BCGE Annual Report 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Communes\Communes - Renseignements\Contact Des Communes\Communes - Renseignements 2020.Xlsx 10.12.20

TAXE PROFESSIONNELLE COMMUNALE Contacts par commune No COMMUNE PERSONNE(S) DE CONTACT No Tél No Fax E-mail [email protected] 1 Aire-la-Ville Claire SNEIDERS 022 757 49 29 022 757 48 32 [email protected] 2 Anières Dominique LAZZARELLI 022 751 83 05 022 751 28 61 [email protected] 3 Avully Véronique SCHMUTZ 022 756 92 50 022 756 92 59 [email protected] 4 Avusy Michèle KÜNZLER 022 756 90 60 022 756 90 61 [email protected] 5 Bardonnex Marie-Laurence MICHAUD 022 721 02 20 022 721 02 29 [email protected] 6 Bellevue Pierre DE GRIMM 022 959 84 34 022 959 88 21 [email protected] 7 Bernex Nelly BARTHOULOT 022 850 92 92 022 850 92 93 [email protected] 8 Carouge P. GIUGNI / P.CARCELLER 022 307 89 89 - [email protected] 9 Cartigny Patrick HESS 022 756 12 77 022 756 30 93 [email protected] 10 Céligny Véronique SCHMUTZ 022 776 21 26 022 776 71 55 [email protected] 11 Chancy Patrick TELES 022 756 90 50 - [email protected] 12 Chêne-Bougeries Laure GAPIN 022 869 17 33 - [email protected] 13 Chêne-Bourg Sandra Garcia BAYERL 022 869 41 21 022 348 15 80 [email protected] 14 Choulex Anne-Françoise MOREL 022 707 44 61 - [email protected] 15 Collex-Bossy Yvan MASSEREY 022 959 77 00 - [email protected] 16 Collonge-Bellerive Francisco CHAPARRO 022 722 11 50 022 722 11 66 [email protected] 17 Cologny Daniel WYDLER 022 737 49 51 022 737 49 50 [email protected] 18 Confignon Soheila KHAGHANI 022 850 93 76 022 850 93 92 [email protected] 19 Corsier Francine LUSSON 022 751 93 33 - [email protected] 20 Dardagny Roger WYSS -

Assem Blage's Festival 1→4.10.20

ÉDITION 2020 : LIBÉRATRICE ET JUBILATOIRE Confinée et défaite ce printemps, la vie culturelle reprend peu à peu sa place libératrice et tous ses droits. Comme les artistes privés de scène pendant trop longtemps, vous attendez avec impatience d’assister de nouveau à des spec- tacles jubilatoires. Après une édition 2019 insolite qui fit la part belle à l’humour décalé et à la magie saisissante, celle de 2020 marque le retour sur l’avant-scène de la danse, de la musique, du cirque et du théâtre IllustratrionDA&D So2design/ Karine Bernadou avec de riches découvertes. A S S E M ! En accueillant une nouvelle fois des artistes d’exception méconnus dans notre canton et des B L A G E ’S spectacles originaux accessibles à un large public, Assemblage’S vous offre une inspiration bienfai- sante avec des premières, des créations et de FESTIVAL belles surprises. 1→4.10.20 Le festival se déroulera bien évidemment dans le respect des mesures sanitaires prescrites par les Musique - Ci!que - Danse - Théâ"!e autorités avec la qualité d’accueil et la convivialité qui sont la marque de fabrique de cet incontour- nable rendez-vous d’automne. «Il n’y a pas de hasard, il n’y a que des rendez-vous» Paul Eluard Billetterie et informations détaillées sur : Assemblages.ch Une soirée d’ouverture unique et bouleversante. Deux spectacles, une soirée typiquement «Assemblage’S». Une pièce qui secoue les publics d’un extrême à l’autre Un spectacle de clôture dédié aux zygomatiques des plus 01 Une compagnie emblématique de la danse contemporaine 02 Une danse qui vaut mille discours pour éclairer avec 03 de l’émotion, de l’éclat de rire au nœud dans la gorge. -

PROGRAMME DES SORTIES Du 16 Mars Au 10 Juin 2019

www.cyclo-chenois.ch Pour le moment, Blaise continue de bricoler le site, notamment en faisant appel à des sites extérieurs permettant de facilement préparer les albums photos et les cartes des sorties. Y a-t-il un connaisseur du web pour l'aider voire reprendre cette tâche et la dynamiser, par exemple en introduisant des alertes d'actualité, en s’ouvrant aux réseaux sociaux et en recourant à des bases de données ? Equipements du club et matériel divers PROGRAMME Les équipements du 40 ème sont disponibles. S’adresser à Blaise. Case postale 18 1226 Thônex DES SORTIES Une liste avec les anciens équipements du club et le matériel à vendre (ou à donner) est disponible via le site internet ( http://www.cyclo-chenois.ch/pdf/VendreOuDonner.pdf ). Chaque membre peut ainsi voir les équipements restants et le matériel, mais aussi proposer des articles à vendre ou à donner. du 16 mars au 10 juin 2019 Bilan des sorties de 2018 Lors des 36 sorties qui ont eu lieu, sur les 40 programmées, 66’465 km ont été parcourus par 69 différent(e)s cyclistes. La participation moyenne a été de 18,6 cyclos. Chaque participant a pédalé 99 km Mêmes heures de départ pour tous les groupes. en moyenne. Attention aux franchissements des carrefours en groupe: Le nombre de participants différents a diminué ces deux dernières années, mais ils ont été plus assidus en Pensez à tous, pas qu’à vous seul ! roulant de plus longues distances. Organisation des groupes et responsables Où ? Quand ? Comment ? Le groupe "entraînement" doit absolument se trouver un ou plusieurs responsables. -

RÉSIDENCE “LES HAUTS-CRÊTS” EDITION No 122 JUILLET 2000 VANDOEUVRES - GE EDITION CRP SUISSE - 1020 RENENS

Ouvrage no 921 Volume 29 Chapitre 4 Fiche 210 REALISATIONS IMMOBILIERES RÉSIDENCE “LES HAUTS-CRÊTS” EDITION no 122 JUILLET 2000 VANDOEUVRES - GE EDITION CRP SUISSE - 1020 RENENS Maître de l’ouvrage 1 Régie Foncière SA, Union Progest Fonds SA, rue de la Fontaine 5, 1211 Genève 3. Architectes Erbeia Bernard, route de Meinier 9, 1253 Vandoeuvres. Collaborateurs : Mahler Léo, Savoye Dominique, Ruffieux Bernard. Ingénieurs civils Jorand et Roget SA, Ingénieurs Civils SIA-AGI, rue de la Faïencerie 2, 1227 Carouge. Bureaux techniques Electricité : Félix Badel & Cie SA, rue de Carouge 114, 1211 Genève 9. Sanitaire : Schneider A. SA, rue des Voisins 18, 1205 Genève. Chauffage : SITUATION / PROGRAMME arborisées du canton, en raison d’une réglemen- Balestra & Galiotto TCC SA, tation sévère des constructions, instituée depuis rue Amat 5 bis, fort longtemps. Elle offre d’autre part de nom- 1211 Genève 21. Secteur résidentiel de l’agglomération breuses infrastructures administratives et com- Ventilation : genevoise. Le chemin des Hauts-Crêts, qui sé- merciales, de même que des écoles et un éventail Traitair SA, pare Vandoeuvres et Cologny, suit la crête d’une remarquable d’installations sportives allant du chemin Riantbosson 10, colline qui domine le lac. Ce secteur constitue un football au tennis et à l’équitation, en passant par 1217 Meyrin. quartier résidentiel de choix, situé à quelques mi- le golf et les activités nautiques les plus diverses. Géotechnique : nutes du centre ville et pourtant préservé des Deux lignes de transports publics desservent éga- Dériaz P. & C. & Cie SA, désagréments inhérents à l’activité urbaine. Il y a lement Vandoeuvres. rue Blavignac 10, plus de trois siècles déjà, les patriciens genevois 1227 Carouge. -

Les Chemins Historiques Du Canton De Genève

Carte de terrain IVS Carte de terrain Talus et délimitation Matériau meuble Rocher Mur de soutènement Mur, mur de parapet Alignement d’arbres, haie Pierre bordière, bordure Dalles bordières verticales Clôture, palissade Revêtements Les chemins historiques Rocher Matériau meuble Empierrement, cailloutis du canton de Genève Pavage, pavement Revêtement artificiel Marches, escaliers, gradins Ouvrages d’art Pont Vestiges de pont Conduite d’eau, tombino Carte d’inventaire IVS Tunnel GE Eléments du paysage routier Pierre de distance Autre pierre Arbre isolé Inscription Croix routière Oratoire, chapelle routière Chapelle Eglise Château-fort, château, ruine Edifice profane Exploitation industrielle Carrière, gravière Embarcadère, port Fontaine Carte d’inventaire Classification Importance nationale Importance régionale Importance locale Substance Tracé historique Tracé historique avec substance Tracé historique avec beaucoup de substance Inventar historischer Verkehrswege der Schweiz Inventaire des voies de communication historiques de la Suisse Inventario delle vie di comunicazione storiche della Svizzera Inventari da las vias da communicaziun istoricas da la Svizra Les chemins historiques d’importance nationale dans le canton de Genève Numération selon l’IVS 1 Genève–Nyon (–Lausanne) 2 Genève–frontière nationale (–Fort-de-L’Ecluse, F) 3 Genève–Carouge–St-Julien-en- Page de couverture Sources des illustrations Nyon Genevois, F (–Seyssel, F) Diversité des chemins historiques dans le Les photos du terrain sont de Yves Bischof- 4 Genève–Carouge–Croix-de-Rozon canton de Genève: chemin creux d’origine berger. Les autres sources sont mentionnées (–Annecy, F) romaine dans une propriété privée à Frontenex dans les légendes. Reproduction des extraits 5 Genève–Veyrier (–Pas-de-l’Echelle, F (à gauche; GE 6.2.1; cf. -

TROINEX-VEYRIER CAROUGE PLAN-LES-OUATES LANCY GRAND-SUD Arcimboldo

n°4 décembre 2017 JOURNAL DES 4 PAROISSES PROTESTANTES DE LA RÉGION SALÈVE Arcimboldo CAROUGE LANCY GRAND-SUD PLAN-LES-OUATES TROINEX-VEYRIER Edito Partir…. H Partir pour rester ? Partir pour revenir ? Pourquoi partir de chez soi - pour aller où, à la recherche de quoi ? Autour de la question de l’immigration on se demande… Pour- quoi les gens partent-ils ? Que cherchent-ils ? Et pourquoi faire un voyage de KT sur ce thème au lieu d’aller faire un projet humanitaire en Afrique ou en Asie ? Ayant immigré moi-même, je me rends compte de l’impor- tance d’aller voir ailleurs pour mieux vivre chez soi. Alors même que j’ai décidé de rester en Eu- rope, je suis persuadée que le fait d’or- ganiser un voyage avec les jeunes est extrêmement important pour les aider à mieux comprendre leur propre pays. Les jeunes avec lesquels nous sommes partis au Canada sont tous majeurs, c’est-à-dire qu’ils sont en âge de voter, de donner leur opinion, de participer à la vie sociale et politique de leur pays, de notre pays. Notre espoir, à nous les organisateurs de ce voyage, est que, ayant vu comment un autre pays gère les questions d’immigration, ils soient en mesure d’apporter peut-être un regard nouveau sur cette question ici, chez eux. Et puis, nous avons bien l’exemple de Dieu qui a "immigré" depuis son ciel pour nous rejoindre sur la terre, pour endosser notre humanité, partager nos joies et nos détresses et nous combler de son amour éternel. -

Le Développement Durable Au Détour Du Chemin

Cologny – Vandœuvres Le développement durable au détour du chemin www.genevedurable.ch Sommaire Pages de bienvenue 2 Le développement durable au détour du chemin 4 ❚ Promenade I Côté Lac 9 ❚ Promenade II Côté Alpes 49 Les principes et objectifs du développement durable 95 Crédits iconographiques, Impressum 97 Faites votre marché, garnissez votre cave, restaurez-vous ! 99 Remerciements 100 www.genevedurable.ch La collection de guides « Le développement durable au détour du chemin » est réalisée : Avec le soutien d’une fondation privée Genevoise 1 Cologny – Vandœuvres Le développement durable au détour du chemin Deux promenades : • Côté Lac • Côté Alpes Raphaëlle JUGE Jean-Bernard LACHAVANNE Avec la collaboration de Rémi MERLE Ricardo GARCIA SANCHEZ L’ASDD est partenaire de Projet reconnu comme « Activité de la Décennie pour l’éducation en vue du développement durable » par la Commission suisse pour l’UNESCO. http://www.decennie.ch © ASDD – mai 2017 2 Avant-propos Chère lectrices, chers lecteurs, Cologny et Vandœuvres se jouxtent et partagent des intérêts communs, notamment à travers les écoles ou le traitement des déchets de jardin par compostage en bordure de champs ou bien encore par la Charte environnementale. Similaires, mais différentes, Vandœuvres campagnarde, Cologny lacustre et sub-urbaine, se complètent. Réunir nos deux communes pour ce guide élaboré par l’Association pour la sensibilisation au développement durable à Genève (ASDD) a du sens. Nos sensibilités au développement durable se rejoignent car nos efforts se concentrent sur l’environnement et le bien-être de nos habitants. Ces actions concrètes sont certes spécifiques à chaque commune, toutefois le renforcement d’initiatives coordonnées apportera un impact encore plus significatif à l’avenir à certains de nos engagements et réalisations. -

Fosc.Ch Fusc.Ch Shab.Ch

Schweizerisches shab.ch Handelsamtsblatt Feuille officielle suisse fosc.ch du commerce Foglio ufficiale svizzero fusc.ch di commercio Andere gesetzliche Publikationen - Autres publications légales - Altre pubblicazioni legali UNIQUE PUBLICATION Conversion du numéro d'identification des entreprises (IDE) dans le registre du commerce du canton de GE. Liste des entités juridiques actives, triées par raison sociale/nom, avec indication du numéro d'entreprise et IDE, état des données: 18.12.2013 La liste compléte sur les pages suivantes 07225832 i Dienstag - Lundi - Lunedì, 19.12.2013, No 245, Jahrgang - année - anno: 131 Andere gesetzliche Publikationen - Autres publications légales, Altre pubblicazioni legali Verschiedenes - Divers - Diversi ID13 IDE RAISON, NOM SIÈGE CH66017050138 CHE291287210 " Le Meilleur d'Ailleurs " Alice Pereira Genève CH66002389681 CHE107742623 "Académie de langues et de commerce" G. et S. Roesner Genève CH66016100076 CHE113718202 "Akash, atelier de bien-être", R. Kilchherr Céligny CH66001179722 CHE107894799 "Allied Services" Compagnie Fiduciaire SA Genève CH66000069692 CHE100091948 "Alphamusic" Jean-Louis Roy Genève CH66000199683 CHE110374000 "Antar" B. Lardi Onex CH66002429703 CHE101412334 "Ardor" L. Immelé Genève CH66001869610 CHE103163030 "Asia-Africa Museum" Hélène Nguyen Tan-Phuoc Genève CH66021470073 CHE113795941 "Au Chien qui Nage", Centre Genevois d'Hydrothérapie Canine, Michèle Despland Robert Carouge (GE) CH66026780114 CHE199795828 "Baszanger", titulaire Y. Cantini-Baszanger Collonge-Bellerive CH66008279940 -

Discover Malbine's Sculptures.Pdf

1 Little girl with the flower 2 Little girl with the fish 3 Skateboard 4 Girl with the cats 5 Little friends m 2 k 6 Little acrobat 2 7 Motherhood with four children 8 Eve 3 9 Little donkey 1 CROPETTES PARK 01 Footballer Cornavin / Poste 6 km 1 1 Young filly COLOGNY Manoir School 12 Silence SAINT-JEAN PARK 31 Circus girl Cologny-Temple 41 Little dancer Isaac-Mercier / Goulart 51 Standing motherhood 5 61 Girl lying on her stomach k m 71 Little friends 81 Little girl with the flower 91 Little girl with the cat 8 4 km 6 9 THÔNEX 7 Trois-Chêne hospital Hôpital des Trois-Chêne km 5 5 1 k HUG m Cantonal hospital Hôpital / Claparède / Augustins BERTRAND PARK 1 Peschier 10 à 19 km 6 UNIVERSITY CAMPUS st. Edouard-Tavan 11 TROINEX TOWN HALL Crêts de Champel Troinex Mairie TPG STOP LOCATION Artistic walk in Geneva Malbine To know more in a few words about Malbine The foundation Art for Help Ursula Malbine was born on the 12th of www.artforhelp.ch April 1917 in Berlin from Jewish-German parents. Both were doctors. Malbine Pré vert park at the “Signal de Bougy” studied cabinetmaker but she found pretty www.signaldebougy.ch early an interest in sculpting, something Malbine she dedicated her life to. Fleeing Nazi Book (with DVD) Germany in 1939 she finds refuge in Slatkine editions Discover Geneva, thanks to Léon Nicole. After a short incursion at the school of fine art, which she can’t stand the guidelines, ’s Malbine quickly finds the teacher who will A woman in sculpture Malbine give her the keys to her art and life, the Association “editions for sculptor Henry Paquet whom she marries creative aging and blue scorpion” sculptures in 1941, becoming a citizen of Geneva and Switzerland. -

Geneva : 45 Communes

Geneva : 45 communes al Aire-la-Ville co Gy am Anières cp Hermance an Avully cq Jussy ao Avusy cr Laconnex ap Bardonnex cs Ville de Lancy aq Bellevue ct Meinier ar Bernex dk Meyrin as Ville de Carouge dl Onex at Cartigny dm Perly Certoux bk Céligny dn Plan-les-Ouates bl Chancy do Pregny Chambesy bm Chêne-Bougeries dp Presinge bn Chêne-Bourg dq Puplinge bo Choulex dr Russin bp Collex-Bossy ds Satigny bq Collonge-Bellerive dt Soral br Cologny ek Thônex bs Confi gnon el Troinex bt Corsier em Vandoeuvres ck Dardagny en Vernier cl Genève eo Versoix cm Genthod ep Veyrier cn Grand-Saconnex IF YOU HAVE DIFFICULTY READING THESE TEXTS, A LARGE FORMAT (A4) VERSION IS AVAILABLE ON : www.ge.ch/integration/publications OR BY CONTACTING THE OFFICE FOR INTEGRATION OF FOREIGNERS, al RUE PIERRE FATIO 15 (4th FLOOR) 1204 GENEVA TEL. 022 546 74 99 www.ge.ch/integration [email protected] 2 WELCOME TO GENEVA - MESSAGE On behalf of the Council of State of the Canton of Geneva and the Association of Geneva Communes (ACG), we extend you a hearty welcome. Geneva has been a place of asylum and refuge for victims of religious persecution since the 16th century, with over a third of its population made up of foreigners. Diversity remains one of the major strengths of Geneva society, in which 194 nationalities are represented today, and solidarity and respect for cultural differences are among the priorities of the political and administrative authorities of both the Canton and the communes of Geneva. -

Cartel Des Sociétés De La Ville De Veyrier

Compte rendu administratif 2018-2019 et financier 2018 Cartel des sociétés de la ville de Veyrier Correspondance : Case postale 137, 1255 Veyrier Local : Avenue du Grand-Salève 8, 1255 Veyrier Président : M. Eric MENETREY, tél. 022 784 34 15 ou 079 306 43 02 E-mail : [email protected] AMICALE DE PÉTANQUE VEYRIER GRAND-DONZEL Président : M. Philippe LAMBELET, chemin du Feuillet 9, 1255 Veyrier, tél. 022 740 32 30 E-mail : [email protected] LES AMIS DU COCHONNET Président : M. Didier PERISSIER, case postale 209, 1255 Veyrier, tél. 079 784 37 58 E-mail : [email protected] ASSOCIATION ANMWE POU AYITI-SECOURS POUR HAÏTI Présidente : Mme Marie-Lourdes DESARDOUIN, chemin du Bois-Gourmand 16, 1234 Vessy, tél. 022 784 35 14 E-mail : [email protected] Site Internet : www.anmwe.ch ASSOCIATION DE PARENTS DE LA COMMUNE DE VEYRIER Correspondance : Case postale 124, 1255 Veyrier Présidence : vacant E-mail : [email protected] Site Internet : www.fapeo.ch/veyrier-pinchat ASSOCIATION DE QUARTIER VEYRIER-RASSES-MARAIS Président : M. Raymond DUCRY, chemin des Rasses 24A, 1255 Veyrier, tél. 079 469 62 20 E-mail : [email protected] ASSOCIATION DES COMMERCANTS DE VEYRIER Président : M. Laurent CHABBEY, route de Vessy 31, 1234 Vessy ASSOCIATION DES INTÉRETS DE PINCHAT Président : M. Jean-Eudes GAUTROT, chemin Sur-Rang 26Bis, 1234 Vessy, tél. 022 301 01 91 E-mail : [email protected] ASSOCIATION DES INTÉRETS DE VESSY Correspondance : Case postale 23, 1234 Vessy Président : M. Max MULLER, route de Veyrier 180 A, 1234 Vessy, tél. 079 541 73 13 E-mail : associationaiv1234@gmailcom Site Internet : www.aiv.ch 1 Compte rendu administratif 2018-2019 et financier 2018 ASSOCIATION ECOLE DE NATATION DE VEYRIER (AENV) Correspondance : Case postale 104, 1255 Veyrier Présidente : Mme Maud ELMALEH Direct. -

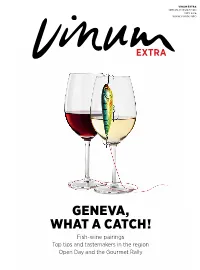

Geneva, What a Catch! Fish-Wine Pairings Top Tips and Tastemakers in the Region Open Day and the Gourmet Rally 04

VINUM EXTRA SPECIAL PUBLICATION MAY 2016 WWW.Vinum.INFO EXTRA GENEVA, WHAT A CATCH! Fish-wine pairings Top tips and tastemakers in the region Open Day and the Gourmet Rally 04 12 08 10 06 Selected highlights from this special issue: our interview with Chandra Kurt, ambassador of the 2015 vintage (page 4); tasting the winners of the Sélection des Vins de Genève contest (page 6); Open Day 2016 (page 8); the Gourmet Rally 2016 (page 10) and our special report on match- ing Geneva wines with fish (page 12 onwards). Read the “Geneva 2016” VINUM Special on your tablet: download the app for free now. Further information: www.vinum.info/ appangebote Contents 04 2015 vintage Editorial Interview with Chandra Kurt, Ambassador for this vintage What a catch! 06 Sélection des Vins de Genève The Sanglier, the Marcassin and the other prize-winners from e often find ourselves marvelling at the dynamism of this constantly- the 2015 awards evolving wine region, and singing the praises of its inimitable local pro- duce, so much so that we occasionally forget just how central the iconic W 08 Open Day lake is to the identity of Romandy’s biggest city. Lake Geneva is the soul of the region, a natural treasure celebrated in all its glory in this special issue. Lake Geneva, or Lac Behind the scenes at a small estate Léman to the French-speaking community, is home to around thirty species of fish and a big winery and shellfish. Unfortunately, perch remains an all too familiar sight on Swiss menus (95% of the fillets consumed in Switzerland are actually imported from Eastern 10 Gourmet Rally 2016 Europe or Africa).