Annual Report 2010/11

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![Contents [Edit] Africa](https://docslib.b-cdn.net/cover/9562/contents-edit-africa-79562.webp)

Contents [Edit] Africa

Low cost carriers The following is a list of low cost carriers organized by home country. A low-cost carrier or low-cost airline (also known as a no-frills, discount or budget carrier or airline) is an airline that offers generally low fares in exchange for eliminating many traditional passenger services. See the low cost carrier article for more information. Regional airlines, which may compete with low-cost airlines on some routes are listed at the article 'List of regional airlines.' Contents [hide] y 1 Africa y 2 Americas y 3 Asia y 4 Europe y 5 Middle East y 6 Oceania y 7 Defunct low-cost carriers y 8 See also y 9 References [edit] Africa Egypt South Africa y Air Arabia Egypt y Kulula.com y 1Time Kenya y Mango y Velvet Sky y Fly540 Tunisia Nigeria y Karthago Airlines y Aero Contractors Morocco y Jet4you y Air Arabia Maroc [edit] Americas Mexico y Aviacsa y Interjet y VivaAerobus y Volaris Barbados Peru y REDjet (planned) y Peruvian Airlines Brazil United States y Azul Brazilian Airlines y AirTran Airways Domestic y Gol Airlines Routes, Caribbean Routes and y WebJet Linhas Aéreas Mexico Routes (in process of being acquired by Southwest) Canada y Allegiant Air Domestic Routes and International Charter y CanJet (chartered flights y Frontier Airlines Domestic, only) Mexico, and Central America y WestJet Domestic, United Routes [1] States and Caribbean y JetBlue Airways Domestic, Routes Caribbean, and South America Routes Colombia y Southwest Airlines Domestic Routes y Aires y Spirit Airlines Domestic, y EasyFly Caribbean, Central and -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

Liste-Exploitants-Aeronefs.Pdf

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, XXX C(2009) XXX final COMMISSION REGULATION (EC) No xxx/2009 of on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) EN EN COMMISSION REGULATION (EC) No xxx/2009 of on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) THE COMMISSION OF THE EUROPEAN COMMUNITIES, Having regard to the Treaty establishing the European Community, Having regard to Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a system for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/EC1, and in particular Article 18a(3)(a) thereof, Whereas: (1) Directive 2003/87/EC, as amended by Directive 2008/101/EC2, includes aviation activities within the scheme for greenhouse gas emission allowance trading within the Community (hereinafter the "Community scheme"). (2) In order to reduce the administrative burden on aircraft operators, Directive 2003/87/EC provides for one Member State to be responsible for each aircraft operator. Article 18a(1) and (2) of Directive 2003/87/EC contains the provisions governing the assignment of each aircraft operator to its administering Member State. The list of aircraft operators and their administering Member States (hereinafter "the list") should ensure that each operator knows which Member State it will be regulated by and that Member States are clear on which operators they should regulate. -

Delivering Excellent Service Quality in Low Cost Aviation

MASTER THESIS IMM – International Marketing & Management DELIVERING EXCELLENT SERVICE QUALITY IN LOW COST AVIATION A Process Perspective on the Passenger Market in Copenhagen Airport December 2009 Rasmus Lindstrøm Jensen Advisor: Jesper Clement COPENHAGEN BUSINESS SCHOOL Preface The following thesis is composed on the basis of empirical data collected at Norwegian, Cimber Sterling and six individual airline passengers. I would like to thank Lone Koch (Vice President of Product Management, Cimber Sterling ) and Johan Bisgaard Larsen (Marketing Manager, Norwegian - CPH ) for the kindness and dedication. They contributed with precious information in devising the problem statement and further made the execution of the questionnaire survey possible. Further, I would like to thank Adam Høyer ( Co+Hoegh ), Christoffer Casparij ( Væksthus Sjælland ), Lene Susgaard Henriksen ( Novo Nordisk ), Morten Kaaber ( Muuto New Nordic ), Ditte Clément ( CBS ) and Line Lundø ( CBS ) for contributing with valuable information in the focus group interview. Finally, I would like to thank my advisor Jesper Clement for being a committed and pleasant advisor and sparring partner throughout the entire process. Since the number of pages in thesis exceeds 80 pages a calculation of the magnitude has been made to keep the record straight. The calculation are based on the assumption that one normal page corresponds to 2275 characters and one figure corresponds to 800 characters. Thus the actual number of pages is calculated; (169.675 + (800*16)/2275 = 80,2 pages). Consequently, the thesis keeps within the specified boundaries. Copenhagen, December 2009 Rasmus Lindstrøm Jensen Executive Summary This thesis explores the concept of service quality and customer satisfaction with low cost airlines in Copenhagen Airport. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Industry Monitor the EUROCONTROL Bulletin on Air Transport Trends

Issue N°141. 31/05/12 Industry Monitor The EUROCONTROL bulletin on air transport trends European flights declined by 2.7% in April. EUROCONTROL statistics and forecasts 1 May update of the two-year flight forecast is for a Other statistics and forecasts 2 downward revision of 0.4 percentage points to 1.7% fewer flights in 2012 than in 2011. The Passenger airlines 3 outlook for 2013 is for 1.6% growth. Cargo 6 ACI reported overall passenger traffic at Financial results of airlines 7 European airports to be up 3.4% in 1Q12 on Environment 7 1Q11 whereas aircraft movements decreased by 1.7%. Airports 8 Oil 8 European airlines selected in this bulletin recorded €1.7 billion operating losses during Aircraft Manufacturing 9 1Q12, a 17% increase on the same period a year Economy 9 ago. Regulation 9 Oil prices reduced to €79 per barrel on 31 May, Fares 9 dropping 15% from April. EUROCONTROL statistics and forecasts European flights declined by 2.7% in April compared with the same month last year and were similar to April 2009 levels. Strikes in Portugal, but mainly in France resulted in circa 5,000 flight cancellations. With the exception of charter and low-cost, both up 3% and 1.2% respectively on April 2011, other market segments were down circa 4% (see Figure 1) (EUROCONTROL, May). Based on preliminary data for delay from all causes, 36% of flights were delayed on departure in April, resulting in a 3 percentage point increase on April 2011. Analysis of the causes of delay shows a notable increase in reactionary delay. -

1 Determinants for Seat Capacity Distribution in EU and US, 1990-2009

Determinants for seat capacity distribution in EU and US, 1990-2009. Pere SUAU-SANCHEZ*1; Guillaume BURGHOUWT 2; Xavier FAGEDA 3 1Department of Geography, Universitat Autònoma de Barcelona, Edifici B – Campus de la UAB, 08193 Bellaterra, Spain E-mail: [email protected] 2Airneth, SEO Economic Research, Roetersstraat 29, 1018 WB Amsterdam, The Netherlands E-mail: [email protected] 3Department of Economic Policy, Universitat de Barcelona, Av.Diagonal 690, 08034 Barcelona, Spain E-mail: [email protected] *Correspondance to: Pere SUAU-SANCHEZ Department of Geography, Universitat Autònoma de Barcelona, Edifici B – Campus de la UAB, 08193 Bellaterra, Spain E-mail: [email protected] Telephone: +34 935814805 Fax: +34 935812100 1 Determinants for seat capacity distribution in EU and US, 1990-2009. Abstract Keywords: 2 1. Introduction Air traffic is one of the factors influencing and, at the same time, showing the position of a city in the world-city hierarchy. There is a positive correlation between higher volumes of air passenger and cargo flows, urban growth and the position in the urban hierarchy of the knowledge economy (Goetz, 1992; Rodrigue, 2004; Taylor, 2004; Derudder and Witlox, 2005, 2008; Bel and Fageda, 2008). In relation to the configuration of mega-city regions, Hall (2009) remarks that it is key to understand how information moves in order to achieve face-to-face communication and, over long distances, it will continue to move by air, through the big international airports (Shin and Timberlake, 2000). This paper deals with the allocation of seat capacity among all EU and US airports over a period of 20 years. -

Winglets on Sterling Airlines B737

PRESS RELEASE Nice, 1st February 2008 Winglets on Sterling Airlines B737 Sterling Airlines is introducing winglets on its Boeing 737NG fleet. Winglets are now a must-have for middle-haul airlines, as they reduce fuel burn by extending the wing area and reducing aerodynamic drag at the wingtip. Paul Woodman, Sterling Airlines Engineering Director, says: “When the facts and figures regarding the winglets were put to Sterling Airlines by the manufacturer, Aviation Partners Boeing, it was clear that they had to be installed. It was then down to the engineering department to manage the project and ensure we delivered the aircraft back to service on time and on budget, which we did in co-operation with our project partner.” Peter Christian Jensen, Sterling Airlines Chief Pilot, and in Flight Operations, adds: “It is correct that Sterling Airlines has introduced a project concerning fuel saving. The positive impact of winglets is demonstrated as below: 1. Fuel policy in Sterling dictates that pilots tank-up with the exact amount of fuel needed as per calculation for each flight. 2. When taxiing, only 1 engine on is needed. 3. More economical and efficient planning is done for descent profile. 4. Removal of the stairs normally in the aircraft, as they weigh around 700kgs. This equipment is not mandatory. With the present statistical information we have, winglets saved us approx. 7.51 % fuel.” With Sterling Airlines’ good punctuality and major airports you do not waste your time on travelling – and you spend less on air fares and get more money to pamper yourself and your loved ones with. -

Bombardier Business Aircraft and Are Not Added to This Report

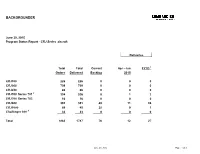

BACKGROUNDER June 30, 2015 Program Status Report - CRJ Series aircraft Deliveries Total Total Current Apr - Jun FYTD 1 Orders Delivered Backlog 2015 CRJ100 226 226 0 0 0 CRJ200 709 709 0 0 0 CRJ440 86 86 0 0 0 CRJ700 Series 701 2 334 326 8 1 2 CRJ700 Series 705 16 16 0 0 0 CRJ900 391 351 40 11 24 CRJ1000 68 40 28 0 1 Challenger 800 3 33 33 0 0 0 Total 1863 1787 76 12 27 June 30, 2015 Page 1 of 3 Program Status Report - CRJ Series aircraft CRJ700 CRJ700 CRJ700 CRJ700 Customer Total Total CRJ100 CRJ100 CRJ200 CRJ200 CRJ440 CRJ440 Series 701 Series 701 Series 705 Series 705 CRJ900 CRJ900 CRJ1000 CRJ1000 Orders Delivered Backlog Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Adria Airways 12 11 1 0 0 5 5 0 0 0 0 0 0 7 6 0 0 AeroLineas MesoAmericanas 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Air Canada 56 56 0 24 24 17 17 0 0 0 0 15 15 0 0 0 0 Air Dolimiti 5 5 0 0 0 5 5 0 0 0 0 0 0 0 0 0 0 Air Littoral 19 19 0 19 19 0 0 0 0 0 0 0 0 0 0 0 0 Air Nostrum 81 56 25 0 0 35 35 0 0 0 0 0 0 11 11 35 10 Air One 10 10 0 0 0 0 0 0 0 0 0 0 0 10 10 0 0 Air Wisconsin 64 64 0 0 0 64 64 0 0 0 0 0 0 0 0 0 0 American Airlines 54 30 24 0 0 0 0 0 0 0 0 0 0 54 30 0 0 American Eagle 47 47 0 0 0 0 0 0 0 47 47 0 0 0 0 0 0 Arik Air 7 5 2 0 0 0 0 0 0 0 0 0 0 4 4 3 1 Atlantic Southeast (ASA) 57 57 0 0 0 45 45 0 0 12 12 0 0 0 0 0 0 Atlasjet 3 3 0 0 0 0 0 0 0 0 0 0 0 3 3 0 0 Austrian arrows 4 13 13 0 0 0 13 13 0 0 0 0 0 0 0 0 0 0 BRIT AIR 49 49 0 20 20 0 0 0 0 15 15 0 0 0 0 14 14 British European 4 4 0 0 0 4 4 0 0 0 0 0 0 0 0 0 0 China Eastern Yunnan 6 6 0 0 0 6 6 0 0 0 0 0 0 0 0 0 0 China Express 28 18 10 0 0 0 0 0 0 0 0 0 0 28 18 0 0 Cimber Air 2 2 0 0 0 2 2 0 0 0 0 0 0 0 0 0 0 COMAIR 130 130 0 110 110 0 0 0 0 20 20 0 0 0 0 0 0 DAC AIR 2 2 0 0 0 2 2 0 0 0 0 0 0 0 0 0 0 Delta Connection 168 168 0 0 0 94 94 0 0 30 30 0 0 44 44 0 0 Delta Air Lines 40 40 0 0 0 0 0 0 0 0 0 0 0 40 40 0 0 Estonian Air 3 3 0 0 0 0 0 0 0 0 0 0 0 3 3 0 0 The Fair Inc. -

Case No COMP/M.2672 - SAS / SPANAIR

EN Case No COMP/M.2672 - SAS / SPANAIR Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 05/03/2002 Also available in the CELEX database Document No 302M2672 Office for Official Publications of the European Communities L-2985 Luxembourg COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 05/03/2002 SG (2002) D/228776 In the published version of this decision, some PUBLIC VERSION information has been omitted pursuant to Article 17(2) of Council Regulation (EEC) No 4064/89 concerning non-disclosure of business secrets and other confidential information. The omissions are shown thus […]. Where possible the information omitted has been replaced by ranges of figures or a MERGER PROCEDURE general description. ARTICLE 6-1(b) DECISION To the notifying party Dear Sirs, Subject: Case No COMP/M.2672 - SAS/Spanair Notification of 4.2.2002 pursuant to Article 4 of Council Regulation No 4064/89 1. On 4.2.2002, the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EEC) No 4064/891 (“The Merger Regulation) by which the undertaking Scandanavian Airlines Systems Denmark-Norway- Sweden (SAS) proposes to acquire sole control of Spanair Holding S.L (Spanair) within the meaning of article 3 (1) (b) of the aforementioned Council Regulation, through a purchase of shares. 2. After examination of the notification, the Commission has concluded that the notified operation falls within the scope of Council Regulation (EEC) No 4064/89 and does not raise serious doubts as to its compatibility with the common market and with the EEA Agreement. -

SAS-Annual-Report-1998-English.Pdf

Annual Report 1998 The SAS Group SAS Danmark A/S • SAS Norge ASA • SAS Sverige AB A strong traffic system Table of contents SAS offers its customers a global traffic system. This is a network which provides Important events during 1998 1 SAS assets 49 them with convenient and efficient travel Comments from the President 2 SAS’s brand 50 connections between continents, coun- A presentation of SAS 4 The aircraft fleet 51 tries and towns, and which enables SAS to SAS and the capital market 5 Risk management and credit ratings 54 continue to be successful in an increasing- SAS International Hotels 12 ly competitive market. Data per share Financial reports 57 SAS participates actively in the creation SAS Danmark A/S 13 The structure of the SAS Group 58 and development of Star Alliance™, the SAS Norge ASA 14 Comments from the Chairman 59 world’s strongest airline alliance involving SAS Sverige AB 15 Report by the Board of Directors 60 the partnership of SAS, Air Canada, Luft- Ten-year financial overview 16 SAS Group’s Statement of Income 62 hansa, Thai Airways International, United SAS Group’s Balance Sheet 64 Airlines and Varig Brazilian Airlines. Air New The international market situation 19 SAS Group’s Statement of Changes Zealand and Ansett Australia become active International trends 20 in Financial Position 66 members from March 28; All Nippon Airways Development of the industry 22 Accounting and valuation principles 69 later in 1999. Customer needs and preferences 25 Notes 71 In the Scandinavian market, SAS offers Auditors Report 77 an unbeatable network together with its Markets and traffic 27 SAS’s Board of Directors 78 regional partners Cimber Air, Widerøe, Markets 28 SAS’s Management 80 Skyways, Air Botnia and Maersk. -

Annual Report 2009

2 A N N U A L 2 REPORT 2009 FINANCIAL HIGHLIGHTS (million DKK) 2005 2006 2007 2008 2009 Operating revenue 869.7 1,011.7 1,074.7 1,152.1 1,112.9 Primary operating income 71.9 94.8 70.7 74.6 50.0 Income before taxes 67.8 90.8 73.2 83.1 52.8 Profit/loss for the year 40.8 75.0 49.3 56.7 36.8 Assets 503.2 566.8 554.8 568.2 611.7 Equity 334.7 408.9 458.2 514.9 551.7 Equity and reserves 809.4 865.0 972.9 1,011.3 1,043.7 Investments in fixed assets 72.5 108.8 83.4 115.6 147.9 Number of employees (December 31st) 569 613 620 669 668 Net profit ratio 8.3% 9.4% 6.6% 6.5% 4.4% Rate of return 8.9% 11.0% 7.3% 7.4% 4.8% Return of invested 13.1% 20.2% 11.4% 11.6% 6.9% Solvency ratio 41.4% 47.3% 47.1% 50.9% 52.9% STATISTICS Unit 2005 2006 2007 2008 2009 Length of scheduled service network Km 13,578 13,527 17,922 14,235 14,235 Number of towns served Towns 21 22 22 21 21 Kilometres flown, scheduled 1000 4,578 4,806 5,247 5,195 4,972 Airborne hours, total Hours 17,994 21,084 23,136 24,056 22,583 Airborne hours, scheduled Hours 10,430 10,877 11,738 11,696 11,076 Available tonne-kilometre, scheduled 1000 75,881 77,993 86,322 82,185 74,539 Revenue tonne-kilometre, scheduled 1000 48,554 49,485 51,301 53,542 49,934 Total load factor, scheduled Percent 64.0% 63.4% 59.4% 65.1% 67.0% Number of passengers carried 1000 343 372 403 421 399 Available seat-kilometre, scheduled 1000 554,939 573,325 641,339 604,333 578,207 Revenue seat-kilometre, scheduled 1000 427,174 441,422 468,752 485,351 458,534 Cabin factor, scheduled Percent 77.0% 77.0% 73.1% 80.3% 79.3% Average