The Automotive Sector in Pakistan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Contacts in Japan Contacts in Asia

TheDirectoryof JapaneseAuto Manufacturers′ WbrldwidePurchaslng ● Contacts ● トOriginalEqulpment ● トOriginalEqulpment Service トAccessories トMaterials +RmR JA払NAuTOMOBILEMANUFACTURERSAssocIATION′INC. DAIHATSU CONTACTS IN JAPAN CONTACTS IN ASIA OE, Service, Accessories and Material OE Parts for Asian Plants: P.T. Astra Daihatsu Motor Daihatsu Motor Co., Ltd. JL. Gaya Motor 3/5, Sunter II, Jakarta 14350, urchasing Div. PO Box 1166 Jakarta 14011, Indonesia 1-1, Daihatsu-cho, Ikeda-shi, Phone: 62-21-651-0300 Osaka, 563-0044 Japan Fax: 62-21-651-0834 Phone: 072-754-3331 Fax: 072-751-7666 Perodua Manufacturing Sdn. Bhd. Lot 1896, Sungai Choh, Mukim Serendah, Locked Bag No.226, 48009 Rawang, Selangor Darul Ehsan, Malaysia Phone: 60-3-6092-8888 Fax: 60-3-6090-2167 1 HINO CONTACTS IN JAPAN CONTACTS IN ASIA OE, Service, Aceessories and Materials OE, Service Parts and Accessories Hino Motors, Ltd. For Indonesia Plant: Purchasing Planning Div. P.T. Hino Motors Manufacturing Indonesia 1-1, Hinodai 3-chome, Hino-shi, Kawasan Industri Kota Bukit Indah Blok D1 No.1 Tokyo 191-8660 Japan Purwakarta 41181, Phone: 042-586-5474/5481 Jawa Barat, Indonesia Fax: 042-586-5477 Phone: 0264-351-911 Fax: 0264-351-755 CONTACTS IN NORTH AMERICA For Malaysia Plant: Hino Motors (Malaysia) Sdn. Bhd. OE, Service Parts and Accessories Lot P.T. 24, Jalan 223, For America Plant: Section 51A 46100, Petaling Jaya, Hino Motors Manufacturing U.S.A., Inc. Selangor, Malaysia 290 S. Milliken Avenue Phone: 03-757-3517 Ontario, California 91761 Fax: 03-757-2235 Phone: 909-974-4850 Fax: 909-937-3480 For Thailand Plant: Hino Motors Manufacturing (Thailand)Ltd. -

Master List of DTP Participants

Institute of Business Administration, Karachi Center for Executive Education Directors' Training Program Certification Year - No Program Name Designation Organization No. Certitied CCL Pharmaceuticals 215 IBA/DTP - 0213 2019 Dr. Shahzad Khan Chief Operating Officer CCL Pharmaceuticals Pvt Ltd Pvt Ltd 216 IBA/DTP - 0214 2019 IBA-Karachi Faisal Jalal IBA Faculty IBA-Karachi 217 IBA/DTP - 0215 2019 Self Lubna Pathan Director own Business 218 IBA/DTP - 0216 2019 Indus Clean Energy Masood Hasan Khan Head of Commercial Indus Clean Energy 219 IBA/DTP - 0217 2019 Avanceon Limited Naveed Ali Baig Director Avanceon Limited Senior Executive Vice President - 220 IBA/DTP - 0218 2019 Premier Insurance Nina Afridi Premier Insurance Head of HR & Administration 221 IBA/DTP - 0219 2019 Hinopak Motors Ltd. Yoshihiko Nanami President & CEO Hinopak Motors Ltd. 222 IBA/DTP - 0220 2019 Hinopak Motors Ltd. Shigeru Tsuchiya Executive Vice President Hinopak Motors Ltd. Vice President & Director 223 IBA/DTP - 0221 2019 Hinopak Motors Ltd. Takehito Sasaki Hinopak Motors Ltd. Production Vice President & Chief Financial 224 IBA/DTP - 0222 2019 Hinopak Motors Ltd. Fahim Aijaz Sabzwari Hinopak Motors Ltd. Officer 225 IBA/DTP - 0223 2019 Hinopak Motors Ltd. Naushad Riaz Vice President Hinopak Motors Ltd. 226 IBA/DTP - 0224 2019 Hinopak Motors Ltd. Syed Samad Siraj Deputy General Manager Hinopak Motors Ltd. 227 IBA/DTP - 0225 2019 Hinopak Motors Ltd. Muhammad Zahid Hasan Deputy General Manager Hinopak Motors Ltd. 228 IBA/DTP - 0226 2019 Hinopak Motors Ltd. Ahsan Waseem Akhtar Senior Manager HR, Admin & HSE Hinopak Motors Ltd. 229 IBA/DTP - 0227 2019 Hinopak Motors Ltd. Abdul Basit Departmental Head Finance Hinopak Motors Ltd. -

Poland Regional Cities-Comfort-Vehicle-List

Make Model Year Oldsmobile 19 Oldsmobile Alero Oldsmobile Aurora Oldsmobile Bravada Oldsmobile Cutlass Supreme Oldsmobile Intrigue Oldsmobile Silhouette Dodge Attitude Dodge Avenger 2013 Dodge Caliber Dodge Caravan 2015 Dodge Challenger Dodge Charger 2013 Dodge Dakota Dodge Dart 2015 Dodge Durango 2013 Dodge Grand Caravan 2015 Dodge Intrepid Dodge JCUV Dodge Journey 2013 Dodge Magnum 2013 Dodge Neon 2015 Dodge Nitro 2013 Dodge Ram 1500 Dodge Ram 2500 Dodge Ram 3500 Dodge Ram 4500 Dodge Ram 700 Dodge Ram Van 2015 Dodge Sprinter Dodge Stratus 2015 Dodge Stretch Limo Dodge Viper Dodge Vision Dodge i10 Land Rover Defender 2013 Land Rover Discovery 2013 Land Rover Freelander 2013 Land Rover Freelander 2 Land Rover LR2 Land Rover LR3 Land Rover LR4 Land Rover Range Rover 2013 Land Rover Range Rover Evoque 2013 Land Rover Range Rover Sport 2013 Land Rover Range Rover Velar 2013 Land Rover Range Rover Vogue 2013 Chevrolet Agile Chevrolet Astra 2015 Chevrolet Astro Chevrolet Avalanche 2013 Chevrolet Aveo Chevrolet Aveo5 Chevrolet Beat Chevrolet Blazer Chevrolet Bolt Chevrolet CMV Chevrolet Camaro Chevrolet Caprice Chevrolet Captiva 2013 Chevrolet Cavalier Chevrolet Celta Chevrolet Chevy Chevrolet City Express Chevrolet Classic Chevrolet Cobalt 2015 Chevrolet Colorado Chevrolet Corsa Chevrolet Corsa Sedan Chevrolet Corsa Wagon Chevrolet Corvette Chevrolet Corvette ZR1 Chevrolet Cruze 2015 Chevrolet Cruze Sport6 Chevrolet Dmax Chevrolet Enjoy Chevrolet Epica 2013 Chevrolet Equinox 2013 Chevrolet Esteem Chevrolet Evanda 2013 Chevrolet Exclusive Chevrolet -

Hinopak Motors Limited List of Shareholders Not Provided Their Cnic S.No Folio No

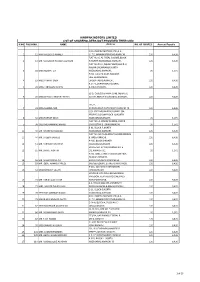

HINOPAK MOTORS LIMITED LIST OF SHAREHOLDERS NOT PROVIDED THEIR CNIC S.NO FOLIO NO. NAME Address NO. OF SHARES Amount Payable C/O HINOPAK MOTORS LTD.,D-2, 1 12 MIR MAQSOOD AHMED S.I.T.E.,MANGHOPIR ROAD,KARACHI., 120 6,426 FLAT NO. 6, AL-FAZAL SQUARE,BLOCK- 2 13 MR. MANZOOR HUSSAIN QURESHI H,NORTH NAZIMABAD,KARACHI., 120 6,426 FLAT NO.19-O, IQBAL PLAZA,BLOCK-O, NAGAN CHOWRANGI,NORTH 3 18 MISS NUSRAT ZIA NAZIMABAD,KARACHI., 20 1,071 H.NO. E-13/40,NEAR RAILWAY LINE,GHARIBABAD, 4 19 MISS FARHAT SABA LIAQUATABAD,KARACHI., 120 6,426 R.177-1,SHARIFABADFEDERAL 5 24 MISS TABASSUM NISHAT B.AREA,KARACHI., 120 6,426 52-D, Q-BLOCK,PAHAR GANJ, NEAR LAL 6 28 MISS SHAKILA ANWAR FATIMA KOTTHI,NORTH NAZIMABAD,KARACHI., 120 6,426 171/2, 7 31 MISS SAMINA NAZ AURANGABAD,NAZIMABAD,KARACHI-18. 120 6,426 C/O. SYED MUJAHID HUSSAINP-394, PEOPLES COLONYBLOCK-N, NORTH 8 32 MISS FARHAT ABIDI NAZIMABADKARACHI, 20 1,071 FLAT NO. A-3FARAZ AVENUE, BLOCK- 9 38 SYED MOHAMMAD HAMID 20GULISTAN-E-JOHARKARACHI, 20 1,071 B-91, BLOCK-P,NORTH 10 40 MR. KHURSHID MAJEED NAZIMABAD,KARACHI. 120 6,426 FLAT NO. M-45,AL-AZAM SQUARE,FEDRAL 11 44 MR. SALEEM JAWEED B. AREA,KARACHI., 120 6,426 A-485, BLOCK-DNORTH 12 51 MR. FARRUKH GHAFFAR NAZIMABADKARACHI. 120 6,426 HOUSE NO. D/401,KORANGI NO. 5 13 55 MR. SHAKIL AKHTAR 1/2,KARACHI-31. 20 1,071 H.NO. 3281, STREET NO.10,NEW FIDA HUSSAIN SHAIKHA 14 56 MR. -

Mv680491 Arizona Department of Transportation Mv579d Motor Vehicle Division 1801 West Jefferson Phoenix, Arizona 85001 May 2011

MV680491 ARIZONA DEPARTMENT OF TRANSPORTATION MV579D MOTOR VEHICLE DIVISION 1801 WEST JEFFERSON PHOENIX, ARIZONA 85001 MAY 2011 2011 LICENSED AUTOMOTIVE RECYCLER -- AR BROKER -- B DISTRIBUTOR -- DS MOBILE HOME DEALER FOR PLATES ONLY -- M MANUFACTURER -- MF NEW MOTOR VEHICLE DEALER -- N TITLE SERVICE COMPANY -- TS USED MOTOR VEHICLE DEALER -- U WHOLESALE AUCTION DEALER -- WA WHOLESALE MOTOR VEHICLE DEALER -- WD - 1- LICENSE DEALERSHIP NAME AND ADDRESS PHONE NO EXP DATE PRODUCTS AUTHORIZED TO SELL _______ ___________________________ ________ __________ ___________________________ ------ AR ------ L00000021 A A A 20TH STREET AUTO WRECKING INC 6022582020 12/31/2011 (AR112) 3244 S 40TH ST PHOENIX AZ 850401623 L00000057 A A NATIONAL TOWING AUTO PARTS 6022725331 12/31/2011 (AR165) 3410 W WASHINGTON ST PHOENIX AZ 850094705 P O BOX 42321 PHOENIX AZ 85080 L00000175 A AND S AUTO WRECKING 6022439119 12/31/2011 (AR458) 2449 W BROADWAY RD PHOENIX AZ 850412003 L00000125 A C S AUTO WRECKING ** DBA: MUNCHINO INVESTMENT INC L00000302 A TO Z AUTO RECYCLER 6022721680 12/31/2011 (AR595) 2724 W BUCKEYE RD PHOENIX AZ 850095742 L00010226 A-Z QUALITY AUTO AND TRUCK PARTS LLC 6022684558 03/31/2012 2149 W BROADWAY RD # 2 PHOENIX AZ 850412107 L00010579 A-1 TRUCK AND VAN WRECKING 4809830511 12/31/2011 1708 S TOMAHAWK RD APACHE JUNCTION AZ 851197780 7325 E NOPAL AVE MESA AZ 85209 L00008372 AA AUTO PARTS ** DBA: G S FUTURES LLC - 2- LICENSE DEALERSHIP NAME AND ADDRESS PHONE NO EXP DATE PRODUCTS AUTHORIZED TO SELL _______ ___________________________ ________ __________ -

Franchise Business in Pakistan an Analytical

i FRANCHISE BUSINESS IN PAKISTAN─AN ANALYTICAL STUDY IN SHARIAH PERSPECTIVE RESEARCH THESIS FOR PhD ISLAMIC STUDIES 1439ھ/2017ء Submitted by Supervised by GHULAM MUSTAFA DR. MUHAMMAD SAAD SIDDIQUI Roll No PhD 01-14 Professor INSTITUTE OF ISLAMIC STUDIES UNIVERSITY OF THE PUNJAB LAHORE, PAKISTAN SESSION 2014-19 ii In the name of ALLAH The Compassionate, the Merciful iii ۡ ۡ ا ۡق َرأۡۡبۡ ٱ ۡس مۡۡ َرب َكۡٱلَّ ذيۡ َخ َل َق١ۡۡۡ َخ َل َقۡٱ ۡ ۡلن ََٰس َنۡۡ م ۡنۡ َع َل ٍق٢ۡۡۡٱ ۡق َرأۡۡ َو َربُّ َكۡٱ ۡۡلَ ۡك َر مۡۡ ۡ ٣ۡۡٱلَّ ذيۡ َعلَّ َمۡبۡ ٱل َق َل م٤ۡۡۡ َعلَّ َمۡۡٱ ۡ ۡلن ََٰس َنۡۡ َماۡ َل ۡمۡيَ ۡع َل ۡم٥ۡۡ ۡ 1. Read in the name of your Lord Who created. 2. He created man from a clot. 3. Read and your Lord is most Honorable, 4. Who taught (to write) with the pen? 5. Taught man what he knew not. iv DEDICATION This work is dedicated to my very kind, affectionate, very loving, courageous and beloved parents and teachers. May ALLAH Almighty live them long and blissful. Student Name: Ghulam Mustafa Roll No: 01-14 Institute of Islãmic Studies Session: 2014-19 v CERTIFICATE The thesis: “FRANCHISE BUSINESS IN PAKISTAN-AN ANALYTICAL STUDY IN SHAIRAH PERSPECTIVE” by Ghulam Mustafa is approved in its present form by the Institute of Islãmic Studies as satisfying the thesis requirement for the degree of PhD in Islãmic Studies and it also fulfils the respective requirement of University of the Punjab and HEC. Signature of Supervisor with stamp Dr. -

05001499 007 BUP 1.Pdf

ࠗࡦ࠼ડᬺߩࠣࡠࡃ࡞ᚢ⇛ ᐕᣣ ᣣᧄ⾏ᤃᝄ⥝ᯏ᭴㧔ࠫࠚ࠻ࡠ㧕 ᶏᄖ⺞ᩏㇱ 1 ߪߓߦ ㄭᐕࠗࡦ࠼ડᬺߩࠢࡠࠬࡏ࠳M&A ߇ᵴ⊒ൻߒߡ߹ߔޕ2007 ᐕߩ࠲࠲ࠬ࠴࡞ ߦࠃࠆࠦࠬࠣ࡞ࡊ⾈ޔ2006 ᐕߩ࠼ࠢ࠲࠺ࠖࡏ࠻࠭ߦࠃࠆࡌ ࠲ࡈࠔࡓ⾈ߥߤ߇⸥ᙘߦᣂߒߣߎࠈߢߔޕߎࠇࠄߩࡔࠟ࠺ࠖ࡞એᄖߦ߽ήᢙߩ M&A ߇ⴕࠊࠇߡ߅ࠅޔࠗࡦ࠼ડᬺߪࠣࡠࡃ࡞ൻࠍㅴޔޟࠗࡦ࠼ᄙ࿖☋ડᬺޠߣߥࠅߟ ߟࠅ߹ߔޕߎࠇࠄࠗࡦ࠼ડᬺߪᦸߥࡄ࠻࠽ߦޔࠆߪᚻߏࠊ┹⋧ᚻߦߥࠅ ߃߹ߔޕᧄ⺞ᩏߩ⋡⊛ߪޔߎ߁ߒߚਥⷐࠗࡦ࠼ડᬺߩၮᧄᖱႎ߿ߘߩᶏᄖᚢ⇛ࠍᢛℂߔࠆ ߎߣߢޔᣣᧄડᬺߩෳ⠨ߣߥࠆ⾗ᢱࠍឭଏߔࠆߎߣߦࠅ߹ߔޕ ߹ߚޔࠫࠚ࠻ࡠߢߪޔㅜޔ☨࿖ડᬺߩࠗࡦ࠼ะߌࠝࡈ࡚ࠪࠕࡦࠣ⺞ᩏࠍታᣉߒߡ ߹ߔޕᧄ⺞ᩏߪޔߎࠇߣ㑐ㅪߒߡޔࠗࡦ࠼߳ߩࠝࡈ࡚ࠪࠕࡦࠣޔ․ߦ⍮⼂㓸⚂⊛ߥᬺോ ࠍኻ⽎ߣߔࠆ࠽࠶ࠫࡊࡠࠬࠕ࠙࠻࠰ࠪࡦࠣ㧔KPO㧕ࠍ⥄りߢታ〣ߒޔߘߩ⚿ᨐ ࠍࠝࡈ࡚ࠪࠕࡦࠣ⺞ᩏႎ๔ᦠߦᵴ߆ߔࠃ߁ߦ⸘↹ߒߚ߽ߩߢ߽ࠅ߹ߔޕౕ⊛ߦߪޔ ࠫࠚ࠻ࡠߪ⺞ᩏߩડ↹߅ࠃ߮ࡊࡠࠫࠚࠢ࠻ࡑࡀࠫࡔࡦ࠻ߩߺࠍⴕޔߢߩ⺞ᩏߪో 㕙⊛ߦࠗࡦ࠼ߩ⺞ᩏડᬺࠗࡃࡘࠨࡉߦࠕ࠙࠻࠰ࠬߒ߹ߒߚޕ ޟࠗࡦ࠼ડᬺߩᶏᄖᚢ⇛ޠ⺞ᩏࡊࡠࠫࠚࠢ࠻ߩ-21ࡢࠢࡈࡠ ട╩䊶ୃᱜ ᦨ⚳ႎ๔ᦠ䈱ฃข ᦨ⚳ႎ๔ᦠ䈱⚊ ᦨ⚳ ਇὐ䈱⏕ൻ ႎ๔ ᦨ⚳⏕ ⠡⸶ቢੌ ⋙⸶䇮⸶䈮䈧䈇䈩 ੑ㊀䉼䉢䉾䉪 䊐䉞䊷䊄䊋䉾䉪 ౝኈ䈱⏕ൻ ౝኈ䈱ਇὐ䉕⏕ ⠡⸶ ᣣᧄ⺆⠡⸶ ⠡⸶㐿ᆎ䉕ᜰ␜ ⠡⸶䉕㐿ᆎ 㐿ᆎ䉕ᜰ␜ ⧷ᢥ䈪䈱 ᦨ⚳ႎ๔ ⧷ᢥਛ㑆ႎ๔ ⧷ᢥ䈪䈱 䈱䊐䉞䊷䊄䊋䉾䉪䇮 ਛ㑆ႎ๔ ਇὐ䈱⏕ൻ ⺞ᩏ ታᣉ ⺞ᩏታᣉ 䊒䊨䉳䉢䉪䊃䊶 䊙䊈䊷䉳䊞䊷 ⺞ᩏ⸳⸘วᗧ 䊶⺞ᩏ⸳⸘䈱ឭ᩺ 䉝䊅䊥䉴䊃 䊶ⷐઙቯ⟵䈱⏕ ⸘↹ 䊶䊒䊨䉳䉢䉪䊃䊶䉼䊷䊛 䊶⺞ᩏડ↹┙᩺ 䇭䈱ㆬቯ 䊶ⷐઙቯ⟵ ⠡⸶ᜂᒰ 䉳䉢䊃䊨䋨᧲੩䋩 䉟䊋䊥䊠䉰䊷䊑㩿䊆䊠䊷䊂䊥䊷䋩 䉟䊋䊥䊠䉰䊷䊑䋨ᶏ䋩 2 ࠝࡈ࡚ࠪࠕࡦࠣታ〣ߩᚑᨐߪޔޟࠗࡦ࠼ࠝࡈ࡚ࠪࠕࡦࠣޠ㧔ࠫࠚ࠻ࡠೀ㧕ࠍߏⷩߊ ߛߐޕ߹ߚޔࠫࠚ࠻ࡠߩ࠙ࠚࡉࠨࠗ࠻㧔ർ☨ߩ⺞ᩏࡐ࠻㧦 http://www.jetro.go.jp/biz/world/n_america/reports/㧕ߦޔᧄ⺞ᩏߩ⧷⺆ ႎ๔ᦠࠍឝタߒߡ ߅ࠅ߹ߔޕ ᧄᦠߪޔࠗࡃࡘࠨࡉ␠߆ࠄฃ㗔ߒߚႎ๔ᦠߦޔࠫࠚ࠻ࡠߦߡട╩ୃᱜࠍട߃ߡ߅ࠅ ߹ߔ߇ޔౝኈߩᱜ⏕ᕈߦߟߡߪޔၮᧄ⊛ߦᆔ⸤ߒߚࠗࡦ࠼ߩ⺞ᩏડᬺࠗࡃࡘࠨࡉߩ ⺞ᩏ⢻ജߦଐߞߡ߹ߔޕ ߹ߚޔᧄᦠࠍߏⷩߚߛߊߦߚߞߡߪޔԘᧄᢥਛߢ↪ߒߡࠆ࠺࠲߿ታ㑐ଥߪ ା㗬ߢ߈ࠆߣᕁࠊࠇࠆฦ⒳ᖱႎߦၮߠߡࠆ߽ߩߩޔߘߩᱜ⏕ᕈޔቢోᕈߦߟߡޔࠫ ࠚ࠻ࡠޔࠗࡃࡘࠨࡉߣ߽⸽ࠍߔࠆ߽ߩߢߪߥߎߣޔԙࠫࠚ࠻ࡠߪᧄႎ๔ߩ⺰ᣦߣ ৻⥌ߒߥઁߩ⾗ᢱࠍ⊒ⴕߒߡࠆޔࠆߪᓟ⊒ⴕߔࠆ႐ว߽ࠆߎߣޔԚᧄႎ๔ߪ ⺒⠪ߩᣇޘ߳ߩᖱႎឭଏࠍ⋡⊛ߣߒߚ߽ߩߢࠅޔ․ቯߩᛩ⾗್ᢿࠍଦߔ߽ߩߢߪߥߊޔ ႎ๔ᦠߩౝኈࠍෳ⠨ߦߒߡⴕࠊࠇߚ⚻ᷣⴕὑߩ⚿ᨐߦኻߒߡࠫࠚ࠻ࡠ߅ࠃ߮ࠗࡃࡘࠨ ࡉߪ⽿છࠍ⽶ࠊߥߎߣޔߦߟߡޔߏੌ⸃߅㗿⥌ߒ߹ߔޕ ᧄᦠ߇⥝㓉ߒᆎߚࠗࡦ࠼ડᬺ߳ߩℂ⸃ࠍᷓࠃ߁ߣߐࠇࠆࡆࠫࡀࠬࡄࠬࡦࠍߪߓ ޔߏ㑐ᔃࠍ㗂ߚᣇߦޔዋߒߢ߽߅ᓎߦ┙ߡ߫ᐘߢߔޕ ᣣᧄ⾏ᤃᝄ⥝ᯏ᭴ ᶏᄖ⺞ᩏㇱ ࡊࡠࠫࠚࠢ࠻ᜂᒰ⠪৻ⷩ ᣣᧄ⾏ᤃᝄ⥝ᯏ᭴ ᶏᄖ⺞ᩏㇱ ർ☨⺖㧔ડ↹ో⛔㧕 ડ↹✬㓸㧦 ㋈ᧁ ᣣᧄࡊࡠࠫࠚࠢ࠻ࡑࡀࠫࡖ㧦 ↰ਛિ ⋙⸶㧦 㒙ㇱᄙᤋሶ ࠗࡃࡘࠨࡉ ࠗࡦ࠼࠴ࡓ㧔⺞ᩏᜂᒰ㧕 ࡊࠫࠚࠢ࠻⛔㧦 ࠕࠪࡘࠪࡘࠣࡊ࠲㧔Ashish Gupta㧕 ࠗࡦ࠼ࡊࡠࠫࠚࠢ࠻ࡑࡀࠫࡖ㧦 ࠕࠫࠚࠗࡧࠔࠪࡘ࠾㧔Ajay Varshney㧕 ⺞ᩏᜂᒰ㧦 ࠕࡆ࠽ࡉࡊࡠࡅ࠻㧔Abhinav Purohit㧕 ⺞ᩏᜂᒰ㧦 ࠕࠞࠪࡘࠢࡑ࡞ࠫࠚࠗࡦ㧔Akash Kumar Jain㧕 ⺞ᩏᜂᒰ㧦 ࠕࡒ࠲ࠞ࡞㧔Amita Kalra㧕 ਛ࿖࠴ࡓ 㧔⠡⸶ᜂᒰ㧕 ⠡⸶ᬺ⛔㧦ࠛ࠼ࡢ࠼Aࠕ࠳ࡓࠬࠠ㧔Edward A. -

India-Pakistan Trade: Perspectives from the Automobile Sector in Pakistan

Working Paper 293 India-Pakistan Trade: Perspectives from the Automobile Sector in Pakistan Vaqar Ahmed Samavia Batool January 2015 1 INDIAN COUNCIL FOR RESEARCH ON INTERNATIONAL ECONOMIC RELATIONS Table of Contents List of Abbreviations ................................................................................................................... iii Abstract ......................................................................................................................................... iv 1. Introduction ........................................................................................................................... 1 2. Methodology and Data .......................................................................................................... 2 3. Automobile Industry in Pakistan ......................................................................................... 3 3.1 Evolution and Key Players............................................................................................ 4 3.2 Structure of the Industry ............................................................................................... 6 3.3 Production structure ..................................................................................................... 7 3.4 Market Structure ........................................................................................................... 8 4. Automobile Trade of Pakistan............................................................................................ 10 4.1 Import -

Financial Analysis of Toyota Indus Motor Company

Financial Analysis of Toyota Indus Motor Company 2017 Financial Analysis of Toyota Indus Motor Company Financial Year 2011-2016 Ayesha Majid Lahore School of economics 5/1/2017 Financial Analysis of Toyota Indus Motor Company i Table of Contents Preamble .................................................................................................................... 1 Categories of Financial Ratios Analysed ................................................................ 1 Limitations .............................................................................................................. 2 Toyota Indus Motors................................................................................................... 3 Company Profile ..................................................................................................... 3 Financial Profile ...................................................................................................... 3 Introduction ............................................................................................................. 4 Mission Statement ............................................................................................... 5 Vision Statement ................................................................................................. 5 Slogan ................................................................................................................. 5 Quote Summary as on 1st May 2017 .......................................................................... 6 -

Annual 2012.Pdf

A View of Baluchistan Wheels Limited Vision Mission To Produce Automotive Wheels and Allied Products of International Quality Standard of ISO 9002 and contribute towards national economy by import substitution, exports, taxation, employment and consistently compensate the stake holders through stable returns. BALUCHISTAN WHEELS LIMITED Table of Contents Corporate Information 04 Notice of the Meeting 06 Our Leadership Team 08 Directors Report to the Shareholders 10 Pattern of Shareholding 16 Breakup of Shareholding 17 Statement of Compliance with the Code of 19 Corporate Governance Statement of Compliance with the 21 Best Practices on Transfer Pricing Review Report to the Members on Statement 22 of Compliance with the Best Practices of the Code of Corporate Governance Auditors Report 23 Balance Sheet 24 Profit and Loss Account 25 Statement of Comprehensive Income 26 Cash Flow Statement 27 Statement of Changes in Equity 28 Notes to the Financial Statements 29 Six years at a Glance 53 Form of Proxy New Induction of CO2 Welding New Induction of Automobile Disc profile Forming Machine by Spinning Process BALUCHISTAN WHEELS LIMITED Corporate Information Mr. Muhammad Siddique Misri Mr. Razak H. M. Bengali Mr. Muhammad Irfan Ghani Chairman Chief Executive Chief Operating Officer BOARD OF DIRECTORS Mr.Muhammad Siddique Misri Chairman(Executive Director) Mr.Razak H.M.Bengali Chief Executive(Executive Director) Mr. Muhammad Irfan Ghani Chief Operating Officer(Executive Director) Syed Haroon Rashid Director (Nominee - NIT)(Non Executive Director) Syed Zubair Ahmed Shah Director (Nominee - NIT)(Non Executive Director) Mr.Muhammad Javed Director(Executive Director) Mr.Irfan Ahmed Qureshi Director(Executive Director) COMPANY SECRETARY Mr.Irfan Ahmed Qureshi BOARD AUDIT COMMITTEE Syed Haroon Rashid - Chairman Director Syed Zubair Ahmed Shah- Member Director Mr. -

Monthly Magazine

Issue 6, January 2007 With circulation of over 31,000+ copies every month Monthly Magazine Pakistan Rs. 50 U.A.E. AED 5 International US$ 5 )NTERVIEWWITH 'ET TOGETHERS (YUNDAI$EWAN-OTORS 3POTTED %XPLAINING#64 (OW2ADIATORS7ORK www.pakwheels.com January 2007 www.pakwheels.com January 2007 www.pakwheels.com January 2007 safaa.u.t.o.m.o.b.i.l.e.s Deals in all kinds of New and Used Automobiles R 111/2, Khalid Bin Walid Road, Block 2, P.E.C.H.S. Karachi. Ph: 4529256, 4388788, 4388799 Fax: 4559642 E-mail: [email protected] www.pakwheels.com January 2007 www.pakwheels.com January 2007 3)2%.(/2.3%2)%3 !,!2-,)'(43%2)%3 ,)'(4"!23%2)%3 Editors Note FASCOMCOM % MAILAUTOLINE &AX #ELL 4EL -!*INNAH2OAD +ARACHI ' 2IMPA0LAZA (EAD/FFICE ,%$LIGHT Editor #ARELECTRONICHORN Well, well this time with the celebrations of New Year we’ve tweaked our traditional cover story from wheels into wheels! YES, Superbikes is ,%$ what we have featured this month, though most of them are stock but still hell fast. This issue, along with our usual stuff, we did an interview Jag 8$ ! with Hyundai Dewan Motors CEO and MD so make sure you have a look at it. 5LTRA THINREVOLVINGLIGHTBAR To fill the missing gap we have included quite a few more short articles for your reading pleasure for which we have been receiving Associate Editor complains that there are too less of articles – also a regular review of Imported Toyota Corolla can be found on page 0! Sania Zafar 4"$ '! $ 3TREETEAGLE,%$LIGHTBAR Usually December is a slow monthly mainly due to end of the year with Christmas & Eid coming up. -

Infomation for SECP Till Nov 2020.Xlsx

Information required for the SECP notice DTP 1 Lahore List of Certified Directors Session I: Jan 21-22, 2013 - Session II: Mar 25-26, 2013 S.NO Name of Participant Designation Organization Area of Expertise 1 Ali Altaf Saleem Executive Director Shakarganj Mills Ltd Finance 2 Abdul Rafay Siddique, FCA - Abdul Rafay, Chartered Accountants Accounting & Finance 3 Mohammad Saleem, FCA Partner M. Yousuf Adil Saleem & Co. Audit/Finance/Corporate Affairs/Taxation Business Analysis, Internal Control Risks, Risk Mitigation, Strategic Planning, Business 4 Omer Naseer Risk Analyst InfoTech Private Ltd Management Director Finance & CFO's responsibilities,Looking after Operations of the company especially Production, Safety and 5 Javed Iqbal, FCA Ittehad Chemicals Ltd. CFO Environment, CSR Contracts Management/ interpretation/ (Power Purchase Agreement, Implementation Agreement, 6 Zain-Ul-Abidin, FCA Chief Financial Officer Japan Power Generation Ltd. O&M Agreements) 7 Muneeb Ahmed Dar Director/Chairman First Elite Capital Mudaraba Credit/ Risk Management Chief Executive 8 Shafqat Ellahi Shaikh Ellcot Spinning Mills Ltd/Nagina Group Entrepreneur Officer 9 Muhammad Rizwan Akbar, FCA Chief Financial Officer The Lake City Holdings (Pvt) Ltd. Finance, Audit, Tax and Management. 10 Asif Baig Mirza Director Lahore Stock Exchange Ltd. Financial Management and Economic Analysis 11 Sultan Mubashir, FCA Executive Director Ellcot Spinning Mills Ltd/Nagina Group Financial reporting, Treasury, Corporate &Taxation and Organisation Management 12 Bushra Naz Malik, FCA Director Lahore Stock Exchange Ltd. Governance and Risk Management Have over 29 Years of Post Qualification Experience in diversified fields of Finance, Corporate 13 Waqar Ullah, FCA Director Finance Tariq Glass Industries Ltd. Affairs, Taxation and Allied Matters 14 Naseer A.