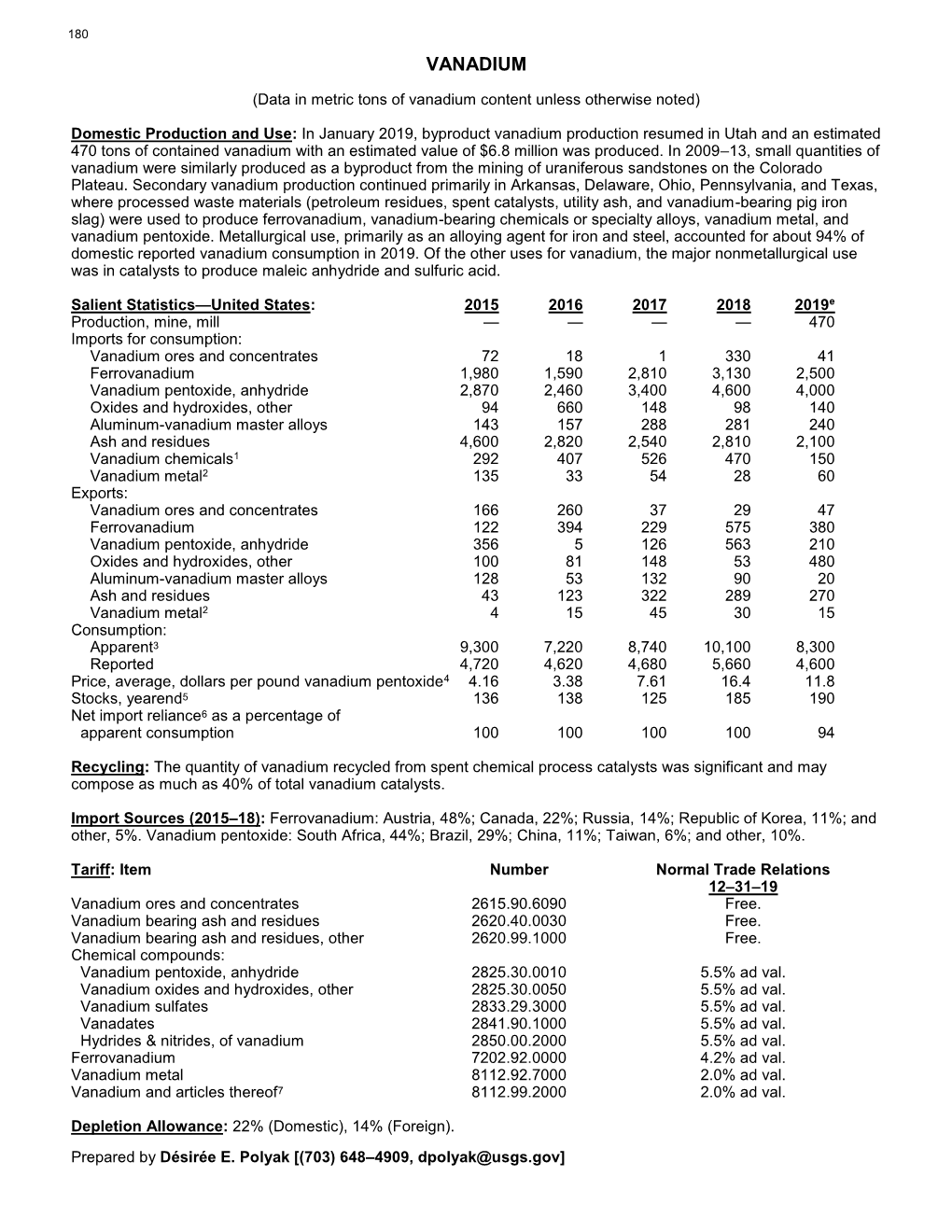

Vanadium Data Sheet

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vanadium Pentoxide and Other Inorganic Vanadium Compounds

This report contains the collective views of an international group of experts and does not necessarily represent the decisions or the stated policy of the United Nations Environment Programme, the International Labour Organization, or the World Health Organization. Concise International Chemical Assessment Document 29 VANADIUM PENTOXIDE AND OTHER INORGANIC VANADIUM COMPOUNDS Note that the layout and pagination of this pdf file are not identical to the printed CICAD First draft prepared by Dr M. Costigan and Mr R. Cary, Health and Safety Executive, Liverpool, United Kingdom, and Dr S. Dobson, Centre for Ecology and Hydrology, Huntingdon, United Kingdom Published under the joint sponsorship of the United Nations Environment Programme, the International Labour Organization, and the World Health Organization, and produced within the framework of the Inter-Organization Programme for the Sound Management of Chemicals. World Health Organization Geneva, 2001 The International Programme on Chemical Safety (IPCS), established in 1980, is a joint venture of the United Nations Environment Programme (UNEP), the International Labour Organization (ILO), and the World Health Organization (WHO). The overall objectives of the IPCS are to establish the scientific basis for assessment of the risk to human health and the environment from exposure to chemicals, through international peer review processes, as a prerequisite for the promotion of chemical safety, and to provide technical assistance in strengthening national capacities for the sound management -

US Schedule for Internet V2

Draft as of March 23, 2007 Subject to legal review for accuracy, clarity and consistency. Annex 3.3 - - Industrial/Textile Schedule for the United States Tariff Elimination US 8 digit Description MFN RATE Schedule 03011000 Live ornamental fish Free I 03019100 Live trout Free I 03019200 Live eels Free I 03019300 Live carp Free I 03019900 Live fish, other than trout, eel, carp or ornamental fish Free I 03021100 Trout, fresh or chilled, excluding fillets, other meat portions, livers and roes Free I Pacific, Atlantic and Danube salmon, fresh or chilled, excluding fillets, other 03021200 meat portions, livers and roes Free I Salmonidae other than trout or Pacific, Atlantic & Danube salmon, fresh or 03021900 chilled, excluding fillets, other meat portions, livers & roes Free I Halibut and Greenland turbot, fresh or chilled, excluding fillets, other meat 03022100 portions, livers and roes Free I 03022200 Plaice, fresh or chilled, excluding fillets, other meat portions, livers and roes Free I 03022300 Sole, fresh or chilled, excluding fillets, other meat portions, livers and roes 1.1 cents/kg A Flat fish, nesi, fresh or chilled, excluding fillets, other meat portions, livers 03022900 and roes Free I Albacore or longfinned tunas, fresh or chilled, excluding fillets, other meat 03023100 portions, livers and roes Free I Yellowfin tunas, fresh or chilled, excluding fillets, other meat portions, livers 03023200 and roes Free I Skipjack or stripe-bellied bonito, fresh or chilled, excluding fillets, other meat 03023300 portions, livers and roes Free -

Ferro Vanadium Production Business. Ferrovanadium Market Is Expected to Expand at a CAGR of 5.0% Between 2018 and 2028

www.entrepreneurindia.co Introduction Ferro Vanadium is an alloy which is formed by combining iron and vanadium with a vanadium content range of 35%-85%. Ferro Vanadium is a universal hardener, strengthener and anti-corrosive additive for steels like high-strength low-alloy (HSLA) steel, tool steels, as well as other ferrous-based products. Ferro vanadium belongs to the category of ferroalloy. Ferro vanadium is an alloy which is formed by combining iron and vanadium. Ferrovanadium contains 35% to 85% of vanadium depending on applications of the product in end-use industry. Ferro vanadium is an alloy material that is used in manufacturing of steel. It imparts desirable properties such as abrasion resistance, high temperature and hardenability. www.entrepreneurindia.co Ferro vanadium used for manufacturing of steel offers the end product with high stability against alkalis as well as acids such as sulphuric and hydrochloric acids. In addition, products containing ferro vanadium are at reduced risk to be susceptible to corrosion. Ferro vanadium also helps in reducing the overall weight of the material as well as increasing the overall tensile strength of the end product. In addition, it helps in promoting fine grain size and increasing hardenability through precipitation of nitrides and carbides. Ferro vanadium is manufactured using an electric arc furnace in which scrap iron is melted initially and then it is combined with the mixture of aluminum as well as flux such as calcium fluoride and calcium oxide. It is usually supplied in pallet boxes or in shrink wrapped in super bags. www.entrepreneurindia.co Ferro Vanadium is produced from Vanadium Sludge & usually available in the range with V: 50-85%. -

The Determination of Vanadium and Chromium in Ferrovanadium by Electrometric Titration' by G

Oct., 1921 THE JOURNAL OF INDUSTRIAL AND ENGINEERING CHEMISTRY 939 CONCLUSIONS Modifications in bleaching methods give promise of greater The chemical characteristics of soda and sulfate pulps result,s than modifying cooking methods. indicate that they are a very pure form of wood cellulose and Modifications in which the bleaching operation was divided capable of high yields of white fibrous and resistant material. into two steps, with washing between steps, cut the bleach The sulfate process is much more efficient than the soda requirement in two. process in yielding a bleachable pulp from coniferous wood. Pulps of better quality, both from physical and chemical The coloring matter in pulps is of the nature of a dye and considerations, are obtained by cooking the wood as little can be removed without materially reducing yields. Most as possible in isolating the fibers and by accomplishing as of the action in cooking to reduce bleach consumption is to much of the burden of purification as possible in the bleaching dissolve and degrade the cellulose. and washing operations. The Determination of Vanadium and Chromium in Ferrovanadium by Electrometric Titration' By G. L. Kelley, J. A. Wiley, R. T. Bohn and W. e. Wright MIDVALESTEEL & ORDNANCE C0.p NICETOWNPLANT, PHILADELPHIA, PENNSYLVANtd The object of this paper is to describe a method for the When the vanadyl sulfate is titrated at 80" C. with perman- determination of vanadium in ferrovanadium not subject ganate in a similar acid concentration, the change of poten- to interference by chromium, which is so often present. Kel- tial is about 60 mv. -

Toxicological Profile for Vanadium

TOXICOLOGICAL PROFILE FOR VANADIUM U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES Public Health Service Agency for Toxic Substances and Disease Registry September 2012 VANADIUM ii DISCLAIMER Use of trade names is for identification only and does not imply endorsement by the Agency for Toxic Substances and Disease Registry, the Public Health Service, or the U.S. Department of Health and Human Services. VANADIUM iii UPDATE STATEMENT A Toxicological Profile for Vanadium, Draft for Public Comment was released in September 2009. This edition supersedes any previously released draft or final profile. Toxicological profiles are revised and republished as necessary. For information regarding the update status of previously released profiles, contact ATSDR at: Agency for Toxic Substances and Disease Registry Division of Toxicology and Human Health Sciences (proposed) Environmental Toxicology Branch (proposed) 1600 Clifton Road NE Mailstop F-62 Atlanta, Georgia 30333 VANADIUM iv This page is intentionally blank. VANADIUM v FOREWORD This toxicological profile is prepared in accordance with guidelines* developed by the Agency for Toxic Substances and Disease Registry (ATSDR) and the Environmental Protection Agency (EPA). The original guidelines were published in the Federal Register on April 17, 1987. Each profile will be revised and republished as necessary. The ATSDR toxicological profile succinctly characterizes the toxicologic and adverse health effects information for the toxic substances each profile describes. Each peer-reviewed profile identifies and reviews the key literature that describes a substance's toxicologic properties. Other pertinent literature is also presented but is described in less detail than the key studies. The profile is not intended to be an exhaustive document; however, more comprehensive sources of specialty information are referenced. -

Vanadium Recycling in the United States in 2004

U.S. Department of the Interior U.S. Geological Survey Vanadium Recycling in the United States in 2004 By Thomas G. Goonan U.S. GEOLOGICAL SURVEY CIRCULAR 1196–S Version 1.1, October 6, 2011 FLOW STUDIES FOR RECYCLING METAL COMMODITIES IN THE UNITED STATES U.S. Department of the Interior KEN SALAZAR, Secretary U.S. Geological Survey Marcia K. McNutt, Director U.S. Geological Survey, Reston, Virginia: 2011 Version 1.0 was released online August 4, 2011. Version 1.1 was released online October 6, 2011, to show a revision in the recycling rate on p. S3 and S10. For more information on the USGS—the Federal source for science about the Earth, its natural and living resources, natural hazards, and the environment, visit http://www.usgs.gov or call 1–888–ASK–USGS. For an overview of USGS information products, including maps, imagery, and publications, visit http://www.usgs.gov/pubprod To order this and other USGS information products, visit http://store.usgs.gov Any use of trade, product, or firm names is for descriptive purposes only and does not imply endorsement by the U.S. Government. Although this report is in the public domain, permission must be secured from the individual copyright owners to reproduce any copyrighted materials contained within this report. Suggested citation: Goonan, T.G., 2011, Vanadium recycling in the United States in 2004 (ver. 1.1, October 6, 2011), chap. S of Sibley, S.F., ed., Flow studies for recycling metal commodities in the United States: U.S. Geological Survey Circular 1196, p. S1–S17, available only online. -

Shipyard Industry Standards

Shipyard Industry Standards OSHA 2268-11R 2015 Occupational Safety and Health Act of 1970 “To assure safe and healthful working conditions for working men and women; by authorizing enforcement of the standards developed under the Act; by assisting and encouraging the States in their efforts to assure safe and healthful working conditions; by providing for research, information, education, and training in the field of occupational safety and health.” This publication is not a standard or regulation, and it creates no new legal obligations. It contains recommendations as well as descriptions of mandatory safety and health standards. The recommendations are advisory in nature, informational in content, and are intended to assist employers in providing a safe and healthful workplace. The Occupational Safety and Health Act (OSH Act) requires employers to comply with safety and health standards and regulations promulgated by OSHA or by a state with an OSHA-approved state plan. In addition, the Act’s General Duty Clause, Section 5(a)(1), requires employers to provide their employees with a workplace free from recognized hazards likely to cause death or serious physical harm. Material contained in this publication is in the public domain and may be reproduced, fully or partially, without permission. Source credit is requested but not required. This information will be made available to sensory-impaired individuals upon request. Voice phone: (202) 693-1999; tele- typewriter (TTY) number: 1-877-889-5627. Shipyard Industry Standards U.S. Department of Labor Occupational Safety and Health Administration OSHA 2268-11R 2015 Cover photo from the American Shipbuilding Association, courtesy of General Dynamics NASSCO in San Diego, CA. -

Ferrovanadium and Nitrided Vanadium from Russia

Ferrovanadium and Nitrided Vanadium From Russia Investigation No. 731-TA-702 (Second Review) Publication 3887 September 2006 U.S. International Trade Commission COMMISSIONERS Daniel R. Pearson, Chairman Shara L. Aranoff, Vice Chairman Jennifer A. Hillman Stephen Koplan Deanna Tanner Okun Charlotte R. Lane Robert A. Rogowsky Director of Operations Staff assigned Russell Duncan, Investigator Gerald Houck, Industry Analyst Karen Veninga Driscoll, Attorney Diane Mazur, Supervisory Investigator Address all communications to Secretary to the Commission United States International Trade Commission Washington, DC 20436 U.S. International Trade Commission Washington, DC 20436 www.usitc.gov Ferrovandium and Nitrided Vanadium From Russia Investigation No. 731-TA-702 (Second Review) Publication 3887 September 2006 CONTENTS Page Determination................................................................... 1 Views of the Commission ......................................................... 3 Introduction .................................................................... I-1 Background .................................................................. I-1 The original investigation and first review ......................................... I-1 Commerce’s administrative reviews............................................... I-3 Commerce’s final results of expedited sunset review.................................. I-4 Distribution of Continued Dumping and Subsidy Offset Act funds ....................... I-4 Related investigations......................................................... -

OSHA Hazard Classification Guidance for Manufacturers, Importers, And

HAZARD COMMUNICATION Hazard Classification Guidance for Manufacturers, Importers, and Employers OSHA 3844-02 2016 Occupational Safety and Health Act of 1970 “To assure safe and healthful working conditions for working men and women; by authorizing enforcement of the standards developed under the Act; by assisting and encouraging the States in their efforts to assure safe and healthful working conditions; by providing for research, information, education, and training in the field of occupational safety and health.” Material contained in this publication is in the public domain and may be reproduced, fully or partially, without permission. Source credit is requested but not required. This information will be made available to sensory- impaired individuals upon request. Voice phone: (202) 693-1999; teletypewriter (TTY) number: 1-877-889-5627. This publication provides a general overview of a particular standards-related topic. This publication does not alter or determine compliance responsibilities which are set forth in OSHA standards, and the Occupational Safety and Health Act. Moreover, because interpretations and enforcement policy may change over time, for additional guidance on OSHA compliance requirements, the reader should consult current administrative interpretations and decisions by the Occupational Safety and Health Review Commission and the courts. This guidance document is not a standard or regulation, and it creates no new legal obligations. It contains recommendations as well as descriptions of mandatory safety and health standards. The recommendations are advisory in nature, informational in content, and are intended to assist employers in providing a safe and healthful workplace. The Occupational Safety and Health Act requires employers to comply with safety and health standards and regulations promulgated by OSHA or by a state with an OSHA-approved state plan. -

Vanadyl Sulfate Indicated Effects on Body Weight in Animals While Studies with Sodium Metavanadate Showed Effects on Urinary Markers

Chemical Information Review Document for Oral Exposure to Tetravalent and Pentavalent Vanadium Compounds Supporting Nomination for Toxicological Evaluation by the National Toxicology Program January 2008 National Toxicology Program National Institute of Environmental Health Sciences National Institutes of Health U.S. Department of Health and Human Services Research Triangle Park, NC http://ntp.niehs.nih.gov/ Abstract Vanadium (CAS No. 7440-62-2) is an element that exists in a number of oxidation states ranging from -1 to +5 and can be found in various locales around the world. Absorption of vanadium from the gastrointestinal tract is poor and most ingested vanadium is typically converted to vanadyl. Excretion of absorbed vanadium is primarily via urine while unabsorbed vanadium is mainly eliminated in feces. Studies indicate that toxicity is dependent on the valence of vanadium, increasing with increasing valence. Thus, pentavalent vanadium is more toxic than tetravalent vanadium. Acute toxicity studies indicate that administration of vanadium compounds is associated with locomotor impairments and effects on respiratory and cardiovascular systems. Short-term studies indicate that while pentavalent vanadium compounds produced effects on a variety of hematological markers, tetravalent compounds do not appear to have similar effects. Both valence states are associated with alterations in body weight, and food and fluid intake after short-term oral administration. Chronic studies with vanadyl sulfate indicated effects on body weight in animals while studies with sodium metavanadate showed effects on urinary markers. A few studies indicated that toxicological effects of vanadium compounds can be modified by the presence of other compounds. Tetravalent vanadium compounds were shown to have impacts on the structures within reproductive organs, survival rate of weanlings, sperm density and motility, fertility, and litter size. -

VANADIUM PENTOXIDE 1. Exposure Data

pp227-292.qxp 31/05/2006 09:49 Page 227 VANADIUM PENTOXIDE 1. Exposure Data 1.1 Chemical and physical data 1.1.1 Nomenclature The nomenclature of selected vanadium compounds is given in Table 1. Chem. Abstr. Serv. Reg. No.: 1314-62-1 Deleted CAS Reg. No.: 12503-98-9; 56870-07-6; 87854-55-5; 87854-56-6; 166165- 37-3; 172928-47-1; 184892-22-6; 200577-85-1; 203812-34-4; 251927-12-5; 410546- 90-6 Chem. Abstr. Serv. Name: Vanadium oxide (V2O5) IUPAC Systematic Name: Vanadium oxide Synonyms: CI 77938; divanadium pentaoxide; pentaoxodivanadium; vanadic acid anhydride; vanadin (V) oxide (see also Table 1) 1.1.2 Empirical formula and relative molecular mass V2O5 Relative molecular mass: 181.88 1.1.3 Chemical and physical properties of the pure substance (a) Description: Yellow to rust-brown orthorhombic crystals (O’Neil, 2001; Lide, 2003); yellow-orange powder or dark-gray flakes (Bauer et al., 2003; National Institute for Occupational Safety and Health, 2005) (b) Boiling-point: 1800 °C, decomposes (Lide, 2003) (c) Melting-point: 670 °C (Lide, 2003); 690 °C (O’Neil, 2001) (d ) Density: 3.36 (O’Neil, 2001; Lide, 2003) (e) Solubility: Slightly soluble in water (0.1−0.8 g/100 cm3); soluble in concentrated acids and alkalis; insoluble in ethanol (Woolery, 1997; O’Neil, 2001) ( f ) Stability: Reacts with chlorine or hydrochloric acid to form vanadium oxytri- chloride; absorbs moisture from the air (ESPI, 1994). –227– pp227-292.qxp 31/05/2006 09:49 Page 228 228 IARC MONOGRAPHS VOLUME 86 Table 1. -

Preparation of Vanadium Metal John Reed Long Iowa State College

Iowa State University Capstones, Theses and Retrospective Theses and Dissertations Dissertations 1951 Preparation of vanadium metal John Reed Long Iowa State College Follow this and additional works at: https://lib.dr.iastate.edu/rtd Part of the Chemical Engineering Commons Recommended Citation Long, John Reed, "Preparation of vanadium metal " (1951). Retrospective Theses and Dissertations. 13315. https://lib.dr.iastate.edu/rtd/13315 This Dissertation is brought to you for free and open access by the Iowa State University Capstones, Theses and Dissertations at Iowa State University Digital Repository. It has been accepted for inclusion in Retrospective Theses and Dissertations by an authorized administrator of Iowa State University Digital Repository. For more information, please contact [email protected]. NOTE TO USERS This reproduction is the best copy available. UMI FBlfARATION OP VANADIUM KETAL by John Re@d Long A Dissertation Submitted to the Graduate Faculty in Partial Fulfillment of The Requirements for the Degree of DOCTOR OP PHILOSOPHY Major Subject! Chemical Engineering Approved Signature was redacted for privacy. Signature was redacted for privacy. Head of Major^epartment Signature was redacted for privacy. of Graduate College Iowa state College 1951 UMI Number: DP12433 INFORMATION TO USERS The quality of this reproduction is dependent upon the quality of the copy submitted. Broken or indistinct print, colored or poor quality illustrations and photographs, print bleed-through, substandard margins, and improper alignment can adversely affect reproduction. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if unauthorized copyright material had to be removed, a note will indicate the deletion.