2006 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![4910-06-P DEPARTMENT of TRANSPORTATION Federal Railroad Administration [Docket Number FRA-2015-0019] Petition for Waiver of Comp](https://docslib.b-cdn.net/cover/3016/4910-06-p-department-of-transportation-federal-railroad-administration-docket-number-fra-2015-0019-petition-for-waiver-of-comp-493016.webp)

4910-06-P DEPARTMENT of TRANSPORTATION Federal Railroad Administration [Docket Number FRA-2015-0019] Petition for Waiver of Comp

This document is scheduled to be published in the Federal Register on 04/03/2015 and available online at http://federalregister.gov/a/2015-07617, and on FDsys.gov 4910-06-P DEPARTMENT OF TRANSPORTATION Federal Railroad Administration [Docket Number FRA-2015-0019] Petition for Waiver of Compliance In accordance with part 211 of Title 49 Code of Federal Regulations (CFR), this provides the public notice that by a document dated February 27, 2015, Norfolk Southern Corporation (NS) has petitioned the Federal Railroad Administration (FRA) for a waiver of compliance from certain provisions of the Federal railroad safety regulations contained at 49 CFR part 213. FRA assigned the petition Docket Number FRA-2015-0019. Pursuant to 49 CFR 213.113(a), NS requests a waiver from the accepted practice of stop/start rail testing to start a pilot test process for nonstop continuous testing. The projected starting date for implementing the test process would be May 1, 2015, for a period of 3 years. The test process will commence initially on the main tracks of the Dearborn Division Chicago Line (Cleveland, OH, to Chicago, IL, Milepost (MP) CD 181.2–523.3). Once this district has been completed, NS will expand to the following locations: (1) Dearborn Division Cleveland Line (Ravenna to Drawbridge, MP RD 85.9– 123.2), Chicago District (Chicago, IL, to Hobart, IN, MP B 518.7–486.5), Lake Erie District (Euclid to Bay Village B 172.0–197.3); (2) Lake Division Chicago, Fostoria, & 2 Cleveland Districts (Hobart, IN, to Bay Village, OH, MP B 486.5–197.3); (3) -

Federal Register/Vol. 76, No. 135/Thursday, July 14, 2011/Notices

41556 Federal Register / Vol. 76, No. 135 / Thursday, July 14, 2011 / Notices Mississippi Department of trains and engines between CP Bloom at online at http://www.dot.gov/ Transportation, Environmental MP–PT 351.6 near Pittsburg, PA and CP privacy.html. Division, 401 North West Street, Solomon. Issued in Washington, DC on July 7, 2011. • Operations on the Fort Wayne Line, Jackson, MS 39201. Robert C. Lauby, Mississippi Department of Pittsburgh Division from CP Rochester at MP–PC 29.5, near East Rochester, PA Deputy Associate Administrator for Transportation, First District Regulatory & Legislative Operations. Headquarters, 1901 N. Gloster Street, to CP Alliance at MP–PC 83.2. Tupelo, MS 38803. • Operations on the Conemaugh Line, [FR Doc. 2011–17681 Filed 7–13–11; 8:45 am] Federal Railroad Administration, Region Pittsburgh Division from CP Conpit at BILLING CODE 4910–06–P 3, 61 Forsyth Street—Suite 16T20, MP–LC 0.0, near Bolivar, PA to CP Kiski at MP–LC 47.8, near Freeport, PA. Atlanta, GA 30303–3104. DEPARTMENT OF TRANSPORTATION In addition, electronic versions of the A copy of the petition, as well as any Draft EIS and appendices are available written communications concerning the Federal Railroad Administration through FRA’s Web site at http:// petition, is available for review online at www.fra.dot.gov/rpd/freight/3002.shtml http://www.regulations.gov and in [Docket Number FRA–2009–0052] person at the Department of and the MDOT Web site at http:// Petition for Waiver of Compliance www.gomdot.com/Home/Projects/ Transportation’s Docket Operations Studies/Northern/ Facility, 1200 New Jersey Ave., SE., In accordance with Part 211 of Title TupeloRailroadRelocation/Home.aspx. -

Summary and Generalization of the Conrail Electrification Study Results for Application to Other Railroads

/ ) 6 Contract No. DOT-TSC-1686 SUMMARY AND GENERALIZATION OF THE CONRAIL ELECTRIFICATION STUDY RESULTS FOR APPLICATION TO OTHER RAILROADS Edward G. Schwarm Arthur D. Little, Inc. Acorn Park Cambridge, MA 02140 MARCH, 1980 FINAL REPORT Prepared for U.S. DEPARTMENT OF TRANSPORTATION TRANSPORTATION SYSTEMS CENTER Kendall Square Cambridge, MA 02142 Technical Report Documentation Page 1. Report No. 3. Recipient's Catalog No. .4 . Title, and Subti tle 5. Report Date March 27, 1980 Summary and Generalization of the Conrail Electrifi cation Study Results for Application to Other Rail 6e Performing Organization Coda roads DTS-742 8. Performing Organization Report No. 7. Author'*) * Edward G. Schwarm 83054 9, Performing Orgoniration Nomo and Address 10. Work Unit No. (TRAIS) R-933/RR-932 Arthur D. Little, Inc.“ Acorn Park 11. Contract or Grant No. Cambridge, MA 02140 DOT-TSC-1686 13. Type of Report and Period Covered 12. Sponsoring Agency Nome and Address Final Report, April 1979 U.S. Department of Transportation to March 1980 .Federal Railroad.Administration Office of Research and Development T4« Sponsoring Agency Code Washington, D.C. 20590 RRD-22 15. Supplementary Notes * Report prepared under contract to: Transportation Systems Center, U.S. Department of Transportation, Kendall Square, Cambridge, MA 02142 16. Abstract The recent railroad electrification feasibility study of the Conrail line segment from Harrisburg to Pittsburgh is reviewed in this report. Approach to design and operational strategy are discussed. A summary of costs and units for various investment and cost items is presented, escalated into 1980 dollars. Of particular interest to the reader are the comments regarding the more general application of the methodology and cost figures to subsequent railroad electri fication studies. -

Telltales New1.Pub

August Telltales 2010 Newsletter of the Boulder Model Railroad Club Blairsville, PA (shown above) lies between Pittsburgh and Johnstown on the Conemaugh Division of the Pennsylvania Railroad. BMRC member Gary Rauch plans to make Blairsville a focus on his layout and will explain to us this month why it offers so many unique modeling opportunities (more info on page 5). The contest topic is “Locomotive Servicing,” which should result in a fine display of coaling towers, roundhouses, sand facilities and more, so join us for an evening of learning and fun on Thursday, August 12, 7:15 PM (or 6:00 PM for dinner beforehand, as so many members are doing) at the American Legion Hall, 1150 Pine in Louisville . Don’t miss it! EDITORIAL Time is running out! I volunteered to open my home for a layout tour on September 25th and, like others who have stepped forward at various times during the year, I fear I will not complete everything on my “To Do” list before the fateful day. And it doesn’t help that we are in the middle of summer, which means yard work, some traveling, and other stuff that always gets saved up for when the weather will be nice. I’ve attended many layout tours over my time in the BMRC, and I’ve set a rule for myself that I won’t display my layout on another tour unless I have made enough significant changes in it (on it? with it?) to justify asking visitors to come and look at it again. Which explains why I am nervous about getting everything on my list checked off. -

Freight Rail Projects

Pennnsylvania Intercity Passenger and Freight Rail Plan Appendix 9 Freight Rail Projects SEPTEMBER 2010 Appendix 9 Freight Rail Projects In an effort to identify the capital needs of the freight industry in Pennsylvania, PennDOT conducted an extensive outreach initiative, in coordination with the Keystone State Railroad Association, to secure input from all 65 operating railroads within the Pennsylvania freight rail network. This outreach effort included solicitation for planned capital projects at rail-related conferences and e-mail correspondence, as well as follow-up telephone calls during July and August 2010. The project submissions provided in the following table characterize the full extent of known planned capital investments for railroad infrastructure across Pennsylvania as of August 2010. The table is organized alphabetically by railroad and lists projects by implementation timeframe (near-term: 1-3 years, mid-term: 3-5, and long-term: more than 5 years). Brief project descriptions, location, and estimated costs are also included. Project categories were contributed by the Keystone State Railroad Association. PennDOT will also evaluate all submitted projects against the goals and objectives outlined in the Pennsylvania Intercity Passenger and Freight Rail Plan to assist the Department in making future funding decisions. PennDOT’s grant application process will be used to maintain a current list of projects. Appendix 9 – Rail Freight Projects Pennsylvania Intercity Passenger and Freight Rail Plan Connections to the Future 2035 -

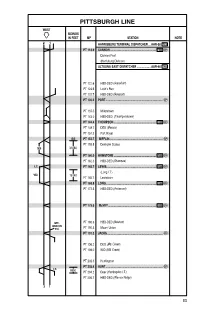

Pittsburgh Line West Sidings in Feet Mp Station Note 2 1 Harrisburg Terminal Dispatcher

PITTSBURGH LINE WEST SIDINGS IN FEET MP STATION NOTE 2 1 HARRISBURG TERMINAL DISPATCHER ... AAR-58 723 PT 118.9 CANNON .............................................................. RM CP Division Post (Harrisburg Division) ALTOONA EAST DISPATCHER ................... AAR-46 146 PT 122.6 HBD-DED (Aquaduct) PT 124.6 Losh’s Run PT 131.7 HBD-DED (Newport) PT 133.5 PORT ............................................................................. CP PT 137.5 Millerstown PT 143.0 HBD-DED (Thompsontown) PT 144.4 THOMPSON ......................................................... RM CP PT 148.7 DED (Mexico) PT 151.2 Port Royal SS PT 153.7 MIFFLIN ........................................................................ CP PT 155.8 Denholm Scales SS 31680 PT 160.0 HAWSTONE ......................................................... RM CP PT 162.3 HBD-DED (Shawnee) I.T. PT 165.7 LEWIS ................................................................... RM CP (Long I.T.) YD. 16140 PT 165.7 Lewistown PT 168.8 LONG .................................................................... RM CP PT 172.3 HBD-DED (Anderson) PT 179.6 McVEY ................................................................. RM CP MT. PT 186.6 HBD-DED (Newton) UNION YD. PT 190.3 Mount Union PT 191.3 JACKS ........................................................................... CP PT 196.2 DED (Mill Creek) PT 198.0 WID (Mill Creek) PT 202.3 Huntingdon PT 202.4 HUNT ............................................................................. CP I.T. 8650 PT 204.2 Deer (Huntingdon -

Pennsylvania's Steel City Gateway

MAP OF THE MONTH Pennsylvania’s Steel City gateway © 2016 Kalmbach Publishing Co., Trains magazine. This material may not be reproduced in any form without permission from the publisher. Your all-time guide to the Pennsy’s main line into Pittsburgh, mapping decades of rail history www.TrainsMag.com Strangford 22 Blairsville Conemaugh Line Westmoreland 22 Blt. as WP 1883; 403 Murrysville Heritage Trail PT300 to PRR 1903 to Saltsburg FUN FACT: Much of ‘Pennsylvanian’ P Line relocated FUN FACT: The eastern the stone for the 1950 and 2014 Delmont Westbound No. 43 Indiana acksaddle Gap o/s Torrance 1906 abutment of the Conemaugh Seward Rockville Bridge was Dep. Johnstown 6:00 p.m. Branch Line bridge at Lockport was quarried near here. s T (Blairsville Jct.) / 22 CKR Dep. Latrobe 6:41 p.m. Conemaugh Dam Site of Blt. 1851, PT285 o CKR FUN FACT: The Conemaugh ab. 1953 built for the Pennsylvania 56 C T flood plain Cokeville Co ugh o Turtle Creek Branch Dep. Greensburg 6:52 p.m. Line is 15 miles longer than nema Canal aqueduct. n Export r Robindale em Lyons Run Jct. Blt. 1910, ab. 1960 Eastbound No. 42 the Pittsburgh Line, but CP PACK Rive Blt. by PRR a PT295 Robinson S Dundale Branch Dep. Greensburg 8:11 a.m. because of its easier water- u ang Hollo Lyons Run Branch ville gh Riv East Pittsburgh Branch Blt. 1900, ab. 1942 New Dep. Latrobe 8:21 a.m. level grades, is used for er Pitcairn Blt. 1893, ab. 1949 Dep. Johnstown 9:04 a.m. -

Danville Flyer a Publication of the Danville Junction Chapter, Inc

DANVILLE FLYER A PUBLICATION OF THE DANVILLE JUNCTION CHAPTER, INC, The DANVILLE FLYER is published monthly by the DANVILLE JUNCTION CHAPTER of the NATIONAL RAILWAY HISTORICAL SOCIETY for its members and other interestedNRHS persons. The DANVILLE JUNCTION CHAPTER, NRHS, is a not-for-profit corporation organized to preserve the history of railroading in Eastern Illinois and Western Indiana and operates a museum located in the former Chicago and Eastern Illinois Railroad depot on East Benton Street in Rossville, Illinois. The museum is open weekends from Memorial Day to Labor Day, noon to 4 PM, and features many railroad displays plus a large operating HO model railroad. Membership in the Chapter is open to anyone having an interest in any aspect of railroading. Dues per year are $12.00 for Chapter membership in addition to $17.00 for NRHS membership. Meetings are held on the third (3rd) Thursday of each month (except July, August and December) at the Cooke Business Forms, N. Vermilion Street, next to the Central Illinois Bank, Danville, Il. beginning at 7:30 PM Central Time. OFFICERS FOR 1997 - Our 29th Year PRESIDENT: Larry Prosser VICE PRESIDENT: Jesse E. Bennett SECRETARY: William Darner TREASURER: Allen Cooke NATIONAL DIRECTOR: R. M. Schroeder PROGRAM CHAIRMAN: William Darner MUSEUM DIRECTOR: Robert Gallippi HISTORIAN: Jesse Bennett EDITOR: Richard M. Schroeder - [email protected] PUBLISHER: Allen Cooke P.O. Box 1013 Cooke Business Forms,Inc. Danville, IL. 61834-1013 John Cooke Sr., Honorary Member MEMBER: Illinois State Historical Society - Illinois Association of Museums Visit our Chapter WWW Home Page On-Line - http://www.prairienet.org/djc-nrhs/ Volume 29 January 1997 Number 1 Coming Events April 5 & 6, 1997 Next Meeting Model Train Show and Swap Meet - Lin- January 16, 1997 The next meeting will be January 16, coln Square Mall, Urbana, IL 10-6 on Sat- 1997 at Cooke Business Forms, 2500 N. -

February 27, 2015 Mr. Robert Lauby Federal Railroad Administration 1200 New Jersey Avenue SE Washington DC, 20590 Dear Mr. Lauby

/ Norfolk Southern Corporation P. G. Merilli D.R. Goode Building Assistant Vice President 1200 Peachtree Street, NE - Box 142 Maintenance of Way & Structures Atlanta, Georgia 30309 (404) 529 -1470 February 27, 2015 Mr. Robert Lauby Federal Railroad Administration 1200 New Jersey Avenue SE Washington DC, 20590 Dear Mr. Lauby: Pursuant to CFR 49 part 213.113(a), Norfolk Southern Railway herby petitions the Federal Railroad Administration (FRA) for a waiver from the accepted practice of stop /start rail testing for a pilot of non -stop continuous rail testing to begin on May 1, 2015 for a period of up to 3 years. Test will commence initially on the main tracks of the Dearborn Division Chicago Line (Cleveland, OH. to Chicago, IL. MP CD 181.2 - 523.3). Once this district has been completed we would like to expand to the following locations: Dearborn Division Cleveland Line (Ravenna to Drawbridge MP RD 85.9 - 123.2), Chicago District (Chicago, IL. to Hobart, IN. MP B 518.7 - 486.5), Lake Erie District (Euclid to Bay Village B 172.0 - 197.3). Lake Division Chicago, Fostoria & Cleveland Districts (Hobart, IN. to Bay Village, OH. MP B 486.5 - 197.3). Pittsburgh Division Fort Wayne Line (Pittsburgh, Pa. - Crestline, Oh. MP PC 0.0 - 188.7), Pittsburgh Line (Pittsburgh, PA. to CP Cannon MP PT 353.5 - 119.1), Conemaugh Line (CP Conpit to CP Penn MP LC 0.0 - 77.9), Lake Erie District (Eculid to Ashtabula B 172.0 - 129.2), Cleveland Line (Ravenna to Alliance MP RD 85.9 - 67.2). -

Norfolk Southern Railway Annual PTC Progress Report for Period 2015

Norfolk Southern Corporation E. A. Hullemeyer 1200 Peachtree Street, N.E. - Box 123 Director Advanced Train Control Atlanta, Georgia, 30309 Systems Mr. Robert C. Lauby Associate Administrator for Railroad Safety / Chief Safety Officer Federal Railroad Administration 1200 New Jersey Avenue, S.E., Mail Stop 25 Washington, DC 20590 March 31, 2016 RE: Norfolk Southern Railway Positive Train Control Progress Report (Docket FRA – 2010- 0060) Dear Mr. Lauby: With the attached document, Norfolk Southern Railway Company (“NSR”) provides its progress report documenting progress toward achieving its planned PTC Implementation. This report is submitted in accordance with 49 U.S.C. 20157(c)(1) and utilizes the structure of Form FRA F 6180.166 (“Form”) OMB Approval granted 3-16-16 for content. Note that because this report covers calendar year 2015, a year for which annual goals were not covered by the revised PTCIP submitted by NSR as required by the PTC Enforcement and Implementation Act (the “Act”), there is not always a match between the NSR provided data requirements set forth in the Act and the “going forward” data requirements of FRA’s Form. For example, NSR’s revised PTCIP did not contain 2015 year-end goals for equipment installation, training, back office and dispatching locations, or route miles in testing, revenue service demonstration, or operation. Accordingly, many columns of data for the annual goals in this report have a response of “N/A.” Notwithstanding the foregoing, NSR has endeavored to provide in its 2015 report both the data elements now required by the Act as well as other meaningful information related to our progress. -

DANVILLE JUNCTION CHAPTER National Railway Historical Society P.O

when the Editor's train rear-ended Allen's stopped train. So much for command control. command for much So train. stopped Allen's rear-ended train Editor's the when the basement of his recently acquired home. Members had a great time, even your Editor and Treasurer had a slight derailment slight a had Treasurer and Editor your even time, great a had Members home. acquired recently his of basement the After the last meeting members visited the O Gauge layout of Secretary Al McCoy. Al recently constructed the new layout in layout new the constructed recently Al McCoy. Al Secretary of layout Gauge O the visited members meeting last the After DANVILLE JUNCTION CHAPTER National Railway Historical Society P.O. Box 1013 Danville IL 61834-1013 The Danville Flyer FIRST CLASS MAIL DANVILLE FLYER A PUBLICATION OF THE DANVILLE JUNCTION CHAPTER, INC. NRHS The DANVILLE FLYER is published monthly by the DANVILLE JUNCTION CHAPTER of the NATIONAL RAILWAY HISTORICAL SOCIETY for its members and other interested persons. The DANVILLE JUNCTION CHAPTER, NRHS, is a not-for-profit corporation organized to preserve the history of railroading in Eastern Illinois and Western Indiana and operates a museum located in the former Chicago and Eastern Illinois Railroad depot on East Benton Street in Rossville, Illinois. The museum is open weekends from Memorial Day to Labor Day and features many railroad displays plus a large operating HO model railroad. Membership in the Chapter is open to anyone having an interest in any aspect of railroading. Dues per year are $17.00 for Chapter membership in addition to $20.00 for NRHS membership. -

TROUBLES on the PENNSYLVANIA CANAL Myron B

TROUBLES ON THE PENNSYLVANIA CANAL Myron B. Sharp of us have read about the Pennsylvania Canal, one of the great engineering feats of the nineteenth century. Mr. MostWillard R. Rhoads wrote a very interesting and informative article about it in the Western Pennsylvania Historical Maga- zine, Vol. 43, No. 3. Mr. William H. Shank wrote The Amazing Pennsylvania Canal, published in 1965 by the Colonial York County Visitors and Tourists Bureau, Inc., York, Pennsylvania, and Mr. Clarence D.Stephenson of Marion Center, Pennsylvania, published a book titled The Pennsylvania Canal in Westmoreland and Indiana Counties in 1961. These books and articles deal for the most part with the construction and operation of the canal system. The follow- ing material was gathered from letters written to Colonel Jacob D. Mathiot while a member of the legislature from 1831 through 1834. These letters are part of the collection known as the Mathiot Papers, 1 now in the possession of The Historical Society of Western Penn- sylvania. They emphasize the damage done to the canal and to the industries along the canal by floods, injustices, charges of corruption and unfair practices by the canal commissioners and other employees. One of the first letters received by Jacob D. Mathiot after his election to the legislature in 1831 was from an engineer by the name of Mr.Philo Ingerson. 2 Mr. Ingerson built two locks on the canal, No. 3 on the Ligonier Line and No. 12 on the Kiskiminitas- Conemaugh Line.3 A Mr. Sylvester Welch, Esq., was the engineer in charge of one of these sections of the canal and made a final estimate of the cost of one of the locks.