Flocor $99,679.69 $161,309.91 16 Associated Fire Safety Group $86,413.50 $86,413.50 17 Novus Law Group $84,897.69 $282,297.38 18 Klearwater Equip & Technologies $79,336.00 $194,037.80 19 SPCA $75,660.01 $238,437.35 20 Iconix Waterworks LP $73,376.22 $151,087.79 21 Wheatland Builders & Concrete Ltd. $64,728.30 $221,492.63 22 Prince Albert Regional Economic Dev Alliance $61,250.00 $183,750.00 23 Group2 Architechture Engineering Inc $50,902.85 $397,732.08 24 Line West Ltd. -

Payable Payment Report December 2019.Xlsx

Payable Payments From 12/1/2019 to From Start of Year to No. Vendor Name 12/31/2019 12/31/2019 1 Rocky Mountain Phoenix $ 877,674.45 $ 1,485,617.03 2 Municipal Employees Pension Plan $ 573,779.64 $ 7,836,149.25 3 Iconix Waterworks LP $ 334,667.04 $ 3,982,455.79 4 SaskPower $ 281,782.39 $ 3,185,850.21 5 Bank of Montreal - Mastercard $ 157,762.36 $ 2,300,672.48 6 Thorpe Industries Ltd $ 138,119.24 $ 170,852.98 7 Prince Albert Regional Economic Dev Alliance $ 100,000.00 $ 100,000.00 8 PA Separate School Board $ 99,152.72 $ 3,815,407.80 9 Federated Co-Operatives Ltd. $ 81,228.45 $ 1,078,782.18 10 Sask Energy Inc. $ 74,549.56 $ 600,331.80 11 Novus Law Group $ 61,375.95 $ 1,112,017.26 12 CanOps $ 55,921.51 $ 126,676.23 13 Basler Construction Ltd. $ 49,728.00 $ 206,460.00 14 Arctic Refrigeration Inc. $ 49,435.68 $ 305,905.55 15 Clear Tech Industries Inc. $ 45,722.70 $ 673,512.40 16 Playgrounds-R-Us $ 41,445.18 $ 167,340.27 17 Stantec Consulting Ltd. $ 39,956.41 $ 162,585.80 18 Toter, LLC $ 36,803.52 $ 83,793.82 19 Cornerstone Insurance $ 36,546.22 $ 932,953.87 20 Exact Fencing Ltd. $ 34,295.79 $ 94,841.23 21 Sask Housing Corporation $ 25,708.48 $ 25,708.48 22 AECOM Canada Ltd. $ 25,454.99 $ 580,339.53 23 Prince Albert Alarm Systems Ltd $ 25,008.86 $ 32,936.04 24 SPCA $ 24,185.60 $ 389,039.81 25 B & B Construction Group Inc. -

GVRD Board Meeting- June 28, 2006- Agenda

June 15, 2006 NOTICE TO THE GREATER VANCOUVER REGIONAL DISTRICT BOARD OF DIRECTORS You are requested to attend a Regular Meeting of the Greater Vancouver Regional District (GVRD) Board of Directors on Wednesday, June 28, 2006 at 1:30 p.m. in the 2nd Floor Boardroom, 4330 Kingsway, Burnaby, British Columbia. A G E N D A 1. ADOPTION OF THE AGENDA 1.1 June 28, 2006 Regular Meeting Agenda Staff Recommendation: That the GVRD Board adopt the agenda for the GVRD Board regular meeting scheduled for June 28, 2006 as circulated. 2. ADOPTION OF THE MINUTES 2.1 May 24, 2006 Special Meeting Minutes Staff Recommendation: That the GVRD Board adopt the minutes for the GVRD Board special meeting held May 24, 2006 as circulated. 2.2 May 26, 2006 Regular Meeting Minutes Staff Recommendation: That the GVRD Board adopt the minutes for the GVRD Board regular meeting held May 26, 2006 as circulated. 3. DELEGATIONS No delegations presented. 4. PARKS REPORTS 4.1 Pacific Parklands Foundation – Funding and Support Parks Committee Recommendation: That the GVRD Board: a) receive this report as information on activities of the Pacific Parkland Foundation, and; b) request staff develop a proposed multi-year funding program of cash contribution and in-kind support for the Pacific Parklands Foundation as part of GVRD 2007 budget considerations, and that the proposed multi- year funding program be linked to the Pacific Parkland Foundations multi- year business plan. 5. AGRICULTURE REPORTS 5.1 Agriculture Land Protection Agriculture Committee Recommendation: WHEREAS the -

2012 BC Salary Survey Part 1

2012 BC Salary Survey Part 1 Account Broker Insta-Payment Solution $42 000 - $65 000 Account Manager $36,000 - 100,000 Account Manager Jr. BSI Biodegradable Solutions $14/hr Account Manager Sr Services of G. Vancouver $4,295/mon Account Representative New-Line Products $50,000 - $100,000 Accountant $33,000 – 155,000 Accountant Archmetal Industries $33,000 - $43,000 Accountant A/R Public Outreach Fundraising $40,000 Accountant Cost Mansonville Plastics $15 - $25/hr Accountant Jr. Park Place Seniors Living $35,000 - $40,000 Accountant Jr. AG Group $38,000 - $40,000 Accountant Manufacturing J. Bond & Sons Ltd., Mission $20 - $35/hr Accountant Staff-Ent.Lvl Dusangh & Co, CA, Surrey $15/hr Accounting Assistant $35,000 - $60,000 Accounting Assistant UNFI Canada Grocery $35,000 - $39,000 Accounting Assistant Capilano University $3,520 - $3,962/mon Accounting Clerk $28,000 - $52,000 Accounting Clerk Pacific Quorum $28,000 - $30,000 Accounting Clerk M and J Woodcrafts Ltd. $15 - $16/hr Accounting Clerk ZAG Global $38,000 Accounting Clerk Thomas Skinner & Son $11 - $18/hr Accounting Clerk PPSL Head Office $14 - $16/hr Accounting Clerk Cultus Lake Park Board $18 - $25/hr Accounting Clerk Cancork Floor Inc. $12/hr Accounting Clerk Aspects Financial Services $12/hr Accounting Clerk Hana Fisheries Inc. $12 - $14/hr Accounting Clerk City of Abbotsford $24.48 - $28.80/hr Accounting Clerk Hamilton Duncan Armstrong $32,000 - $34,000 Accounting Clerk 1 City of Burnaby $3,232 - $3,791/mon Accounting Clerk 1 Corporation of Delta $23.96 - $28.14/hr Accounting Clerk 2 City of Burnaby $3,646 - $4,283/mon Accounting Clerk I City of Burnaby $3,232 - $3,791/mon Accounting Officer Vancouver Int’l College $2,000 - $3,000/mon Accounting Services Mgr Measure Accounting $60,000 Accounts Payable Clerk $13.50 - $36/hr Accounts Payable Clerk Advanced Nutrients $13.50/hr Accounts Payable/Logistics ROI Recreation $36,000 Accounts Receivable Clerk $16 - $35/hr Accounts Receivable Clerk BE Pressure Supply $34,000 - $40,000 Ad Writer (online ad) Milo Enterprises Inc. -

Your Guide to the North Peace 2021 Online

Your Guide to the North Peace Traditional Territory of the Dane-zaa First Nation Peoples. SUPPORTING OUR LOCAL ECONOMY 1 | 2021 FORT ST. JOHN & REGION GUIDE We would like to thank all of our advertisers; without their support this publication would not be possible. PLEASE TELL OUR ADVERTISERS YOU SAW THEIR AD IN THIS MAGAZINE. diverse. vast. abundant. Fort St. John & Area to the Peace River Regional District! Your Guide Your Guide to the North Peace to the North Peace Traditional Territory of the The Peace River Regional District (PRRD) Dane-zaa First Nation Peoples. is BC’s largest. The PRRD coordinates SUPPORTING OUR LOCAL services and provides infrastructure in ECONOMY electoral (rural) areas and between member municipalities, including: • Solid waste management • Rural water services 1 | 2021 FORT ST. JOHN & REGION GUIDE • Fire protection • Invasive plant control VIEW THE GUIDE ONLINE! Contents • Sewage collection and disposal www.fsjchamber.com Regional Overview .................................4-7 • Regional parks and campgrounds British Communities of the North eaceP .........8-11 • Building inspection Columbia For additional copies contact: Chamber President Message .....................8 • Development and land use planning Meet the Chamber ............................ 12-13 Executive Director Message .................... 14 Go to prrd.bc.ca for more information. Treaty 8 ................................................... 16 Message from our MLA ........................... 17 Britis Columb Tel: 250 785 6037 h Message from Mayor Ackerman ............. 18 Contributors ia [email protected] Our Industries .................................... 20-25 The Fort St. John & Area Oil & Gas ........................................... 28-31 Community Guide is well Britis A Community Space Columb Energy Sector Contributes ................. 32-33 supported by our Business h Community, the City of Fort ia Alternative Energy ............................ -

Environmental Scan June 2008

ENVIRONMENTAL SCAN JUNE 2008 This page left intentionally blank. TABLE OF CONTENTS TABLE OF CONTENTS ................................................................................................................ i EXECUTIVE SUMMARY ............................................................................................................. iii 1. KWANTLEN REGION: A DEMOGRAPHIC PROFILE ............................................. 1 1.1 Population Annual Percentage Change 2002-2007…………………………………………… ......... 1 1.2 Projected Population Change 2007-2016 by Municipality ............................................. 4 1.3 Projected Population Change 2007-2016 by Selected Age Group .................................. 5 1.4 Decomposition of Changes in Population Cohorts in Selected College Regions ………….…7 2. IMMIGRATION .............................................................................................................. 11 2.1 Concentration of Immigrants within the Kwantlen Region ............................................ 12 2.2 Immigrant Status and Period of Immigration .............................................................. 13 2.3 Origin of Immigrants................................................................................................ 15 3. EDUCATION WITHIN THE KWANTLEN REGION .......................................................... 17 3.1 Educational Attainment by Age ................................................................................. 17 3.2 Percentage of Population 15+ with University Degree………………………………………… -

British Columbia Hydro and Power Authority

BRITISH COLUMBIA HYDRO AND POWER AUTHORITY Financial Information Act Return for the Year Ended March 31, 2017 Published in accordance with the Financial Information Act, Revised Statutes of British Columbia 1996, Chapter 140, as amended. FINANCIAL INFORMATION ACT RETURN FOR THE YEAR ENDED MARCH 31, 2017 TABLE OF CONTENTS A. Audited Consolidated Financial Statements F2017 B. British Columbia Hydro and Power Authority and its subsidiary Powerex Corp. Schedule of Remuneration and Expenses – Board of Directors C. British Columbia Hydro and Power Authority Schedule of Remuneration and Expenses – General Schedule of Remuneration and Expenses – Employees Schedule of Payments to Suppliers for Goods and Services Statement of Grants and Contributions D. Columbia Hydro Constructors Ltd. Schedule of Remuneration and Expenses – General Schedule of Remuneration and Expenses – Employees Schedule of Payments to Suppliers for Goods and Services E. Powerex Corp. Schedule of Remuneration and Expenses – General Schedule of Remuneration and Expenses – Employees Schedule of Payments to Suppliers for Goods and Services F. Powertech Labs Inc. Schedule of Remuneration and Expenses – General Schedule of Remuneration and Expenses – Employees Schedule of Payments to Suppliers for Goods and Services 2 British Columbia Hydro and Power Authority MANAGEMENT REPORT The consolidated financial statements of British Columbia Hydro and Power Authority (BC Hydro) are the responsibility of management and have been prepared in accordance with the financial reporting provisions prescribed by the Province of British Columbia pursuant to Section 23.1 of the Budget Transparency and Accountability Act and Section 9.1 of the Financial Administration Act (see Note 2(a)). The preparation of financial statements necessarily involves the use of estimates which have been made using careful judgment. -

From Ideas to Action – CIPEC Annual Report 2015

FROM IDEAS TO ACTION CIPEC ANNUAL REPORT 2015 Canadian Industry Program for Energy Conservation FROM IDEAS TO ACTION CIPEC ANNUAL REPORT 2015 Canadian Industry Program for Energy Conservation Aussi disponible en français sous le titre : Des idées à l’action – Rapport annuel du PEEIC de 2015 © Her Majesty the Queen in Right of Canada, as represented by the Minister of Natural Resources, 2016 For information regarding reproduction rights, contact Natural Resources Canada at [email protected]. Cat. No. M141-3E-PDF (Online) ISSN 1920-3349 Contents Celebrating 40 Years: Facts at a Glance ................. 2 Industry Sector Profiles ........................................ 17 CIPEC Leader Companies by Sector ................... 66 Aluminum ....................................................... 18 About CIPEC ......................................................... 4 CIPEC Trade Associations ................................... 83 Brewery .......................................................... 20 Our Mission ........................................................... 5 Cement .......................................................... 22 Contacts – NRCAN, OEE, Industry Division ......... 84 Chemicals ....................................................... 24 Contact CIPEC ..................................................... 5 Construction ................................................... 26 Dairy ............................................................... 28 Message From the Chair....................................... -

Finance and Intergovernment Committee Meeting Agenda

METRO VANCOUVER REGIONAL DISTRICT FINANCE AND INTERGOVERNMENT COMMITTEE REGULAR MEETING Friday, June 12, 2020 1:00 pm 28th Floor Boardroom, 4730 Kingsway, Burnaby, British Columbia A G E N D A1 1. ADOPTION OF THE AGENDA 1.1 June 12, 2020 Regular Meeting Agenda That the Finance and Intergovernment Committee adopt the agenda for its regular meeting scheduled for June 12, 2020 as circulated. 2. ADOPTION OF THE MINUTES 2.1 May 13, 2020 Regular Meeting Minutes That the Finance and Intergovernment Committee adopt the minutes of its regular meeting held May 13, 2020 as circulated. 3. DELEGATIONS 4. INVITED PRESENTATIONS 5. REPORTS FROM COMMITTEE OR STAFF 5.1 Affordable Housing Development Reserve Fund Bylaw No. 1309, 2020 Designated Speaker: Dean Rear, Chief Financial Officer/General Manager, Financial Services and Heather McNell, General Manager, Regional Planning and Housing Services That the MVRD Board: a) establish a new statutory reserve for the Affordable Housing function to receive, hold and provide funds for new affordable housing development; and b) give first, second, and third reading to the Affordable Housing Development Reserve Fund Bylaw No. 1309, 2020; and c) pass and finally adopt the Affordable Housing Development Reserve Fund Bylaw No. 1309, 2020. 1 Note: Recommendation is shown under each item, where applicable. June 5, 2020 Finance and Intergovernment Committee Finance and Intergovernment Committee Regular Agenda June 12, 2020 Agenda Page 2 of 3 5.2 2019 Statement of Financial Information Designated Speaker: Dean Rear, Chief Financial Officer/General Manager, Financial Services That the MVRD Board approve the Statement of Financial Information for the year ended December 31, 2019. -

Download the Face of Leadership™ BC Score Card 2015

The Face of Leadership™ BC SCORE CARD 2015 1 Foreword 2 Introductory comments by Tamara Vrooman 3 Executive Summary 5 Why Is This Important? 5 The Youth Perspective 6 An Interview with Tina Keeper 7 Methodology 9 Key Findings 10 Overall Results 11 Consumer Discretionary / Consumer Staples 13 Energy 14 Financials 15 Health Care 16 Industrials 17 Information Technology 18 Materials 19 Telecommuniation Services 20 Utilities 22 About Us THE FACE OF LEADERSHIPTM Authors Samantha Jo Simmonds, The Minerva Foundation for BC Women Michael Yow and Jeremy Chan, Corporate Knights Capital Design jimryce.com Michelle Cormack A Girl Named Fred Design + Communication Strategic Counsel Lyn Brown RESEARCH PARTNER FUNDING PARTNER IN-KIND PARTNER The Minerva Foundation for BC Women offers Corporate Knights Capital (CKC) is an investment unique programs for women to develop their advisory and research firm based in Toronto, leadership capacity and reach their full potential. Canada. CKC is a certified B Corporation and a From leadership programs to education awards, proud signatory of the United Nations-supported and culturally-relevant programming developed in Principles for Responsible Investment (PRI). CKC’s partnership with Aboriginal women, Minerva elevates mission is to accelerate the transition to long-term, the visibility, influence and contribution of women to sustainable capitalism by building world-class change the face of leadership in BC. Since 2001, investment portfolios for the global investment Minerva has directed more than $10,000,000 community. For more information about CKC, towards leadership and career exploration please visit www.corporateknightscapital.com. programming for women and girls. FOREWORD Follow the Leader STUDIES SHOW consistently that Score Card shows the BC results the study sample are serving on board gender diversity correlates with better fare as well as, or better than, chosen committees. -

Financial Information Act Return for the Year Ended March 31, 2020

BRITISH COLUMBIA HYDRO AND POWER AUTHORITY Financial Information Act Return for the Year Ended March 31, 2020 Published in accordance with the Financial Information Act, Revised Statutes of British Columbia 1996, Chapter 140, as amended. 1 FINANCIAL INFORMATION ACT RETURN FOR THE YEAR ENDED MARCH 31, 2020 TABLE OF CONTENTS Statement of Financial Information Approval 3 Audited Consolidated Financial Statements Fiscal 2020 4 British Columbia Hydro and Power Authority and its subsidiary Powerex Corp. Schedule of Remuneration and Expenses – Board of Directors 73 British Columbia Hydro and Power Authority Schedule of Debts 75 Schedule of Guarantee and Indemnity Agreements 76 Schedule of Remuneration and Expenses 77 Schedule of Payments to Suppliers for Goods and Services 154 Statement of Grants and Contributions 191 Powerex Corp. Schedule of Remuneration and Expenses 192 Schedule of Payments to Suppliers for Goods and Services 196 Powertech Labs Inc. Schedule of Remuneration and Expenses 200 Schedule of Payments to Suppliers for Goods and Services 204 2 BRITISH COLUMBA HYDRO AND POWER AUTHORITY STATEMENT OF FINANCIAL INFORMATION APPROVAL The undersigned represents the Board of Directors of the British Columbia Hydro and Power Authority and approves the information contained in the Statement and Schedules of Financial Information prepared in accordance with the Financial Information Act. Kenneth G. Peterson Chair of the Board 3 British Columbia Hydro and Power Authority Management Report The consolidated financial statements of British Columbia Hydro and Power Authority (BC Hydro) are the responsibility of management and have been prepared in accordance with International Financial Reporting Standards. The preparation of financial statements necessarily involves the use of estimates which have been made using careful judgment. -

Membership Directory

2013/2014 Membership Directory The Richmond Chamber of Commerce is recognized as the leading business organization in Richmond, committed to the development and enhancement of the economic well being of our community. RBC Dominion Securities Inc. Personal advice makes all the difference RBC Dominion Securities is proud to serve Richmond families Our team delivers solutions for all aspects of your financial life, and businesses. Our team of Investment Advisors are active from wealth management to financial and insurance planning. members in the community, supporting events and causes that If you have any needs in these areas, please contact any of our benefit the Richmond area. qualified Investment Advisors. The Investment Advisors of RBC Dominion Securities, Richmond SANDRA NASS ALAN RAE BILL JAFFE KAM SAHOTA ANTHONY CHEUNG CHARLIE CHAN VP & Investment Advisor Vice President & Director VP & Portfolio Manager Investment Advisor Investment Advisor Investment Advisor [email protected] [email protected] [email protected] [email protected] [email protected] [email protected] 604-718-3111 604-665-0666 604-665-0677 604-718-3122 604-718-3882 604-718-3109 KENT CHEN RICHARD RAND CHUNLIN LI NOËL PHILIPPOT PETER WONG RUSSELL MACKAY Investment Advisor Investment Advisor Investment Advisor Investment Advisor Investment Advisor Investment Advisor [email protected] [email protected] [email protected] [email protected] [email protected] [email protected] 604-257-7678 604-665-8117 604-257-7463 604-257-7693 604-257-7159 604-257-7082