(SAARC) Energy Centre (SEC) Islamabad, Pakistan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2016 Buick Lacrosse Owner Manual

2k16_CS6_Buick_Lacrosse_23180150C.ai 1 2/9/2016 9:49:19 AM C M Y CM MY CY CMY K 23180150 C Buick LaCrosse Owner Manual (GMNA-Localizing-U.S./Canada/Mexico- 9159288) - 2016 - CRC - 10/5/15 Contents Introduction . 2 In Brief . 5 Keys, Doors, and Windows . 26 Seats and Restraints . 49 Storage . 97 Instruments and Controls . 100 Lighting . 148 Infotainment System . 156 Climate Controls . 157 Driving and Operating . 163 Vehicle Care . 226 Service and Maintenance . 313 Technical Data . 326 Customer Information . 330 Reporting Safety Defects . 341 OnStar . 345 Index . 355 Buick LaCrosse Owner Manual (GMNA-Localizing-U.S./Canada/Mexico- 9159288) - 2016 - CRC - 2/3/16 2 Introduction Introduction This manual describes features that Helm, Incorporated may or may not be on the vehicle Attention: Customer Service because of optional equipment that 47911 Halyard Drive was not purchased on the vehicle, Plymouth, MI 48170 model variants, country USA specifications, features/applications that may not be available in your Using this Manual region, or changes subsequent to the printing of this owner manual. To quickly locate information about the vehicle, use the Index in the The names, logos, emblems, Refer to the purchase back of the manual. It is an slogans, vehicle model names, and documentation relating to your alphabetical list of what is in the vehicle body designs appearing in specific vehicle to confirm the manual and the page number where this manual including, but not limited features. it can be found. to, GM, the GM logo, BUICK, the BUICK Emblem, and LACROSSE Keep this manual in the vehicle for are trademarks and/or service quick reference. -

Poland Regional Cities-Comfort-Vehicle-List

Make Model Year Oldsmobile 19 Oldsmobile Alero Oldsmobile Aurora Oldsmobile Bravada Oldsmobile Cutlass Supreme Oldsmobile Intrigue Oldsmobile Silhouette Dodge Attitude Dodge Avenger 2013 Dodge Caliber Dodge Caravan 2015 Dodge Challenger Dodge Charger 2013 Dodge Dakota Dodge Dart 2015 Dodge Durango 2013 Dodge Grand Caravan 2015 Dodge Intrepid Dodge JCUV Dodge Journey 2013 Dodge Magnum 2013 Dodge Neon 2015 Dodge Nitro 2013 Dodge Ram 1500 Dodge Ram 2500 Dodge Ram 3500 Dodge Ram 4500 Dodge Ram 700 Dodge Ram Van 2015 Dodge Sprinter Dodge Stratus 2015 Dodge Stretch Limo Dodge Viper Dodge Vision Dodge i10 Land Rover Defender 2013 Land Rover Discovery 2013 Land Rover Freelander 2013 Land Rover Freelander 2 Land Rover LR2 Land Rover LR3 Land Rover LR4 Land Rover Range Rover 2013 Land Rover Range Rover Evoque 2013 Land Rover Range Rover Sport 2013 Land Rover Range Rover Velar 2013 Land Rover Range Rover Vogue 2013 Chevrolet Agile Chevrolet Astra 2015 Chevrolet Astro Chevrolet Avalanche 2013 Chevrolet Aveo Chevrolet Aveo5 Chevrolet Beat Chevrolet Blazer Chevrolet Bolt Chevrolet CMV Chevrolet Camaro Chevrolet Caprice Chevrolet Captiva 2013 Chevrolet Cavalier Chevrolet Celta Chevrolet Chevy Chevrolet City Express Chevrolet Classic Chevrolet Cobalt 2015 Chevrolet Colorado Chevrolet Corsa Chevrolet Corsa Sedan Chevrolet Corsa Wagon Chevrolet Corvette Chevrolet Corvette ZR1 Chevrolet Cruze 2015 Chevrolet Cruze Sport6 Chevrolet Dmax Chevrolet Enjoy Chevrolet Epica 2013 Chevrolet Equinox 2013 Chevrolet Esteem Chevrolet Evanda 2013 Chevrolet Exclusive Chevrolet -

Mv680491 Arizona Department of Transportation Mv579d Motor Vehicle Division 1801 West Jefferson Phoenix, Arizona 85001 May 2011

MV680491 ARIZONA DEPARTMENT OF TRANSPORTATION MV579D MOTOR VEHICLE DIVISION 1801 WEST JEFFERSON PHOENIX, ARIZONA 85001 MAY 2011 2011 LICENSED AUTOMOTIVE RECYCLER -- AR BROKER -- B DISTRIBUTOR -- DS MOBILE HOME DEALER FOR PLATES ONLY -- M MANUFACTURER -- MF NEW MOTOR VEHICLE DEALER -- N TITLE SERVICE COMPANY -- TS USED MOTOR VEHICLE DEALER -- U WHOLESALE AUCTION DEALER -- WA WHOLESALE MOTOR VEHICLE DEALER -- WD - 1- LICENSE DEALERSHIP NAME AND ADDRESS PHONE NO EXP DATE PRODUCTS AUTHORIZED TO SELL _______ ___________________________ ________ __________ ___________________________ ------ AR ------ L00000021 A A A 20TH STREET AUTO WRECKING INC 6022582020 12/31/2011 (AR112) 3244 S 40TH ST PHOENIX AZ 850401623 L00000057 A A NATIONAL TOWING AUTO PARTS 6022725331 12/31/2011 (AR165) 3410 W WASHINGTON ST PHOENIX AZ 850094705 P O BOX 42321 PHOENIX AZ 85080 L00000175 A AND S AUTO WRECKING 6022439119 12/31/2011 (AR458) 2449 W BROADWAY RD PHOENIX AZ 850412003 L00000125 A C S AUTO WRECKING ** DBA: MUNCHINO INVESTMENT INC L00000302 A TO Z AUTO RECYCLER 6022721680 12/31/2011 (AR595) 2724 W BUCKEYE RD PHOENIX AZ 850095742 L00010226 A-Z QUALITY AUTO AND TRUCK PARTS LLC 6022684558 03/31/2012 2149 W BROADWAY RD # 2 PHOENIX AZ 850412107 L00010579 A-1 TRUCK AND VAN WRECKING 4809830511 12/31/2011 1708 S TOMAHAWK RD APACHE JUNCTION AZ 851197780 7325 E NOPAL AVE MESA AZ 85209 L00008372 AA AUTO PARTS ** DBA: G S FUTURES LLC - 2- LICENSE DEALERSHIP NAME AND ADDRESS PHONE NO EXP DATE PRODUCTS AUTHORIZED TO SELL _______ ___________________________ ________ __________ -

Electric Vehicle Infrastructure for the Monterey Bay Area the Associa� on of Monterey Bay Area Governments August 2013

E V Electric Vehicle Infrastructure for the Monterey Bay Area The Associa on of Monterey Bay Area Governments August 2013 The prepara on of this document was funded by a grant awarded by the Monterey Bay Unifi ed Air Pollu on Control District (MUAPCD), as part of the AB2766 program. Project Staff Alan Romero, Monterey Bay Unifi ed Air Pollu on Control District (MBUAPCD) AMBAG Dawn Mathes, Monterey County Resource Management Agency (RMA) Paul Hierling, Planner Carl P. Holm, Monterey County RMA Cody Meyer, Planner Craig Spencer, Monterey County RMA Anais Schenk, Planner Mario Salazar, Monterey County RMA Jason Adelaars, GIS Michael Ricker, City of Salinas Ecology Ac on Veronica Lezama, San Benito Council of Piet Canin, Vice President, Transporta on Governments Group Tegan Speiser, Santa Cruz County RTC Emily Glanville, Program Specialist Michael Zeller, TAMC Monterey Bay Unifi ed Air James Wasserman, Zero Motorcycles, Plug- Pollu on Control District In America Alan Romero, Air Quality Planner III Megan Tolbert, CSU Monterey Bay EV Communi es Alliance Piet Canin, Ecology Ac on Richard Corcoran, PEV Owner Richard Schorske, CEO Teresa Buika, UC Santa Cruz Previous staff contributors Richard Schorske, EV Communi es Alliance John Doughty Randy Deshazo, Principal Planner Linda Meckel, Planner, Project Manager MBEVA Plug-In Electric Vehicle Coordina ng Council Sharon Sarris, Green Fuse Energy Kris Markey, Offi ce of Monterey County Supervisor Parker Andy Hartmann, Interna onal Brotherhood of Electrical Workers Cheryl Schmi , City of Santa Cruz For more informa on regarding this study, contact Anais Schenk at [email protected] 2 E V Electric Vehicle Infrastructure for the Monterey Bay Area Execu ve Summary.............................................................................................................................................. -

U.S. Department of Transportation Federal Motor Carrier Safety Administration REGISTER

U.S. Department of Transportation Federal Motor Carrier Safety Administration REGISTER A Daily Summary of Motor Carrier Applications and of Decisions and Notices Issued by the Federal Motor Carrier Safety Administration DECISIONS AND NOTICES RELEASED May 25, 2021 -- 10:30 AM NOTICE Please note the timeframe required to revoke a motor carrier's operating authority for failing to have sufficient levels of insurance on file is a 33 day process. The process will only allow a carrier to hold operating authority without insurance reflected on our Licensing and Insurance database for up to three (3) days. Revocation decisions will be tied to our enforcement program which will focus on the operations of uninsured carriers. This process will further ensure that the public is adequately protected in case of a motor carrier crash. Accordingly, we are adopting the following procedure for revocation of authority; 1) The first notice will go out three (3) days after FMCSA receives notification from the insurance company that the carrier's policy will be cancelled in 30 days. This notification informs the carrier that it must provide evidence that it is in full compliance with FMCSA's insurance regulations within 30 days. 2) If the carrier has not complied with FMCSA's insurance requirements after 30 days, a final decision revoking the operating authority will be issued. NAME CHANGES NUMBER TITLE DECIDED MC-1008252 FJ EXPRESS INC - ELK GROVE, CA 05/20/2021 MC-1021969 SUPREME LOGISTICS SERVICES LLC - IRVING, TX 05/20/2021 MC-1094340 NOOR & NAAZ PABLA -

Download the Carlisle ELECTRICAL & WIRING TREASURED MOTORCAR SERVICES RED BEARDS TOOLS Events App for Iphone and L 195-198, M 196-199 Android

OFFICIAL EVENT GUIDE Contents WORLD’S FINEST CAR SHOWS & AUTOMOTIVE EVENTS 5 WELCOME 7 FORD MOTOR COMPANY 9 SPECIAL GUESTS 10 EVENT HIGHLIGHTS 15 WOMEN’S OASIS 2019-2020 EVENT SCHEDULE 17 NPD SHOWFIELD HIGHLIGHTS JAN. 18-20, 2019 FEATURED VEHICLE DISPLAYS: AUTO MANIA 19 FORD GT PROTOTYPE ALLENTOWN PA FAIRGROUNDS JAN. 17-19, 2020 FEATURED VEHICLE DISPLAY: FEB. 22-24, 2019 21 FORD NATIONALS SELECT WINTER AUTOFEST LAKELAND SUN ’n FUN, LAKELAND, FL FEB. 21-23, 2020 FEATURED VEHICLE DISPLAY: 22 40 YEARS OF THE FOX BODY LAKELAND WINTER FEB. 22-23, 2019 COLLECTOR CAR AUCTION FEATURED VEHICLE DISPLAY: SUN ’n FUN, LAKELAND, FL FEB. 21-22, 2020 25 50 YEARS OF THE MACH 1 APRIL 24-28, 2019 FEATURED VEHICLE DISPLAY: SPRING CARLISLE CARLISLE PA FAIRGROUNDS 26 50 YEARS OF THE BOSS APRIL 22-26, 2020 FEATURED VEHICLE DISPLAY: SPRING CARLISLE APRIL 25-26, 2019 29 50 YEARS OF THE ELIMINATOR COLLECTOR CAR AUCTION CARLISLE EXPO CENTER APRIL 23-24, 2020 29 SOCIAL STOPS IMPORT & PERFORMANCE MAY 17-19, 2019 EVENT MAP NATIONALS 20 CARLISLE PA FAIRGROUNDS MAY 15-17, 2020 19 EVENT SCHEDULE FORD NATIONALS MAY 31-JUNE 2, 2019 PRESENTED BY MEGUIAR’S 34 GUEST SPOTLIGHT CARLISLE PA FAIRGROUNDS JUNE 5-7, 2020 37 SUMMER OF ’69 CHEVROLET NATIONALS JUNE 21-22, 2019 CARLISLE PA FAIRGROUNDS 39 VENDORS: BY SPECIALTY JUNE 26-27, 2020 CARLISLE AUCTIONS JUNE 22, 2019 43 VENDORS: A-Z SUMMER SALE CARLISLE EXPO CENTER JUNE 27, 2020 48 ABOUT OUR PARTNERS JULY 12-14, 2019 CARLISLE FAIRGROUNDS CHRYSLER NATIONALS 51 POLICIES & INFORMATION CARLISLE PA FAIRGROUNDS JULY 10-12, 2020 53 CONCESSIONS TRUCK NATIONALS AUG. -

Download Paper

Charging the Future: Challenges and Opportunities for Electric Vehicle Adoption Faculty Research Working Paper Series Henry Lee Harvard Kennedy School Alex Clark Climate Policy Initiative September 2018 RWP18-026 Visit the HKS Faculty Research Working Paper Series at: https://www.hks.harvard.edu/research-insights/publications?f%5B0%5D=publication_types%3A121 The views expressed in the HKS Faculty Research Working Paper Series are those of the author(s) and do not necessarily reflect those of the John F. Kennedy School of Government or of Harvard University. Faculty Research Working Papers have not undergone formal review and approval. Such papers are included in this series to elicit feedback and to encourage debate on important public policy challenges. Copyright belongs to the author(s). Papers may be downloaded for personal use only. www.hks.harvard.edu ENVIRONMENT AND NATURAL RESOURCES Charging the Future Challenges and Opportunities for Electric Vehicle Adoption Henry Lee Alex Clark PAPER AUGUST 2018 Environment and Natural Resources Program Belfer Center for Science and International Affairs Harvard Kennedy School 79 JFK Street Cambridge, MA 02138 www.belfercenter.org/ENRP The authors of this report invites use of this information for educational purposes, requiring only that the reproduced material clearly cite the full source: Lee, Henry, and Alex Clark, “Charging the Future: Challenges and Opportunities for Electric Vehicle Adoption.” Belfer Center for Science and International Affairs, Cambridge, Mass: Harvard University, August 2018. Statements and views expressed in this report are solely those of the authors and do not imply endorsement by Harvard University, the Harvard Kennedy School, or the Belfer Center for Science and International Affairs. -

Electric and Hybrid Cars SECOND EDITION This Page Intentionally Left Blank Electric and Hybrid Cars a History

Electric and Hybrid Cars SECOND EDITION This page intentionally left blank Electric and Hybrid Cars A History Second Edition CURTIS D. ANDERSON and JUDY ANDERSON McFarland & Company, Inc., Publishers Jefferson, North Carolina, and London LIBRARY OF CONGRESS CATALOGUING-IN-PUBLICATION DATA Anderson, Curtis D. (Curtis Darrel), 1947– Electric and hybrid cars : a history / Curtis D. Anderson and Judy Anderson.—2nd ed. p. cm. Includes bibliographical references and index. ISBN 978-0-7864-3301-8 softcover : 50# alkaline paper 1. Electric automobiles. 2. Hybrid electric cars. I. Anderson, Judy, 1946– II. Title. TL220.A53 2010 629.22'93—dc22 2010004216 British Library cataloguing data are available ©2010 Curtis D. Anderson. All rights reserved No part of this book may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying or recording, or by any information storage and retrieval system, without permission in writing from the publisher. On the cover: (clockwise from top left) Cutaway of hybrid vehicle (©20¡0 Scott Maxwell/LuMaxArt); ¡892 William Morrison Electric Wagon; 20¡0 Honda Insight; diagram of controller circuits of a recharging motor, ¡900 Manufactured in the United States of America McFarland & Company, Inc., Publishers Box 611, Je›erson, North Carolina 28640 www.mcfarlandpub.com To my family, in gratitude for making car trips such a happy time. (J.A.A.) This page intentionally left blank TABLE OF CONTENTS Acronyms and Initialisms ix Preface 1 Introduction: The Birth of the Automobile Industry 3 1. The Evolution of the Electric Vehicle 21 2. Politics 60 3. Environment 106 4. Technology 138 5. -

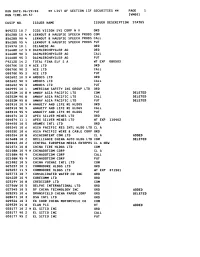

LIST of SECTION 13F SECURITIES ** PAGE 1 RUN TIME:09:57 Ivmool

RUN DATE:06/29/00 ** LIST OF SECTION 13F SECURITIES ** PAGE 1 RUN TIME:09:57 IVMOOl CUSIP NO. ISSUER NAME ISSUER DESCRIPTION STATUS B49233 10 7 ICOS VISION SYS CORP N V ORD B5628B 10 4 * LERNOUT & HAUSPIE SPEECH PRODS COM B5628B 90 4 LERNOUT & HAUSPIE SPEECH PRODS CALL B5628B 95 4 LERNOUT 8 HAUSPIE SPEECH PRODS PUT D1497A 10 1 CELANESE AG ORD D1668R 12 3 * DAIMLERCHRYSLER AG ORD D1668R 90 3 DAIMLERCHRYSLER AG CALL D1668R 95 3 DAIMLERCHRYSLER AG PUT F9212D 14 2 TOTAL FINA ELF S A WT EXP 080503 G0070K 10 3 * ACE LTD ORD G0070K 90 3 ACE LTD CALL G0070K 95 3 ACE LTD PUT GO2602 10 3 * AMDOCS LTD ORD GO2602 90 3 AMDOCS LTD CALL GO2602 95 3 AMDOCS LTD PUT GO2995 10 1 AMERICAN SAFETY INS GROUP LTD ORD G0352M 10 8 * AMWAY ASIA PACIFIC LTD COM DELETED G0352M 90 8 AMWAY ASIA PACIFIC LTD CALL DELETED G0352M 95 8 AMWAY ASIA PACIFIC LTD PUT DELETED GO3910 10 9 * ANNUITY AND LIFE RE HLDGS ORD GO3910 90 9 ANNUITY AND LIFE RE HLDGS CALL GO3910 95 9 ANNUITY AND LIFE RE HLDGS PUT GO4074 10 3 APEX SILVER MINES LTD ORD GO4074 11 1 APEX SILVER MINES LTD WT EXP 110402 GO4450 10 5 ARAMEX INTL LTD ORD GO5345 10 6 ASIA PACIFIC RES INTL HLDG LTD CL A G0535E 10 6 ASIA PACIFIC WIRE & CABLE CORP ORD GO5354 10 8 ASIACONTENT COM LTD CL A ADDED G1368B 10 2 BRILLIANCE CHINA AUTO HLDG LTD COM DELETED 620045 20 2 CENTRAL EUROPEAN MEDIA ENTRPRS CL A NEW G2107X 10 8 CHINA TIRE HLDGS LTD COM G2108N 10 9 * CHINADOTCOM CORP CL A G2108N 90 9 CHINADOTCOM CORP CALL G2lO8N 95 9 CHINADOTCOM CORP PUT 621082 10 5 CHINA YUCHAI INTL LTD COM 623257 10 1 COMMODORE HLDGS LTD ORD 623257 11 -

Plug-In Hybrid Electric Vehicle Value Proposition Study

DOCUMENT AVAILABILITY Reports produced after January 1, 1996, are generally available free via the U.S. Department of Energy (DOE) Information Bridge: Web site: http://www.osti.gov/bridge Reports produced before January 1, 1996, may be purchased by members of the public from the following source: National Technical Information Service 5285 Port Royal Road Springfield, VA 22161 Telephone: 703-605-6000 (1-800-553-6847) TDD: 703-487-4639 Fax: 703-605-6900 E-mail: [email protected] Web site: http://www.ntis.gov/support/ordernowabout.htm Reports are available to DOE employees, DOE contractors, Energy Technology Data Exchange (ETDE) representatives, and International Nuclear Information System (INIS) representatives from the following source: Office of Scientific and Technical Information P.O. Box 62 Oak Ridge, TN 37831 Telephone: 865-576-8401 Fax: 865-576-5728 E-mail: [email protected] Web site: http://www.osti.gov/contact.html This report was prepared as an account of work sponsored by an agency of the United States Government. Neither the United States government nor any agency thereof, nor any of their employees, makes any warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of any information, apparatus, product, or process disclosed, or represents that its use would not infringe privately owned rights. Reference herein to any specific commercial product, process, or service by trade name, trademark, manufacturer, or otherwise, does not necessarily constitute or imply its endorsement, recommendation, or favoring by the United States Government or any agency thereof. The views and opinions of authors expressed herein do not necessarily state or reflect those of the United States Government or any agency thereof. -

Supervisors Study Office Space Need

Do~for Begins lnlerns~ip AI Lansing Sf. Lawrence MnHon;s nr.wcst doctor of medl · clnn, Dr, Milton c. l:lcrgeon, br! gins his lntcrn~hlp nl Sl. Law 4 Sections ~ 2,6 Pc1gos l'oncc hospltnl In Lansing .Tuly 1 Dr. Bcrgcon rcm!IV!!cl hi~ de grcc of doctor of mcdlclrm at thr Bank P.roperty University of Michigan Snl!rruny Cash Is Left On Monday ami Tuesday am. Offers New View Wcdnesrlny of lust wcelc he wr·otr Supervisors Study his stale hrmrrl exnmlnatlnns nnr' On· Soil Plan There's a new view In Mason has qunlllled to practice rnodlclnc now that the .3 buildings on the ' The new doctor Is the son of . Dart Nnlionnl bnnit property ut There Is $3,000 left of the $!'10,· Ash anrl Pnrk have been removed, Mr. unrl Mrs. J, C. Ber•grwn of 000 provided for farmer·s lo lm· The view between Ash and the Dlnmonrl road, Mnson. LJe wa~ prove land Iuken out of corn unci Mich lgan Bell building and be· Office Space Need grndualed from Mason hlgl1 Wllettt prorluctJon nnd placed In tween the Smith property and sdrool In 10·16, After 4 yeurs ol the ltcreagc reserve. Supervisors began a scrlo'us service In the nflVY he entered Parlt street Is unohstructcrl. lng-. Another solution nffcred was The money 'will compensate Bnnlt olflclals have snlcl they study of Lnnslng branch office eonstructlon of an office illlihtl'ng Mlchlgnn Slate university, recelv needs Wednesday, , lng n bachelor of sdcncc degree f;u·mcrs for tiling, liming and have 1\o Immediate plans for use at the Ingham Chest ho:->pltalsllc. -

The Automotive Sector in Pakistan

Final Report THE AUTOMOTIVE SECTOR IN PAKISTAN TABLE OF CONTENTS LIST OF ACRONYMS 1 EXECUTIVE SUMMARY 4 CHAPTER 1: INTRODUCTION 9 1.1. Terms of Reference 9 1.2. History of the Sector 10 1.3. Review of Literature 12 CHAPTER 2: THE AUTOMOTIVE SECTOR 16 2.1. Coverage 16 2.2. Sizing of the Sector 16 2.3. Contribution To The Economy 26 2.4. Demand Analysis 32 CHAPTER 3: POLICY AND REGULATORY FRAMEWORK 34 3.1. TRIMS 34 3.2. Investment Policy 36 3.3. Trade Policies 38 3.4. Tariff Policy 39 3.5. Auto Industry Development Programme 43 3.6. Policy and Standards 44 CHAPTER 4: EXTENT OF EFFECTIVE PROTECTION 45 4.1. Methodology 45 4.2. Results 46 4.3. Recommendations on Tariff Reform 47 CHAPTER 5: ASSESSMENT OF COMPETITION IN THE SECTOR 52 5.1. Methodology for Assessing Degree of Competition 52 5.2. Measure of Extent of Competition 53 5.3. Assessment of Competition in the Automotive Sector 54 CHAPTER 6: PROFILE OF THE SAMPLE OF VENDORS 58 6.1. Objectives of the Survey 58 6.2. The Sample 58 6.3. Legal Status 61 ii 6.4. Membership of Associations 61 6.5. Investment and Capacity 62 6.6. Turnover 63 6.7. Employment 63 6.8. Cost Structure 64 6.9. Gross Profit and Value Added 64 CHAPTER 7: KEY ISSUES IN THE VENDING INDUSTRY 66 7.1. Impact of Tariff Protection 66 7.2. Extent of Competition 70 7.3. Degree of Competitiveness 71 7.4. Factors Influencing Growth 71 7.5.