Wolves of Paseo

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Philippine Election ; PDF Copied from The

Senatorial Candidates’ Matrices Philippine Election 2010 Name: Nereus “Neric” O. Acosta Jr. Political Party: Liberal Party Agenda Public Service Professional Record Four Pillar Platform: Environment Representative, 1st District of Bukidnon – 1998-2001, 2001-2004, Livelihood 2004-2007 Justice Provincial Board Member, Bukidnon – 1995-1998 Peace Project Director, Bukidnon Integrated Network of Home Industries, Inc. (BINHI) – 1995 seek more decentralization of power and resources to local Staff Researcher, Committee on International Economic Policy of communities and governments (with corresponding performance Representative Ramon Bagatsing – 1989 audits and accountability mechanisms) Academician, Political Scientist greater fiscal discipline in the management and utilization of resources (budget reform, bureaucratic streamlining for prioritization and improved efficiencies) more effective delivery of basic services by agencies of government. Website: www.nericacosta2010.com TRACK RECORD On Asset Reform and CARPER -supports the claims of the Sumilao farmers to their right to the land under the agrarian reform program -was Project Director of BINHI, a rural development NGO, specifically its project on Grameen Banking or microcredit and livelihood assistance programs for poor women in the Bukidnon countryside called the On Social Services and Safety Barangay Unified Livelihood Investments through Grameen Banking or BULIG Nets -to date, the BULIG project has grown to serve over 7,000 women in 150 barangays or villages in Bukidnon, -

ABS-CBN Investor Presentation Company Overview

Investor Presentation August 2016 UBS Investor Forum HongKong & Singapore 1 ABS-CBN Investor Presentation Company Overview Financial Highlights Industry and Competitive Landscape Summary 2 ABS-CBN Investor Presentation OVERVIEW: Business Segments • Free-to-Air TV and Studio • Global Distribution Operations • Films and Music • Cable Channels / Publishing • Pay TV Pay TV • Internet broadband • Value added services • ABS-CBN mobile – MVNO New • Digital Terrestrial Television Businesses • Kidzania – franchise from Mexico • O Shopping – home TV shopping 3 ABS-CBN Investor Presentation Revenue Mix For the six months ended June 30, 2016 Advertising Revenue Consumer Sales 40% 60% 19% 13% 8% Sky Cable Global Others 4 ABS-CBN Investor Presentation Free-to-Air TV: CH2 and CH23 • Consistent leader in national audience shares and ratings among 13 FTA channels. • Power ratio of 1.3 : 1.0 • ABS-CBN Free-to-air TV advertising revenues: More than 90% of company’s total advertising revenues. 60% FTA market share. TOTAL DAY PRIMETIME AUDIENCE Total SHARE Total PH Mega Metro Mega Metro PH ABS-CBN 2 44 32 35 49 36 40 GMA 7 34 40 34 32 40 35 TV 5 7 7 6 6 7 6 Others 15 21 25 13 17 19 Source: Kantar Media TV Measurement, Total Philippines as of June 30, 2016 Primetime shows contribute 71% of total Channel 2 airtime revenues. 5 ABS-CBN Investor Presentation Digital Terrestrial TV (DTT) • Implementing Rules and Regulations COVERAGE AREA released December 17, 2014. Benguet Pangasinan • Launched February 2015. Tarlac Nueva Ecija • First-mover advantage Pampanga • More than 1.4M boxes sold to date Bulacan Metro Manila (3) • Significantly improved signal in Mega Rizal Manila and Central Luzon Cavite Incremental advertising revenues Laguna Metro Cebu expected from: Davao (new!) . -

Sun Life Foundation Philippines 2018 Annual Report

1 SUN LIFE FOUNDATION ANNUAL REPORT 2018 2 TABLE OF CONTENTS 04 MESSAGES A BRIGHTER WORLD FOR ARTS & CULTURE 04 A Note from the Chairman of the Board 56 Preserving our National Heritage 06 A Note from the President 58 Sulong, OPM! 08 A Note from the Executive Director 60 Weaving Light and Love to the Inabal A BRIGHTER WORLD FOR EDUCATION DISASTER RELIEF 12 Shining on the Beduk Legacy 66 Relief in the Face of Adversity 14 Raising Funds for Education, Diabetes Awareness 16 Helping Scholars Rise for the Future DONOR DRIVEN 18 Rebuilding the Future with 120 Classrooms 70 Transporting Hope with Yellow Boats 22 Nanay Negosyantes Stock up on Skills Opportunities 74 Nourishing the Future of Marawi 24 Forming Better Money Habits among Public School Teachers VOLUNTEERISM 80 Spreading the Light with Back-to-School Kits A BRIGHTER WORLD FOR HEALTH 82 Donating the Gift of Life 28 Embracing the Gift of Childhood 84 Ushering a Brighter Future with Brigada Eskwela 30 Living Healthier Lives with Ideas Positive 87 Coming into a Full Circle of Kindness 32 Nourishing the Next Generation 36 Making Surgeries Safer and More Accessible 92 FINANCIAL STATEMENT A BRIGHTER WORLD FOR THE ENVIRONMENT 98 BOARD OF DIRECTORS 40 Protecting the Beautiful Biodiversity of Sablayan 44 Parking the Heritage & History of the Mighty Pasig River 52 Banking on Progress with Sustainable Eco-Tourism Table of Contents 3 A NOTE FROM THE CHAIRMAN OF THE BOARD “ For though we are a grant-giving Foundation, we want our contribution to be purposeful rather than merely transactional.” What is a lifetime partnership? For the Sun Life Foundation, Because for any intervention to last, our work should it is a commitment we give to our partner organizations, be collective and consistent. -

Subscription Reasons...Y

INDEPENDENT COMMUNICATIONS AUTHORITY OF SOUTH AFRICA APPLICATIONS FOR COMMERCIAL SATELLITE AND CABLE SUBSCRIPTION BROADCASTING LICENCES REASONS FOR DECISIONS NOVEMBER 2007 1 TABLE OF CONTENTS SECTION A: OVERVIEW ..............................................................................................6 1. INTRODUCTION....................................................................................................6 2. BACKGROUND .....................................................................................................6 3. PROCEDURE ........................................................................................................6 4. RELEVANT CRITERIA AND CONSIDERATIONS ...............................................6 5. GENERAL FINDINGS............................................................................................6 5.5. Corporate Status ....................................................................................................6 5.6. Ownership and control restrictions ........................................................................6 5.9. Management and experience ................................................................................6 5.10. Staffing ...........................................................................................................6 5.11. Finance...........................................................................................................6 5.12. Research – demand and need .....................................................................6 -

Y 0 U BELONG

W H E R E y 0 u BELONG THE MARKET a static-marred AM radio station called DZBB. This small radio station, now an institution in AM Television reached Philippine shores in 1953 radio, became the flagship of RBS as it ventured and since then, it has become a highly popular into television ten years later via TV Channel 7. medium for information and entertainment. Be In 1974, Stewart gave way to the new man ing the primary source of entertainment &: in· agement triumvirate composed of Felipe Gozon, formation, television has found its way into ma· Gilberto Duavit, and Menardo Jimenez. From a jority of Philippine homes. black-and-white (B&W) station whose only claim For over 12.7 million television households to fame were Popeye reruns and scratched vid in the Philippines, one brand stands out when it eos of "Combat", Channel 7 set the trend by in comes to responsible, balanced, innovative and troducing new equipment, new technology and award-winning television programming· GMA new programming. Network, Inc. (GMA TV Channel 7). With its introduction of popular mini-series GMA presently blankets over 93% of the Phil from the U.S., Channel 7 became the new home ippine archipelago with its 44 originating and of quality programming. With a broader audi relay stations nationwide.lt also operates a rap ence base and a new image, Channel 7 was re idly growing radio network of 32 stations named GMA (Greater Manila Area) which sym· throughout the country. bolized its expanded reach and power. Locally and internationally, GMA's potential These programming innovations were sup market is expanding. -

GMA Films, Inc., Likewise Contributed to the Increase Our Company

Aiming Higher About our cover In 2008, GMA Network, Inc. inaugurated the GMA Network Studios, the most technologically-advanced studio facility in the country. It is a testament to our commitment to enrich the lives of Filipinos everywhere with superior entertainment and the responsible delivery of news and information. The 2008 Annual Report’s theme, “Aiming Higher,” is our commitment to our shareholders that will enable us to give significant returns on their investments. 3 Purpose/Vision/Values 4 Aiming Higher the Chairman’s Message 8 Report on Operations by the EVP and COO 13 Profile of the Business 19 Corporate Governance 22 A Triumphant 2008 32 GMA Network Studios 34 Corporate Social Responsibility 38 A Rewarding 2008 41 Executive Profile 50 Contact Information 55 Financial Statements GMA ended 2008 awash with cash amounting to P1.688 billion and free of debt, which enabled us to upgrade our regional facilities, complete our new building housing state-of-the-art studios and further expand our international operations. AIMING HIGHER THE CHAIRMAN’S MESSAGE Dear Fellow Shareholders: The year 2008 will be remembered for the Our efforts in keeping in step with financial crisis that started in the United States and its domino-effect on the rest of the world. The the rest of the world will further Philippine economy was not spared, and for the first time in seven years, gross domestic product improve our ratings and widen our (GDP) slowed down to 4.6%. High inflation, high reach as our superior programs will oil prices and the deepening global financial crisis in the fourth quarter caused many investors serious be better seen and appreciated by concerns. -

Wet-Weather Family Bonding Levels up with Kidzania, Partners…Page 3

AUGUST 2015 www.lopezlink.ph At the Lopez Museum. See story on page 9. http://www.facebook.com/lopezlinkonline www.twitter.com/lopezlinkph Let’s gear up for the Big One THE Big One, they call it, the magnitude 7.2 earthquake generated by the West Valley Fault that could leave more than 30,000 people dead and about 148,000 injured as homes and office buildings collapse all over Metro Manila and parts of Luzon. Turn to page 6 PHOTO SOURCE: http://files.umwblogs.org/blogs.dir/3114/files/2013/04/MadsNissen_Rampen144.jpg Family bonding Jana Agoncillo levels up with is back as Wet-weather …page 12 KidZania, partners…page 3 Ningning …page 4 busters Lopezlink August 2015 Biz News Biz News Lopezlink August 2015 ABS-CBN, Asian Eye win Reader’s CSC bares secret Digest Trusted Brand awards anew ABS-CBN Corporation was of approval named most trusted Philip- v a l i d a t e s behind success of pine TV network for the fifth not only the time while Asian Eye Institute quality of received its third most trusted our services eye center award at the annual but also the ABS-CBN programs Reader’s Digest Trusted Brand confidence Awards 2015 organized by of the con- WHAT is ABS-CBN’s secret My Heart” hugely successful. SKY Cable COO Ray Montinola (4th from left) and Play Innovations Inc. president Maricel Pangilinan-Arenas Reader’s Digest Asia-Pacific. sumers in formula behind its successful Santos-Concio also said (3rd from left) do the KidZania pose with (l-r) SKY Cable Marketing head Alan Supnet, CFO Eloisa Balmoris, Play The Kapamilya network our brand. -

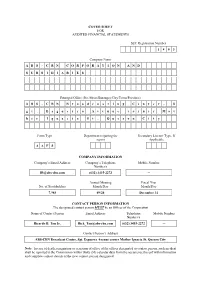

COVER SHEET for AUDITED FINANCIAL STATEMENTS SEC Registration Number 1 8 0 3 Company Name A

COVER SHEET FOR AUDITED FINANCIAL STATEMENTS SEC Registration Number 1 8 0 3 Company Name A B S - C B N C O R P O R A T I O N A N D S U B S I D I A R I E S Principal Office (No./Street/Barangay/City/Town/Province) A B S - C B N B r o a d c a s t i n g C e n t e r , S g t . E s g u e r r a A v e n u e c o r n e r M o t h e r I g n a c i a S t . Q u e z o n C i t y Form Type Department requiring the Secondary License Type, If report Applicable A A F S COMPANY INFORMATION Company’s Email Address Company’s Telephone Mobile Number Number/s [email protected] (632) 3415-2272 ─ Annual Meeting Fiscal Year No. of Stockholders Month/Day Month/Day 7,985 09/24 December 31 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Mobile Number Number/s Ricardo B. Tan Jr. [email protected] (632) 3415-2272 ─ Contact Person’s Address ABS-CBN Broadcast Center, Sgt. Esguerra Avenue corner Mother Ignacia St. Quezon City Note: In case of death, resignation or cessation of office of the officer designated as contact person, such incident shall be reported to the Commission within thirty (30) calendar days from the occurrence thereof with information and complete contact details of the new contact person designated. -

Mapping Online Child Safety in Asia-Pacific Acknowledgments

July 2017 Mapping Online Child Safety in Asia-Pacific Acknowledgments This report is the outcome of a three-month research fellowship programme supported by Google. Research for the report, as well as the initial draft, was done by Jee Eun Choi. The report was revised by Noelle Francesca de Guzman and Rajnesh Singh, and was edited by Christine Apikul. Internet Society – APAC Bureau 9 Temasek Boulevard #09-01 Suntec Tower 2 Singapore 038989 Tel: +65 6407 1470 Fax: +65 6407 1501 Email: [email protected] www.internetsociety.org Follow us on Twitter @ISOCapac Follow us on Scoopt.it! http://www.scoop.it/t/internet-in-asia-pacific internetsociety.org @internetsociety 2 Executive Summary In today’s age, the Internet has become essential for developing and strengthening the capacities of children. But at the same time, use of the Internet can come with some risks for young Internet users. It can create new challenges with regards to their safety and protection - both in the physical and virtual worlds. However, quick-fix interventions that limit children’s online access tend to result in a loss of opportunity for them to take advantage of the benefits of the Internet. There is limited research on child online safety in Asia-Pacific --this report outlines some of the resources that are currently available. It provides an overview of initiatives, focusing on policies that are in place to tackle child online safety in selected economies in the region, and an introduction to the different actors involved in addressing the various risks that children can face online. -

Philippines in View Philippines Tv Industry-In-View

PHILIPPINES IN VIEW PHILIPPINES TV INDUSTRY-IN-VIEW Table of Contents PREFACE ................................................................................................................................................................ 5 1. EXECUTIVE SUMMARY ................................................................................................................................... 6 1.1. MARKET OVERVIEW .......................................................................................................................................... 6 1.2. PAY-TV MARKET ESTIMATES ............................................................................................................................... 6 1.3. PAY-TV OPERATORS .......................................................................................................................................... 6 1.4. PAY-TV AVERAGE REVENUE PER USER (ARPU) ...................................................................................................... 7 1.5. PAY-TV CONTENT AND PROGRAMMING ................................................................................................................ 7 1.6. ADOPTION OF DTT, OTT AND VIDEO-ON-DEMAND PLATFORMS ............................................................................... 7 1.7. PIRACY AND UNAUTHORIZED DISTRIBUTION ........................................................................................................... 8 1.8. REGULATORY ENVIRONMENT .............................................................................................................................. -

Us East Time (St)

JULY 2012 NORTH AMERICA MONDAY TUESDAY WEDNESDAY THURSDAY FRIDAY SATURDAY SUNDAY JULY 9 JULY 10 JULY 11 JULY 12 JULY 13 JUL Y 7 JULY 8 ET ET 12 A RATED K (11:25-12:15) MAALAALA MO KAYA 12 A X-FACTOR WALANG HANGGAN (R) (11:55-12:35) (R) (11:30-12:30) PHILIPPINES X-FACTOR SUNDAY KAHIT PUSO’Y MASUGATAN (12:35-1:10) PHILIPPINES 1 (12:15-1:15) SATURDAY 1 GANDANG GABI VICE KUNG AKO’Y IIWAN MO (R) (1:10-1:40) (12:30-1:30) (1:15-2:00) BANANA SPLIT 2 PHR: HIYAS (1:40-2:20) JUNE 30 EP. (R) 2 THE WAY (1:30-2:30) YOU LOOK BANDILA (2:20-3:05) AT ME BOTTOMLINE 3 (2:30-3:30) 3 (2:00-3:40) XXX GAPLESS PATROL NG PILIPINO AKO ANG SIMULA KRUSADA SOCO (3:05-3:45) (3:05-3:45) (3:05-3:45) (3:05-3:45) (3:05-3:45) STORYLINE 4 BALITANG AMERICA (R)(3:45-4:15) (3:30-4:10) 4 ASAP (R) STORYLINE (R) SALAMAT DOK SAT BOTTOMLINE (R) SALAMAT DOK SUN RATED K (R2) CITIZEN PINOY (4:15-5:05) (R)(4:15-5:05) (4:15-5:05) (R)(4:15-5:05) (4:15-5:05) 5 (3:40-5:45) (R)(4:10-5:10) 5 PATROL NG PILIPINO KRIS TV (R) (5:05-6:00) (R) (5:10-5:50) 6 ADOBO NATION KRUSADA (R) 6 (R)(5:45-6:45) (5:50-6:30) FAILON NGAYON TODA MAX (R) (6:30-6:55) 7 JUNE 30 EP. -

Real Life Revisited on GMA Life TV to Be a Winner in This Adventure Sport

The ratings are out and the results are astoundingly clear-your GMA’s newly-launched primetime series Iglot starred by Claudine Kapuso Network GMA 7 leads the way among local channels once Barretto and new child star Milkcah Wynne Nacion delivers an again in the race towards the topmost spot! impressive debut performance vis-à-vis the competition’s 100 Days to Heaven. Respected and recognized ratings service provider Nielsen TV Audience Measurement recently came out with the August data (August 28 to 31 based on overnight ratings), and the outcome Afternoon Wins In the afternoon block (12nn to 6pm), GMA maintained its edge favors GMA by a 4.1 point margin over its longtime rival ABS-CBN, over ABS-CBN nationwide. The recently launched Pahiram ng which has a 30.9 standing. Meanwhile, despite its aggressive Isang Ina, billed by Carmina Villarroel, Bea Binene, Jake Vargas, marketing, TV5 capped off the month with 16.1 share points. and Maxene Magalona, upheld the winning performance made by Kylie Padilla’s Blusang Itim. Let the Numbers Talk The lead of 4.1 points means that GMA had almost 155,000 more Overall, for the month of August, GMA’s afternoon programs TV households from all over the country watching its shows. scored 41.5 household share points nationwide, ahead of ABS- Using an assumption of five viewers per household, the lead CBN’s 24.8, and TV5’s 15.4. would translate to GMA having about 774,000 more viewers over ABS-CBN. Compared to TV5, GMA had about 709,000 more TV The gap of 16.7 points over ABS-CBN means that more than households or an estimated advantage of roughly 3.5 million more 634,000 households and more than 3.1million more viewers viewers.