Appendix C Aviation Activity Forecast

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Final Supplement to the Final Environmental Impact Statement

GNOSS FIELD AIRPORT SUPPLEMENT TO THE FINAL ENVIRONMENTAL IMPACT STATEMENT FINAL CHAPTER ONE BACKGROUND This document is the Final Supplement to the Final Environmental Impact Statement (SEIS), prepared in support of the Federal actions related to the proposed runway and parallel taxiway extension at Gnoss Field Airport (DVO or Airport). This Final SEIS updates the previous National Environmental Policy Act of 1969 (NEPA) analyses to address changes in the forecasted aviation activity and the critical aircraft at DVO and adds an additional alternative for environmental impact evaluation. The SEIS has been prepared pursuant to the NEPA and its implementing regulations found at Title 40, Code of Federal Regulations (CFR) §§ 1500-1508. The Federal Aviation Administration (FAA) published a Final Environmental Impact Statement (EIS) in June 2014 in support of the Federal actions related to the proposed runway and parallel taxiway extension at DVO. During the preparation of the response to comments on the June 2014 Final EIS, the FAA informally reviewed aviation operations activity from the FAA Traffic Flow Management System Counts (TMFSC) database associated with aviation activity at DVO. After that evaluation, the FAA concluded that existing conditions regarding the aviation activity at DVO may have changed from those described in the June 2014 Final EIS.1 Therefore, a formal analysis was required to verify the current aviation activity level and critical aircraft for DVO. That formal analysis was contained in an April 2016 Purpose and Need Working Paper, which was circulated for public review and comment. The April 2016 Purpose and Need Working Paper identified that the critical aircraft classification and associated runway length requirement at DVO had changed from what was described in the June 2014 Final EIS. -

Inventory of Existing Conditions

Buchanan Field Airport Master Planning Program Field A. INVENTORY OF EXISTING CONDITIONS Buchanan A > Inventory of Existing Conditions INTRODUCTION. Buchanan Field Airport (CCR) is the major general aviation reliever airport serving Contra Costa County and multiple communities located in the northeastern portion of the greater San Francisco Bay Area (see Figure A1). The Airport has been a catalyst for business growth in the region and has served as an anchor for the local employment base, as well as meeting the aviation transportation needs. Situated in an unincorporated portion of Contra Costa County, directly adjacent to the thriving urban heartbeat of the City of Concord, Buchanan Field Airport is a vital component of the transportation infrastructure serving the region for tourism and business. Buchanan Field Airport is well equipped to serve regional demand related to general aviation and business aviation needs. The Airport has a reputation as being an excellent aviation facility that offers a safe and efficient operational environment. The Bay Area continues to experience significant increases in business activity, commercial and residential growth, and economic development. Because of this, Buchanan Field Airport is also being presented with increasing operational and facility demands. Many of the areas surrounding the Airport, with many high quality homes and environmental amenities, have experienced significant residential development, resulting in homeowner concerns about the effect that the Airport may have on their lifestyle. Some of these homes and facilities are located within a two to three mile radius of the Airport. Thus, the Airport may influence the social, economic, and physical environments of the area in which it operates. -

CACAP 0506.Pmd

Spring 2006 The Official Magazine of California Wing Civil Air Patrol Dark Passages California’s Most Perilous Air Routes 10 Tips for Surviving Plus: • Rough Air Over Riverside Summer Encampment • Altoids-Can Engineering Puts CAWG Cadets Speak Out of School DFing in a Shirt Pocket Into the Mystic Slipstream • Cessna 182Ts Land in NorCal The Late Col. Don Towse Let His Soul and Spirit Fly— • Handling Electrified And Left Us a Lovely Memoir Emergencies EAGLE EYE 2 Dark Passages Flying California’s Most Perilous Air Routes COLUMNS Commander’s Comments 11 Eagle Call is an authorized publication serving the Bird’s Eye View 15 interests of the California Wing of the United States Air Force Auxiliary Civil Air Patrol. It is published by a private firm in no way connected with the FIELD MANUAL 17 Department of the Air Force or with the Civil Air Breathtaking Ingenuity Patrol Corporation. The appearance of advertisements You’ll Never Look at Your Altoids in this publication, including supplements and inserts, Tin the Same Way Again does not constitute an endorsement by the U.S. Air Force or CAP of the products and services advertised ES101 23 herein. Scorch this Hot Quiz for a Cool Summer Eagle Call encourages contributions from all CAP members, military personnel, and related agencies. THE CADET COSMOS 27 Material must be original, free of copyright constraint, unpublished, and submitted only to Eagle 10 Tips for Surviving Encampment Call, which reserves the right to approve, reject, edit, abridge or expand any submission. Features should be discussed in advance with the Editor, Capt. -

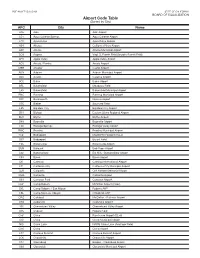

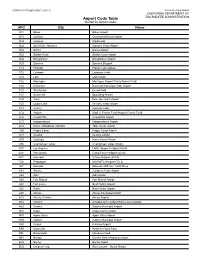

Airport Code Table (Sorted by City)

BOE-810-FTI (S1) (5-10) STATE OF CALIFORNIA BOARD OF EQUALIZATION Airport Code Table (Sorted by City) APC City Name A26 Adin Adin Airport L54 Agua Caliente Springs Agua Caliente Airport L70 Agua Dulce Agua Dulce Airpark A24 Alturas California Pines Airport AAT Alturas Alturas Municipal Airport 2O3 Angwin Virgil O. Parrett Field (Angwin-Parrett Field) APV Apple Valley Apple Valley Airport ACV Arcata / Eureka Arcata Airport MER Atwater Castle Airport AUN Auburn Auburn Municipal Airport AVX Avalon Catalina Airport 0O2 Baker Baker Airport BFL Bakersfield Meadows Field L45 Bakersfield Bakersfield Municipal Airport BNG Banning Banning Municipal Airport O02 Beckwourth Nervino Airport O55 Bieber Southard Field L35 Big Bear City Big Bear City Airport BIH Bishop Eastern Sierra Regional Airport BLH Blythe Blythe Airport D83 Boonville Boonville Airport L08 Borrego Springs Borrego Valley Airport BWC Brawley Brawley Municipal Airport 7C4* Bridgeport MCMWTC Heliport (7CL4) O57 Bridgeport Bryant Field F25 Brownsville Brownsville Airport BUR Burbank Bob Hope Airport L62 Buttonwillow Elk Hills - Buttonwillow Airport C83 Byron Byron Airport CXL Calexico Calexico International Airport L71 California City California City Municipal Airport CLR Calipatria Cliff Hatfield Memorial Airport CMA Camarillo Camarillo Airport O61 Cameron Park Cameron Airpark C62* Camp Roberts McMillan Airport (CA62) SYL Camp Roberts / San Miguel Roberts AHP CSL Camp San Luis Obispo O’Sullivan AHP CRQ Carlsbad McClellan - Palomar Airport O59 Cedarville Cedarville Airport 49X Chemehuevi -

Air Transportation Element

Sonoma County General Plan 2020 AIR TRANSPORTATION ELEMENT Sonoma County Permit and Resource Management Department 2550 Ventura Avenue Santa Rosa, CA 95403 Adopted by Resolution No. 08-0808 of the Sonoma County Board of Supervisors September 23, 2008 Draft Revision July 2011 AIR TRANSPORTATION ELEMENT TABLE OF CONTENTS 1. INTRODUCTION ................................................................................................................................................ 1 1.1 PURPOSE AND AUTHORITY .................................................................................................................. 1 1.2 RELATIONSHIP TO OTHER ELEMENTS ............................................................................................... 1 1.3 ORGANIZATION ....................................................................................................................................... 2 2. BACKGROUND .................................................................................................................................................. 3 2.1 HISTORICAL OVERVIEW ........................................................................................................................ 3 2.2 EXISTING AIRPORTS AND SERVICE LEVELS .................................................................................... 3 2.3 INSTITUTIONAL ROLES .......................................................................................................................... 3 3. AIR TRANSPORTATION DEMAND AND THE COUNTY AIRPORT SYSTEM -

Acronyms and Glossary

GNOSS FIELD AIRPORT SUPPLEMENT TO THE FINAL ENVIRONMENTAL IMPACT STATEMENT FINAL ACRONYMS The following is a list of acronyms used in this SEIS. 069 Petaluma Municipal Airport 0Q3 Sonoma Valley Airport 0Q9 Sonoma Skypark 3D Three-Dimensional AAAE American Association of Airport Executives AANG Arizona Air National Guard AC Advisory Circular ACCRI Aviation Climate Change Research Initiative ACHP Advisory Council on Historic Preservation ACIP Airports Capital Improvement Program ACM Asbestos Containing Material AEDT Aviation Environmental Design Tools AEM Area Equivalent Method AGL Above Ground Level AIM Aeronautical Information Management AIP Airport Improvement Program ALP Airport Layout Plan ANCA Airport Noise and Capacity Act of 1990 APC Napa County Airport APE Area of Potential Effect APU Auxiliary Power Unit AQCR Air Quality Control Region ARDF Airport Research and Development Foundation ARFF Aircraft Rescue and Fire Fighting ART Adapting to Rising Tides ASA Airport Service Area ASCE American Society of Civil Engineers ASNA Aviation Safety and Noise Abatement Act AST Aboveground Storage Tank ATC Air Traffic Control ATCM Asbestos Airborne Toxic Control Measure Plan ATCT Airport Traffic Control Tower AvGas Low-lead aviation gasoline BAAQMD Bay Area Air Quality Management District BAT Best Available Technology Economically Achievable BCA Benefit Cost Analysis BCDC San Francisco Bay Conservation and Development Commission BCFE Billion Cubic Feet BCT Best Conventional Pollutant Control Technology BFC-IP Bayfront Conservation – Industrial -

Sonoma Creek Baylands Strategy Final Report – May 2020

Sonoma Creek Baylands Strategy Final Report – May 2020 Sonoma Creek Baylands Strategy 1 May 2020 Acknowledgements Project Team Kendall Webster, Sonoma Land Trust Julian Meisler, Sonoma Land Trust Wendy Eliot, Sonoma Land Trust Jeremy Lowe, San Francisco Estuary Institute Ellen Plane, San Francisco Estuary Institute Scott Dusterhoff, San Francisco Estuary Institute Sam Veloz, Point Blue Conservation Science Michelle Orr, ESA James Gregory, ESA Stephanie Bishop, ESA Renee Spenst, Ducks Unlimited Steve Carroll, Ducks Unlimited Anne Morkill, U.S. Fish and Wildlife Service Meg Marriott, U.S. Fish and Wildlife Service Melissa Amato, U.S. Fish and Wildlife Service Science Advisory Panel Susan Haydon, Sonoma Water Carlos Diaz, Sonoma Water Larry Wyckoff, California Department of Fish and Wildlife Karen Taylor, California Department of Fish and Wildlife Jessica Davenport, San Francisco Bay Restoration Authority Peter Baye Stuart Seigel, San Francisco Bay National Estuarine Research Reserve Joy Albertson, U.S. Fish and Wildlife Service John Klochak, U.S. Fish and Wildlife Service Jessica Pollitz, Sonoma Resource Conservation District Laurel Collins, Watershed Sciences Steve Lee, Sonoma Ecology Center Funded By San Francisco Bay Restoration Authority U.S. Fish and Wildlife Service Resources Legacy Fund Dolby Family Fund Sonoma Creek Baylands Strategy 2 May 2020 Table of Contents Chapter 1 .......................................................................................................................................................7 Introduction -

![Acronyms and Glossary of Terms[PDF]](https://docslib.b-cdn.net/cover/6104/acronyms-and-glossary-of-terms-pdf-4866104.webp)

Acronyms and Glossary of Terms[PDF]

GNOSS FIELD AIRPORT ENVIRONMENTAL IMPACT STATEMENT FINAL ACRONYMS The following is a list of acronyms used in this EIS. 069 Petaluma Municipal Airport 0Q3 Sonoma Valley Airport 3D Three-Dimensional AC Advisory Circular ACHP Advisory Council on Historic Preservation AGL Above Ground Level AIM Aeronautical Information Management AIP Airport Improvement Program ALP Airport Layout Plan ANCA Airport Noise and Capacity Act of 1990 APC Napa County Airport APE Area of Potential Effect APU Auxiliary Power Unit AQCR Air Quality Control Region ARDF Airport Research and Development Foundation ARFF Aircraft Rescue and Fire Fighting ASA Airport Service Area ASCE American Society of Civil Engineers ASNA Aviation Safety and Noise Abatement Act AST Aboveground Storage Tank ATC Air Traffic Control ATCT Airport Traffic Control Tower AvGas Low-lead aviation gasoline BAAQMD Bay Area Air Quality Management District BAT Best Available Technology Economically Achievable BCDC San Francisco Bay Conservation and Development Commission BCT Best Conventional Pollutant Control Technology BMPs Best Management Practices BOD Biochemical Oxygen Demand BTU British Thermal Units BUSTR The Bureau of Underground Storage Tanks Regulations CAA Clean Air Act CAAQS California Ambient Air Quality Standards Caltrans California Department of Transportation CCR California Code of Regulations CDFG California Department of Fish and Game - as of January 1, 2013 the California Department of Fish and Game changed its name to the California Department of Fish and Wildlife (CDFW). For consistency -

Regional Airport System Plan

Regional Airport System Plan General Aviation Element Final Report Regional Airport Planning Committee June 2003 REGIONAL AIRPORT SYSTEM PLAN GENERAL AVIATION ELEMENT FINAL REPORT Prepared for the Regional Airport Planning Committee of ABAG, BCDC, MTC The preparation of this report has been financed in part by grants from the Federal Aviation Administration, U.S. Department of Transportation. The contents of this report do not necessarily reflect the official views or policy of the U.S. Department of Transportation. Prepared by ARIES CONSULTANTS LTD. Morgan Hill, California June 2003 TABLE OF CONTENTS Chapter Page PART 1. REGIONAL INTERESTS AND PLAN RECOMMENDATIONS 1 OVERVIEW ................................................................................................. 1-1 1.1 Introduction......................................................................................... 1-1 1.2 What is General Aviation.................................................................... 1-4 1.3 Observations ....................................................................................... 1-4 1.4 Defining a Regional Interest ............................................................... 1-6 1.5 Recommendations............................................................................... 1-7 2 GENERAL AVIATION TRENDS AND ISSUES ..................................... 2-1 2.1 Introduction......................................................................................... 2-1 2.2 Airport System Requirements............................................................ -

![Appendix C-1: Aviation Activity Forecast[PDF]](https://docslib.b-cdn.net/cover/9217/appendix-c-1-aviation-activity-forecast-pdf-6179217.webp)

Appendix C-1: Aviation Activity Forecast[PDF]

GNOSS FIELD AIRPORT SUPPLEMENT TO THE FINAL ENVIRONMENTAL IMPACT STATEMENT FINAL APPENDIX C-1 AVIATION ACTIVITY FORECAST This appendix includes the forecast of aviation activity for Gnoss Field Airport that was prepared for the Updated Purpose and Need Working Paper. The FAA approved this aviation forecast in February 2018 with the publication of the Updated Purpose and Need Working Paper. Landrum & Brown Appendix C-1 – Aviation Activity Forecast January 2020 Page C-1 - 1 GNOSS FIELD AIRPORT SUPPLEMENT TO THE FINAL ENVIRONMENTAL IMPACT STATEMENT FINAL THIS PAGE INTENTIONALLY LEFT BLANK Landrum & Brown Appendix C-1 – Aviation Activity Forecast January 2020 Page C-1 - 2 APPENDIX C-1 AVIATION ACTIVITY FORECAST GNOSS FIELD AIRPORT Prepared By: Landrum & Brown February 2018 Page C-1 - 3 GNOSS FIELD AIRPORT AVIATION ACTIVITY FORECAST FINAL TABLE OF CONTENTS PAGE 1.0 Purpose and Context ......................................................................... 1 2.0 General Aviation Forecast Information ................................................. 2 2.1 Prior Forecasts ................................................................................. 3 2.1.1 1989 Airport Master Plan ................................................................... 3 3.0 Catchment Area ............................................................................... 4 4.0 Historical National and Local Trends .................................................... 4 4.1 National and Local Economy ............................................................... 4 -

PRINT and E-MEDIA Opportunity Guide 12 AAAE DELIVERS for AIRPORT EXECUTIVES Editorial Mission

PRINT AND E-MEDIA opportunity guide 12 AAAE DELIVERS FOR AIRPORT EXECUTIVES Editorial Mission To Our Aviation Industry Friends: or more than 20 years, Airport Magazine has offered our airport and Fcorporate readers editorial content that provides “how-to” information for their long-range and short-term planning. This remains our mission. We offer operational and management articles written by industry leaders who share their knowledge base with the rest of the airport community. Feature articles for 2012 will highlight technology, security, aircraft rescue fire fighting/airfield safety, concessions, architecture/engineering, and so much more. Our editorial coverage is greatly assisted by the help of the magazine’s editorial advisory board-a panel of 17 airport and aviation industry corporate officials who lend their knowledge and time to ensure that Airport Magazine provides what our readers want and need. Our plans for 2012 would not be possible, however, without the many advertisers who help to support our magazine. Companies that market to the airport community entrust Airport Magazine to deliver their message directly to the buyers, and with each issue we strive to earn that trust anew. All of us at Airport Magazine look forward to working with you in 2012. May it be a prosperous year for all of you. Sincerely, Barbara Cook Editor [email protected] Reach Decision-Makers Our readers are the people who make the decisions and sign the checks 23,000 Airport or more than 23 years, Airport Magazine has been the publication of choice for airport Professionals executives from around the world. Over those 23 years we’ve built a loyal and dedicated Freadership based on trusted and valued editorial. -

CDTFA-810-FTH Airport Code Table

CDTFA-810-FTH (S1F) REV. 1 (10-17) STATE OF CALIFORNIA CALIFORNIA DEPARTMENT OF Airport Code Table TAX AND FEE ADMINISTRATION (Sorted by Airport Code) APC City Name 0O2 Baker Baker Airport 0O4 Corning Corning Municipal Airport 0O9 Gasquet Ward Field 0Q3 Schellville / Sonoma Sonoma Valley Airport 0Q4 Selma Selma Airport 0Q5 Shelter Cove Shelter Cove Airport 0Q6 Shingletown Shingletown Airport 0Q9 Sonoma Sonoma Skypark 1C9 Hollister Frazier Lake Airpark 1O2 Lakeport Lampson Field 1O3 Lodi Lodi Airport 1O5 Montague Montague Airport (Yreka Rohrer Field) 1O6 Dunsmuir Dunsmuir Municipal-Mott Airport 1Q1 Strathmore Eckert Field 1Q2 Susanville Spaulding Airport 1Q4 Tracy New Jerusalem Airport 1Q5 Upper Lake Gravelly Valley Airport 2O1 Quincy Gansner Field 2O3 Angwin Virgil O. Parrett Field (Angwin-Parrett Field) 2O6 Chowchilla Chowchilla Airport 2O7 Independence Independence Airport 2Q3 Davis / Woodland / Winters Yolo County Airport 36S Happy Camp Happy Camp Airport 3O1 Gustine Gustine Airport 3O8 Coalinga Harris Ranch Airport 49X Chemehuevi Valley Chemehuevi Valley Airport 4C0* Los Angeles LAPD Hooper Heliport (4CA0) 4C3* Pleasanton Camp Parks Heliport (4CA3) 60C* Concord Q Area Heliport (60CA) 7C4* Bridgeport MCMWTC Heliport (7CL4) 9L2 Edwards Edwards AFB Aux. North Base A24 Alturas California Pines Airport A26 Adin Adin Airport A28 Fort Bidwell Fort Bidwell Airport A30 Fort Jones Scott Valley Airport A32 Dorris Butte Valley Airport AAT Alturas Alturas Municipal Airport ACV Arcata / Eureka Arcata Airport AHC Herlong Amedee Army Airfield (Sierra Army Depot) AJO Corona Corona Municipal Airport APC Napa Napa County Airport APV Apple Valley Apple Valley Airport AUN Auburn Auburn Municipal Airport AVX Avalon Catalina Airport BAB Marysville Beale Air Force Base BFL Bakersfield Meadows Field BIH Bishop Eastern Sierra Regional Airport BLH Blythe Blythe Airport BLU Emigrant Gap Blue Canyon - Nyack Airport CDTFA-810-FTH (S1B) REV.