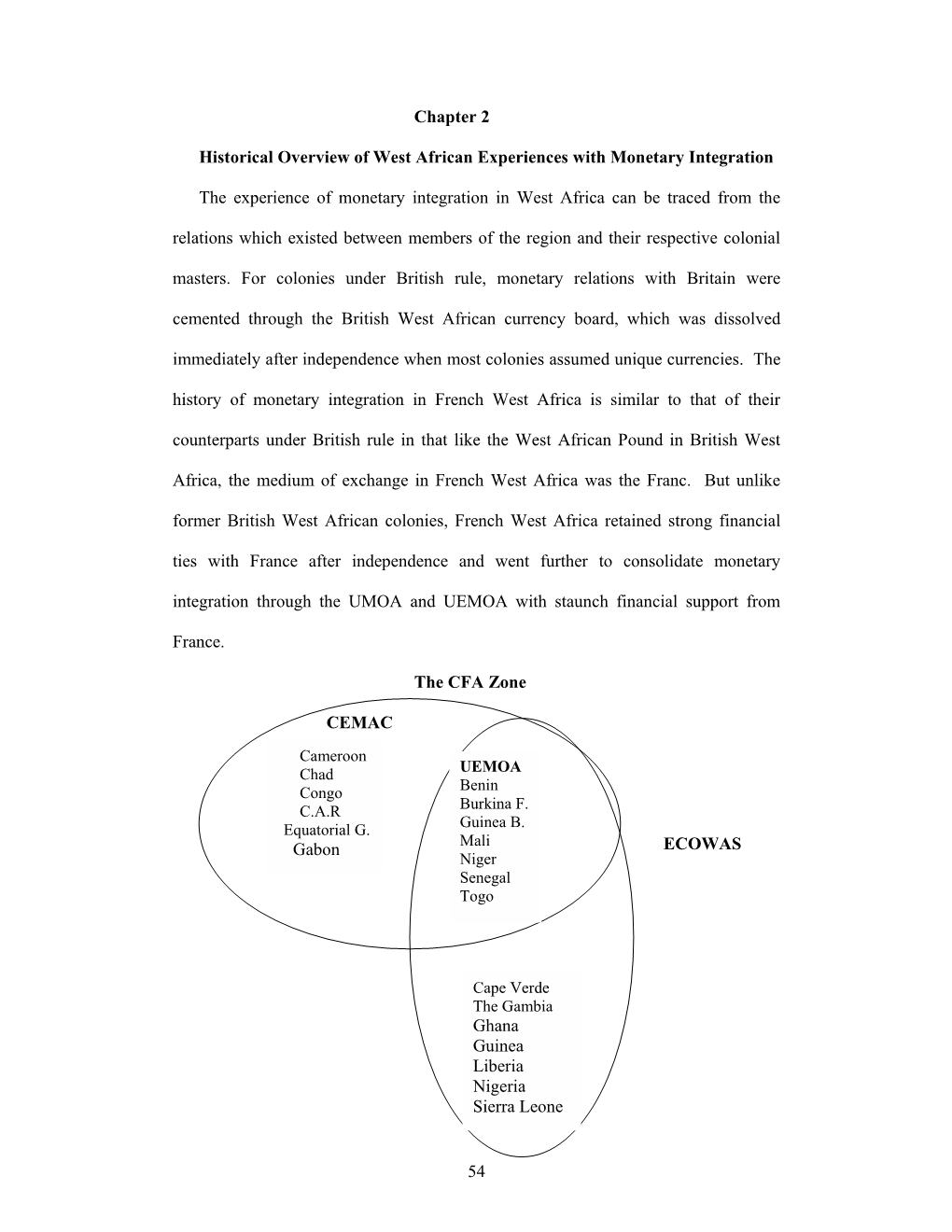

54 Chapter 2 Historical Overview of West African Experiences With

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bibliography

BIbLIOGRAPHY 2016 AFI Annual Report. (2017). Alliance for Financial Inclusion. Retrieved July 31, 2017, from https://www.afi-global.org/sites/default/files/publica- tions/2017-05/2016%20AFI%20Annual%20Report.pdf. A Law of the Abolition of Currencies in a Small Denomination and Rounding off a Fraction, July 15, 1953, Law No.60 (Shōgakutsūka no seiri oyobi shiharaikin no hasūkeisan ni kansuru hōritsu). Retrieved April 11, 2017, from https:// web.archive.org/web/20020628033108/http://www.shugiin.go.jp/itdb_ housei.nsf/html/houritsu/01619530715060.htm. About PBC. (2018, August 21). The People’s Bank of China. Retrieved August 21, 2018, from http://www.pbc.gov.cn/english/130712/index.html. About Us. Alliance for Financial Inclusion. Retrieved July 31, 2017, from https:// www.afi-global.org/about-us. AFI Official Members. Alliance for Financial Inclusion. Retrieved July 31, 2017, from https://www.afi-global.org/sites/default/files/inlinefiles/AFI%20 Official%20Members_8%20February%202018.pdf. Ahamed, L. (2009). Lords of Finance: The Bankers Who Broke the World. London: Penguin Books. Alderman, L., Kanter, J., Yardley, J., Ewing, J., Kitsantonis, N., Daley, S., Russell, K., Higgins, A., & Eavis, P. (2016, June 17). Explaining Greece’s Debt Crisis. The New York Times. Retrieved January 28, 2018, from https://www.nytimes. com/interactive/2016/business/international/greece-debt-crisis-euro.html. Alesina, A. (1988). Macroeconomics and Politics (S. Fischer, Ed.). NBER Macroeconomics Annual, 3, 13–62. Alesina, A. (1989). Politics and Business Cycles in Industrial Democracies. Economic Policy, 4(8), 57–98. © The Author(s) 2018 355 R. Ray Chaudhuri, Central Bank Independence, Regulations, and Monetary Policy, https://doi.org/10.1057/978-1-137-58912-5 356 BIBLIOGRAPHY Alesina, A., & Grilli, V. -

What Makes the CFA Franc Zone a Special Form of Monetary Integration ?

Articles What Makes the CFA Franc Zone a Special Form of Monetary Integration ? Souleymane NDAO* to the overall stability of their competitive positions. Given that the currency was issued Summary: by supranational central banks and that France experienced a relatively high stability The CFA franc zone is the most notable of the price level throughout the 1980s, the example today of a regime change in which countries of the CFA franc zone managed sovereign countries are united not only to use to achieve discipline and credibility in the the same currency unit, but also to add value implementation of their macroeconomic to that of another monetary unit in a fixed policies. relationship. In some important respects, this In addition, the external guarantee zone differs from other monetary unions, mechanism credits, in the form of overdrafts including emerging unification of the European to operations accounts with France, helped currencies, so the traditional criteria applied mitigate some of the effects of the deterioration to identify the optimal monetary zones are of the positions of net foreign assets. Therefore, not sufficient to assess its performance. if the collective well-being depends primarily on It is indeed difficult by using only traditional price stability and growth, belonging to the area criteria to argue that the African franc zone is a has obviously been beneficial to those countries. natural monetary area: the intraregional trade However, the collective well-being also depends is quite limited, the structure of production -

University of Florida Thesis Or Dissertation Formatting

THE POLITICS OF ELECTORAL REFORM IN FRANCOPHONE WEST AFRICA: THE BIRTH AND CHANGE OF ELECTORAL RULES IN MALI, NIGER, AND SENEGAL By MAMADOU BODIAN A DISSERTATION PRESENTED TO THE GRADUATE SCHOOL OF THE UNIVERSITY OF FLORIDA IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY UNIVERSITY OF FLORIDA 2016 © 2016 Mamadou Bodian To my late father, Lansana Bodian, for always believing in me ACKNOWLEDGMENTS I want first to thank and express my deepest gratitude to my supervisor, Dr. Leonardo A. Villalón, who has been a great mentor and good friend. He has believed in me and prepared me to get to this place in my academic life. The pursuit of a degree in political science would not be possible without his support. I am also grateful to my committee members: Bryon Moraski, Michael Bernhard, Daniel A. Smith, Lawrence Dodd, and Fiona McLaughlin for generously offering their time, guidance and good will throughout the preparation and review of this work. This dissertation grew in the vibrant intellectual atmosphere provided by the University of Florida. The Department of Political Science and the Center for African Studies have been a friendly workplace. It would be impossible to list the debts to professors, students, friends, and colleagues who have incurred during the long development and the writing of this work. Among those to whom I am most grateful are Aida A. Hozic, Ido Oren, Badredine Arfi, Kevin Funk, Sebastian Sclofsky, Oumar Ba, Lina Benabdallah, Amanda Edgell, and Eric Lake. I am also thankful to fellow Africanists: Emily Hauser, Anna Mwaba, Chesney McOmber, Nic Knowlton, Ashley Leinweber, Steve Lichty, and Ann Wainscott. -

West Africa from Franco CFA to Eco: Economic Issues

ISSN: 2278-3369 International Journal of Advances in Management and Economics Available online at: www.managementjournal.info REVIEW ARTICLE West Africa from Franco CFA to Eco: Economic Issues Palumbo Vincenzo*, Villani Chiara Universita’ di Napoli Federico II Italy. *Corresponding Author Email: [email protected] Abstract: Born 73 years ago, exactly on December 26, 1945, the day France ratified the Bretton Woods agreements, the CFA franc is the currency adopted by 14 African states and for years the subject of controversy at the local level as well as in France itself. For some months the debate has become international and now this often criticized currency will give way to a new common currency called Eco. Keywords: West Africa, Economic issue, Franco CFA. Article Received: 01 Jan 2021 Revised: 24 Jan 2021 Accepted: 15 Feb. 2021 Introduction First of all, we need to take a big step back in single and independent currency it finally time: It was December 1945 when a decree appears to them as a concrete step in the signed by General Charles de Gaulle actually instituted a currency. Thus was born the direction of real autonomy. But the reality is CFA franc, which at the time when Paris more complex and beyond ideological and ratified the Bretton Woods accords meant political positions there is an objective way in Franco of the French colonies of Africa. which it is possible to approach the issue: economic science. Thus a monetary union was born. The 14 nations that are part of it today are in fact CFA: Economic Technicisms between divided into the Economic and Monetary Advantages and Disadvantages Union of West Africa (UEMOA) and the Substantially, the Economic Technical Economic and Monetary Community of Characteristics on Which the CFA Central Africa (CEMAC). -

Côte D'ivoire Mali

COUNTRY PROFILE 2000 Côte d’Ivoire Mali This Country Profile is a reference tool, which provides analysis of historical political, infrastructural and economic trends. It is revised and updated annually. The EIU’s quarterly Country Reports analyse current trends and provide a two-year forecast. The full publishing schedule for Country Profiles is now available on our website at http://www.eiu.com/schedule The Economist Intelligence Unit 15 Regent St, London SW1Y 4LR United Kingdom The Economist Intelligence Unit The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For over 50 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide. The EIU delivers its information in four ways: through subscription products ranging from newsletters to annual reference works; through specific research reports, whether for general release or for particular clients; through electronic publishing; and by organising conferences and roundtables. The firm is a member of The Economist Group. London New York Hong Kong The Economist Intelligence Unit The Economist Intelligence Unit The Economist Intelligence Unit 15 Regent St The Economist Building 25/F, Dah Sing Financial Centre London 111 West 57th Street 108 Gloucester Road SW1Y 4LR New York Wanchai United Kingdom NY 10019, US Hong Kong Tel: (44.20) 7830 1000 Tel: (1.212) 554 0600 Tel: (852) 2802 7288 Fax: (44.20) 7499 9767 Fax: (1.212) 586 1181/2 Fax: (852) 2802 7638 E-mail: [email protected] E-mail: [email protected] E-mail: [email protected] Website: http://www.eiu.com Electronic delivery This publication can now be viewed by subscribing online at http://store.eiu.com/brdes.html Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-line databases and as direct feeds to corporate intranets. -

Metadata on the Exchange Rate Statistics

Metadata on the Exchange rate statistics Last updated 26 February 2021 Afghanistan Capital Kabul Central bank Da Afghanistan Bank Central bank's website http://www.centralbank.gov.af/ Currency Afghani ISO currency code AFN Subunits 100 puls Currency circulation Afghanistan Legacy currency Afghani Legacy currency's ISO currency AFA code Conversion rate 1,000 afghani (old) = 1 afghani (new); with effect from 7 October 2002 Currency history 7 October 2002: Introduction of the new afghani (AFN); conversion rate: 1,000 afghani (old) = 1 afghani (new) IMF membership Since 14 July 1955 Exchange rate arrangement 22 March 1963 - 1973: Pegged to the US dollar according to the IMF 1973 - 1981: Independently floating classification (as of end-April 1981 - 31 December 2001: Pegged to the US dollar 2019) 1 January 2002 - 29 April 2008: Managed floating with no predetermined path for the exchange rate 30 April 2008 - 5 September 2010: Floating (market-determined with more frequent modes of intervention) 6 September 2010 - 31 March 2011: Stabilised arrangement (exchange rate within a narrow band without any political obligation) 1 April 2011 - 4 April 2017: Floating (market-determined with more frequent modes of intervention) 5 April 2017 - 3 May 2018: Crawl-like arrangement (moving central rate with an annual minimum rate of change) Since 4 May 2018: Other managed arrangement Time series BBEX3.A.AFN.EUR.CA.AA.A04 BBEX3.A.AFN.EUR.CA.AB.A04 BBEX3.A.AFN.EUR.CA.AC.A04 BBEX3.A.AFN.USD.CA.AA.A04 BBEX3.A.AFN.USD.CA.AB.A04 BBEX3.A.AFN.USD.CA.AC.A04 BBEX3.M.AFN.EUR.CA.AA.A01 -

European Economic Integration and the Franc Zone: the Future of the Cfa Franc After 1996

NINETEEN EUROPEAN ECONOMIC INTEGRATION AND THE FRANC ZONE: THE FUTURE OF THE CFA FRANC AFTER 1996 ALLECHI M'BET and AMLAN MADELEINE NIAMKEY AFRICAN ECONOMIC RESEARCH CONSORTIUM CONSORTIUM POUR LA RECHERCHE ECONOMIQUE EN AFRIQUE European economic integration and the Franc Ion©: the future ©f the CFA franc after 1996 Part I: Historical background and a new evaluation of monetary co-operation in the CFA countries Other publications in the AERC Research Paper Series: Structural Adjustment Programmes and the Coffee Sector in Uganda by Germina Ssemogerere, Research Paper 1. Real Interest Rates and the Mobilization of Private Savings in Africa by F.M. Mwega, S.M. Ngola and N. Mwangi, Research Paper 2. Mobilizing Domestic Resources for Capital Formation in Ghana: the Role of Informal Financial Markets by Ernest Aryeetey and Fritz Gockel, Research Paper 3. The Informal Financial Sector and Macroeconomic Adjustment in Malawi by C. Chipeta and M.L.C. Mkandawire, Research Paper 4. The Effects of Non-Bank Financial Intermediaries on Demand for Money in Kenya by S.M. Ndele, Research Paper 5. Exchange Rate Policy and Macroeconomic Performance in Ghana by C.D. Jebuni, N.K. Sowa and K.S. Tutu, Research Paper 6. A Macroeconomic-Demographic Model for Ethiopia by Asmerom Kidane, Research Paper 7. Macroeconomic Approach to External Debt: the Case of Nigeria by S. Ibi Ajayi, Research Paper 8. The Real Exchange Rate and Ghana's Agricultural Exports by K. Yerfi Fosu, Research Paper 9. The Relationship Between the Formal and Informal Sectors of the Financial Market in Ghana by E. Aryeetey, Research Paper 10. -

Brev Til Fortrykt Papir

STATSADVOKATEN FOR SÆRLIG ØKONOMISK OG INTERNATIONAL KRIMINALITET KAMPMANNSGADE 1 1604 KØBENHAVN V TELEFON 72 68 90 00 FAX 45 15 01 19 E-mail: [email protected] Web: www. anklagemyndigheden. dk Web: www. hvidvask. dk Hvidvask XML Ver. 4.0 Content 1. Summary .............................................................................................................................................. 4 2. Conventions used in this document ...................................................................................................... 5 3. Description of XML Nodes .................................................................................................................. 6 3.1 Node ”report” ................................................................................................................................. 6 3.1.1 Subnode report _indicators ...................................................................................................... 8 3.2 Node transaction ............................................................................................................................. 9 3.3 Node Activity ............................................................................................................................... 12 3.4.1 Node t_from_my_client............................................................................................................. 13 3.4.2 Node t_from .............................................................................................................................. 15 -

Côte D'ivoire Mali 1996-97

COUNTRY PROFILE Côte d’Ivoire Mali Our quarterly Country Report on Côte d’Ivoire and Mali analyses current trends. This annual Country Profile provides background political and economic information. 1996-97 The Economist Intelligence Unit 15 Regent Street, London SW1Y 4LR United Kingdom The Economist Intelligence Unit The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For over 40 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide. The EIU delivers its information in four ways: through subscription products ranging from newsletters to annual reference works; through specific research reports, whether for general release or for particular clients; through electronic publishing; and by organising conferences and roundtables. The firm is a member of The Economist Group. London New York Hong Kong The Economist Intelligence Unit The Economist Intelligence Unit The Economist Intelligence Unit 15 Regent Street The Economist Building 25/F, Dah Sing Financial Centre London 111 West 57th Street 108 Gloucester Road SW1Y 4LR New York Wanchai United Kingdom NY 10019, USA Hong Kong Tel: (44.171) 830 1000 Tel: (1.212) 554 0600 Tel: (852) 2802 7288 Fax: (44.171) 499 9767 Fax: (1.212) 586 1181/2 Fax: (852) 2802 7638 Electronic delivery EIU Electronic Publishing New York: Lou Celi or Lisa Hennessey Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 London: Moya Veitch Tel: (44.171) 830 1007 Fax: (44.171) 830 1023 This publication is available on the following electronic and other media: Online databases CD-ROM Microfilm FT Profile (UK) Knight-Ridder Information World Microfilms Publications (UK) Tel: (44.171) 825 8000 Inc (USA) Tel: (44.171) 266 2202 DIALOG (USA) SilverPlatter (USA) University Microfilms Inc (USA) Tel: (1.415) 254 7000 Tel: (1.800) 521 0600 LEXIS-NEXIS (USA) Tel: (1.800) 227 4908 Copyright © 1996 The Economist Intelligence Unit Limited. -

I. the Economic Environment

Mali WT/TPR/S/43 Page 1 I. THE ECONOMIC ENVIRONMENT (1) MAJOR FEATURES OF THE ECONOMY 1. Mali is a landlocked country in West Africa which covers an area of 1,241,238 km2 and in 1997 had nearly ten million inhabitants. The capital, Bamako, has about one million inhabitants; the other cities, the largest of which are Ségou, Mopti, Sikasso and Gao, have fewer than 100,000 inhabitants. There is a sizeable drift away from the land, particularly to the capital: the proportion of the population living in cities rose from 14 per cent in 1970 to 27 per cent in 1995 (Table I.1). Illiteracy (69 per cent of the total population in 1995) and poor access to health care have helped to keep the infant mortality rate high (123% in 1995); average life expectancy at birth is 50 years. Table I.1 Basic social data, 1970-95 Indicators 1970 1990 1995 Population (millions) 5.3 8.1 9.0 Urban population (percentage) 14 24 27 Annual rate of population growth (percentage) .. 1.8 2.0 Infant mortality rate (children< 1 year) (per '000 live births) 204 166 123 Life expectancy at birth 38 48 50 Public spending on health (percentage of GDP) .. 0.6 0.5 Public spending on education (percentage of GDP) .. 2.4 2.2 Illiteracy (percentage of population) .. 68 69 - Men .. 59 61 - Women 76 77 Human development indicator (HDI ranking/total number of countries) .. 156/160 171/175 .. Not available. Source: World Bank, various publications; United Nations Development Programme, Human Development Report, several issues. -

The Big Reset

REVISED s EDITION Willem s Middelkoop s TWarh on Golde and the Financial Endgame BIGs s RsE$EAUPTs The Big Reset The Big Reset War on Gold and the Financial Endgame ‘Revised and substantially enlarged edition’ Willem Middelkoop AUP Cover design: Studio Ron van Roon, Amsterdam Photo author: Corbino Lay-out: Crius Group, Hulshout Amsterdam University Press English-language titles are distributed in the US and Canada by the University of Chicago Press. isbn 978 94 6298 027 3 e-isbn 978 90 4852 950 6 (pdf) e-isbn 978 90 4852 951 3 (ePub) nur 781 © Willem Middelkoop / Amsterdam University Press B.V., Amsterdam 2016 All rights reserved. Without limiting the rights under copyright reserved above, no part of this book may be reproduced, stored in or introduced into a retrieval system, or transmitted, in any form or by any means (electronic, mechanical, photocopying, recording or otherwise) without the written permission of both the copyright owner and the author of the book. To Moos and Misha In the absence of the gold standard, there is no way to protect savings from confiscation through inflation. There is no safe store of value. If there were, the government would have to make its holding illegal, as was done in the case of gold. If everyone decided, for example, to convert all his bank deposits to silver or copper or any other good, and thereafter declined to accept checks as payment for goods, bank deposits would lose their purchasing power and government-created bank credit would be worthless as a claim on goods. -

P Agricultural Sector Adjute ,1F2,- AV Association Villageois ( Deepiiprment L'ak) BAD Banque Africaine De D6vt1ue Pernent (,-4-Fzafn (Oitir2

PA AL' Fertilizer Policy Research Program for Tropical Africa The Policy Environment and Fertilizer Sector Development in Mali: An Assessment B. L. Bumb and J. F. Teboh International Fertilizer Development Center (IFDC) Muscle Shoals, Alabama U.SA and F. Mariko and M. Thiam Institut d'Economie Rurale (IER) Bamako, Mah December 1992 Table of Contents PaW Chapter 1-Introduction ............................................... 1 Chapter 2-The Macroeconomic Setting .................................. 14 Chapter 3-Role of Agriculture in the National Economy ..................... 54 Chapter 4-Fertilizer Sector Development ................................. 71 Chapter 5-The Policy Environment: An Analytical Framework ................ 120 Chapter 6-Evolution and Assessment of the Policy Environment in Mali ........ 140 Chapter 7-Summary and Conclusions ................................... 169 Acronyms aod Ab'ib -- na s ADB African Development Bak ARPON Amelioration de la RizicL.1'hrz Faysam.i dan1"Office, di. N'igeo ASAP Agricultural Sector AdjuTe ,1F2,- AV Association Villageois ( DeepiiprmEnt L'ak) BAD Banque Africaine de D6vt1ue pernent (,-4-fzafn (oitir2. B.an& ( BCEAO Banque Centrale des Etati , A i,"A ti & i"O.utest. West African States) l3B k Ndali) BDM Banque du Dveloppemrn4, di ,Va!j ( .,,(zt BIAO Banque Internationale p. , ,, ad, ,Deposit $,ik ,-Ajif BMCD Banque Malienne de Cro~iiX cc J. ff41'tS (1Iredlt (Naovai Auricui.ltur.ai BNDA Banque Nationale de DAvi.p, inr - Xgicti. Development Bank) B BOAD Banque Ouest Africaine du Dve&IppTme~nt (V: nzeii, yehlpme C mk CCCE Caisse Centrale de Coop6r.ion Ecor,,aiique CFDT Compagnie Franqaise poa, rt D6,vo~oppem,.iv,- 't det. U_,?ir ',2: 4W: ,Co,:r Textile Development Compn:y .,,I T-m4,c .