Public Accounts Committee 1960-61

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

District Wise List of Village Having Population of 1600 to 2000 in Jharkhand

District wise list of village having population of 1600 to 2000 in Jharkhand VILLAGE BLOCK DISTRICT Base branch 1 Turio Bermo Bokaro State Bank of India 2 Bandhdih Bermo Bokaro Bank of India 3 Bogla Chandankiyari Bokaro State Bank of India 4 Gorigram Chandankiyari Bokaro State Bank of India 5 Simalkunri Chandankiyari Bokaro State Bank of India 6 Damudi Chandankiyari Bokaro State Bank of India 7 Boryadi Chandankiyari Bokaro State Bank of India 8 Kherabera Chandankiyari Bokaro Bank of India 9 Aluara Chandankiyari Bokaro Bank of India 10 Kelyadag Chandankiyari Bokaro State Bank of India 11 Lanka Chandankiyari Bokaro State Bank of India 12 Jaytara Chas Bokaro Jharkhand Gramin Bank 13 Durgapur Chas Bokaro Bank of India 14 Dumarjor Chas Bokaro Central Bank of India 15 Gopalpur Chas Bokaro Jharkhand Gramin Bank 16 Radhanagar Chas Bokaro Central Bank of India 17 Buribinor Chas Bokaro Bank of India 18 Shilphor Chas Bokaro Bank of India 19 Dumarda Chas Bokaro Central Bank of India 20 Mamar Kudar Chas Bokaro Bank of India 21 Chiksia Chas Bokaro State Bank of India 22 Belanja Chas Bokaro Central Bank of India 23 Amdiha Chas Bokaro Indian Overseas Bank 24 Kalapather Chas Bokaro State Bank of India 25 Jhapro Chas Bokaro Central Bank of India 26 Kamaldi Chas Bokaro State Bank of India 27 Barpokharia Chas Bokaro Bank of India 28 Madhuria Chas Bokaro Canara Bank 29 Jagesar Gomia Bokaro Allahabad Bank Bank 30 Baridari Gomia Bokaro Bank of India 31 Aiyar Gomia Bokaro State Bank of India 32 Pachmo Gomia Bokaro Bank of India 33 Gangpur Gomia Bokaro State -

Mine Closure Report for Govindpur Phase-Ii Open Cast Project (1.2 Mty)

MINE CLOSURE REPORT FOR GOVINDPUR PHASE-II OPEN CAST PROJECT (1.2 MTY) (CENTRAL COALFIELDS LIMITED) AUGUST 2011 Regional Institute – III Central Mine Planning & Design Institute Ltd. (A Subsidiary of Coal India Ltd.) Gondwana Place, Kanke Road Ranchi-834008, Jharkhand 1 INTRODUCTION 1.1 About the Mine Govindpur OCP was worked earlier. Upper Kargali seam was planned and worked under the name of Govindpur OCP. The same report was expanded to include the underlying Bermo seam under the name of Govindpur Expansion OCP. The present Govindpur Ph-II OCP was planned as a new project to extract coal up to the lower most opencastable seam (i.e. Karo-VI seam) including area already worked in Govindpur OCP & Govindpur Expansion OCP. Total leasehold area of Govindpur Ph-II OCP includes both virgin and worked area. The name Govindpur Ph-II is incidental as in Ph-I, the upper seams of Kargali and Bermo have already been worked under the name of Govindpur OCP & Govindpur Expansion OCP (Not as Govindpur Ph-I OCP). History of Mine The PR of this project was prepared as a new project. The report proposed to exploit the upper Karo Group of seams (Seam VI to XI) based on the “Geological Report on Coal Exploration Govindpur North Block, East Bokaro Coalfield” prepared in Dec 2001 and the area south of Bermo Seam incrop upto 180 m depth line on Seam-VI floor in the south, bounded on the east by Mantico Nalla and on the west by Borrea Fault (F7-F7). This is a sector not covered in the geological report of Gobindpur North block (2001), and has now been defined for including additional reserves south of the original limits of Gobindpur North block. -

Pre-Feasibility Report for Integrated Steel Plant of Electrosteel Steels Limited for Production of 3.0MTPA Hot Metal with Blast

2019 PRE-FEASIBILITY REPORT FOR INTEGRATED STEEL PLANT OF ELECTROSTEEL STEELS LIMITED FOR PRODUCTION OF 3.0 MTPA HOT METAL WITH BLAST FURNACE (1×1050 m3, 1×350 m3, 1×1700 m3) ALONG WITH CPP OF CAPACITY 160 MW M/s ELECTROSTEEL STEELS LIMITED (an enterprise of Vedanta Limited) at Siyaljori, Bhagabandh, Budhibinor, Alkusha, Dhandabar, Bandhdih, Hutupathar , Dist Bokaro, Jharkhand -827013 Pre-feasibility Report for Integrated Steel Plant of Electrosteel Steels Limited for production of 3.0MTPA Hot Metal with Blast Furnace (1×1050 m3, 1×350 m3, 1×1700 m3) along with CPP of Capacity 160 MW located at village Siyaljori, Bhagabandh, Budhibinor, Alkusha, Dhandabar, Bandhdih, Hutupathar, Dist Bokaro, Jharkhand-827013 Table of Contents CHAPTER-1............................................................................................................ 7 EXECUTIVE SUMMARY........................................................................................... 7 CHAPTER-2.......................................................................................................... 11 INTRODUCTION OF THE PROJECT......................................................................... 11 2.0 INTRODUCTION ..........................................................................................................11 2.1 IDENTIFICATION OF THE PROJECT & PROJECT PROPONENT.......................................12 2.2 BRIEF DESCRIPTION AND NATURE OF THE PROJECT...................................................13 2.2.1 Chronology of the Project Implementation..........................................................13 -

Environmental Statement of Bokaro Colliery Opencast Project for 2015-16

ENVIRONMENTAL STATEMENT OF BOKARO COLLIERY OPENCAST PROJECT FOR 2015-16 CENTRAL COALFIELDS LIMITED ENVIRONMENT DIVISION CCL,RANCHI Page-2 E X E C U T I V E S U M M A R Y E-1. This Annual Environmental Statement has been prepared as per the Gazette Notification No. G.S.R. 329(E) dated 13 th March’92, the Ministry of Environment & Forests, Government of India. E-2 Bokaro Opencast Project of Central Coalfields Limited is located in the East-Bokaro Coalfields of Bokaro Distt. of Jharkhand state. The mine block is situated on the north of Damodar river after railway line. The total area of the block is about 7 sq.Km.The project location and other surface features are given in the plan annexed as ANNEXURE . E-3 The annual target of production for the year 2015-16 is 70000 Tes. The project has achieved the production during 2015-16 is 84113 Tes. E-4 The Environmental Monitoring was carried out quarterly as per the guide lines of Ministry of Environment & Forest(MOEF).The Environmental Monitoring results for four quarters of 2015-16 are appended as ANNEXURE. E-5 Ambient air quality is monitored to study the level of air pollution. The main air pollutant is suspended particulate matter(SPM).It is difficult to quantity the amount of air pollutants generated due to opencast mining. E-6 Water is not directly used during mining for coal production. It percolates into working area during mining operation. However ,water is consumed for other purposes ,mainly for dust suppression. -

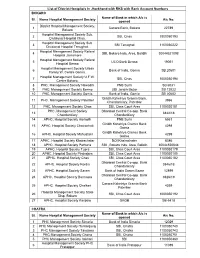

List of District Hostpitals in Jharkhand with RKS with Bank Account Numbers BOKARO Name of Bank in Which A/C Is Sl

List of District Hostpitals In Jharkhand with RKS with Bank Account Numbers BOKARO Name of Bank in which A/c is Sl. Name Hospital Management Society A/c No. opened District Hospital Management Society, 1 Canara Bank, Bokaro 22789 Bokaro Hospital Management Society Sub. 2 SBI, Chas 1000050193 Divisional Hospital Chas. Hospital Management Society Sub. 3 SBI Tenughat 1100050222 Divisional Hospital Tenughat. Hospital Management Society Referal 4 SBI, Bokaro Inds, Area, Balidih 30044521098 Hospital Jainamore Hospital Management Society Referal 5 UCO Bank Bermo 19051 Hospital Bermo Hospital Management Society Urban 6 Bank of India, Gomia SB 20601 Family W. Centre Gomia. Hospital Management Society U.F.W. 7 SBI, Chas 1000050194 Centre Bokaro. 8 PHC. Management Society Nawadih PNB Surhi SB 6531 9 PHC. Management Society Bermo UBI Jaridih Bazar SB 12022 10 PHC. Management Society Gomia Bank of India, Gomia SB 20602 Giridih Kshetriya Gramin Bank, 11 PHC. Management Society Paterber 3966 Chandankiary, Paterbar 12 PHC. Management Society Chas SBI, Chas Court Area 1100020181 PHC. Management Society Dhanbad Central Co-opp. Bank 13 3844/18 Chandankiary Chandankiary 14 APHC. Hospital Society Harladih PNB Surhi 6551 Giridih Kshetriya Gramin Bank 15 APHC. Hospital Society Chatrochati 4298 Goima Giridih Kshetriya Gramin Bank 16 APHC. Hospital Society Mahuatanr 4299 Goima 17 APHC. Hospital Society Khairachatar BOI Khairachater 8386 18 APHC. Hospital Society Pathuria SBI , Bokaro Inds. Area, Balidih 30044520844 19 APHC. Hospital Society Tupra SBI, Chas Court Area 1100050179 20 APHC. Hospital Society Pindrajora SBI, Chas Court Area 1100050180 21 APHC. Hospital Society Chas SBI, Chas Court Area 1100050182 Dhanbad Central Co-opp. -

Government Ofjharkhand Istrict Survey Report for Sand Ing in Bokaro District

GOVERNMENT OFJHARKHAND DISTRICT SURVEY REPORT FOR SAND MINING IN BOKARO DISTRICT, JHARKHAND (As per Notification No.S.O. 3611 (E) New Delhi, 25th July 2018 of Ministry of Environment, Forest and Climate Change) PreparedBy: District Environment Impact Assessment Authority (DEIAA) , Bokaro February, 2019 Sl. No. CONTENTS PAGE NO. 1 Introduction 1-2 2 Overview Of Mining Activity In District 2 List Of Mining Leases In District Bokaro With 3 3-12 Location, Area And Period Of Validity Details Of Royalty Or Revenue Received In Last Three 4 13 Years Details Of Production Of Sand Or Bajari Or Minor 5 13 Mineral In Last Three Years 6 Process Of Deposition Of Sediments In The Rivers 13 -14 7 General Profile Of The District 15 -17 8 Land Utilization Pattern In The District 17 -18 9 Physiography Of The District 19 10 Rainfall: Month Wise 20 11 Geology And Mineral Wealth 21 -22 Detail of rivers or streams and other sand source in the 12 23-26 district 13 River wise Availability of Sand or Gravel or Aggregates 27 -30 Details of Existing Mining Lease of Sand & Aggregates in 14 31-45 Bokaro District 15 Field Photographs 46 -47 16 Conclusion & Recommendations 48 -49 17 Certificate 50 PREFACE In Compliance to the Notification Issued by the Ministry of Environment, Forest And Climate Change Dated 15.01.2016, the preparation of District Survey Report of River bed mining and other minor minerals is in accordance appendix 10 of the notification, it is also mentioned here that the procedure followed for the preparation of District Survey Report is as per the notification, guidelines. -

National Mission for Clean Ganga

NATIONAL MISSION FOR CLEAN GANGA Ministry of Jal Shakti, Department of Water Resources, River Development & Ganga Rejuvenation, Government of India Final Environmental and Social Due Diligence Report CONSTRUCTION OF STP & I&D STRUCTURES IN PHUSRO NAGAR PARISHAD November 2020 LEA ASSOCIATES SOUTH ASIA PVT. LTD. New Delhi, India TABLE OF CONTENTS EXECUTIVE SUMMARY ............................................................................................................................................... 1 1. INTRODUCTION.................................................................................................................................................. 1 1.1 NAMAMI GANGE PROGRAMME ....................................................................................................................... 2 1.2 STRUCTURE OF THE REPORT ............................................................................................................................. 4 2. PROJECT DESCRIPTION ....................................................................................................................................... 5 2.3 ABOUT THE CITY ................................................................................................................................................ 5 2.4 EXISTING SCENARIO OF SEWERAGE FACILITIES IN PHUSRO CITY ...................................................................... 6 2.5 NECESSITY OF THIS PROJECT ............................................................................................................................ -

Directory Establishment

DIRECTORY ESTABLISHMENT SECTOR :RURAL STATE : JHARKHAND DISTRICT : Bokaro Year of start of Employment Sl No Name of Establishment Address / Telephone / Fax / E-mail Operation Class (1) (2) (3) (4) (5) NIC 2004 : 1010-Mining and agglomeration of hard coal 1 PROJECT OFFICE POST OFFICE DISTRICT BOKARO, JHARKHAND , PIN CODE: 829144, STD CODE: NA , TEL NO: NA , FAX 1975 51 - 100 MAKOLI NO: NA, E-MAIL : N.A. 2 CENTRAL COAL FIELD LIMITED AMLO BERMO BOKARO , PIN CODE: 829104, STD CODE: NA , TEL NO: NA , FAX NO: NA, 1972 101 - 500 E-MAIL : N.A. 3 PROJECT OFFICER KHASMAHAL PROJECT VILL. KURPANIA POST SUNDAY BAZAR DISTRICT BOKARO PIN 1972 101 - 500 CODE: 829127, STD CODE: NA , TEL NO: NA , FAX NO: NA, E-MAIL : N.A. 4 SRI I. D. PANDEY A T KARGAL POST . BERMO DISTRICT BOKARO STATE JHARKHAND , PIN CODE: NA , STD CODE: 06549, TEL NO: 1960 > 500 221580, FAX NO: NA, E-MAIL : N.A. 5 SRI S K. BALTHARE AT TARMI DAH DISTRICT BOKARO STATE - JHARKHAND , PIN CODE: NA , STD CODE: NA , TEL NO: NA 1973 > 500 P.O.BHANDARI , FAX NO: NA, E-MAIL : N.A. 6 PROJECT OFFICER CCL MAKOLI POST CE MAKOLI DISTRICT BOKARO STATE JAHARKHAND PIN CODE: 829144, STD CODE: NA , TEL 1975 > 500 OFFFI NO: NA , FAX NO: NA, E-MAIL : N.A. NIC 2004 : 1410-Quarrying of stone, sand and clay 7 SANJAY SINGH VILL KHUTR PO ANTR PS JARIDIH DIST BOKARO JHARKHANDI PIN CODE: 829138, STD CODE: 1989 10 - 50 NA , TEL NO: NA , FAX NO: NA, E-MAIL : N.A. -

Central Coalfields Limited

Central Coalfields Limited Office of the General Manager, B&K Area Area Purchase Cell ; B&K Area Office, Kargali, PO: Bermo, Dist: Bokaro, PIN: 829104 Email: [email protected], Fax: 06549-220938, M: 8987784725 Ref: CCL/B&K/APC/Carbon Brush Holder/LTE/14-15/52 Date:08.01.2015 LIMITED TENDER ENQUIRY (Two-Bid) 1. M/s J.J. Carbon Products, 118P & 119P., New Ancillary Area ,Tupudana, Hatia , Ranchi ‐834003 2. M/s Kisan Enterprises, II‐D/101, Industral Area , Bokaro Steel City 827014 3. M/s Standard Electro System Pvt. Ltd., II‐D/102, Industrial Area Bokaro Steel City 827014 4. M/s Hindustan Facing Industry Pvt. Ltd., 40/5 Gariahat Road (South) Kolkata ‐700031 5. M/s R. Traders , Om Bhawan, PO Dhansar, Dist. Dhanbad828106 Important: Apart from above firms , other firms for the tendered item can also participate if fulfilling the criteria given below. Dear Sirs, Sub : Tender for procurement ofCarbon Brusher &Carbon Brush Holderfor EKG‐5A Shovel of B&K Area Kargali. Submission of Tender In Two‐ Bid System ( Techno –Commercial & Price‐ Bid) Estimated Amount Rs.57298 ( Rs. Fifty Two Thousand Two Hundred Ninety EightOnly) Opening date of sale of Document 13/01/2015 Closing Date of Sale of Document 18/01/2015 Last date of submission of Offer Up to 3.00 PM on 19/01/2015 Due date for opening of Tender At 04.00 PM on 19/01/2015 1. Sealed Tenders are invited for supply of material as indicated in the Schedule of requirement – Annexure “A”. 2.The tender to be submitted in a single envelope containing two separate envelopes properly sealed. -

Pre-Feasibility Study for Coal Mine Methane Recovery and Utilization at the Sawang Colliery, East Bokaro Coal Field, India

U.S. EPA Coalbed Methane OUTREACH PROGRAM Pre-feasibility Study for Coal Mine Methane Recovery at the Sawang Colliery, East Bokaro Coal Field, India U.S. Environmental Protection Agency June 2015 1 Pre-Feasibility Study for Coal Mine Methane Recovery and Utilization at the Sawang Colliery, East Bokaro Coal Field, India Sponsored by: U.S. Environmental Protection Agency, Washington, DC USA Prepared by: Advanced Resources International, Inc. June 2015 Disclaimer This report was prepared for the United States Environmental Protection Agency (USEPA). This analysis uses publicly available information in combination with information obtained through direct contact with mine personnel. USEPA does not: (a) make any warranty or representation, expressed or implied, with respect to the accuracy, completeness, or usefulness of the information contained in this report, or that the use of any apparatus, method, or process disclosed in this report may not infringe upon privately owned rights; (b) assume any liability with respect to the use of, or damages resulting from the use of, any information, apparatus, method, or process disclosed in this report; or (c) imply endorsement of any technology supplier, product, or process mentioned in this report. Acknowledgements This publication was developed at the request of the USEPA, in support of the Global Methane Initiative (GMI). In collaboration with the Coalbed Methane Outreach Program (CMOP), Advanced Resources International, Inc. (ARI) authored this report based on information obtained from the coal -

Bermo Block, Bokaro, Jharkhand)

Water Management Plan (Bermo block, Bokaro, Jharkhand) Details of Assessment Unit State Jharkhand District Bokaro Block/Mandal/Taluka/Firka Bermo Category as per latest GW Over-Exploited Safe/Semi-Critical/ assessment Critical/ OE Hydrogeological Details Average Annual Rainfall 1096.70 mm (Period) Aquifer Sandstone, Shale Major aquifer as per Granite gneiss aquifer Mapping Discharge of Wells lps Dugwells 1 Tubewells - Borewells 0.5 - 5 DCB - Water Quality Fresh Fresh/Saline Any other Quality Issue - Annual Water Availability Fresh water Ground Water (Annual 15.13 Quantum in MCM Availability extractable GW Recharge) Surface water including Yet to receive the Quantum in MCM major water bodies data Grey water Domestic Yet to receive the Quantum in MCM Availability data Industrial Yet to receive the Quantum in MCM data Annual Water Consumption (Ground Water) Agriculture 0.19 Quantum in MCM Domestic 5.49 Quantum in MCM Industrial 18.61 Quantum in MCM Decadal Water consumption - MCM/year trends (Period) (Rise/falling/no change) Common GW Types Dug well/Bore Abstraction well/ TW/DCB etc. Structure Average Depth M bgl Dugwells 10-15 Borewells 50-100 Tubewells - DCB - Future Availability Surface Water Yet to receive the MCM data Ground Water 0.00 Monitoring Surface Water Average inflow Yet to receive the Cusec Monitoring data Average outflow Yet to receive the Cusec data Quality Yet to receive the Potable/Non data potable Ground Water Average DTW Pre-monsoon-4.17 M bgl Monitoring Post-monsoon-3.13 Average Decadal Water Pre-monsoon m/year (Rise/ -

Central Coalfields Limited (April, 2017)

A Mini Ratna Company Summary of Karo Exp OCP (1.5 MTPA) & Proposed Remediation Plan and Natural & Community Resource Augmentation Plan (NCRAP) (As per MoEF&CC notification no S.O. 804 (E) , dated 14 th March, 2017) (Bokaro & Kargali Area) Central Coalfields Limited (April, 2017) Prepared by Regional Institute- III Central Mine Planning & Design Institute Ltd. (A Subsidiary of Coal India Ltd.) Gondwana Place, Kanke Road Ranchi-834008, Jharkhand 1 Index Sl. No. Particulars Page No. 1. Summary of Karo Exp OCP (1.5 MTPA) 3-12 2. Remediation Plan and Natural & Community 13-17 Resource Augmentation Plan (NCRAP) 3. Disclosure of consultants and laboratory 18 4. Plates 19-22 2 Brief Description of Karo OCP 1 Introduction Karo OCP is located in B&K Area of CCL in Bokaro district of Jharkhand. The PR of Karo OCP was approved by CIL Board for a rated capacity of 3.5 MTY in August, 2006. As per approved PR, two quarries were planned having a capacity of 1.5 MTPA for Quarry-I and 2.00 MTPA for Quarry-II. The EC of project was granted for 1.50 MTPA capacity in Quarry-I only (limited to part area having released forest land and non-forest land only) vide letter number J- 11015/544/2009-IA. II(M) dated 24.12.2014 within project area of 226.33 Ha (instead of original area of 570.26 Ha). The Project Report of Karo Expansion OCP (11/15 MTPA) including Quarry-I & II and integrated non-coking coal Karo Washery (7.0 MTPA) was approved by CCL Board on 21.05.2013.