Malaysia Astro Malaysia Holdings

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IPR2013 Bahasa Malaysia.Pdf

KEPERLUAN STATUTORI Mengikut Bahagian V, Bab 15, Seksyen 123-125 Akta Komunikasi dan Multimedia 1998, dan Bahagian II, Seksyen 6 Akta Perkhidmatan Pos 2012, Suruhanjaya Komunikasi dan Multimedia Malaysia dengan ini menerbitkan dan menghantar kepada Menteri Komunikasi dan Multimedia salinan Laporan Prestasi Industri (IPR) bagi tahun berakhir 31 Disember 2013. 2 SURUHANJAYA KOMUNIKASI DAN MULTIMEDIA MALAYSIA (MCMC), 2014 Maklumat atau bahan dalam penerbitan ini dilindungi di bawah hak cipta dan, kecuali jika dinyatakan sebaliknya, boleh disalin semula untuk kegunaan bukan perdagangan dengan syarat ianya disalin dengan tepat dan tidak digunakan dalam konteks yang mengelirukan. MCMC sebagai sumber bahan, hendaklah dikenalpasti dan taraf hakcipta diperakui bagi mana-mana bahan yang perlu disalin semula. Kebenaran untuk menyalin tidak merangkumi mana-mana maklumat atau hak cipta yang dimiliki oleh individu, organisasi atau pihak ketiga. Kebenaran atau menyalin semula makumat atau bahan tersebut hendaklah diperolehi daripada pemilik hak cipta berkenaan. Semua kerja ini adalah berdasarkan sumber-sumber yang boleh dipercayai, tetapi MCMC tidak menjamin ketepatan atau kesempurnaan apa-apa maklumat untuk sebarang tujuan dan tidak boleh bertanggungjawab bagi apa-apa kesilapan atau ketinggalan yang ketara. Diterbitkan oleh: Suruhanjaya Komunikasi dan Multimedia Malaysia Off Persiaran Multimedia 63000 Cyberjaya, Selangor Darul Ehsan T: +603 8688 8000 F: +603 8688 1000 Talian Bebas Tol: 1- 800-888-030 Laman Sesawang: www.mcmc.gov.my ISSN 1823 – 3724 -

AKSHAYA DIGINET CABLE VISION PRIVATE LIMITED Broadcasters Bouquets

AKSHAYA DIGINET CABLE VISION PRIVATE LIMITED Broadcasters Bouquets TOTAL BROADCASTER BOUQUET NAME CHANNELS DRP CHANNELS SUN TV, SUN NEWS, SUN MUSIC, SUN LIFE, KTV, CHUTTI TV, TAMIL BASIC 7 ₹ 40.00 ADITHYA TV KUSHI TV, GEMINI TV, GEMINI NEWS, GEMINI MUSIC, TELUGU BASIC 7 ₹ 30.00 GEMINI MOVIES, GEMINI LIFE, GEMINI COMEDY SUN TV, KUSHI TV, KTV, GEMINI TV, GEMINI NEWS, GEMINI TELUGU PRIME 9 ₹ 40.00 MUSIC, GEMINI MOVIES, GEMINI LIFE, GEMINI COMEDY SURYA TV, SURYA MUSIC, SURYA MOVIES, SURYA COMEDY, KERALA BASIC 5 ₹ 20.00 KOCHU TV UDAYA TV, SURYA TV, SURYA MUSIC, SURYA MOVIES, KERALA PRIME 8 ₹ 35.00 SURYA COMEDY, SUN TV, KTV, KOCHU TV UDAYA TV, UDAYA NEWS, UDAYA MUSIC, UDAYA MOVIES, KANNDA BASIC 6 ₹ 30.00 UDAYA COMEDY, CHINTU TV SUN UDAYA TV, UDAYA NEWS, UDAYA MUSIC, UDAYA MOVIES, KANNADA PRIME 9 ₹ 45.00 UDAYA COMEDY, SUN TV, KTV, GEMINI TV, CHINTU TV SUN TV, KTV, ADITHYA, SUN MUSIC, CHUTTI, SUN NEWS, SUN LIFE, GEMININ TV, GEMINI MOVIES, GEMINI COMEDY, GEMINI MUSIC, KUSHI TV, GEMINI LIFE, UDAYA TV, UDAYA SUN ULTIMATE 23 ₹ 65.00 MOVIES, UDAYA COMEDY, UDAYA MUSIC, CHINTU TV, SURYA TV, SURYA MOVIES, KOCHU TV, SURYA MUSIC, SURYA COMEDY. SUN TV HD, KTV HD, ADITYA TV, SUN MUSIC HD, CHUTTI TAMIL BASIC HD 7 ₹ 70.00 TV, SUN NEWS, SUN LIFE SUN TV, KTV, ADITHYA, SUN MUSIC, CHUTTI TV, SUN NEWS, TAMIL SUPER SUN LIFE, GEMINI TV, GEMINI MOVIES, SURYA TV, SURYA 11 ₹ 50.00 MOVIES JAYA BOUQUET-1 JAYA TV, JAYA PLUS, JAYA MAX, J MOVIE 4 ₹ 10.50 MEGA BOUQUET-1 MEGA TV, MEGA MUSIC, MEGA 24 3 ₹ 02.80 RAJ BOUQUET-1 RAJ TV, RAJ MUSIX, RAJ DIGITAL PLUS, -

Recognising Perak Hydro's

www.ipohecho.com.my FREE COPY IPOH echoechoYour Voice In The Community February 1-15, 2013 PP 14252/10/2012(031136) 30 SEN FOR DELIVERY TO YOUR DOORSTEP – ISSUE ASK YOUR NEWSVENDOR 159 Malaysian Book Listen, Listen Believe in Royal Belum Yourself of Records World Drums and Listen broken at Festival 2013 Sunway’s Lost World of Tambun Page 3 Page 4 Page 6 Page 9 By James Gough Recognising Perak Hydro’s Malim Nawar Power Staion 2013 – adaptive reuse as a training Contribution to Perak and maintenance facility adan Warisan Malaysia or the Malaysian Heritage BBody, an NGO that promotes the preservation and conservation of Malaysia’s built Malim Nawar Power Station 1950’s heritage, paid a visit recently to the former Malim Nawar Power Station (MNPS). According to Puan Sri Datin Elizabeth Moggie, Council Member of Badan Warisan Malaysia, the NGO had forwarded their interest to TNB to visit MNPS to view TNB’s effort to conserve their older but significant stations for its heritage value. Chenderoh Dam Continued on page 2 2 February 1-15, 2013 IPOH ECHO Your Voice In The Community “Any building or facility that had made a significant contribution to the development of the country should be preserved.” – Badan Warisan Malaysia oggie added that Badan Warisan was impressed that TNB had kept the to the mining companies. buildings as is and practised adaptive reuse of the facility with the locating of Its standard guideline was MILSAS and REMACO, their training and maintenance facilities, at the former that a breakdown should power station. not take longer than two Moggie added that any building or facility that had made a significant contribution hours to resume operations to the development of the country should be preserved for future generations to otherwise flooding would appreciate and that power generation did play a significant part in making the country occur at the mine. -

Bayaran Khas Aidilfitri Penggerak Masjid, Surau

www.selangorkini.my @Media_Selangor selangortv.my MediaSelangor PERCUMA 23 - 29 Mei 2019, 18 - 24 Ramadan 1440 Penjawat awam gembira Harga 27 barangan Diego Maradona boikot Budaya malam tujuh likur terima bonus tiga bulan dikawal sempena Aidilfitri filem kisah hidup semakin ditelan zaman Bayaran khas Aidilfitri penggerak masjid, surau OLEH NADIAH ZAMLUS & NORHAYATI UMOR GOMBAK - Selangor menyediakan peruntukan khas RM400 seorang bagi penggerak masjid dan RM300 seorang bagi petugas surau ber- sempena sambutan Aidilfitri awal Jun ini. Nazir, dua imam, dua bilal, dan dua siak masjid di seluruh negeri mendapat bayaran khas itu dikenali Insentif Mahabbah Ramadan yang diumumkan 17 Mei lalu. DIGITAL Untuk surau, kerajaan negeri me- nyediakan bayaran khas kepada pe- ngerusi surau, dua imam, bilal dan siak. Dato Menteri Besar, Amirudin Shari berkata, insentif yang me- rangkumi 12,995 penerima itu membabitkan 2,053 surau dan 390 masjid di serata Selangor. Kerajaan Negeri memperuntuk- kan RM4.17 juta untuk tujuan ini, se- lain bayaran khas sebulan gaji untuk kakitangan awam dan agensi-agen- si terpilih bawah kerajaan negeri. “Kerajaan Negeri sentiasa mema- hami bebanan tugas yang dihadapi pihak pengurusan masjid dan surau, Dato' Menteri Besar bersama pemimpin Kerajaan Negeri dan penjawat awam menunjukkan simbol ' bonus tiga bulan' selepas sepanjang Ramadan. Ada di antara mengumumkan Insentif Mahabbah Selangor di Dewan Jubli Perak, Shah Alam pada 17 Mei. Foto oleh Asri Sapfie petugas termasuk nazir, imam, bilal dan siak yang bekerja 24 jam. Kerajaan Negeri ketika Program 19,244 penjawat awam negeri jabatan Persekutuan yang ber- khas sebanyak tiga bulan gaji “Jika ada program sahur, awal- Iftar Bersama Jemaah Masjid At- membabitkan peruntukan RM khidmat di negeri ini. -

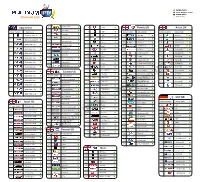

Distributor Retail Price of Broadcaster Bouquet

DISTRIBUTOR RETAIL PRICE OF BROADCASTER BOUQUET SL NO OF STAR INDIA PVT LTD PACAKGE NO CHANNELS RATE* NAME ASIANET, ASIANET MOVIES, ASIANET PLUS, STARSPORTS1, STARSPORTS2, STARSPORTS3, STAR YES SILVER- SPORTS FIRST, NATIONAL GEOGRAPHIC,NATIONAL GEOGRAPHIC WILD. STAR 1 9 39.00 VIJAY, VIJAY SUPER, STAR SPORTS1 TAMIL / HINDI, STARSPORTS2, STAR SPORTS 3, STAR SPORTS YES GOLD- 2 11 FIRST, NATIONAL GEOGRAPHIC, NATIONAL GEOGRAPHIC WILD, ASIANET, ASIANET MOVIES, ASIANET 49.00 STAR PLUS. ASIANET HD, ASIANET MOVIES, ASIANET PLUS, STAR SPORTS HD 1, STAR SPORTS HD 2, STAR SPORTS 3, STAR SPORTS FIRST, NATIONAL GEOGRAPHIC HD, NAT GEO WILD HD, STAR PLUS HD , STAR BHARAT STAR 55- HD , STAR UTASAV , STAR UTSAV MOVIES , MOVIES OK , UTV HD , UTV ACTION , UTV MOVIES , UTV 3 19 95.00 MAL- HD- BINDASS PREMI ASIANET , ASIANET MOVIES, ASIANET PLUS, STAR SPORTS 1, STAR SPORTS 2, STAR SPORTS 3, STAR SPORTS FIRST, NATIONAL GEOGRAPHIC , NAT GEO WILD , STAR PLUS , STAR BHARAT , STAR UTASAV , STAR UTSAV MOVIES , MOVIES OK , UTV ACTION , UTV MOVIES , UTV BINDASS YES STAR 4 18 59.00 HIN- MAL VALUE STAR MOVIES ,STAR WORLD , FOX LIFE. YES STAR 5 3 15.00 ENG MINI ASIANET HD, ASIANET MOVIES, ASIANET PLUS, STAR SPORTS HD 1, STAR SPORTS HD 2, STAR SPORTS YES STAR 3, STAR SPORTS FIRST, NATIONAL GEOGRAPHIC HD, NAT GEO WILD HD HD MLM 6 9 75.00 VIJAY, VIJAY SUPER, STAR SPORTS1 TAMIL / HINDI, STARSPORTS2, STAR SPORTS 3, STAR SPORTS YES STAR FIRST, NATIONAL GEOGRAPHIC, NATIONAL GEOGRAPHIC WILD . TAMIL 7 8 25.00 ASIANET HD, ASIANET MOVIES, ASIANET PLUS, STAR SPORTS HD 1, STAR SPORTS HD 2, STAR SPORTS YES PLATI- 3, STAR SPORTS FIRST, NATIONAL GEOGRAPHIC HD, NAT GEO WILD HD, STAR SPORTS SELECT HD 1, STAR MLM STAR SPORTS SELECT HD2, STAR MOVIES HD, STAR MOVIES SELECT HD, STAR WORLD HD, STAR HD 8 17 WORLD PREMIERE HD, FOX LIFE HD, BABY TV HD. -

Liste Des Chaines

Available channel temporary unabled channel disabled channel Channels List channel replay Setanta Sport 46 92 Gold Family UK Asian UK 47 Box Nation channel number channel name 93 Dave channel number channel name channel number channel name 48 ESPN HD 1 beIN Sports News HD 94 Alibi 104 SKY ONE 158 Zee tv UK 49 Eurosport UK 95 E4 105 Sky Two UK 159 Zee cinema UK 2 Bein Sports Global HD 50 Eurosport 2 UK 96 More 4 106 Sky Living 160 Zee Punjabi UK 3 BEIN SPORT 1 HD 51 Sky Sports News 97 Dmax 107 Sky Atlantic UK 161 Zing UK 52 At The Races 4 BEIN SPORT 2 HD 98 5 STAR 108 Sky Arts1 162 Star Gold UK 53 Racing UK 5 BEIN SPORT 3 HD 99 3E 109 Sky Real Lives UK 163 Star Jalsha UK 54 Motor TV 100 Magic 110 Fox UK 164 Star Plus UK 6 BEIN SPORT 4 HD 55 Manchester United Tv 101 TV 3 111 Comedy Central UK 165 Star live UK 7 BEIN SPORT 5 HD 56 Chealsea Tv 102 Film 4 121 Comedy Central Extra UK 166 Ary Digital UK 57 Liverpool Tv 8 BEIN SPORT 6 HD 103 Flava 125 Nat Geo UK 167 Sony Tv UK 113 Food Network 126 Nat Geo Wild uk 168 Sony Sab Tv UK 9 BEIN SPORT 7 HD Cinema Uk 114 The Vault 127 Discovery UK 169 Aaj Tak UK 10 BEIN SPORT 8 HD channel number channel name 115 CBS Reality 128 Discovery Science uk 170 Geo TV UK 60 Sky Movies Premiere UK 11 BEIN SPORT 9 HD 116 CBS Action 129 Discovery Turbo UK 171 Geo news UK 61 Sky Select UK 12 BEIN SPORT 10 HD 130 Discovery History 172 ABP news Uk 62 Sky Action UK 117 CBS Drama 131 Discovery home UK 13 BEIN SPORT 11 HD 63 Sky Modern Great UK 118 True Movies 132 Investigation Discovery 64 Sky Family UK 119 True Movies -

Table of Contents

TABLE OF CONTENTS PAGE Introduction ANANDA KRISHNAN PROFILE AND BACKGROUND 3 - 8 MAXIS COMMUNICATION COMPANY PROFILE 9 - 12 ASTRO COMPANY PROFILE 13 - 20 STYLE OF LEADERSHIP 21 - 24 LEADERSHIP THEORY ADAPTATION 25 Conclusion 26 References 27 1 (a) Background of the leader: the aim of this section is to know and understand the leader as a person and the bases for his/her success. The data and information should be taken from any published sources such as newspapers, company reports, magazines, journals, books etc. INTRODUCTION ANANDA KRISHNAN Who is Ananda Krishnan? According to a report then by Bernama News Agency, the grandfathers of Tan Sri T. Ananda Krishnan and Tan Sri G. Gnanalingam had been brought to Malaysia from Jaffna by British colonial rulers to work in Malaysia¶s Public Works Department, a common practice then as Jaffna produced some of the most educated people in the whole country. Tan Sri Gnanalingam himself told one of our ministers that he wants to put something back into this country because his grandfather was Sri Lankan," Deputy Director-General of Sri Lanka's Board of Investment (BOI) Santhusht Jayasuriya had told a a group of visiting Malaysian journalists then, 2 according to the Bernama 2003 story. Gnanalingam, executive chairman of Malaysia's Westport, held talks with Prime Minister Ranil Wickremesinghe during a visit to Malaysia in 2003 and the former followed up with a visit to Colombo. In the same year a Memorandum of Understanding was formalized in March this year between 'Westport' and the Sri Lanka Ports Authority (SLPA). Westport is keen to invest in Sri Lanka but no formal process has begun. -

SEATRU Newsletter 2010

Vol. 2, No.1 December 2010 SEATRU Newsletter SEATRU Updates on Conservation, Research and Outreach Programs 2010 Message from the Team Leader This year seems to have flown by in a blink. Without realizing it, we are almost at the end of 2010. This year was the second year for my team with SEATRU. With hard work, dedication and commitments from my team members, I can conclude that this year went off better compared to last year. Off course we have encountered few obstacles along the way, but when we work as a team definitely we could overcome each hurdle. The best thing was, as of the previous year we had fun in performing our work, and we have ended this season with joy and laughter! This year the nesting at Chagar Hutang had increased compared to last year. Monitoring was conducted for the whole year from January to December 2010. We have recorded a total of 676 nesting, of which 661 were green turtle nests and 15 were hawksbill turtle nests. From these a total of 40,000 healthy hatchlings were returned back to the sea. Our sincere thanks to all SEATRU volunteers (Slot A to Slot Z) for helping us in monitoring and protecting turtle nests at Chagar Hutang. It has been 18 years since SEATRU first started the sea turtle conservation program at Chagar Hutang. The unit is still very much active and dedicated in saving the sea turtles even though project leaders have changed hands. It is because of your support and action that motivate us to keep on going. -

S.NO CHANNEL NAME 1 SUN TV 2 KTV 3 Adithya TV 4 Sun Music 5

DIGICON TAMIL MAXX - Rs.101.99+GST S.NO CHANNEL NAME 1 SUN TV 2 KTV 3 Adithya TV 4 Sun Music 5 Chutti TV 6 Sun News 7 SUN Life 8 Vijay TV 9 Vijay Super 10 Star Sports 1 Tamil 11 Star Sports 2 12 Star Sports 3 13 Star Sports First 14 National Geographic 15 Nat Geo Wild 16 CNN News 18 17 Colors Tamil 18 FY1 TV18 19 The History Channel 20 News 18 Tamil Nadu 21 News 18 Urdu 22 NICK 23 NICK JR 24 SONIC 25 VH 1 26 Zee Action 27 Zee News 28 Zee Hindustan 29 Living Foodz 30 Zee ETC 31 WION 32 Zee Tamil 33 Zee Keralam 34 Raj TV 35 Raj Digital Plus 36 Raj News 37 Raj Musix 38 Mega TV 39 Mega Musiq 40 Mega 24 41 Jaya TV 42 Jaya Plus 43 Jaya Max 44 J Movies DIGICON TAMIL BASIC - Rs.70+GST S.NO CHANNEL NAME 1 ADITHYA TV 2 CHUTTI TV 3 COLORS TAMIL 4 K TV 5 NEWS18 TN 6 SUN LIFE 7 SUN MUSIC 8 SUN NEWS 9 SUN TV 10 STAR TAMIL 11 WION 12 ZEE ACTION 13 ZEE ETC 14 ZEE HINDUSTAN 15 ZEE KERALAM 16 ZEE NEWS 17 ZEE TAMIL DIGICON FAMILY PACK-Rs.126+GST S.NO CHANNEL NAME 1 AAJ TAK 38 SONIC 2 AAJ TAK TEZ 39 SONY BBC EARTH 3 ADITHYA TV 40 SONY YAY 4 BBC 41 SUN LIFE 5 CARTOON NETWORK 42 SUN MUSIC 6 CHUTTI TV 43 SUN NEWS 7 CNN 44SUN TV 8 CNN NEWS 18 45 TIMES NOW 9 COLORS TAMIL 46 VH1 10 DISNEY 47 VIJAY 11 DISNEY HD 48 WB 12 DISNEY JUNIOR 49 WION 13 DISNEY XD 50 ZEE ACTION 14 ET NOW 51 ZEE ETC 15 FYI 52 ZEE HINDUSTAN 16 HBO 53 ZEE KERALAM 17 HISTORY 54 ZEE NEWS 18 HUNGAMA 55 ZEE TAMIL 19 INDIA TODAY 56 ZOOM 20 K TV 21 MEGA 24 22 MEGA MUSIQ 23 MEGA TV 24 MIRROR NOW 25 MNX 26 MOVIES NOW 27 MTV BEATS HD 28 NEWS 18 TAMIL 29 NEWS 18 URDU 30 NICK 31 NICK JUNIOR 32 POGO 33 -

Latest Rate Card

Connecting brands with Malaysia’s most valuable audience TV Advertising Rate Card • Effective 15 April 2021 Introduction Hi! We appreciate your interest in partnering with us. As the only growing local media platform in Malaysia, you can count on our dedication in delivering customised advertising and marketing solutions for your brand. Together, let’s take your business to the next level across TV, Radio and Digital Platforms, with the added impact of influencers, event activations and marketplaces. We’ve grouped the available TV advertising channels by target audience or interest – Malay, Chinese, Indian, English, GenNext, News and Sports. The advertising rates are priced according to channel value propositions and timebelt viewerships. Enjoy a base rate that starts from RM1,000 for a 30-sec TVC (category x1), with specific pricing ratios for respective durations, as outlined in the following rate table. TV ADVERTISING RATE TABLE (RM GROSS) Category 10 sec 15 sec 20 sec 25 sec 30 sec 35 sec 40 sec 45 sec 50 sec 60 sec x1 500.00 660.00 800.00 900.00 1,000.00 1,180.00 1,300.00 1,500.00 1,700.00 2,000.00 x1.5 750.00 990.00 1,200.00 1,350.00 1,500.00 1,770.00 1,950.00 2,250.00 2,550.00 3,000.00 x2 1,000.00 1,320.00 1,600.00 1,800.00 2,000.00 2,360.00 2,600.00 3,000.00 3,400.00 4,000.00 x2.5 1,250.00 1,650.00 2,000.00 2,250.00 2,500.00 2,950.00 3,250.00 3,750.00 4,250.00 5,000.00 x3 1,500.00 1,980.00 2,400.00 2,700.00 3,000.00 3,540.00 3,900.00 4,500.00 5,100.00 6,000.00 x3.5 1,750.00 2,310.00 2,800.00 3,150.00 3,500.00 4,130.00 4,550.00 -

Astro Case Study

Case Study ASTRO RADIO: VIRTUAL CONSOLE TECHNOLOGY MALAYSIA’S LARGEST BROADCASTER REINVENTS RADIO STUDIOS WITH LAWO VIRTUAL MIXING Case Study VIRTUAL MIXING AT ASTRO RADIO “A RADICAL RE-IMAGINING OF WHAT AN ON-AIR STUDIO COULD LOOK LIKE.” Astro Radio, headquartered in Kuala Lumpur, has become one of Southeast Asia‘s most influential broadcasters since their inception in 1996. With 11 radio formats in multiple languages, including the popular Era, Sinar, Gegar, My, Hitz and other channels, Astro Radio reaches over 15.8 million listeners every week in Malaysia alone. Astro began operations in 1996 and immediately became known for their technological excellence, employing a cutting-edge audio routing system and digital broadcast consoles custom manufactured to meet their technical requirements. But by 2006, Astro needed more capabilities and simpler studio workflows, so that on-air talent could focus on content creation rather than technical duties. “Around 2015, we picked up on the touchscreen trend,” says Bala Murali Subramaney, Astro Radio’s Chief Technology Officer. “We envisioned a full-blown radio broadcast console - on a touchscreen. Not a ‘lite’ console with only some console features nor a touchscreen with a console ‘simulation’.” Astro Radio Broadcast Center, Kuala Lumpur The virtual console Astro engineers envisioned would be a true radio broadcast console, with all the features and functionalities of the professional broadcast consoles they relied on. “We took the best features of our first console, analyzed common operator mistakes and asked for improvement suggestions, then we condensed this data into a comprehensive document and presented it as our mandate to Lawo – whose response was the Zirkon-2s modular broadcast console,” says Bala. -

Filem Lakonan Izzue Islam

Filem Lakonan Izzue Islam. Izzue IslamKelahiranMuhammad Izzul Islam bin Mazlan (1990-06-02) 2 Jun 1990 (umur 29)Kota Bharu, Kelantan, MalaysiaKediamanKuala LumpurPendidikanSijil Pelajaran Malaysia (SPM)PekerjaanPelakon, model, penyanyiTahun aktif2010–kiniKetinggian1.75 m (5 ka 8+7⁄8 in)Berat55 kg (121 lb; 8.7 st)PasanganAwin Nurin (k. 2013)Kerjaya muzikGenrePopPekerjaanPenyanyiInstrumenVokalTahun aktif2011–kiniSyarikat rakamanKRU StudiosKegiatan berkaitanForteen (2011-18) Muhammad Izzul Islam bin Mazlan (lahir 2 Jun 1990)[a] ialah seorang penyanyi, pemuzik dan pelakon Malaysia. Memulakan kerjaya seninya dengan berlakon dan seterusnya nyanyian dengan menyertai sebuah kumpulan di bawah naungan KRU Studios iaitu kumpulan Forteen.[1] Beliau mula dikenali selepas memenangi anugerah "Pelakon Terbaik[2] Festival Filem Malaysia ke-25" dan "Hero Baru Terhebat Anugerah Blokbuster 2". Namanya kian meningkat apabila diberikan tanggungjawab menggalas watak utama di dalam drama Sebenarnya, Saya Isteri Dia!.[3] Kehidupan awal Beliau dilahirkan pada 2 Jun 1990 sebagai Muhammad Izzul Islam bin Mazlan di Kota Bharu, Kelantan dan berkelulusan Sijil Pelajaran Malaysia (SPM). Forteen Rencana utama: Kumpulan Forteen Izzue Islam menyertai kumpulan Forteen sewaktu kumpulan ini ditubuhkan pada 2011. Kumpulan ini turut dianggotai Muhammad Ridzuan Sharifuddin (One), Saiful Ridzuan Abdul Hamid (Ariz) dan Mohd Arif Ameerais Azhar (Ameerais). Forteen mula dikenali umum setelah muncul bersama single "Berdua Bersatu" yang dkeluarkan pada 27 Ogos 2011.[4] Album EP sulung mereka, Kita dikeluarkan pada 19 Disember 2013 diterbitkan oleh KRU Records,[5] mengandungi 6 lagu. Pada 2014, KRU Music mengumumkan bahawa Forteen bakal menganjurkan konsert buat pertama kalinya pada 29 Mac 2014 bagi menghargai peminat mereka[6][7] Namun, pihak menganjur telah menunda konsert tersebut kepada tarikh baharu iaitu 26 April 2014 bagi menghormati kejadian pesawat MH370 yang hilang pada 8 Mac 2014.[8][9] Pada Disember 2016, Izzue menafikan khabar angin mengatakan beliau keluar dari Forteen.