Derbyshire Pension Fund 2019 Valuation Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Minutes of the Meeting of Shardlow & Great Wilne Parish Council Held on Wednesday 28 August 2019 at 7.30Pm at the Village Hall, Shardlow

Minutes of the meeting of Shardlow & Great Wilne Parish Council held on Wednesday 28 August 2019 at 7.30pm at The Village Hall, Shardlow PRESENT: Cllr M Clifton (Chairman), Cllr A Perks (Vice Chairman), Cllr C Leggett, Cllr N Hawksworth, Cllr N Stenner, Cllr P Lees, District Cllr P Watson, Clerk/RFO Fiona Stanbrook (Minutes). There was 1 member of public present. Reference Agenda Item Action 94/2019-20 Apologies for Absence DCllr Dan Corbin, DCllr Neil Atkin 95/2019-20 Declaration of Interest 3 recorded regarding parking Cllr Clifton, Cllr Leggett and Cllr Hawksworth – it was agreed no reason to leave the meeting. 96/2019-20 Public Participation Sue Hampson asked for advice with regard to the development at Castle Donington – DCllr Watson advised any FS developments this close to the parish boundary will be notified and dealt with in the usual way. Wilne Lane is still an issue with overgrown trees and hedges, as is the Greenway; which is being dealt with by DCC. Overgrowth is an issue throughout the village, there is a mix of responsibility for the overgrowth including Canal & River Trust, SDDC, DCC and private householders. Cllr Perks and Cllr Lees spent a large amount of time completing a village walk and making note of areas requiring action and these are now all being actioned. Cllr Hawksworth gave details of restraints the farming community face with hedge cutting due to nesting season – there is also the issue of the weather causing excessive growth this year. Lady in Grey has been painted white – which is not in keeping with the area. -

School Administrator South Wingfield Primary School Church Lane South Wingfield Alfreton Derbyshire DE55 7NJ

School Administrator South Wingfield Primary School Church Lane South Wingfield Alfreton Derbyshire DE55 7NJ School Administrator Newhall Green High School Brailsford Primary School Da Vinci Community College Newall Green High School Main Road St Andrew's View Greenbrow Road Brailsford Ashbourne Breadsall Manchester Derbys Derby Greater Manchester DE6 3DA DE21 4ET M23 2SX School Administrator School Administrator School Administrator Tower View Primary School Little Eaton Primary School Ockbrook School Vancouver Drive Alfreton Road The Settlement Winshill Little Eaton Ockbrook Burton On Trent Derby Derby DE15 0EZ DE21 5AB Derbyshire DE72 3RJ Meadow Lane Infant School Fritchley Under 5's Playgroup Jesse Gray Primary School Meadow Lane The Chapel Hall Musters Road Chilwell Chapel Street West Bridgford Nottinghamshire Fritchley Belper Nottingham NG9 5AA DE56 2FR Nottinghamshire NG2 7DD South East Derbyshire College School Administrator Field Road Oakwood Junior School Ilkeston Holbrook Road Derbyshire Alvaston DE7 5RS Derby Derbyshire DE24 0DD School Secretary School Secretary Leaps and Bounds Day Nursery Holmefields Primary School Ashcroft Primary School Wellington Court Parkway Deepdale Lane Belper Chellaston Sinfin Derbyshire Derby Derby DE56 1UP DE73 1NY Derbyshire DE24 3HF School Administrator Derby Grammar School School Administrator All Saints C of E Primary School Derby Grammar School Wirksworth Infant School Tatenhill Lane Rykneld Road Harrison Drive Rangemore Littleover Wirksworth Burton on Trent Derby Matlock Staffordshire Derbyshire -

South Derbyshire Labour Market Guide

1 TopHat Industries, Foston 3 ATL Warehousing & Offsite housing construction and Distribution, Foston manufacturing in a warehouse setting. Warehousing, distribution and logistics solutions. Key skills: digital design, engineering, estimating, manufacturing, site management, logistics, assembly. Key skills: fleet and operational For more details visit www.tophat.io management, finance, HGV, forklift, customer service, IT Systems. For more details visit YOUR FUTURE YOUR CAREER! www.atl.co.uk DERBY CITY CENTRE 3 1 A516 6 MILES A38 A6 A50 RADBOURNE A511 A50 4 M1 A38 CHURCH BROUGHTON HILTON 5 BURNASTON SHARDLOW SOUTH DERBYSHIRE WILLINGTON REPTON MELBOURNE A511 TICKNALL BRETBY 2 4 Bionical Solutions, Willington SWADLINCOTE Clinical services, healthcare SWADLINCOTE digital agency, contract sales SMISBY and clinical educator solutions. What does Key skills: clinical, research, your local A444 solution architect, designers ROSLISTON area have and developers, digital, sales to offer and customer relations. For more details visit NETHERSEAL www.bionical.com ? 2 The Keystone Group, Swadlincote Steel Lintel and Roof Window manufacturer. 5 Acres Engineering, Melbourne Key skills: fabrication, technical, marketing, sales, engineering, Design, manufacture, assemble of production support administration and managerial. equipment for a range of industries. For more details visit Key skills: engineering, design, product development, www.keystonegroup.co.uk digital, fabrication, technical and creative. For more details visit www.acres.engineering POPULATION -

Melbourne Area Forum

Melbourne Area Forum Tuesday, June 12th, 2018, 6.30pm. Barrow on Trent Village Hall 34, Twyford Road Barrow on Trent DE73 7HA South Derbyshire changing for the better COMMITTEE AND COUNCIL MEETINGS 2018/19 Committee Day Date ANNUAL COUNCIL Thursday 17.05.18 CIVIC COUNCIL Thursday 24.05.18 Audit Sub-Committee: Special Wednesday 30.05.18 Environmental & Development Services Thursday 31.05.18 Planning Tuesday 05.06.18 Housing & Community Services Thursday 07.06.18 Finance & Management Thursday 14.06.18 Overview & Scrutiny Wednesday 20.06.18 Planning Tuesday 26.06.18 COUNCIL Thursday 28.06.18 Etwall JMC Wednesday 11.07.18 Planning Tuesday 17.07.18 Audit Sub-Committee (Special) Wednesday 25.07.18 Finance and Management (Special) Thursday 26.07.18 Planning Tuesday 07.08.18 Environmental & Development Services Thursday 16.08.18 Housing & Community Services Thursday 23.08.18 Finance & Management Thursday 30.08.18 Planning Tuesday 04.09.18 Overview & Scrutiny Wednesday 05.09.18 Audit Sub-Committee Wednesday 19.09.18 COUNCIL Thursday 20.09.18 Planning Tuesday 25.09.18 Etwall JMC Wednesday 26.09.18 Environmental & Development Services Thursday 27.09.18 Housing & Community Services Thursday 04.10.18 Finance & Management Thursday 11.10.18 Planning Tuesday 16.10.18 Overview & Scrutiny Wednesday 17.10.18 COUNCIL Thursday 01.11.18 Planning Tuesday 06.11.18 Environmental & Development Services Thursday 15.11.18 Housing & Community Services Thursday 22.11.18 Planning Tuesday 27.11.18 Overview & Scrutiny Wednesday 28.11.18 Finance & Management Thursday -

Use of Contextual Data at the University of Warwick Please Use

Use of contextual data at the University of Warwick Please use the table below to check whether your school meets the eligibility criteria for a contextual offer. For more information about our contextual offer please visit our website or contact the Undergraduate Admissions Team. School Name School Postcode School Performance Free School Meals 'Y' indicates a school which meets the 'Y' indicates a school which meets the Free School Meal criteria. Schools are listed in alphabetical order. school performance citeria. 'N/A' indicates a school for which the data is not available. 6th Form at Swakeleys UB10 0EJ N Y Abbey College, Ramsey PE26 1DG Y N Abbey Court Community Special School ME2 3SP N Y Abbey Grange Church of England Academy LS16 5EA Y N Abbey Hill School and Performing Arts College ST2 8LG Y Y Abbey Hill School and Technology College, Stockton TS19 8BU Y Y Abbey School, Faversham ME13 8RZ Y Y Abbeyfield School, Northampton NN4 8BU Y Y Abbeywood Community School BS34 8SF Y N Abbot Beyne School and Arts College, Burton Upon Trent DE15 0JL Y Y Abbot's Lea School, Liverpool L25 6EE Y Y Abbotsfield School UB10 0EX Y N Abbotsfield School, Uxbridge UB10 0EX Y N School Name School Postcode School Performance Free School Meals Abbs Cross School and Arts College RM12 4YQ Y N Abbs Cross School, Hornchurch RM12 4YB Y N Abingdon And Witney College OX14 1GG Y NA Abraham Darby Academy TF7 5HX Y Y Abraham Guest Academy WN5 0DQ Y Y Abraham Moss High School, Manchester M8 5UF Y Y Academy 360 SR4 9BA Y Y Accrington Academy BB5 4FF Y Y Acklam Grange -

Land at Blacksmith's Arms

Land off North Road, Glossop Education Impact Assessment Report v1-4 (Initial Research Feedback) for Gladman Developments 12th June 2013 Report by Oliver Nicholson EPDS Consultants Conifers House Blounts Court Road Peppard Common Henley-on-Thames RG9 5HB 0118 978 0091 www.epds-consultants.co.uk 1. Introduction 1.1.1. EPDS Consultants has been asked to consider the proposed development for its likely impact on schools in the local area. 1.2. Report Purpose & Scope 1.2.1. The purpose of this report is to act as a principle point of reference for future discussions with the relevant local authority to assist in the negotiation of potential education-specific Section 106 agreements pertaining to this site. This initial report includes an analysis of the development with regards to its likely impact on local primary and secondary school places. 1.3. Intended Audience 1.3.1. The intended audience is the client, Gladman Developments, and may be shared with other interested parties, such as the local authority(ies) and schools in the area local to the proposed development. 1.4. Research Sources 1.4.1. The contents of this initial report are based on publicly available information, including relevant data from central government and the local authority. 1.5. Further Research & Analysis 1.5.1. Further research may be conducted after this initial report, if required by the client, to include a deeper analysis of the local position regarding education provision. This activity may include negotiation with the relevant local authority and the possible submission of Freedom of Information requests if required. -

Open PDF 715KB

LBP0018 Written evidence submitted by The Northern Powerhouse Education Consortium Education Select Committee Left behind white pupils from disadvantaged backgrounds Inquiry SUBMISSION FROM THE NORTHERN POWERHOUSE EDUCATION CONSORTIUM Introduction and summary of recommendations Northern Powerhouse Education Consortium are a group of organisations with focus on education and disadvantage campaigning in the North of England, including SHINE, Northern Powerhouse Partnership (NPP) and Tutor Trust. This is a joint submission to the inquiry, acting together as ‘The Northern Powerhouse Education Consortium’. We make the case that ethnicity is a major factor in the long term disadvantage gap, in particular white working class girls and boys. These issues are highly concentrated in left behind towns and the most deprived communities across the North of England. In the submission, we recommend strong actions for Government in particular: o New smart Opportunity Areas across the North of England. o An Emergency Pupil Premium distribution arrangement for 2020-21, including reform to better tackle long-term disadvantage. o A Catch-up Premium for the return to school. o Support to Northern Universities to provide additional temporary capacity for tutoring, including a key role for recent graduates and students to take part in accredited training. About the Organisations in our consortium SHINE (Support and Help IN Education) are a charity based in Leeds that help to raise the attainment of disadvantaged children across the Northern Powerhouse. Trustees include Lord Jim O’Neill, also a co-founder of SHINE, and Raksha Pattni. The Northern Powerhouse Partnership’s Education Committee works as part of the Northern Powerhouse Partnership (NPP) focusing on the Education and Skills agenda in the North of England. -

Royal Holloway University of London Aspiring Schools List for 2020 Admissions Cycle

Royal Holloway University of London aspiring schools list for 2020 admissions cycle Accrington and Rossendale College Addey and Stanhope School Alde Valley School Alder Grange School Aldercar High School Alec Reed Academy All Saints Academy Dunstable All Saints' Academy, Cheltenham All Saints Church of England Academy Alsop High School Technology & Applied Learning Specialist College Altrincham College of Arts Amersham School Appleton Academy Archbishop Tenison's School Ark Evelyn Grace Academy Ark William Parker Academy Armthorpe Academy Ash Hill Academy Ashington High School Ashton Park School Askham Bryan College Aston University Engineering Academy Astor College (A Specialist College for the Arts) Attleborough Academy Norfolk Avon Valley College Avonbourne College Aylesford School - Sports College Aylward Academy Barnet and Southgate College Barr's Hill School and Community College Baxter College Beechwood School Belfairs Academy Belle Vue Girls' Academy Bellerive FCJ Catholic College Belper School and Sixth Form Centre Benfield School Berkshire College of Agriculture Birchwood Community High School Bishop Milner Catholic College Bishop Stopford's School Blatchington Mill School and Sixth Form College Blessed William Howard Catholic School Bloxwich Academy Blythe Bridge High School Bolton College Bolton St Catherine's Academy Bolton UTC Boston High School Bourne End Academy Bradford College Bridgnorth Endowed School Brighton Aldridge Community Academy Bristnall Hall Academy Brixham College Broadgreen International School, A Technology -

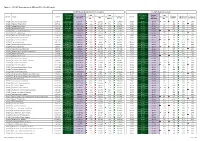

Option 2 - 1.5% NFF Factor Abatement - MFG at 0.50% - Zero HN Transfer

Option 2 - 1.5% NFF factor abatement - MFG at 0.50% - Zero HN transfer Post MFG Budget allocations (before de-delegation) Post MFG Budget rate per pupil NFF Notional % age % age NFF Notional Potential % age Potential Proposed £ Variance with £ Variance with £ Variance % age Variance £ Variance LAEstab School 2019/20 Allocation Variance with Variance with 2019/20 Allocation Proposed Variance with Allocation NFF 2019/20 with NFF with 2019/20 with 2019/20 2020/21 * NFF 2019/20 2020/21 * Allocation NFF 8312001 Roe Farm Primary School £1,640,167 £1,813,500 £1,790,177 -1.3% -£23,323 9.1% £150,010 £4,020 £4,445 £4,388 -1.3% -£57 9.1% £368 8312003 Parkview Primary School £767,814 £837,145 £825,498 -1.4% -£11,647 7.5% £57,684 £3,656 £3,986 £3,931 -1.4% -£55 7.5% £275 8312005 Ashgate Primary School £1,331,118 £1,451,961 £1,431,688 -1.4% -£20,273 7.6% £100,570 £4,083 £4,454 £4,392 -1.4% -£62 7.6% £309 8312405 Becket Primary School £922,952 £996,307 £983,254 -1.3% -£13,053 6.5% £60,302 £4,502 £4,860 £4,796 -1.3% -£64 6.5% £294 8312409 Dale Community Primary School £2,235,013 £2,495,084 £2,458,747 -1.5% -£36,337 10.0% £223,734 £4,064 £4,537 £4,470 -1.5% -£67 10.0% £407 8312424 Pear Tree Infant School £1,206,379 £1,283,454 £1,268,726 -1.1% -£14,728 5.2% £62,347 £4,750 £5,053 £4,995 -1.1% -£58 5.2% £245 8312429 Rosehill Infant and Nursery School £720,741 £763,666 £754,023 -1.3% -£9,643 4.6% £33,282 £4,937 £5,231 £5,165 -1.3% -£66 4.6% £228 8312432 Brackensdale Primary School £1,883,519 £2,039,219 £1,990,230 -2.4% -£48,989 5.7% £106,711 £3,991 £4,325 -

Briefing on Sixth Form Provision

Rep 680 Agenda item 7 Schools Forum – 10 th November 2016 School Sixth Forms - The 14-19 landscape and the diversification of School / College provision 1. Purpose To inform Schools Forum of the challenges faced by School Sixth Forms following changes in Government policy and funding, including the growth of University Technical Colleges (UTCs), Studio Schools, Free Schools and Technical Academies. 2. Policy background The school system has changed significantly over the last five years, with changes to Government funding of Post-16 education in particular being a considerable challenge. Not all the change is recent; Academies, UTCs and Studio Schools for instance were all around in various stages of development prior to 2010. The current school sector, however, is designed to give parents greater choice and schools greater freedom. Currently there exists: • Over 2,000 Academies now open in England • 291 Free Schools now open and 141 in the pipeline – DfE target 500 by 2020 • 34 Studio Schools now open with one in the pipeline • 45 UTCs open. In addition, since September 2013, GFE has been able to offer full time provision to 14-16yrs olds which adds more competition into the education system. 3. Definitions for these new types of organisations • Academies – Primary and Secondary Schools who are no longer part of the Local Authority are directly funded by the EFA and have additional responsibilities. • University Technical Colleges – Offering provision to students aged 14-19yrs, specialising in technical / vocational studies. Provision is full time, combining practical and academic studies which are delivered in work related context. A UTC has a maximum of 600 students. -

Year End 2017 Annual Report and Financial Statements PDF File

Company Registration No. 07442789 (England and Wales) THE DE FERRERS TRUST (A COMPANY LIMITED BY GUARANTEE) ANNUAL REPORT AND FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 AUGUST 2017 THE DE FERRERS TRUST REFERENCE AND ADMINISTRATIVE DETAILS Trustees Mr S L Allen (Accounting officer) Mr A Burns Mrs E Laughlin (Chair) Mrs C Lovell Mr D Moss Mrs C Shaw (Appointed 12 September 2017) Mr M Taylor Mrs J Green Mrs A Smith (Appointed 6 November 2017) Members Mrs E Laughlin (Chair) Mr M Taylor Mrs J Botton Rev. M Freeman Mr A Taylor (appointed 18 November 2016, resigned 16 March 2017) Mr M Hancock (appointed 15 June 2017) Mr K Gaunt (appointed 31 October 2017) Senior management team -Chief Executive Mr S L Allen -Director of Education Mr C A Brown (from 1 September 2017) -Director of Finance Mrs A M Taylor -Director of Human Resources Mrs J Harrison -Director of Governance and Compliance Mrs T Pyszky -Executive Principal Mrs J Green -Principal Mr N Holmes -Principal Mrs H Phillips -Principal Mrs B Breedon -Principal Mrs V Sharples (from 1 May 2017) -Principal Mrs J Kingswood (from 1 September 2017) Company secretary Mrs T Pyszky Company registration number 07442789 (England and Wales) Registered office St Marys Drive Burton on Trent Staffordshire DE13 0LL Academies operated Location Principal The de Ferrers Academy Burton upon Trent Mr N Holmes Horninglow Primary Burton upon Trent Mrs B Breedon Granville Academy Swadlincote Mrs J Kingswood Eton Park Junior Burton upon Trent Mrs H Phillips Lansdowne Burton upon Trent Mrs H Phillips The Pingle Academy -

Na Strednú Školu

PRIPRAVENÝ NA STREDNÚ ŠKOLU Tvoja príručka na prípravu na strednú školu Dodatočné informácie Milí rodičia, Kvôli Covid-19, prechod zo základnej školy na strednú bude vyzerať trocha inak ako po minulé roky. Vzhľadom na situáciu, všetky stredné školy majú svoje vlastné nariadenia a spoja sa s vami samostatne. Aby sme vám s tým pomohli, dali sme dokopy pár aktivít, ktoré budú užitočné pre začiatok diskusie o škola s vašim dieťaťom, aby ste o škole popremýšľali a prepracovali sa k debate. Na koniec sme pridali webové stránky škôl, ktoré naše deti navštevujú ( Zahrnuli sme aj odkaz kde to škola sama rozoberá). Odkazy na webové stránky obsahujú virtuálne prehliadky škôl a množstvo prezentácií od kľúčových zamestnancov škôl… Littleover Community School: http://www.littleover.derby.sch.uk/induction.php Merrill Academy: https://www.merrillacademy.derby.sch.uk/whats- happening/transition Bemrose: http://www.bemrose.derby.sch.uk/year-6-7-transition/ Murray Park: http://www.murraypark.derby.sch.uk/ City of Derby: http://www.cityofderbyacademy.org/ Derby Moor Academy: http://www.derbymoor.derby.sch.uk/Parents/Transition- Process/ Landau Forte College Derby: https://landau-forte.org.uk/ Noel Baker Academy: https://www.noelbakeracademy.co.uk/transition-2/ Saint Benedict: http://saintben.derby.sch.uk/content/y7-2020/ Lees Brook: http://www.leesbrook.co.uk/index.php/admissions/transition-task-1 Allestree Woodlands: https://www.dropbox.com/sh/2q77uahlvc8ijl6/AAC1e1R3Nkp5hA5B3mZfyvVua?dl=0 BBC Bitesize má tiež pár užitočných informácii a videí, ktoré si