1 Determinants for Seat Capacity Distribution in EU and US, 1990-2009

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Delivering Excellent Service Quality in Low Cost Aviation

MASTER THESIS IMM – International Marketing & Management DELIVERING EXCELLENT SERVICE QUALITY IN LOW COST AVIATION A Process Perspective on the Passenger Market in Copenhagen Airport December 2009 Rasmus Lindstrøm Jensen Advisor: Jesper Clement COPENHAGEN BUSINESS SCHOOL Preface The following thesis is composed on the basis of empirical data collected at Norwegian, Cimber Sterling and six individual airline passengers. I would like to thank Lone Koch (Vice President of Product Management, Cimber Sterling ) and Johan Bisgaard Larsen (Marketing Manager, Norwegian - CPH ) for the kindness and dedication. They contributed with precious information in devising the problem statement and further made the execution of the questionnaire survey possible. Further, I would like to thank Adam Høyer ( Co+Hoegh ), Christoffer Casparij ( Væksthus Sjælland ), Lene Susgaard Henriksen ( Novo Nordisk ), Morten Kaaber ( Muuto New Nordic ), Ditte Clément ( CBS ) and Line Lundø ( CBS ) for contributing with valuable information in the focus group interview. Finally, I would like to thank my advisor Jesper Clement for being a committed and pleasant advisor and sparring partner throughout the entire process. Since the number of pages in thesis exceeds 80 pages a calculation of the magnitude has been made to keep the record straight. The calculation are based on the assumption that one normal page corresponds to 2275 characters and one figure corresponds to 800 characters. Thus the actual number of pages is calculated; (169.675 + (800*16)/2275 = 80,2 pages). Consequently, the thesis keeps within the specified boundaries. Copenhagen, December 2009 Rasmus Lindstrøm Jensen Executive Summary This thesis explores the concept of service quality and customer satisfaction with low cost airlines in Copenhagen Airport. -

Industry Monitor the EUROCONTROL Bulletin on Air Transport Trends

Issue N°141. 31/05/12 Industry Monitor The EUROCONTROL bulletin on air transport trends European flights declined by 2.7% in April. EUROCONTROL statistics and forecasts 1 May update of the two-year flight forecast is for a Other statistics and forecasts 2 downward revision of 0.4 percentage points to 1.7% fewer flights in 2012 than in 2011. The Passenger airlines 3 outlook for 2013 is for 1.6% growth. Cargo 6 ACI reported overall passenger traffic at Financial results of airlines 7 European airports to be up 3.4% in 1Q12 on Environment 7 1Q11 whereas aircraft movements decreased by 1.7%. Airports 8 Oil 8 European airlines selected in this bulletin recorded €1.7 billion operating losses during Aircraft Manufacturing 9 1Q12, a 17% increase on the same period a year Economy 9 ago. Regulation 9 Oil prices reduced to €79 per barrel on 31 May, Fares 9 dropping 15% from April. EUROCONTROL statistics and forecasts European flights declined by 2.7% in April compared with the same month last year and were similar to April 2009 levels. Strikes in Portugal, but mainly in France resulted in circa 5,000 flight cancellations. With the exception of charter and low-cost, both up 3% and 1.2% respectively on April 2011, other market segments were down circa 4% (see Figure 1) (EUROCONTROL, May). Based on preliminary data for delay from all causes, 36% of flights were delayed on departure in April, resulting in a 3 percentage point increase on April 2011. Analysis of the causes of delay shows a notable increase in reactionary delay. -

European Air Law Association 23Rd Annual Conference Palazzo Spada Piazza Capo Di Ferro 13, Rome

European Air Law Association 23rd Annual Conference Palazzo Spada Piazza Capo di Ferro 13, Rome “Airline bankruptcy, focus on passenger rights” Laura Pierallini Studio Legale Pierallini e Associati, Rome LUISS University of Rome, Rome Rome, 4th November 2011 Airline bankruptcy, focus on passenger rights Laura Pierallini Air transport and insolvencies of air carriers: an introduction According to a Study carried out in 2011 by Steer Davies Gleave for the European Commission (entitled Impact assessment of passenger protection in the event of airline insolvency), between 2000 and 2010 there were 96 insolvencies of European airlines operating scheduled services. Of these insolvencies, some were of small airlines, but some were of larger scheduled airlines and caused significant issues for passengers (Air Madrid, SkyEurope and Sterling). Airline bankruptcy, focus on passenger rights Laura Pierallini The Italian market This trend has significantly affected the Italian market, where over the last eight years, a number of domestic air carriers have experienced insolvencies: ¾Minerva Airlines ¾Gandalf Airlines ¾Alpi Eagles ¾Volare Airlines ¾Air Europe ¾Alitalia ¾Myair ¾Livingston An overall, since 2003 the Italian air transport market has witnessed one insolvency per year. Airline bankruptcy, focus on passenger rights Laura Pierallini The Italian Air Transport sector and the Italian bankruptcy legal framework. ¾A remedy like Chapter 11 in force in the US legal system does not exist in Italy, where since 1979 special bankruptcy procedures (Amministrazione Straordinaria) have been introduced to face the insolvency of large enterprises (Law. No. 95/1979, s.c. Prodi Law, Legislative Decree No. 270/1999, s.c. Prodi-bis, Law Decree No. 347/2003 enacted into Law No. -

Bombardier Business Aircraft and Are Not Added to This Report

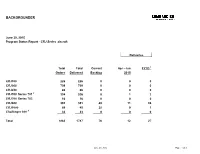

BACKGROUNDER June 30, 2015 Program Status Report - CRJ Series aircraft Deliveries Total Total Current Apr - Jun FYTD 1 Orders Delivered Backlog 2015 CRJ100 226 226 0 0 0 CRJ200 709 709 0 0 0 CRJ440 86 86 0 0 0 CRJ700 Series 701 2 334 326 8 1 2 CRJ700 Series 705 16 16 0 0 0 CRJ900 391 351 40 11 24 CRJ1000 68 40 28 0 1 Challenger 800 3 33 33 0 0 0 Total 1863 1787 76 12 27 June 30, 2015 Page 1 of 3 Program Status Report - CRJ Series aircraft CRJ700 CRJ700 CRJ700 CRJ700 Customer Total Total CRJ100 CRJ100 CRJ200 CRJ200 CRJ440 CRJ440 Series 701 Series 701 Series 705 Series 705 CRJ900 CRJ900 CRJ1000 CRJ1000 Orders Delivered Backlog Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Adria Airways 12 11 1 0 0 5 5 0 0 0 0 0 0 7 6 0 0 AeroLineas MesoAmericanas 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Air Canada 56 56 0 24 24 17 17 0 0 0 0 15 15 0 0 0 0 Air Dolimiti 5 5 0 0 0 5 5 0 0 0 0 0 0 0 0 0 0 Air Littoral 19 19 0 19 19 0 0 0 0 0 0 0 0 0 0 0 0 Air Nostrum 81 56 25 0 0 35 35 0 0 0 0 0 0 11 11 35 10 Air One 10 10 0 0 0 0 0 0 0 0 0 0 0 10 10 0 0 Air Wisconsin 64 64 0 0 0 64 64 0 0 0 0 0 0 0 0 0 0 American Airlines 54 30 24 0 0 0 0 0 0 0 0 0 0 54 30 0 0 American Eagle 47 47 0 0 0 0 0 0 0 47 47 0 0 0 0 0 0 Arik Air 7 5 2 0 0 0 0 0 0 0 0 0 0 4 4 3 1 Atlantic Southeast (ASA) 57 57 0 0 0 45 45 0 0 12 12 0 0 0 0 0 0 Atlasjet 3 3 0 0 0 0 0 0 0 0 0 0 0 3 3 0 0 Austrian arrows 4 13 13 0 0 0 13 13 0 0 0 0 0 0 0 0 0 0 BRIT AIR 49 49 0 20 20 0 0 0 0 15 15 0 0 0 0 14 14 British European 4 4 0 0 0 4 4 0 0 0 0 0 0 0 0 0 0 China Eastern Yunnan 6 6 0 0 0 6 6 0 0 0 0 0 0 0 0 0 0 China Express 28 18 10 0 0 0 0 0 0 0 0 0 0 28 18 0 0 Cimber Air 2 2 0 0 0 2 2 0 0 0 0 0 0 0 0 0 0 COMAIR 130 130 0 110 110 0 0 0 0 20 20 0 0 0 0 0 0 DAC AIR 2 2 0 0 0 2 2 0 0 0 0 0 0 0 0 0 0 Delta Connection 168 168 0 0 0 94 94 0 0 30 30 0 0 44 44 0 0 Delta Air Lines 40 40 0 0 0 0 0 0 0 0 0 0 0 40 40 0 0 Estonian Air 3 3 0 0 0 0 0 0 0 0 0 0 0 3 3 0 0 The Fair Inc. -

Compagnie Aeree Italiane

Compagnie aeree Italiane - Dati di traffico - Flotta - Collegamenti diretti - Indici di bilancio 117 118 Tav. VET 1 Compagnie aeree italiane di linea e charter - traffico 2006 COMPAGNIE Passeggeri trasportati (n.) % Riempimento Ore volate (n.) Voli (n.) Var. Var. Var. (base operativa) 2005 2006 2005 2006 Diff. 2005 2006 2005 2006 % % % attività own risk 44.283 43.452 - 1,9 57 592 2.322 2.433 4,8 1.559 1.594 2,2 Air Dolomiti (1) (Verona) voli operati con 1.248.314 1.421.539 13,9 60 633 45.922 45.757 - 0,4 35.007 33.215 - 5,1 Lufthansa Air Italy 139.105 206.217 48,2 80 800 3.333 5.358 60,8 832 1.385 66,5 (Milano Malpensa) Air One Air One Cityliner 5.264.846 5.662.595 7,6 58 580 77.361 86.189 11,4 63.817 71.161 11,5 Air One Executive (Roma Fiumicino) Air Vallèe 27.353 41.072 50,2 83 54- 29 1.540 2.024 31,4 1.422 2.486 74,8 (Aosta) Alitalia voli di linea 24.196.262 24.453.123 1,1 65 661 551.337 533.389 - 3,3 275.430 263.924 - 4,2 Alitalia Express (Roma Fiumicino) voli charter 122.169 150.652 23,3 79 75- 4 2.052 2.420 17,9 892 1.241 39,1 Alpi Eagles 1.115.079 969.430 - 13,1 58 580 24.806 27.234 9,8 16.891 18.499 9,5 (Venezia) Blue Panorama Airlines Blue Express 1.020.644 1.199.340 17,5 77 803 31.330 32.934 5,1 7.230 11.289 56,1 (Roma Fiumicino) Clubair S.p.A. -

Aeroporti Del Mezzogiorno

AEROPORTI DEL MEZZOGIORNO 2007 AEROPORTI DEL MEZZOGIORNO 2007 Alessandro Bianchi Ministro dei Trasporti Ho trascorso quasi trent’anni della mia vita in Calabria e a Reggio Calabria in particolare. Sono stati anni che ho interamente dedicato allo studio e alla pianifica- zione del territorio, per cui ho ben presente l’importanza di un efficiente sistema di mobilità per l’Italia meridionale e insulare. Le regioni dell’Italia del Sud sono attualmente dotate di un sistema aeroportua- le moderno e quindi lo sforzo che bisogna compiere è in direzione della piena inte- grazione con le reti di trasporto europee, affinché il Mezzogiorno d’Italia diventi la vera testa di ponte continentale verso i paesi della riva sud ed est del Mediter- raneo. Un vasto piano di interventi infrastrutturali negli aeroporti dell’Italia meridionale è in corso di attuazione in esecuzione di Accordi di programma quadro per il tra- sporto aereo sottoscritti con le singole regioni. Sono il frutto di una efficace collabo- razione istituzionale tra l’Unione Europea, che li ha finanziati con i fondi strutturali, le regioni, che hanno impegnato importanti contributi, e il Ministero dei Trasporti e delle Infrastrutture impegnato a centrare l’obiettivo di rendere migliore servizio al cittadino-utente. Comunque è l’intero panorama del trasporto aereo dell’Italia meri- dionale che potrebbe uscire profondamente rinnovato grazie agli interventi del PON Trasporti. Dal punto di vista territoriale la geografia articolata dell’Italia rende prioritarie le esigenze di consolidamento di un vasto network senza privilegiare solo le tratte più redditizie, e la continuità territoriale è prerequisito irrinunciabile perché l’Europa sia veramente unita e perché le barriere geografiche non si trasformino in ostacoli allo sviluppo economico. -

Case No COMP/M.2672 - SAS / SPANAIR

EN Case No COMP/M.2672 - SAS / SPANAIR Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 05/03/2002 Also available in the CELEX database Document No 302M2672 Office for Official Publications of the European Communities L-2985 Luxembourg COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 05/03/2002 SG (2002) D/228776 In the published version of this decision, some PUBLIC VERSION information has been omitted pursuant to Article 17(2) of Council Regulation (EEC) No 4064/89 concerning non-disclosure of business secrets and other confidential information. The omissions are shown thus […]. Where possible the information omitted has been replaced by ranges of figures or a MERGER PROCEDURE general description. ARTICLE 6-1(b) DECISION To the notifying party Dear Sirs, Subject: Case No COMP/M.2672 - SAS/Spanair Notification of 4.2.2002 pursuant to Article 4 of Council Regulation No 4064/89 1. On 4.2.2002, the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EEC) No 4064/891 (“The Merger Regulation) by which the undertaking Scandanavian Airlines Systems Denmark-Norway- Sweden (SAS) proposes to acquire sole control of Spanair Holding S.L (Spanair) within the meaning of article 3 (1) (b) of the aforementioned Council Regulation, through a purchase of shares. 2. After examination of the notification, the Commission has concluded that the notified operation falls within the scope of Council Regulation (EEC) No 4064/89 and does not raise serious doubts as to its compatibility with the common market and with the EEA Agreement. -

SAS-Annual-Report-1998-English.Pdf

Annual Report 1998 The SAS Group SAS Danmark A/S • SAS Norge ASA • SAS Sverige AB A strong traffic system Table of contents SAS offers its customers a global traffic system. This is a network which provides Important events during 1998 1 SAS assets 49 them with convenient and efficient travel Comments from the President 2 SAS’s brand 50 connections between continents, coun- A presentation of SAS 4 The aircraft fleet 51 tries and towns, and which enables SAS to SAS and the capital market 5 Risk management and credit ratings 54 continue to be successful in an increasing- SAS International Hotels 12 ly competitive market. Data per share Financial reports 57 SAS participates actively in the creation SAS Danmark A/S 13 The structure of the SAS Group 58 and development of Star Alliance™, the SAS Norge ASA 14 Comments from the Chairman 59 world’s strongest airline alliance involving SAS Sverige AB 15 Report by the Board of Directors 60 the partnership of SAS, Air Canada, Luft- Ten-year financial overview 16 SAS Group’s Statement of Income 62 hansa, Thai Airways International, United SAS Group’s Balance Sheet 64 Airlines and Varig Brazilian Airlines. Air New The international market situation 19 SAS Group’s Statement of Changes Zealand and Ansett Australia become active International trends 20 in Financial Position 66 members from March 28; All Nippon Airways Development of the industry 22 Accounting and valuation principles 69 later in 1999. Customer needs and preferences 25 Notes 71 In the Scandinavian market, SAS offers Auditors Report 77 an unbeatable network together with its Markets and traffic 27 SAS’s Board of Directors 78 regional partners Cimber Air, Widerøe, Markets 28 SAS’s Management 80 Skyways, Air Botnia and Maersk. -

Annual Report 2009

2 A N N U A L 2 REPORT 2009 FINANCIAL HIGHLIGHTS (million DKK) 2005 2006 2007 2008 2009 Operating revenue 869.7 1,011.7 1,074.7 1,152.1 1,112.9 Primary operating income 71.9 94.8 70.7 74.6 50.0 Income before taxes 67.8 90.8 73.2 83.1 52.8 Profit/loss for the year 40.8 75.0 49.3 56.7 36.8 Assets 503.2 566.8 554.8 568.2 611.7 Equity 334.7 408.9 458.2 514.9 551.7 Equity and reserves 809.4 865.0 972.9 1,011.3 1,043.7 Investments in fixed assets 72.5 108.8 83.4 115.6 147.9 Number of employees (December 31st) 569 613 620 669 668 Net profit ratio 8.3% 9.4% 6.6% 6.5% 4.4% Rate of return 8.9% 11.0% 7.3% 7.4% 4.8% Return of invested 13.1% 20.2% 11.4% 11.6% 6.9% Solvency ratio 41.4% 47.3% 47.1% 50.9% 52.9% STATISTICS Unit 2005 2006 2007 2008 2009 Length of scheduled service network Km 13,578 13,527 17,922 14,235 14,235 Number of towns served Towns 21 22 22 21 21 Kilometres flown, scheduled 1000 4,578 4,806 5,247 5,195 4,972 Airborne hours, total Hours 17,994 21,084 23,136 24,056 22,583 Airborne hours, scheduled Hours 10,430 10,877 11,738 11,696 11,076 Available tonne-kilometre, scheduled 1000 75,881 77,993 86,322 82,185 74,539 Revenue tonne-kilometre, scheduled 1000 48,554 49,485 51,301 53,542 49,934 Total load factor, scheduled Percent 64.0% 63.4% 59.4% 65.1% 67.0% Number of passengers carried 1000 343 372 403 421 399 Available seat-kilometre, scheduled 1000 554,939 573,325 641,339 604,333 578,207 Revenue seat-kilometre, scheduled 1000 427,174 441,422 468,752 485,351 458,534 Cabin factor, scheduled Percent 77.0% 77.0% 73.1% 80.3% 79.3% Average -

Schweizerische Zivilluftfahrt Aviation Civile Suisse

Schweizerische Zivilluftfahrt Jahresstatistik 2001 Aviation civile suisse Statistique annuelle 2001 Bundesamt für Zivilluftfahrt Office fédéral de l’aviation civile Ufficio federale dell’aviazione civile Federal Office for Civil Aviation Neuchâtel, 2002 Die vom Bundesamt für Statistik (BFS) La série «Statistique de la Suisse» publiée herausgegebene Reihe «Statistik der Schweiz» par l'Office fédéral de la statistique (OFS) couvre gliedert sich in folgende Fachbereiche: les domaines suivants: 0 Statistische Grundlagen und Übersichten 0 Bases statistiques et produits généraux 1 Bevölkerung 1 Population 2 Raum und Umwelt 2 Espace et environnement 3 Arbeit und Erwerb 3 Vie active et rémunération du travail 4 Volkswirtschaft 4 Economie nationale 5Preise 5 Prix 6 Industrie und Dienstleistungen 6 Industrie et services 7 Land- und Forstwirtschaft 7 Agriculture et sylviculture 8 Energie 8 Energie 9 Bau- und Wohnungswesen 9 Construction et logement 10 Tourismus 10 Tourisme 11 Verkehr und Nachrichtenwesen 11 Transports et communications 12 Geld, Banken, Versicherungen 12 Monnaie, banques, assurances 13 Soziale Sicherheit 13 Protection sociale 14 Gesundheit 14 Santé 15 Bildung und Wissenschaft 15 Education et science 16 Kultur, Medien, Zeitverwendung 16 Culture, médias, emploi du temps 17 Politik 17 Politique 18 Öffentliche Verwaltung und Finanzen 18 Administration et finances publiques 19 Rechtspflege 19 Droit et justice 20 Einkommen und Lebensqualität der Bevölkerung 20 Revenus et qualité de vie de la population 21 Nachhaltige Entwicklung und regionale -

World Air Transport Statistics, Media Kit Edition 2021

Since 1949 + WATSWorld Air Transport Statistics 2021 NOTICE DISCLAIMER. The information contained in this publication is subject to constant review in the light of changing government requirements and regulations. No subscriber or other reader should act on the basis of any such information without referring to applicable laws and regulations and/ or without taking appropriate professional advice. Although every effort has been made to ensure accuracy, the International Air Transport Associ- ation shall not be held responsible for any loss or damage caused by errors, omissions, misprints or misinterpretation of the contents hereof. Fur- thermore, the International Air Transport Asso- ciation expressly disclaims any and all liability to any person or entity, whether a purchaser of this publication or not, in respect of anything done or omitted, and the consequences of anything done or omitted, by any such person or entity in reliance on the contents of this publication. Opinions expressed in advertisements ap- pearing in this publication are the advertiser’s opinions and do not necessarily reflect those of IATA. The mention of specific companies or products in advertisement does not im- ply that they are endorsed or recommended by IATA in preference to others of a similar na- ture which are not mentioned or advertised. © International Air Transport Association. All Rights Reserved. No part of this publication may be reproduced, recast, reformatted or trans- mitted in any form by any means, electronic or mechanical, including photocopying, recording or any information storage and retrieval sys- tem, without the prior written permission from: Deputy Director General International Air Transport Association 33, Route de l’Aéroport 1215 Geneva 15 Airport Switzerland World Air Transport Statistics, Plus Edition 2021 ISBN 978-92-9264-350-8 © 2021 International Air Transport Association. -

Airlines Codes

Airlines codes Sorted by Airlines Sorted by Code Airline Code Airline Code Aces VX Deutsche Bahn AG 2A Action Airlines XQ Aerocondor Trans Aereos 2B Acvilla Air WZ Denim Air 2D ADA Air ZY Ireland Airways 2E Adria Airways JP Frontier Flying Service 2F Aea International Pte 7X Debonair Airways 2G AER Lingus Limited EI European Airlines 2H Aero Asia International E4 Air Burkina 2J Aero California JR Kitty Hawk Airlines Inc 2K Aero Continente N6 Karlog Air 2L Aero Costa Rica Acori ML Moldavian Airlines 2M Aero Lineas Sosa P4 Haiti Aviation 2N Aero Lloyd Flugreisen YP Air Philippines Corp 2P Aero Service 5R Millenium Air Corp 2Q Aero Services Executive W4 Island Express 2S Aero Zambia Z9 Canada Three Thousand 2T Aerocaribe QA Western Pacific Air 2U Aerocondor Trans Aereos 2B Amtrak 2V Aeroejecutivo SA de CV SX Pacific Midland Airlines 2W Aeroflot Russian SU Helenair Corporation Ltd 2Y Aeroleasing SA FP Changan Airlines 2Z Aeroline Gmbh 7E Mafira Air 3A Aerolineas Argentinas AR Avior 3B Aerolineas Dominicanas YU Corporate Express Airline 3C Aerolineas Internacional N2 Palair Macedonian Air 3D Aerolineas Paraguayas A8 Northwestern Air Lease 3E Aerolineas Santo Domingo EX Air Inuit Ltd 3H Aeromar Airlines VW Air Alliance 3J Aeromexico AM Tatonduk Flying Service 3K Aeromexpress QO Gulfstream International 3M Aeronautica de Cancun RE Air Urga 3N Aeroperlas WL Georgian Airlines 3P Aeroperu PL China Yunnan Airlines 3Q Aeropostal Alas VH Avia Air Nv 3R Aerorepublica P5 Shuswap Air 3S Aerosanta Airlines UJ Turan Air Airline Company 3T Aeroservicios