Corporate Social Responsibilityreport

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

An N U Al R Ep O R T 2018 Annual Report

ANNUAL REPORT 2018 ANNUAL REPORT The Annual Report in English is a translation of the French Document de référence provided for information purposes. This translation is qualified in its entirety by reference to the Document de référence. The Annual Report is available on the Company’s website www.vivendi.com II –— VIVENDI –— ANNUAL REPORT 2018 –— –— VIVENDI –— ANNUAL REPORT 2018 –— 01 Content QUESTIONS FOR YANNICK BOLLORÉ AND ARNAUD DE PUYFONTAINE 02 PROFILE OF THE GROUP — STRATEGY AND VALUE CREATION — BUSINESSES, FINANCIAL COMMUNICATION, TAX POLICY AND REGULATORY ENVIRONMENT — NON-FINANCIAL PERFORMANCE 04 1. Profile of the Group 06 1 2. Strategy and Value Creation 12 3. Businesses – Financial Communication – Tax Policy and Regulatory Environment 24 4. Non-financial Performance 48 RISK FACTORS — INTERNAL CONTROL AND RISK MANAGEMENT — COMPLIANCE POLICY 96 1. Risk Factors 98 2. Internal Control and Risk Management 102 2 3. Compliance Policy 108 CORPORATE GOVERNANCE OF VIVENDI — COMPENSATION OF CORPORATE OFFICERS OF VIVENDI — GENERAL INFORMATION ABOUT THE COMPANY 112 1. Corporate Governance of Vivendi 114 2. Compensation of Corporate Officers of Vivendi 150 3 3. General Information about the Company 184 FINANCIAL REPORT — STATUTORY AUDITORS’ REPORT ON THE CONSOLIDATED FINANCIAL STATEMENTS — CONSOLIDATED FINANCIAL STATEMENTS — STATUTORY AUDITORS’ REPORT ON THE FINANCIAL STATEMENTS — STATUTORY FINANCIAL STATEMENTS 196 Key Consolidated Financial Data for the last five years 198 4 I – 2018 Financial Report 199 II – Appendix to the Financial Report 222 III – Audited Consolidated Financial Statements for the year ended December 31, 2018 223 IV – 2018 Statutory Financial Statements 319 RECENT EVENTS — OUTLOOK 358 1. Recent Events 360 5 2. Outlook 361 RESPONSIBILITY FOR AUDITING THE FINANCIAL STATEMENTS 362 1. -

S O N a S I D R a P P O R T a N N U

SONASID Rapport Annuel 2 0 1 0 [Rapport Annuel 2010] { S ommaire} 04 MESSAGE DU DIRECTEUR GÉNÉRAL 06 HISTORIQUE 07 PROFIL 09 CARNET DE L’ACTIONNAIRE 10 GOUVERNANCE 15 STRATÉGIE 19 ACTIVITÉ 25 RAPPORT SOCIAL 31 ÉLÉMENTS FINANCIERS 3 [Rapport Annuel 2010] Chers actionnaires, L’année 2010 a été particulièrement difficile pour l’ensemble Sonasid devrait en effet profiter d’un marché international des entreprises sidérurgiques au Maroc qui ont subi de favorable qui augure de bonnes perspectives avec la plein fouet à la fois les fluctuations d’un marché international prudence nécessaire, eu égard des événements récents Message du perturbé et la baisse locale des mises en chantier dans imprévisibles (Japon, monde arabe), mais une tendance { l’immobilier et le BTP. Une situation qui a entraîné une qui se confirme également sur le marché local qui devrait réduction de la consommation nationale du rond-à-béton bénéficier dès le second semestre 2011 de la relance des Directeur General qui est passée de 1500 kt en 2009 à 1400 kt en 2010. chantiers d’infrastructures et d’habitat social. } Un recul aggravé par la hausse des prix des matières premières, la ferraille notamment qui a représenté 70% du Nous sommes donc optimistes pour 2011 et mettrons prix de revient du rond-à-béton. Les grands consommateurs en œuvre toutes les mesures nécessaires pour y parvenir. d’acier sont responsables de cette inflation, la Chine en Nous avons déjà en 2010 effectué des progrès notables au particulier, au détriment de notre marché qui, mondialisé, a niveau de nos coûts de transformations, efforts que nous été directement affecté. -

J Lo's Performance in Rabat Provokes Furore

22 June 12, 2015 Culture J Lo’s performance in Rabat provokes furore Saad Guerraoui said Aftati. Another PJD member, Khalid Rahmouni, expressed dis- gust at what he watched on 2M and Rabat called on Khalfi, as the one respon- sible for media policy, to resign. sexually charged per- However, PJD MP Abdeslam Bal- formance by pop diva laji told The Arab Weekly that Khalfi Jennifer Lopez at the does not have authority over public Mawazine music festival TV channels. in Rabat prompted mem- “It is the responsibility of the bersA of the ruling Islamist Justice High Authority of Audiovisual and Development Party (PJD) to call Communication (HACA) to investi- for the resignation of Communica- gate the matter following the min- tions Minister Mustapha el-Khalfi. ister’s request,” said Ballaji who Lopez, 45 and a popular Ameri- was the first MP from PJD’s parlia- can performer, opened the 14th mentary team to ask Khalfi for an Mawazine festival on May 30th, explanation for the concert. performing a nearly two-hour In a message posted on his Fa- long concert for a record crowd of cebook page, Khalfi, who is also 160,000 while millions watched on the government spokesman, an- state-owned television channel 2M. nounced that HACA and the ethics The glamorous New York-born committee of 2M would be inves- singer showcased scanty costumes tigated. Ballaji stressed that broad- and provocative poses as she casting the US singer’s suggestive donned seven different outfits, -in dance routine on a public TV chan- cluding a white leotard, during her nel was against Morocco’s constitu- performance, which was slammed tion, values and media ethics. -

CONSEIL D'administration DU 17 Mars 2021

CONSEIL D’ADMINISTRATION DU 17 Mars 2021 RAPPORT DU CONSEIL D’ADMINISTRATION SUR LES OPERATIONS DE L’EXERCICE 2020 A L’ASSEMBLEE GENERALE ORDINAIRE ANNUELLE Messieurs les Actionnaires, Nous vous avons réuni en Assemblée Générale Ordinaire Annuelle, conformément à la loi et à l’article 22 des statuts, pour entendre le rapport du Conseil d’Administration et celui des Commissaires aux Comptes sur l’exercice clos le 31 décembre 2020. Avant d’analyser l’activité de la Compagnie, nous voudrions vous rappeler brièvement l’environnement économique international et national dans lequel elle a évolué ainsi que le contexte du secteur des assurances. CONTEXTE A l’international Dans un contexte de crise inédit, l’économie mondiale a connu une sévère récession en 2020 (- 3,7% selon la Banque Mondiale), frappée de plein fouet par la pandémie du COVID-19. Confrontée à une grave crise sanitaire (plus de 28,6 millions de cas au 28/02/2021), l’économie américaine a perdu 3,6% en 2020, la pire récession depuis 1946, affectée par les effets de la pandémie. Après une forte remontée du PIB au 3ème trimestre 2020 (+33,1% en glissement annuel), la reprise s’est affaiblie au 4ème trimestre 2020 suite à la résurgence des infections au Coronavirus et la mise en place de nouvelles restrictions locales. Pour sa part, la croissance en Zone Euro accuse un repli historique de 6,8% en 2020 en raison de l’aggravation de la situation sanitaire et la multiplication des mesures de confinement dans la plupart des grandes économies de la Zone. Le recul le plus marqué est en Espagne (-11%) contre -8,8% pour l’Italie, -8,3% pour la France et -5% pour l’Allemagne. -

Morocco Market Brief

MOROCCO MARKET BRIEF www.renewablesnow.com 2 Wind & Solar project development in Morocco by 2020 “2,000 MW of wind power 2,000 MW of solar power Koudia Tanger II 150 MW by 2020” Tanger I Baida 140 MW 300 MW Khallada 120 MW Haouma Jbel Hdid 50 MW 200 MW Ain Beni Mathar Tarfaya Taza 300 MW Midelt Noor MII 150 MW Akhfenir 400 MW Tiskrad 200 MW Noor II Ouarzazate Midelt 300 MW 150-200 MW 100 MW Noor I Ouarzazate 500 MW Foum El Oued Noor III Ouarzazate 100-150 MW Boujdour Amougdoul 60 MW Sebkhat-Tah Boujdour 100 MW Laayoune 50 MW 2000 2001 MW of installed capacity MW of installed capacity 6600 4500 GWh of electricity generation GWh of electricity generation MAD 34.5 MAD 89.4 billion in investment billion in investment This report is available for download at www.renewablesnow.com/research 3 When it comes to clean energy projects in developing countries, Morocco stands out big time with a bold target of sourcing more than half of its electrical energy from renewable sources by 2030 and a firm plan to have 2,000 MW of wind and 2,000 MW of solar power plants by 2020. The North African kingdom, which hosted in Marrakesh COP 22, the UN climate change conference, already has a pretty detailed plan as to how it will transform the country’s energy mix. Noor Ouarzazate In February 2016, Morocco was all over the news with the official launch of the 160-MW first phase of its giant 580 MW Noor solar project near the trading city of Ouarzazate. -

Expat Guide to Casablanca

EXPAT GUIDE TO CASABLANCA SEPTEMBER 2020 SUMMARY INTRODUCTION TO THE KINGDOM OF MOROCCO 7 ENTRY, STAY AND RESIDENCE IN MOROCCO 13 LIVING IN CASABLANCA 19 CASABLANCA NEIGHBOURHOODS 20 RENTING YOUR PLACE 24 GENERAL SERVICES 25 PUBLIC TRANSPORTATION 26 STUDYING IN CASABLANCA 28 EXPAT COMMUNITIES 30 GROCERIES AND FOOD SUPPLIES 31 SHOPPING IN CASABLANCA 32 LEISURE AND WELL-BEING 34 AMUSEMENT PARKS 36 SPORT IN CASABLANCA 37 BEAUTY SALONS AND SPA 38 NIGHT LIFE, RESTAURANTS AND CAFÉS 39 ART, CINEMAS AND THATERS 40 MEDICAL TREATMENT 45 GENERAL MEDICAL NEEDS 46 MEDICAL EMERGENCY 46 PHARMACIES 46 DRIVING IN CASABLANCA 48 DRIVING LICENSE 48 CAR YOU BROUGHT FROM ABROAD 50 DRIVING LAW HIGHLIGHTS 51 CASABLANCA FINANCE CITY 53 WORKING IN CASABLANCA 59 LOCAL BANK ACCOUNTS 65 MOVING TO/WITHIN CASABLANCA 69 TRAVEL WITHIN MOROCCO 75 6 7 INTRODUCTION TO THE KINGDOM OF MOROCCO INTRODUCTION TO THE KINGDOM OF MOROCCO TO INTRODUCTION 8 9 THE KINGDOM MOROCCO Morocco is one of the oldest states in the world, dating back to the 8th RELIGION AND LANGUAGE century; The Arabs called Morocco Al-Maghreb because of its location in the Islam is the religion of the State with more than far west of the Arab world, in Africa; Al-Maghreb Al-Akssa means the Farthest 99% being Muslims. There are also Christian and west. Jewish minorities who are well integrated. Under The word “Morocco” derives from the Berber “Amerruk/Amurakuc” which is its constitution, Morocco guarantees freedom of the original name of “Marrakech”. Amerruk or Amurakuc means the land of relegion. God or sacred land in Berber. -

UNE RETROSPECTIVE 2014-A.Indd

Système de Management de la Qualité certifié ISO 9001 version 2008 par BUREAU VERITAS MAROC LE PREMIER QUOTIDIEN ECONOMIQUE DU MAROC Année marathon II RétRospective L’année où la diplomatie • Tournées royales d’envergure construite avec un montant de 330 mil- lions de DH. Les champs de partenariats ont également compris d’autres secteurs • Le capital immatériel fait son comme les finances, les énergies renou- velables, les infrastructures, le transport, entrée dans l’évaluation de la l’agroalimentaire, les mines, l’habitat… richesse du pays L’impact de cette tournée a été retentis- sant en termes de perception du Maroc dans le continent. En peu de temps, le • Appel à une rupture avec les Souverain a construit une image charis- matique en Afrique. La dynamique de la privilèges et l’économie de rente diplomatie royale a permis un plus grand au Sahara rapprochement avec certains Etats du Sahel, comme le Mali, qui n’étaient pas considérés traditionnellement comme des 2014 est décidément l’année bastions acquis au Maroc. Aujourd’hui, de la consécration de l’orientation afri- le renforcement du partenariat avec ces caine du Maroc. La tournée royale dans Etats se base sur une logique de com- la région, durant les premiers mois de plémentarité. Ces Etats ont demandé de cette année, a montré l’engagement du profiter de l’expertise marocaine dans Royaume en faveur du développement de plusieurs domaines, notamment dans la la coopération Sud-Sud. Le pays ne s’est promotion des ressources humaines, mais pas contenté des beaux discours, mais surtout dans l’encadrement religieux. -

RAPPORT-ANNUEL-ONCF-2016.Pdf

RAPPORT ANNUEL 2016 SA MAJESTÉ LE ROI MOHAMMED VI, QUE DIEU L’ASSISTE Sommaire 06 08 10 20 28 36 50 INTERVIEW COMITÉ DE L’ONCF EN LE TRANSPORT LE FRET ET DES GRANDS PROJETS LA SÉCURITÉ DU DIRECTEUR DIRECTION UN CLIN D’ŒIL DES PASSAGERS LA LOGISTIQUE D’INVESTISSEMENTS ET LA SÛRETÉ GÉNÉRAL Priorité au confort client Au plus près des enjeux Pour un réseau robuste Deux priorités absolues et à la qualité de service sectoriels des entreprises et moderne 58 64 72 80 88 94 LE CAPITAL HUMAIN LA GOUVERNANCE DÉVELOPPEMENT DURABLE UNE COMMUNICATION LA COOPÉRATION SITUATION FINANCIÈRE Un engagement Un système en amélioration Tous contre le réchauffement Innovante et durable FERROVIAIRE À L’INTERNATIONAL Performances globales permanent et des continue climatique Amplification du partenariat Sud‑Sud compétences Quid du projet de la ligne à grande vitesse Si vous ne deviez retenir qu’une seule Tanger‑Casablanca ? chose de l’année 2016 ? Grâce à une forte mobilisation, soutenue par les différentes Les initiatives menées sont certes multiples et ne peuvent parties prenantes, et à un système de gouvernance que nous conforter dans nos choix stratégiques. Mais approprié, ce méga projet est aujourd’hui en phase de si je dois me contenter de citer les événements phares préparation de l’exploitation. Ce projet, dont le coup ayant caractérisé cette année, je citerai le lancement d’envoi officiel des travaux a été donné par Sa Majesté par Sa Majesté Le Roi Mohammed VI, Que Dieu L’Assiste, Le Roi Mohammed VI, Que Dieu L’Assiste, a franchi des du projet de construction de la gare LGV de Rabat paliers importants dans sa réalisation, enregistrant à fin Agdal et notre participation à la COP 22 notamment Interview du 2016 un taux d’avancement global de 86 %. -

2014 Annual Report

2014 ANNUAL REPORT 0 1 9 4 - 2 0 1 years 4 2014 ANNUAL REPORT 0 1 9 4 - 2 0 1 years 4 This is a particularly important year for Attijariwafa bank as we complete our one hundred and tenth year. We are therefore celebrating more than a century of providing banking and banking- related activities in the interests of our country’s economic and industrial development and the well- being of our fellow citizens. M. Mohamed El Kettani Président Directeur Général Chairman and CEO’S Message ANNUAL REPORT ATTIJARIWAFA BANK 2014 Our Group’s history is inextricably intertwined with With the legacy of two century-old banks, that of the Kingdom of Morocco. Not only does that Attijariwafa bank has constantly sought to diversify make us proud, it constantly inspires us to scale even its business lines to provide its corporate customers greater heights. Attijariwafa bank’s history began when with the most sophisticated payment methods two French banks, Compagnie Algérienne de Crédit and financing products to satisfy their constantly et de Banque (CACB) and Banque Transatlantique, evolving requirements. Our Group is also committed to opened branches in Tangier in 1904 and 1911 meeting the needs of all our fellow citizens, whatever respectively. their socio-economic background. For this reason, In the aftermath of the independence, Banque Attijariwafa bank was the first bank to make the Transatlantique became Banque Commerciale financial inclusion of low-income households one du Maroc (BCM) and, in 1987, emerged as the of its strategic priorities. Attijariwafa bank is proud of Kingdom’s leading private sector bank. -

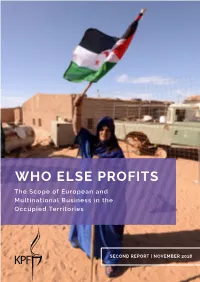

Who Else Profits the Scope of European and Multinational Business in the Occupied Territories

WHO ELSE PROFITS The Scope of European and Multinational Business in the Occupied Territories SECOND RepORT | NOVEMBER 2018 A Saharawi woman waving a Polisario-Saharawi flag at the Smara Saharawi refugee camp, near Western Sahara’s border. Photo credit: FAROUK BATICHE/AFP/Getty Images WHO ELse PROFIts The Scope of European and Multinational Business in the Occupied Territories This report is based on publicly available information, from news media, NGOs, national governments and corporate statements. Though we have taken efforts to verify the accuracy of the information, we are not responsible for, and cannot vouch, for the accuracy of the sources cited here. Nothing in this report should be construed as expressing a legal opinion about the actions of any company. Nor should it be construed as endorsing or opposing any of the corporate activities discussed herein. ISBN 978-965-7674-58-1 CONTENTS INTRODUCTION 2 WORLD MAp 7 WesteRN SAHARA 9 The Coca-Cola Company 13 Norges Bank 15 Priceline Group 18 TripAdvisor 19 Thyssenkrupp 21 Enel Group 23 INWI 25 Zain Group 26 Caterpillar 27 Biwater 28 Binter 29 Bombardier 31 Jacobs Engineering Group Inc. 33 Western Union 35 Transavia Airlines C.V. 37 Atlas Copco 39 Royal Dutch Shell 40 Italgen 41 Gamesa Corporación Tecnológica 43 NAgoRNO-KARABAKH 45 Caterpillar 48 Airbnb 49 FLSmidth 50 AraratBank 51 Ameriabank 53 ArmSwissBank CJSC 55 Artsakh HEK 57 Ardshinbank 58 Tashir Group 59 NoRTHERN CYPRUs 61 Priceline Group 65 Zurich Insurance 66 Danske Bank 67 TNT Express 68 Ford Motor Company 69 BNP Paribas SA 70 Adana Çimento 72 RE/MAX 73 Telia Company 75 Robert Bosch GmbH 77 INTRODUCTION INTRODUCTION On March 24, 2016, the UN General Assembly Human Rights Council (UNHRC), at its 31st session, adopted resolution 31/36, which instructed the High Commissioner for human rights to prepare a “database” of certain business enterprises1. -

2009 MENA-OECD Ministerial Conference Registered Participants

2009 MENA-OECD Ministerial Conference Registered Participants Representing Algérie Mr. Abderrahmane ABEDOU Directeur de Recherche CREAD Ministère de l’enseignement supérieur et de la recherché scientifique (Algérie) Allemagne H.E. Dr. Ulf-Dieter KLEMM Ambassador German Embassy in Morocco Mr. MARCO WIEDEMANN Directeur Général Chambre Allemande Mr. Peter JUNGEN President European Enterprise Institute Arabie Saoudite H.E. Dr. Hamad S. AL-BAZAI Vice Minister of Finance Ministry of Finance Dr. KARAOUI First Secretary Embassy of Saudi Arabia to Morocco Australie H.E. Mr. Christopher LANGMAN Ambassador, Permanent Representative of Delegation of Australia to the Australia to the OECD OECD 03 December 2009 Page 1 sur 100 Representing Autorité Palestinienne H.E. Dr. Ali JARBAWI Minister of Planning and Administrative Ministry of Planning and Development Administrative Development Mr. Jafar HDAIB Director general, Palestine Investment Palestine Investment Promotion Agency Promotion Agency Mr. Baha’ BAKRI Special Advisor to the Minister Ministry of Planning and Administrative Development Mr. John KHOURY Director European Palestinian Credit Guarantee Fund Mr. Mahmoud SHAHEEN Deputy Head General Personnel Council Dr. Khaled Raji ZEIDAN Governance Policy Advisor Ministry of Planning and Ministry of Planning and Administrative Development 03 December 2009 Page 2 sur 100 Representing Bahreïn H.E. Sheikh Mohammed bin Essa AL KHALIFA Chief Executive, Economic Development Economic Development Board Board Mrs. Waheeda AL DOY Director MENA Centre for Investment Mrs. Muneera AL KHALIFA Director of Elections and Referendom - Ministry of Justice and Islamic Acting Director of Cases Affairs Mr. Mohammed ALSHOMALI Lawyer Mr. Abdulla BAQER Head of Primary Sector Development Ministry of Health (Fisheries) Mr. Rashid A.R ISHAQ Advisor, Good Governance Civil Service Bureau Miss Hana KANOO Senior Economist MENA Centre for Investment Mrs. -

Corporate Social Responsibility Report 2012

2012 Corporate Social Responsibility Report 2012 Corporate Social Responsibility Report GOVERNANCE, p.12 COMPLIANCE, « Our Group has for over a century been SAFETY conducting banking business with commitment AND QUALITY : and responsibility. » THE FOUNDATIONS OF TRUST Mohamed EL Kettani, Chairman and Chief Executive Officer p.22 SUMMARY SUPPORTING Convinced that one of the major roles of a financial This report broadly outlines Attijariwafa bank’s vision institution is to facilitate and accelerate economic and actions regarding sustainable development. EMPLOYEE and social development, at Attijariwafa bank, Despite this being the 2012 edition of the CSR Report, DEVELOPMENT sustainable development is an issue that we take corporate social responsibility has underpinned the very seriously, backed by strong ethical values, activities of the entire Group for many years. The report commitment, leadership, solidarity and citizenship. summarises the sustainable development challenges facing Attijariwafa bank as well as the initiatives undertaken to date in respect of quality, compliance As a supporter of government and professional ethics programmes, financier of the real in order to establish p.34 CONTRIBUTING TO economy, investor and partner to « Attijariwafa bank’s approach to Corporate a relationship of trust MOROCCAN CIVIL large, medium and small enterprises, Social Responsibility (CSR) is a state of with all stakeholders. our Group has for over a century mind, a collective consciousness, which It also shows how the SOCIETY been conducting banking business goes far beyond a simple set of managerial Group is committed with commitment and responsibility. responsibilities. in its daily actions to BY PROMOTING EDUCATION, » Such responsibility lies in our acting as a responsible ART AND CULTURE ability to help Moroccan society employer.