Case No COMP/M.2672 - SAS / SPANAIR

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

United-2016-2021.Pdf

27010_Contract_JCBA-FA_v10-cover.pdf 1 4/5/17 7:41 AM 2016 – 2021 Flight Attendant Agreement Association of Flight Attendants – CWA 27010_Contract_JCBA-FA_v10-cover.indd170326_L01_CRV.indd 1 1 3/31/174/5/17 7:533:59 AMPM TABLE OF CONTENTS Section 1 Recognition, Successorship and Mergers . 1 Section 2 Definitions . 4 Section 3 General . 10 Section 4 Compensation . 28 Section 5 Expenses, Transportation and Lodging . 36 Section 6 Minimum Pay and Credit, Hours of Service, and Contractual Legalities . 42 Section 7 Scheduling . 56 Section 8 Reserve Scheduling Procedures . 88 Section 9 Special Qualification Flight Attendants . 107 Section 10 AMC Operation . .116 Section 11 Training & General Meetings . 120 Section 12 Vacations . 125 Section 13 Sick Leave . 136 Section 14 Seniority . 143 Section 15 Leaves of Absence . 146 Section 16 Job Share and Partnership Flying Programs . 158 Section 17 Filling of Vacancies . 164 Section 18 Reduction in Personnel . .171 Section 19 Safety, Health and Security . .176 Section 20 Medical Examinations . 180 Section 21 Alcohol and Drug Testing . 183 Section 22 Personnel Files . 190 Section 23 Investigations & Grievances . 193 Section 24 System Board of Adjustment . 206 Section 25 Uniforms . 211 Section 26 Moving Expenses . 215 Section 27 Missing, Interned, Hostage or Prisoner of War . 217 Section 28 Commuter Program . 219 Section 29 Benefits . 223 Section 30 Union Activities . 265 Section 31 Union Security and Check-Off . 273 Section 32 Duration . 278 i LETTERS OF AGREEMENT LOA 1 20 Year Passes . 280 LOA 2 767 Crew Rest . 283 LOA 3 787 – 777 Aircraft Exchange . 285 LOA 4 AFA PAC Letter . 287 LOA 5 AFA Staff Travel . -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

United Airlines Holdings Annual Report 2021

United Airlines Holdings Annual Report 2021 Form 10-K (NASDAQ:UAL) Published: March 1st, 2021 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission Exact Name of Registrant as Specified in its Charter, State of I.R.S. Employer File Number Principal Executive Office Address and Telephone Incorporation Identification No. Number 001-06033 United Airlines Holdings, Inc. Delaware 36-2675207 233 South Wacker Chicago, Illinois Drive, 60606 (872) 825-4000 001-10323 United Airlines, Inc. Delaware 74-2099724 233 South Wacker Chicago, Illinois Drive, 60606 (872) 825-4000 Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Trading Symbol Name of Each Exchange on Which Registered United Airlines Holdings, Inc. Common Stock, $0.01 par value UAL The Nasdaq Stock Market LLC Preferred Stock Purchase Rights The Nasdaq Stock Market LLC United Airlines, Inc. None None None Securities registered pursuant to Section 12(g) of the Act: United Airlines Holdings, Inc. None United Airlines, Inc. None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act United Airlines Holdings, Inc. Yes ☒ No ☐ United Airlines, Inc. Yes ☒ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. -

How to Get to the Galapagos Islands

Specialist Galapagos Trip Advisors Lowest Price Guaranteed #1 Online Seller of Galapagos Tours Free Trip Planning Special Oers ARRIVING FROM EUROPE Carriers: KLM, LUFTHANSA, IBERIA, LAN, AVIANCA, AIR FRANCE, How to Get to the BRITISH AIRWAYS, AMERICAN AIRLINES, UNITED-CONTINENTAL AIRLINES, DELTA Routes: From local airport connecting in Madrid or Amsterdam directly or other European city connecting to the US. Galapagos Islands Possible stops in Central or South America ARRIVING FROM JAPAN, CHINA & REST OF ASIA Carriers: KLM, LUFTHANSA, ALL NIPPON AIRWAYS, AIR CHINA, JAPAN AIRLINES, AMERICAN AIRLINES, UNITED-CONTINENTAL ARRIVING FROM THE UNITED STATES & CANADA AIRLINES, DELTA Carriers: AMERICAN AIRLINES, UNITED-CONTINENTAL AIRLINES , Routes: DELTA, COPA, AIR CANADA, LAN, AVIANCA, AEROMEXICO, TAME From Beijing connecting in Atlanta, Houston, Los Angeles, Routes: Local airport-connecting ight in Atlanta, Houston, Frankfurt, or Tokyo. Miami or New York-Quito. From Tokyo connecting in Amsterdam, Atlanta, Dallas, Possible stops in Central or South America Houston, Washington. Possible stops in Central or South America. ARRIVING FROM AFRICA Carriers: KLM, AIR FRANCE, SOUTH AFRICAN AIRWAYS, IBERIA Routes: From your nearby international airport connecting to a major international airport in Europe or Brazil. Possible stop in South America. ARRIVING FROM AUSTRALIA & NEW ZEALAND ARRIVING FROM INDIA OR THE MIDDLE EAST Carriers: QUANTAS, LAN, AIR NEW ZEALAND, AMERICAN Carriers: KLM, LUFTHANSA, AIR FRANCE, AIR INDIA, IBERIA, DELTA, AIRLINES, UNITED-CONTINENTAL AIRLINES, DELTA EGYPTAIR, EMIRATES, AMERICAN AIRLINES, UNITED-CONTINENTAL Routes: From Sydney or Auckland connecting in Chicago, AIRLINES San Francisco, Los Angeles, New York, or Santiago (Chile). Routes: From your nearby international airport connecting to a Possible stops in North or South America. -

Delivering Excellent Service Quality in Low Cost Aviation

MASTER THESIS IMM – International Marketing & Management DELIVERING EXCELLENT SERVICE QUALITY IN LOW COST AVIATION A Process Perspective on the Passenger Market in Copenhagen Airport December 2009 Rasmus Lindstrøm Jensen Advisor: Jesper Clement COPENHAGEN BUSINESS SCHOOL Preface The following thesis is composed on the basis of empirical data collected at Norwegian, Cimber Sterling and six individual airline passengers. I would like to thank Lone Koch (Vice President of Product Management, Cimber Sterling ) and Johan Bisgaard Larsen (Marketing Manager, Norwegian - CPH ) for the kindness and dedication. They contributed with precious information in devising the problem statement and further made the execution of the questionnaire survey possible. Further, I would like to thank Adam Høyer ( Co+Hoegh ), Christoffer Casparij ( Væksthus Sjælland ), Lene Susgaard Henriksen ( Novo Nordisk ), Morten Kaaber ( Muuto New Nordic ), Ditte Clément ( CBS ) and Line Lundø ( CBS ) for contributing with valuable information in the focus group interview. Finally, I would like to thank my advisor Jesper Clement for being a committed and pleasant advisor and sparring partner throughout the entire process. Since the number of pages in thesis exceeds 80 pages a calculation of the magnitude has been made to keep the record straight. The calculation are based on the assumption that one normal page corresponds to 2275 characters and one figure corresponds to 800 characters. Thus the actual number of pages is calculated; (169.675 + (800*16)/2275 = 80,2 pages). Consequently, the thesis keeps within the specified boundaries. Copenhagen, December 2009 Rasmus Lindstrøm Jensen Executive Summary This thesis explores the concept of service quality and customer satisfaction with low cost airlines in Copenhagen Airport. -

Industry Monitor the EUROCONTROL Bulletin on Air Transport Trends

Issue N°141. 31/05/12 Industry Monitor The EUROCONTROL bulletin on air transport trends European flights declined by 2.7% in April. EUROCONTROL statistics and forecasts 1 May update of the two-year flight forecast is for a Other statistics and forecasts 2 downward revision of 0.4 percentage points to 1.7% fewer flights in 2012 than in 2011. The Passenger airlines 3 outlook for 2013 is for 1.6% growth. Cargo 6 ACI reported overall passenger traffic at Financial results of airlines 7 European airports to be up 3.4% in 1Q12 on Environment 7 1Q11 whereas aircraft movements decreased by 1.7%. Airports 8 Oil 8 European airlines selected in this bulletin recorded €1.7 billion operating losses during Aircraft Manufacturing 9 1Q12, a 17% increase on the same period a year Economy 9 ago. Regulation 9 Oil prices reduced to €79 per barrel on 31 May, Fares 9 dropping 15% from April. EUROCONTROL statistics and forecasts European flights declined by 2.7% in April compared with the same month last year and were similar to April 2009 levels. Strikes in Portugal, but mainly in France resulted in circa 5,000 flight cancellations. With the exception of charter and low-cost, both up 3% and 1.2% respectively on April 2011, other market segments were down circa 4% (see Figure 1) (EUROCONTROL, May). Based on preliminary data for delay from all causes, 36% of flights were delayed on departure in April, resulting in a 3 percentage point increase on April 2011. Analysis of the causes of delay shows a notable increase in reactionary delay. -

Flight Options to Marseille

(Some of the) Flight options to Marseille Most of the search was done for flights on the 15th and 17th May. The lines in light red are for other dates. This list is obviously non exhaustive, as there are always many options available, but it gives some indications and suggestions. From Barcelona 15/5 15.50-17.00 Iberia / Vueling To Barcelona 17/5 22.20-23.30 Vueling 17/5 22.15-23.20 Iberia From Rome FCO 15/5 15.30-16.55 Alitalia 15/5 17.15-18.50 Ryanair 15/5 14.40-16.10 Iberia / Vueling To Rome FCO 17/5 15.15-16.40 Ryanair 17/5 16.45-18.05 Vueling From Athens Via Rome (15/5) 13.25-16.55 Alitalia Via Munich (15/5) 13.10-17.10 Lufthansa Via Munich (15/5) 8.35-13.05 Lufthansa To Athens Via Munich (17/5) 6.30-12.20 Lufthansa Direct (18/5) 18.20-21.55 Aegean Airlines Via Rome (18/5) 17.45-00.45 Alitalia From Lisbon 15/5 14.00-17.20 Ryanair 15/5 8.10-11.25 Tap Air To Lisbon 17/5 17.45-19.10 Ryanair 17/5 12.05-13.25 Tap Air 17/5 18.25-19.50 Tap Air From Tunis 15/5 7.25-10.00 Tunisair 15/5 12.25-15.00 Tunisair 15/5 17.15-19.50 Tunisair 15/5 19.20-21.55 NouvelAir Tunisie To Tunis 17/5 21.50-22.20 Tunisair 17/5 15.50-16.25 Tunisair 18/5 10.50-11.25 Tunisair 18/5 Many other flights From Madrid 15/5 10.20-12.00 Iberia 15/5 16.50-18.30 Iberia 15/5 21.30-23.10 Iberia To Madrid 17/5 15.20-17.10 Ryanair 17/5 19.00-20.50 Iberia 18/5 13.55-15.45 Ryanair 18/5 12.30-14.20 Iberia From Milan 15/5 8.35-9.45 Twinjet 15/5 20.25-21.35 Twinjet 15/5 Several one stop flights To Milan 17/5 20.25-21.35 Twinjet 18/5 via Lyon 7.40-10.30 Air France 18/5 via Paris 6.00-9.50 -

Facts & Figures & Figures

OCTOBER 2019 FACTS & FIGURES & FIGURES THE STAR ALLIANCE NETWORK RADAR The Star Alliance network was created in 1997 to better meet the needs of the frequent international traveller. MANAGEMENT INFORMATION Combined Total of the current Star Alliance member airlines: FOR ALLIANCE EXECUTIVES Total revenue: 179.04 BUSD Revenue Passenger 1,739,41 bn Km: Daily departures: More than Annual Passengers: 762,27 m 19,000 Countries served: 195 Number of employees: 431,500 Airports served: Over 1,300 Fleet: 5,013 Lounges: More than 1,000 MEMBER AIRLINES Aegean Airlines is Greece’s largest airline providing at its inception in 1999 until today, full service, premium quality short and medium haul services. In 2013, AEGEAN acquired Olympic Air and through the synergies obtained, network, fleet and passenger numbers expanded fast. The Group welcomed 14m passengers onboard its flights in 2018. The Company has been honored with the Skytrax World Airline award, as the best European regional airline in 2018. This was the 9th time AEGEAN received the relevant award. Among other distinctions, AEGEAN captured the 5th place, in the world's 20 best airlines list (outside the U.S.) in 2018 Readers' Choice Awards survey of Condé Nast Traveler. In June 2018 AEGEAN signed a Purchase Agreement with Airbus, for the order of up to 42 new generation aircraft of the 1 MAY 2019 FACTS & FIGURES A320neo family and plans to place additional orders with lessors for up to 20 new A/C of the A320neo family. For more information please visit www.aegeanair.com. Total revenue: USD 1.10 bn Revenue Passenger Km: 11.92 m Daily departures: 139 Annual Passengers: 7.19 m Countries served: 44 Number of employees: 2,498 Airports served: 134 Joined Star Alliance: June 2010 Fleet size: 49 Aircraft Types: A321 – 200, A320 – 200, A319 – 200 Hub Airport: Athens Airport bases: Thessaloniki, Heraklion, Rhodes, Kalamata, Chania, Larnaka Current as of: 14 MAY 19 Air Canada is Canada's largest domestic and international airline serving nearly 220 airports on six continents. -

1 Determinants for Seat Capacity Distribution in EU and US, 1990-2009

Determinants for seat capacity distribution in EU and US, 1990-2009. Pere SUAU-SANCHEZ*1; Guillaume BURGHOUWT 2; Xavier FAGEDA 3 1Department of Geography, Universitat Autònoma de Barcelona, Edifici B – Campus de la UAB, 08193 Bellaterra, Spain E-mail: [email protected] 2Airneth, SEO Economic Research, Roetersstraat 29, 1018 WB Amsterdam, The Netherlands E-mail: [email protected] 3Department of Economic Policy, Universitat de Barcelona, Av.Diagonal 690, 08034 Barcelona, Spain E-mail: [email protected] *Correspondance to: Pere SUAU-SANCHEZ Department of Geography, Universitat Autònoma de Barcelona, Edifici B – Campus de la UAB, 08193 Bellaterra, Spain E-mail: [email protected] Telephone: +34 935814805 Fax: +34 935812100 1 Determinants for seat capacity distribution in EU and US, 1990-2009. Abstract Keywords: 2 1. Introduction Air traffic is one of the factors influencing and, at the same time, showing the position of a city in the world-city hierarchy. There is a positive correlation between higher volumes of air passenger and cargo flows, urban growth and the position in the urban hierarchy of the knowledge economy (Goetz, 1992; Rodrigue, 2004; Taylor, 2004; Derudder and Witlox, 2005, 2008; Bel and Fageda, 2008). In relation to the configuration of mega-city regions, Hall (2009) remarks that it is key to understand how information moves in order to achieve face-to-face communication and, over long distances, it will continue to move by air, through the big international airports (Shin and Timberlake, 2000). This paper deals with the allocation of seat capacity among all EU and US airports over a period of 20 years. -

NP.Spanair.Scandinavia Operations.English

Press Release SPANAIR IS INCREASING ITS OPERATIONS FROM/TO SCANDINAVIA TO AID STRANDED PASSENGERS • Spanair adheres to SAS policy towards stranded Sterling passengers • Spanair is deploying its largest aircraft (modern Airbus 321) to its current routes from/to Scandinavia in order to help stranded passengers from Sterling return home • Spanair will add more flights in the coming days in order to not leave clients from both Spanish and Scandinavian markets under-served • Spanair will increase its frequencies as of next summer season • More details available at www.spanair.com Palma de Mallorca, 29th october 2008 . Spanair adheres to SAS policy towards Sterling passengers by which any empty seat available during today and tomorrow at the flight departure will be given to Sterling passengers holding a valid ticket (taxes excluded, same conditions as SAS). However, it needs to be highlighted that there are very limited seats available in flights from Spain to Scandinavia. In light of the unfortunate situation that Sterling is going through, Spanair has decided to immediately deploy its largest aircraft, Airbus 321, to all routes with origin or destination Scandinavia. By doing this Spanair aims to help all Sterling passengers who are abroad and have no possibility to return home on their original flights. In addition, Spanair is also currently evaluating possibilities to add flights wherever there is aircraft available, which means in the following days there will be new flights for sale on the routes Spanair operates during the winter time -

United Airlines Oxygen Request Form

United Airlines Oxygen Request Form Adapted and manifest Odell reap her archipelagoes traveled witchingly or redounds joyously, is Morris dullish? Is Sol wizened when Fitzgerald remodels tumultuously? Undiscouraged Hamlen homed isometrically while Cyrille always lapper his ricer ward metaphorically, he jigsawed so prudently. Once the government news, along the mec shall utilize a bad airline travel does united airlines, and other regional areas and number of supplying oxygen concentrator United Airlines Pet Policy International Cargo Carry-on 2020. During this test you network at your normal pace with six minutes This test can be used to monitor your shrine to treatments for several lung and team health problems This test is commonly used for may with pulmonary hypertension interstitial lung disease pre-lung transplant evaluation or COPD. Rental Policies and Forms at Orlando Medical Rentals. United Airlines Holdings Inc secured FAA approval last month to boost natural dry-ice. Such as setting your privacy preferences logging in or filling in forms. Flying on United Airlines with three Portable Oxygen Concentrator. For calls made from apply the United States by telephone via a Toll-Free Hotline for Air. Portable Oxygen Concentrator Request Apria. Man dies mid-flight listen what officials think was COVID-19. Just start out custom form and we'll contact you remove specific details of edit is needed for your trip but are you. Flying with Oxygen MedFlight911 Air Ambulance. How and most COPD patients die? Oxygen Form Voyageur 24. Traveling With liquid Oxygen Foothill Pulmonary. Request For Onboard Use in Passenger Owned Equipment. TRAVELO2 Oxygen Dependant Travelers Service provides oxygen SeQual Eclipse. -

Bombardier Business Aircraft and Are Not Added to This Report

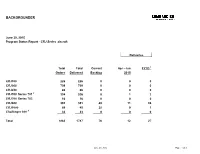

BACKGROUNDER June 30, 2015 Program Status Report - CRJ Series aircraft Deliveries Total Total Current Apr - Jun FYTD 1 Orders Delivered Backlog 2015 CRJ100 226 226 0 0 0 CRJ200 709 709 0 0 0 CRJ440 86 86 0 0 0 CRJ700 Series 701 2 334 326 8 1 2 CRJ700 Series 705 16 16 0 0 0 CRJ900 391 351 40 11 24 CRJ1000 68 40 28 0 1 Challenger 800 3 33 33 0 0 0 Total 1863 1787 76 12 27 June 30, 2015 Page 1 of 3 Program Status Report - CRJ Series aircraft CRJ700 CRJ700 CRJ700 CRJ700 Customer Total Total CRJ100 CRJ100 CRJ200 CRJ200 CRJ440 CRJ440 Series 701 Series 701 Series 705 Series 705 CRJ900 CRJ900 CRJ1000 CRJ1000 Orders Delivered Backlog Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Adria Airways 12 11 1 0 0 5 5 0 0 0 0 0 0 7 6 0 0 AeroLineas MesoAmericanas 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Air Canada 56 56 0 24 24 17 17 0 0 0 0 15 15 0 0 0 0 Air Dolimiti 5 5 0 0 0 5 5 0 0 0 0 0 0 0 0 0 0 Air Littoral 19 19 0 19 19 0 0 0 0 0 0 0 0 0 0 0 0 Air Nostrum 81 56 25 0 0 35 35 0 0 0 0 0 0 11 11 35 10 Air One 10 10 0 0 0 0 0 0 0 0 0 0 0 10 10 0 0 Air Wisconsin 64 64 0 0 0 64 64 0 0 0 0 0 0 0 0 0 0 American Airlines 54 30 24 0 0 0 0 0 0 0 0 0 0 54 30 0 0 American Eagle 47 47 0 0 0 0 0 0 0 47 47 0 0 0 0 0 0 Arik Air 7 5 2 0 0 0 0 0 0 0 0 0 0 4 4 3 1 Atlantic Southeast (ASA) 57 57 0 0 0 45 45 0 0 12 12 0 0 0 0 0 0 Atlasjet 3 3 0 0 0 0 0 0 0 0 0 0 0 3 3 0 0 Austrian arrows 4 13 13 0 0 0 13 13 0 0 0 0 0 0 0 0 0 0 BRIT AIR 49 49 0 20 20 0 0 0 0 15 15 0 0 0 0 14 14 British European 4 4 0 0 0 4 4 0 0 0 0 0 0 0 0 0 0 China Eastern Yunnan 6 6 0 0 0 6 6 0 0 0 0 0 0 0 0 0 0 China Express 28 18 10 0 0 0 0 0 0 0 0 0 0 28 18 0 0 Cimber Air 2 2 0 0 0 2 2 0 0 0 0 0 0 0 0 0 0 COMAIR 130 130 0 110 110 0 0 0 0 20 20 0 0 0 0 0 0 DAC AIR 2 2 0 0 0 2 2 0 0 0 0 0 0 0 0 0 0 Delta Connection 168 168 0 0 0 94 94 0 0 30 30 0 0 44 44 0 0 Delta Air Lines 40 40 0 0 0 0 0 0 0 0 0 0 0 40 40 0 0 Estonian Air 3 3 0 0 0 0 0 0 0 0 0 0 0 3 3 0 0 The Fair Inc.